BSJQ - DCF: Locking In High Returns With Fixed Term Closed-End Bond Funds

2023-07-26 11:48:43 ET

Summary

- The BNY Mellon Alcentra Global Credit Income 2024 Target Term Fund Inc. (DCF) is a fixed term closed-end credit fund with a December 2024 maturity.

- The DCF fund is currently trading at a 5.3% discount to NAV, and its portfolio is estimated to be trading at a 3% discount to par.

- Combining with the fund's 5.5% distribution, investors may be able to 'lock in' 7-9% forward returns assuming normalized credit losses.

A few weeks ago, I penned a bullish article on the Invesco BulletShares 2026 High Yield Corporate Bond ETF ( BSJQ ), arguing investors may be able to lock in an attractive 6%+ forward return on the BSJQ ETF, given high yield bonds are trading with equity-like returns.

This article looks at the BNY Mellon Alcentra Global Credit Income 2024 Target Term Fund Inc. ( DCF ), which may offer an even more attractive forward return, albeit in a shorter-term fund.

The DCF fund is a fixed-maturity closed-end fund that primarily invests in high yield bonds, senior loans, and structured credit investments. With a portfolio of securities trading at a discount to par and the portfolio trading at a discount to NAV, investors may be able to lock in an attractive annualized 7-9% forward return to December 2024. I rate DCF a buy.

Fund Overview

The BNY Mellon Alcentra Global Credit Income 2024 Target Term Fund Inc. ((DCF)) is a closed-end credit fund with a maturity date of December 1, 2024. The DCF fund invests in high yield bonds, leveraged loans, and structured credit investments.

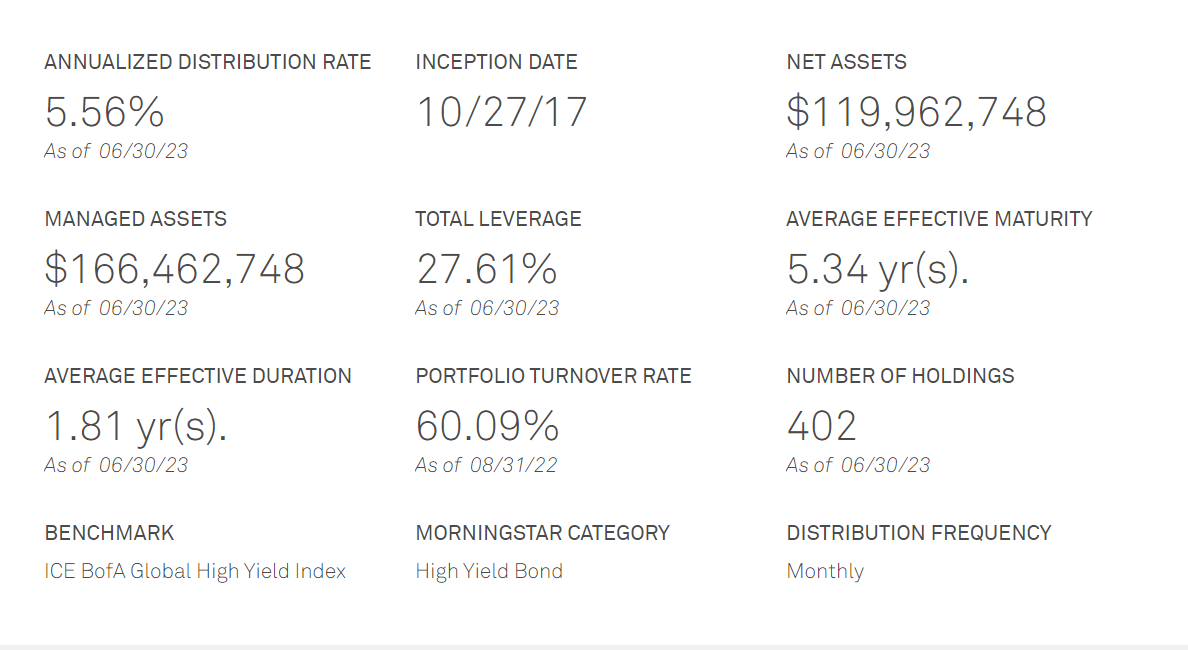

The DCF fund has $120 million in net assets and charges a 2.42% total expense ratio (Figure 1). The DCF fund employs leverage to enhance returns and has 27.6% effective leverage as of June 30, 2023.

