DBSDF - DBS Group: Upbeat Mid-Term Outlook Outweighs Near-Term Headwinds

2023-06-07 06:18:40 ET

Summary

- DBS outlined the path to structurally higher mid-term ROEs at its investor day this year.

- The capital position is also set to move lower, unlocking capital return upside.

- With DBS stock trading at undemanding levels relative to its high-teens % ROE potential, the stock offers compelling value.

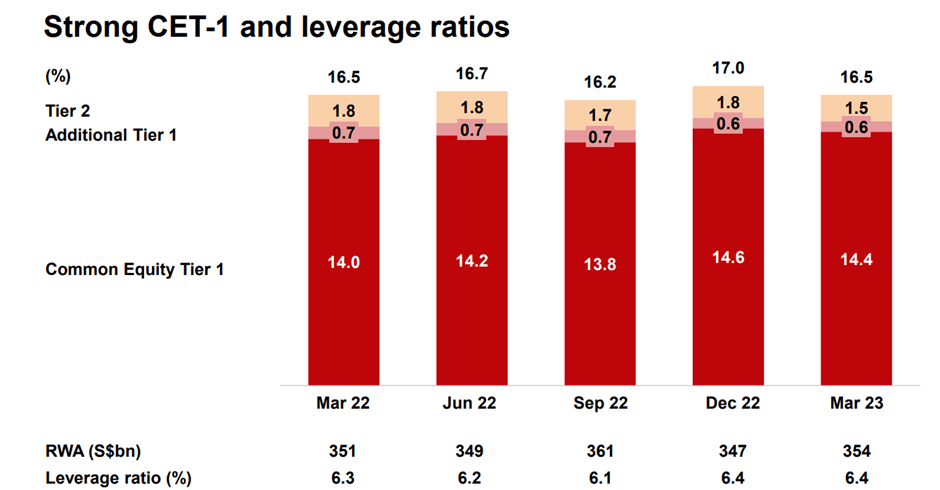

DBS Group ( OTCPK:DBSDF ) management kicked off this year’s investor day with a bullish mid-term ROE target range of 15-17% (vs. 15.0% in 2022), providing some much-needed optimism after revising down its 2023 guidance for loans growth, net interest margins ((NIM)), and fee income in Q1. While the near-term outlook isn’t great, there are silver linings. For one, the NIM downside is limited at 2.05-2.10% for year-end (vs. 2.12% in Q1). And even with the sharp interest rate hikes, asset quality is pristine - DBS has seen no stress within its loan book, with management conservatively maintaining sizeable allowances on top of a robust capital position (14.4% CET-1 in Q1). Supported by S$3bn of excess capital (based on management’s lowered CET-1 operating range), the guidance for a baseline dividend increase by 24c/year over the mid-term seems well within reach. And with ample room for further distribution upside via higher ordinary dividends, specials, or buybacks, I wouldn’t rule out upward revisions from here. Bank valuations tend to compress ahead of a rate cut cycle, but with DBS stock already de-rated to an undemanding ~1.4x P/Book, the downside seems limited heading into a potential H2 pivot.

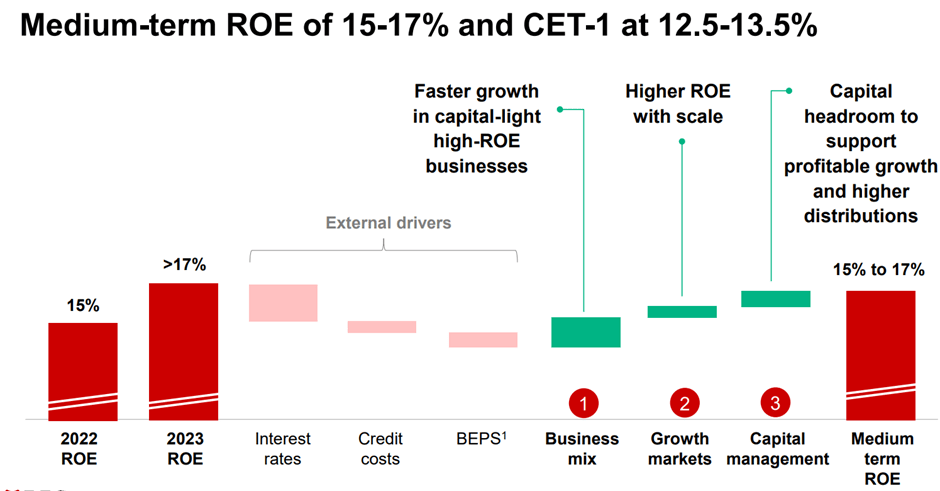

Mid-Term ROE Target Range Gets an Uplift to 15-17%

This year’s tech-focused DBS investor day was the first since the 2017 ‘digital’ update, highlighting the bank’s key achievements in recent years in building up its tech capabilities. Highlights include its data platform (now a competitive differentiator vs. peers) and effective portfolio risk management, both of which have unlocked new growth opportunities in different markets. The bank's tech initiatives have also been a key driver of the significant ROE uplift across its consumer and small/medium enterprise segments, as well as fee-earnings businesses. Some of the ~3.8%pts ROE uplift (to 15% in 2022) is down to cyclical factors like higher rates, though the majority is attributable to structural drivers such as the foreign currency-led expansion of its deposit franchise (+1.6%pts) and growth in high-ROE fee income businesses (+0.6%pts), along with improvements in its credit risk management (+0.3%pts).