{kind=link}

Portfolio Holdings

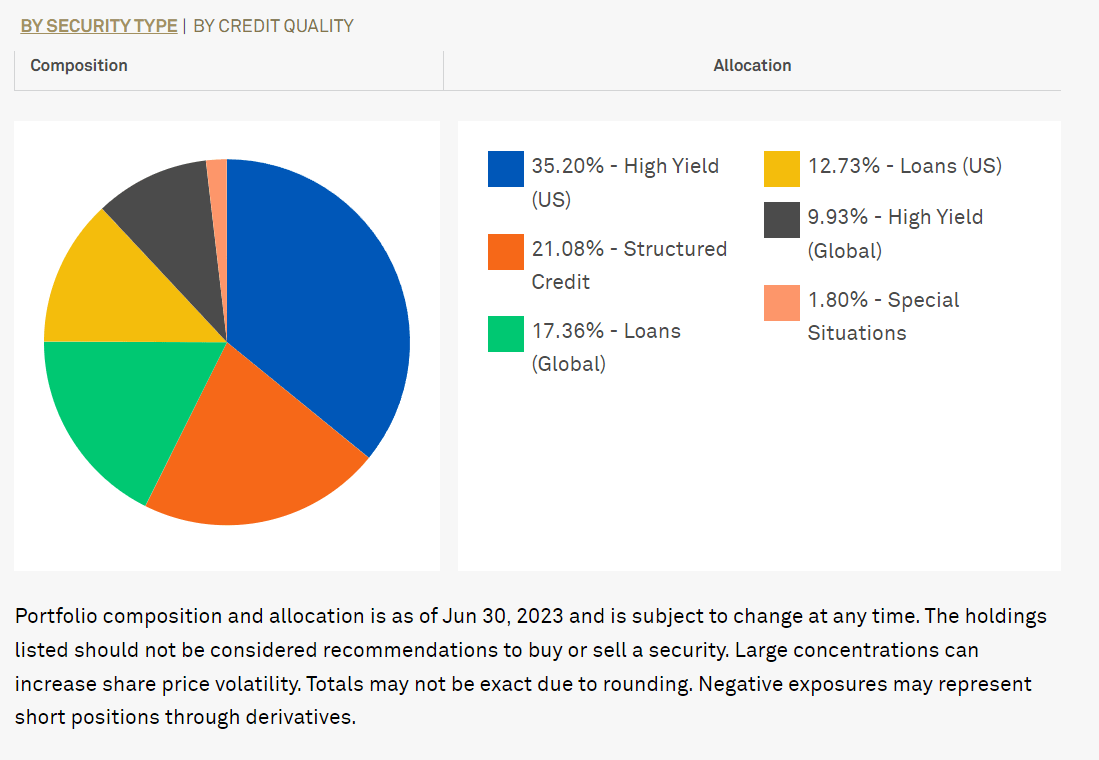

From figure 1 above, we can see DCF's portfolio has an average effective duration of 1.8 years. Figure 2 shows the current sector allocation of the DCF fund. The biggest sector weights are in U.S. high yield (35.2%), structured credit (21.1%), global loans (17.4%), U.S. loans (12.7%), and global high yield (9.9%).

{kind=link}

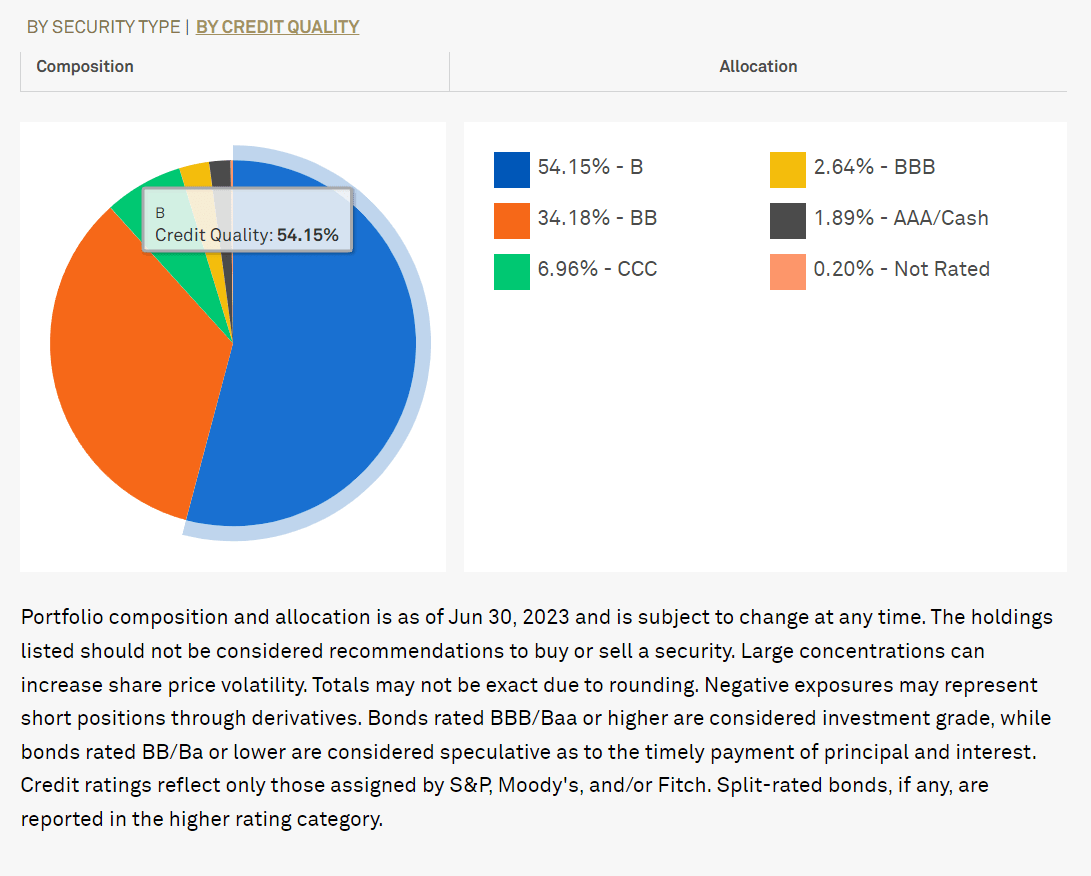

Credit ratings in the DCF fund are primarily non-investment grade, with B-rated (54.2%) and BB-rated (34.2%) being the largest allocations (Figure 3).

Figure 3 - DCF fund credit quality allocation (bnymellon.com)