{kind=link}

DBS Group

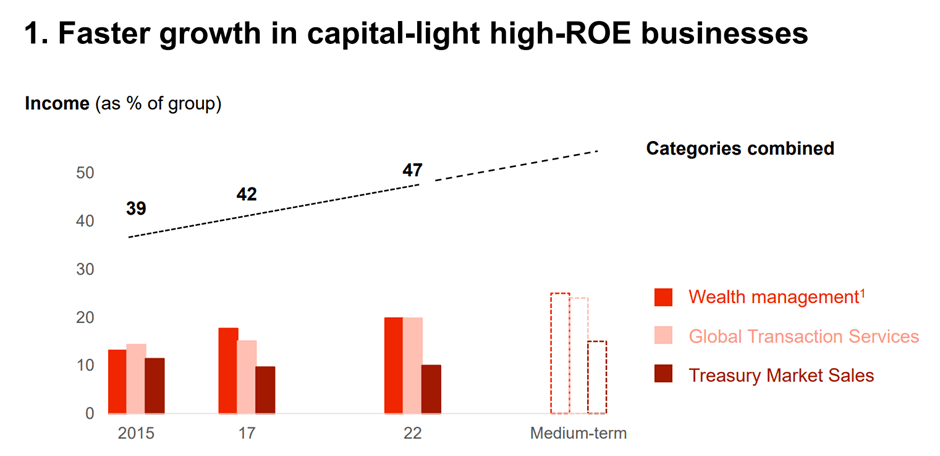

From here, DBS expects further ROE expansion to a 15-17% range – an up to 2%pts increase from 2022 levels but down from the 18.6% peak in Q1. While ‘higher for longer’ expected interest rates (albeit down from the Q1 peak) will play a key role, management expects growth in capital-light, high ROE businesses (e.g., wealth management, transaction services, and treasury sales) to contribute to the largest delta. Elsewhere, DBS has also penciled in contributions from new markets like India, Indonesia, and Taiwan, where the growth opportunities remain untapped. Of the three, India will be one to watch post-acquisition of Lakshmi Vilas Bank , which affords DBS a physical base to expand its addressable market. The India franchise ROE is also currently running at ~5% ROE in 2022, well below the high-teens % of industry leaders like HDFC Bank ( HDB ) and ICICI ( IBN ), and at the current high-single-digit % growth (off a low base), there remains ample runway for DBS to outgrow the broader market. Backed by a strong excess capital position, M&A presents incremental upside to the guidance, with the focus likely on the digital side for its core markets and on building a larger physical footprint for its emerging growth markets.

{kind=link}

DBS Group

A Robust Capital Position Ensures Through-Cycle Resilience

On the capital side, DBS is targeting its CET-1 ratio within a 12.5-13.5% range, well below the >14% in Q1. This makes sense as we enter a rate-cut cycle, where portfolio stress should ease. Property values in Singapore have also held up well so far despite property in other developed markets (mainly Europe) already under pressure from the rate headwinds; hence, any default risks on its real estate-backed loan book should be well contained. Management also sees asset quality remaining intact (based on portfolio stress-testing) through a recession, hence the comfort in lowering their capital ratio targets. Where the bank could feel a near-term hit is on the P&L side, as a recession in Singapore could pressure NIMs via higher credit costs. With the market also pricing in a rate cut pivot in H2, the downward revisions to NIMs (2.05-2.1%) and loan growth (3-5%) in Q1 seem prudent.

{kind=link}

DBS Group

The good news is that a target CET-1 operating range of 12.5-13.5% leaves the bank with ~S$3bn of excess capital to work with. A bigger headroom means more distribution upside in the coming years, with a step up in the ordinary dividend, the most likely scenario, followed by special dividends and buybacks. Per management, a base case scenario would see the ordinary dividend per share raised by S$0.24 per year in the mid-term, implying a ~7% yield based on the current stock price. While this also implies a higher payout at ~60% (vs. ~50% historically), the strong balance sheet should ensure any distribution is well-covered.

Upbeat Mid-Term Outlook Outweighs Near-Term Headwinds

With management committing to bullish mid-term ROE targets of 15-17% and 12.5-13.5% CET-1 at its latest investor day, DBS appears poised for more upside after the disappointment of its downward guidance revision in Q1. The near-term hurdles remain, though, with the central bank moving towards a likely rate cut pivot later this year, implying NIM downside potentially beyond the full-year target of 2.05-2.10%. In contrast with the margin concerns, DBS’ loan book has seen limited stress through this rate hike cycle; alongside the bank’s substantial allowances and capital position, asset quality shouldn’t be an issue as rates move lower from here.

As for the dividends (current baseline guidance for a 24c/year increase), the S$3bn excess capital position (assuming the bank’s optimal CET-1 operating range) entails further upside to the distribution – if not via higher ordinary dividends, special dividends, and share buybacks are additional options. At ~1.4x P/Book, there’s a lot to like on the valuation as well, with DBS screening cheaply by historical standards and relative to its high-teens % ROE potential.

For further details see:

DBS Group: Upbeat Mid-Term Outlook Outweighs Near-Term Headwinds