{kind=link}

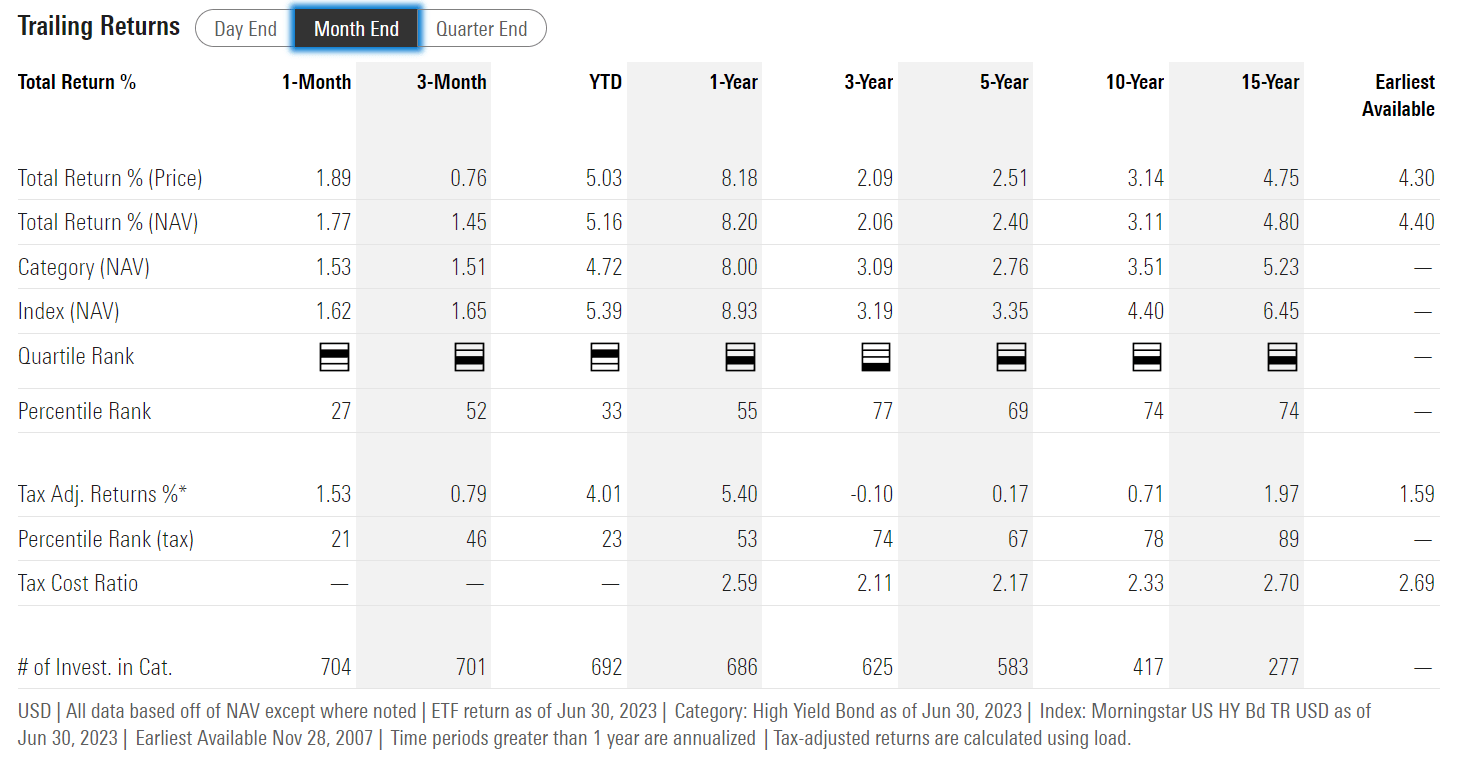

Returns

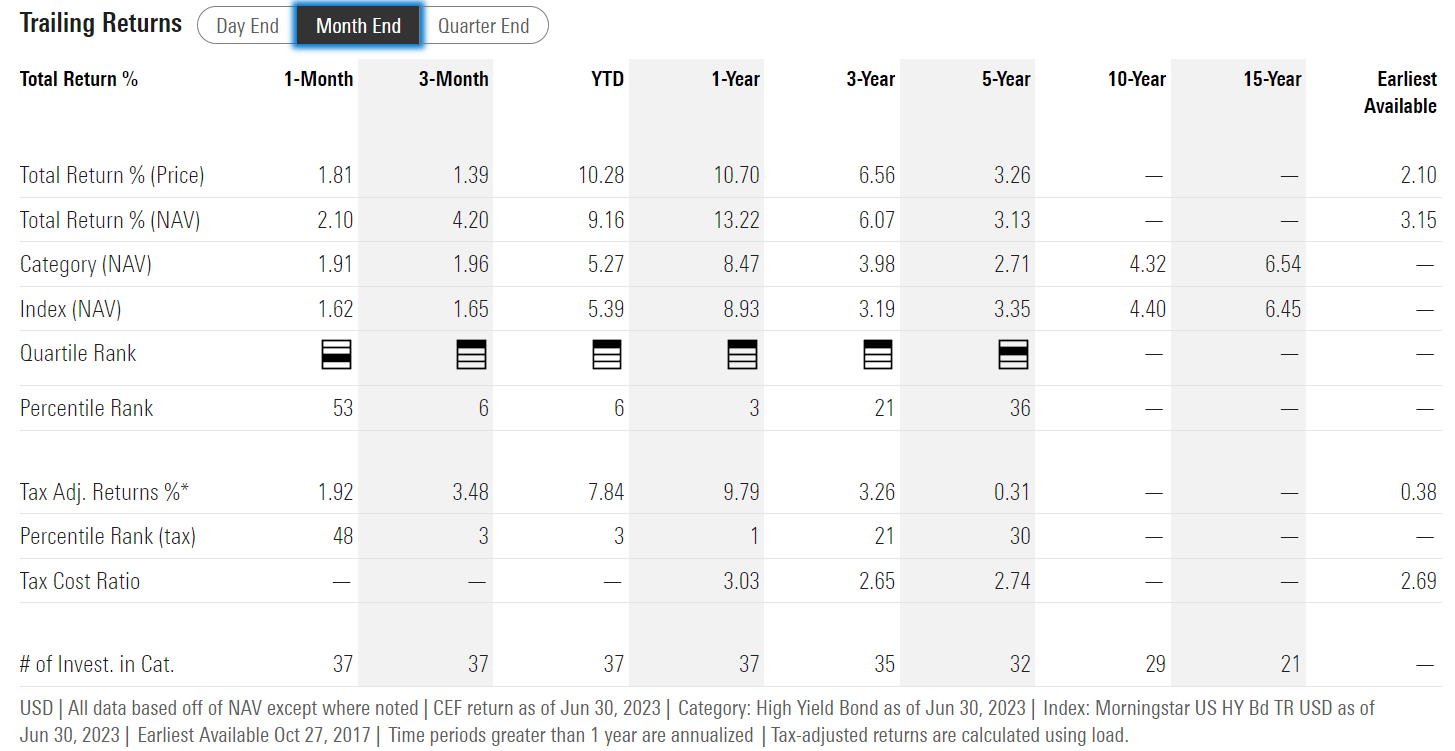

Figure 4 shows the historical returns for the DCF. Returns for the DCF fund have been decent, with 1/3/5Yr average annual returns of 13.2%, 6.1% and 3.1% respectively to June 30, 2023.

{kind=link}

Furthermore, DCF's return has been better than a passive high yield index fund like the SPDR Bloomberg High Yield Bond Fund ( JNK ), which has only returned 8.2%, 2.1%, and 2.4% respectively in the same timeframes.

{kind=link}

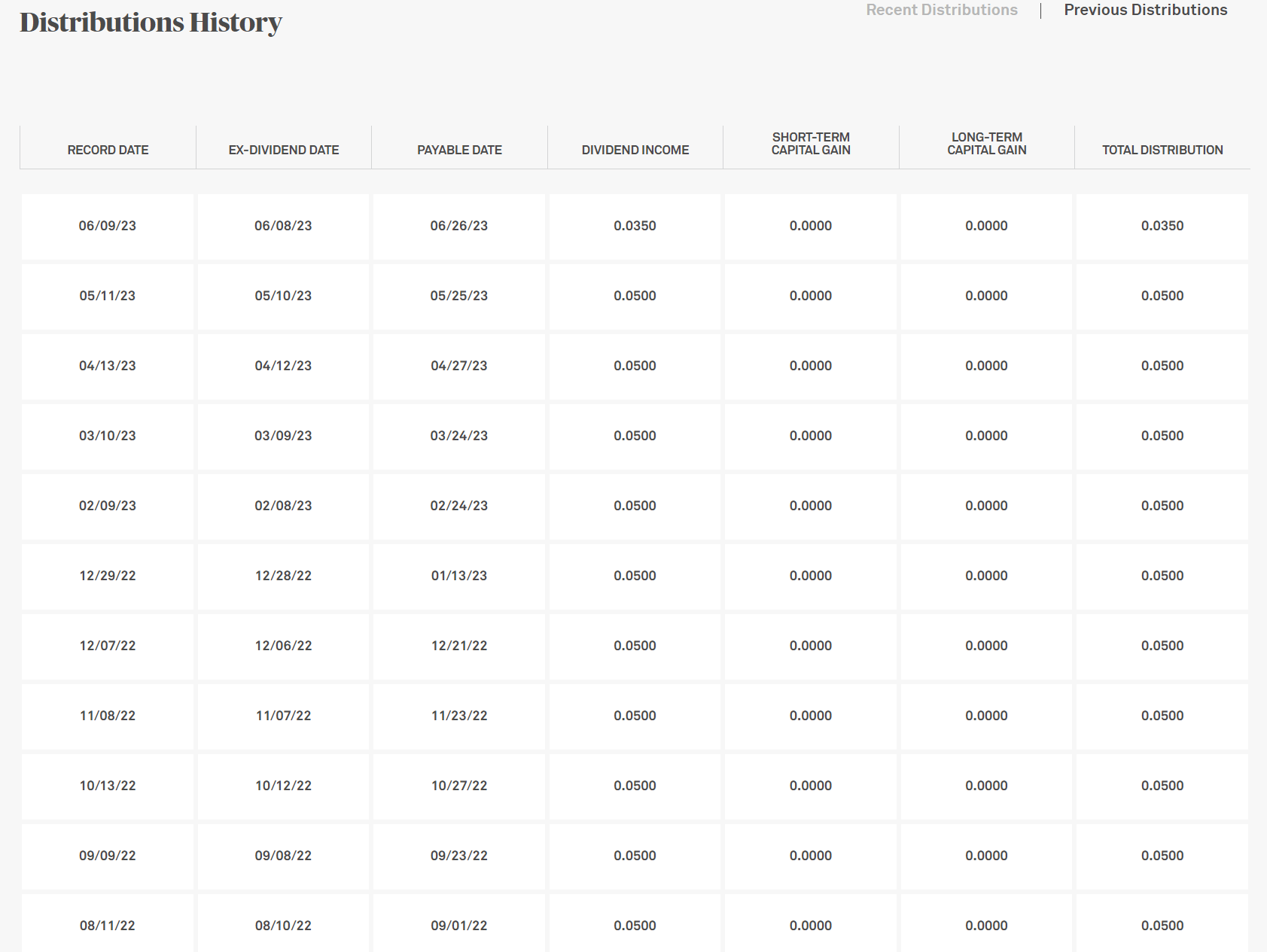

Distribution & Yield

Currently, the DCF fund is paying a monthly distribution of $0.035 / share, or a forward yield of 5.5% on market price and 5.2% on NAV. DCF's monthly distribution was recently cut from $0.05 / month. (Figure 6).

{kind=link}

DCF's distribution appears well covered, as the fund's portfolio has a 30-Day SEC yield of 9.8% (Figure 7).

{kind=link}

Another way to think about the sustainability of DCF's distribution is to compare the fund's average annual returns of 6.1% over 3 years vs. the fund's distribution yield of 5.2% of NAV. Since the fund's average returns are higher than its distribution yield, there should be no concern on the distribution sustainability.

Portfolio Holdings At A Discount To Par

Also, with a portfolio yield of 9.8% compared to weighted average coupon of 7.75% for the DCF fund, it appears the average security within DCF's portfolio is trading at an estimated ~3% discount to par (this is estimated using NPV = discounted cash flow of 7.75% coupon at 9.8% interest rate for 1.5 years) (Figure 8).

Figure 8 - DCF's weighted average coupon is 7.75% (DCF factsheet)

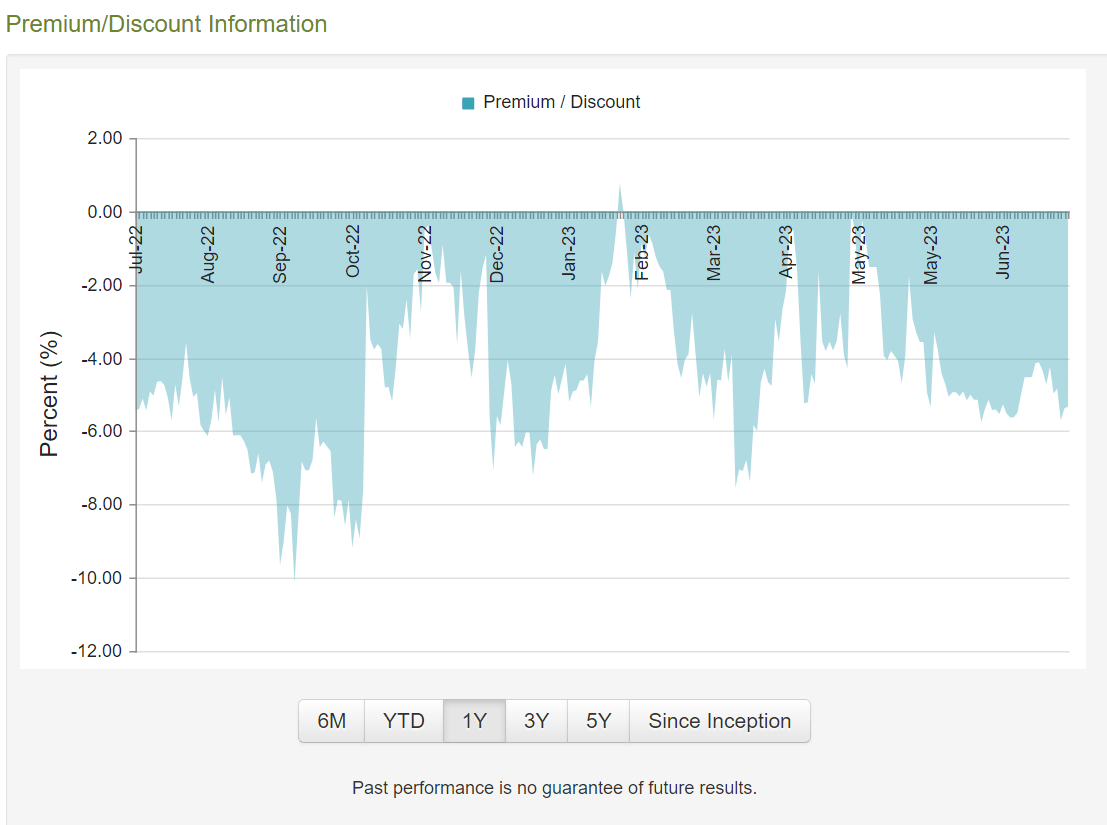

DCF Fund Trading At A Discount To NAV

In addition to holding discounted securities, the DCF fund itself is trading at a 5.3% discount to NAV (Figure 9).

Figure 9 - DCF trades at a 5.3% discount to NAV (cefconnect.com)

{kind=link}

Investors May Be Able To Lock In ~7-9% Return

With the DCF fund currently trading at a 5.3% discount to NAV, assuming there are no defaults within DCF's portfolio, investors buying the fund today may be able to earn a ~11% annualized forward return over the next 18 months. This is calculated as 5.5% from the distribution yield, 3.5% from the discount to NAV closing at maturity in December 2024 (5.3% / 1.5 years), and 2% from the fund's discounted holdings accreting to par at maturity in December 2024 (3% / 1.5 years).

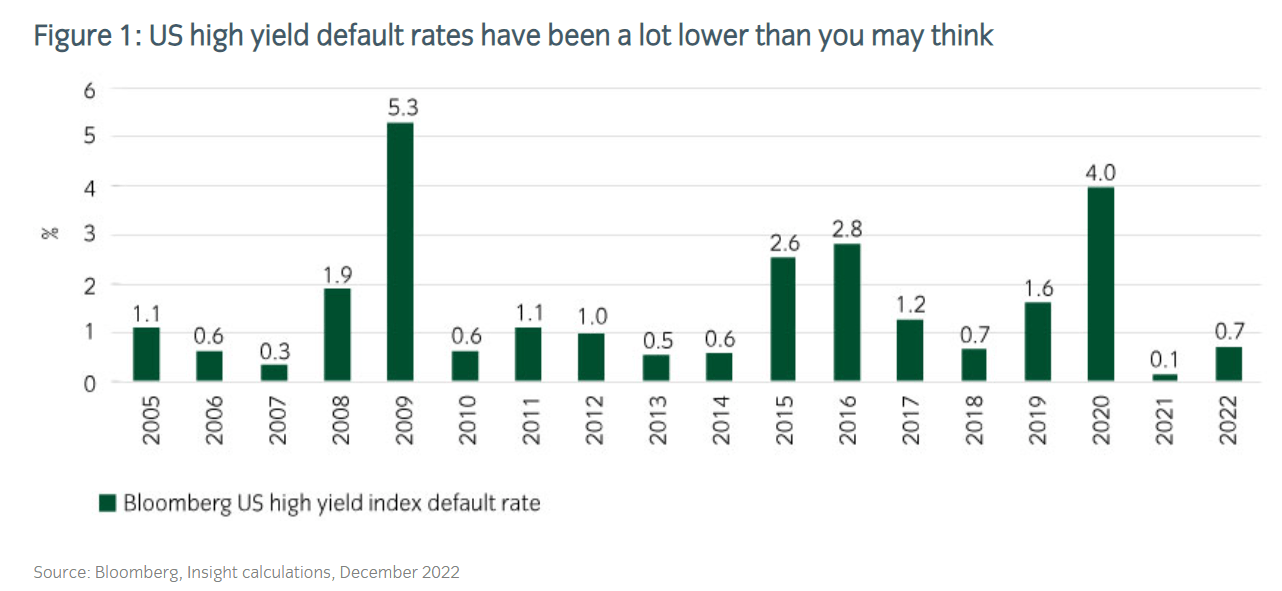

Offsetting this gross return will be any credit defaults experienced within DCF's portfolio. U.S. high yield default rates have historically averaged 1.5% over the past 15 years with peak default rates of 5.3% and 4.0% in 2009 and 2020 due to the Great Financial Crisis and the COVID-pandemic respectively, according to data from Insight Investment , (Figure 5).

Figure 10 - Historical U.S. high yield default rates (Insight Investment)

{kind=link}

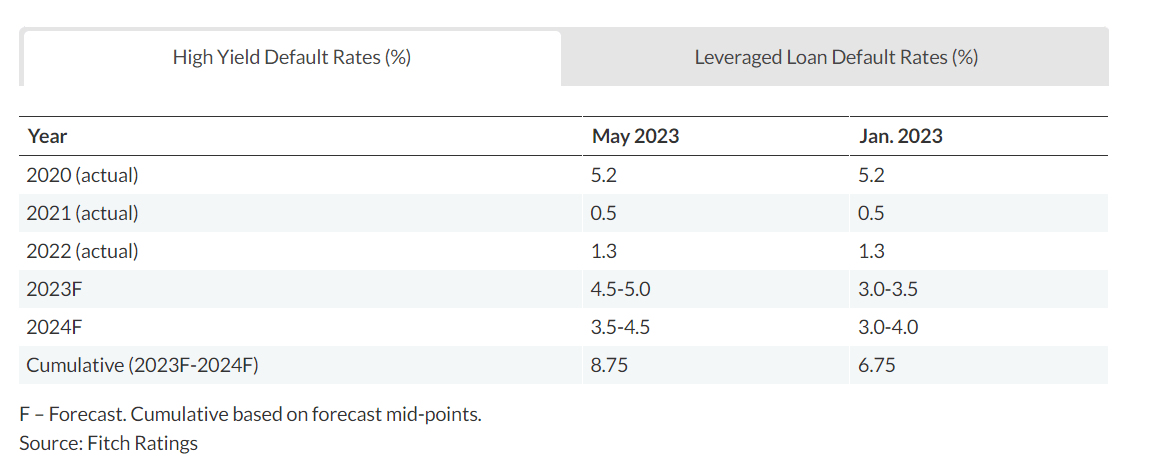

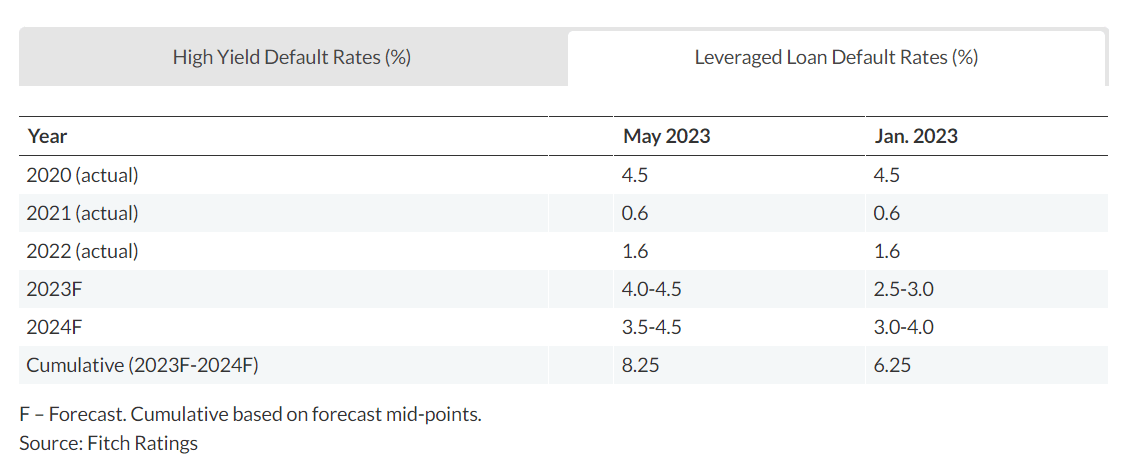

Fitch , one of the leading credit rating agencies, expect 2023 default rates to be between 4.5-5.0% for high yield bonds and 4.0-4.5% for leveraged loans, as economic growth weakens (Figure 11 and 12).

Figure 11 - Fitch forecast for 2023 high yield bond defaults (fitchratings.com)

{kind=link}

Figure 12 - Fitch forecast for 2023 leveraged loan defaults (fitchratings.com)

{kind=link}

Assuming Fitch is correct and defaults are 4.0% to 5.0% in the next year, combined with 30-50% recoveries upon default, then investors should expect a 2.0-3.5% drag from defaults within the typical high yield bond / leveraged loan portfolio like DCF's.

Combining the credit default drag with the topline 11% return calculated above, I believe investors in the DCF fund may be able to lock in a 7-9% annualized return for the next 18 months if they invest in the DCF fund until maturity.

Investors should note this is the expected annualized forward return for holding the DCF fund until December 2024. If the U.S. economy were to fall into recession in the next 18 months, then credit spreads may widen and DCF's NAV may decline. However, this NAV decline should be 'earned back' as the underlying portfolio of bonds and loans march towards maturity in December 2024.

Upside Vs. Downside in DCF?

On the upside, increasingly, many economists are backtracking on their projections for a U.S. recession. If the U.S. economy avoids a recession, then the default experience may be better than what Fitch is expecting, in which case forward returns could be closer to the 11% theoretical return.

On the downside, if we assume a worse than expected default experience, for example, 6% over the next year (note, the Great Financial Crisis saw a 5.3% default rate in 2009), then total returns may turn out to be closer to 7%. Furthermore, the DCF fund holds 21% in structured credit securities that may experience higher loss rates than the typical high yield bond or leveraged loan.

Conclusion

With high yield credit instruments offering attractive equity-like returns, I believe investors may be able to 'lock in' attractive forward returns on fixed-term investment funds like the BNY Mellon Alcentra Global Credit Income 2024 Target Term Fund Inc.

In addition to paying an attractive 5.5% distribution yield, the DCF fund is currently trading at a 5.3% discount to NAV. Furthermore, the average security in DCF's portfolio is estimated to be trading at a 3% discount to par. With only 18 months to maturity, investors buying the DCF fund today may be able to lock in an attractive 7-9% forward return for 18 months, assuming credit losses are in line with what Fitch is forecasting.

In the event of a bad recession, investors should still be able to generate positive average annual total returns if the fund is held to maturity in December 2024, as the coupons, accretion to par, and closing of the fund's discount to NAV should more than offset even the worst historical default experience.

For further details see:

DCF: Locking In High Returns With Fixed Term Closed-End Bond Funds