DCF - DCF: Presenting An Opportunity

2023-07-31 02:18:02 ET

Summary

- BNY Mellon Alcentra Global Credit Income 2024 Target Term Fund offers an opportunity for investors to buy shares at a discount, with its anticipated liquidation date at the end.

- The fund's portfolio is invested mostly in below-investment-grade credit quality, and it carries a sizeable allocation of its portfolio to investments outside of the U.S.

- Risks to consider include the portfolio's maturity extended beyond the anticipated termination date, and a possible extension of the term date for up to six months without shareholder approval.

Written by Nick Ackerman, co-produced by Stanford Chemist.

BNY Mellon Alcentra Global Credit Income 2024 Target Term Fund ( DCF ) has recently offered investors another opportunity to pick up shares at an attractive discount. This fund is worth watching as its anticipated liquidation date is coming up at the end of 2024. We would expect the discount to narrow as we head into the liquidation date. Of course, the fund can extend or attempt to extend this liquidation date in various ways, and it's always possible they will do so.

Here is how Stanford Chemist has exploited the discount/premium mechanic with DCF in the past. This is the other way that CEFs can be exploited for opportunities, in general, even if they aren't term funds. DCF just happens to be one with the longer opportunity of liquidating at NAV.

We've actually traded around the premium/discount fluctuations in DCF quite successfully in our Tactical Income-100 portfolio over the last year, allowing us to reap excellent annualized returns over short periods of time by exploiting the swings in valuation.

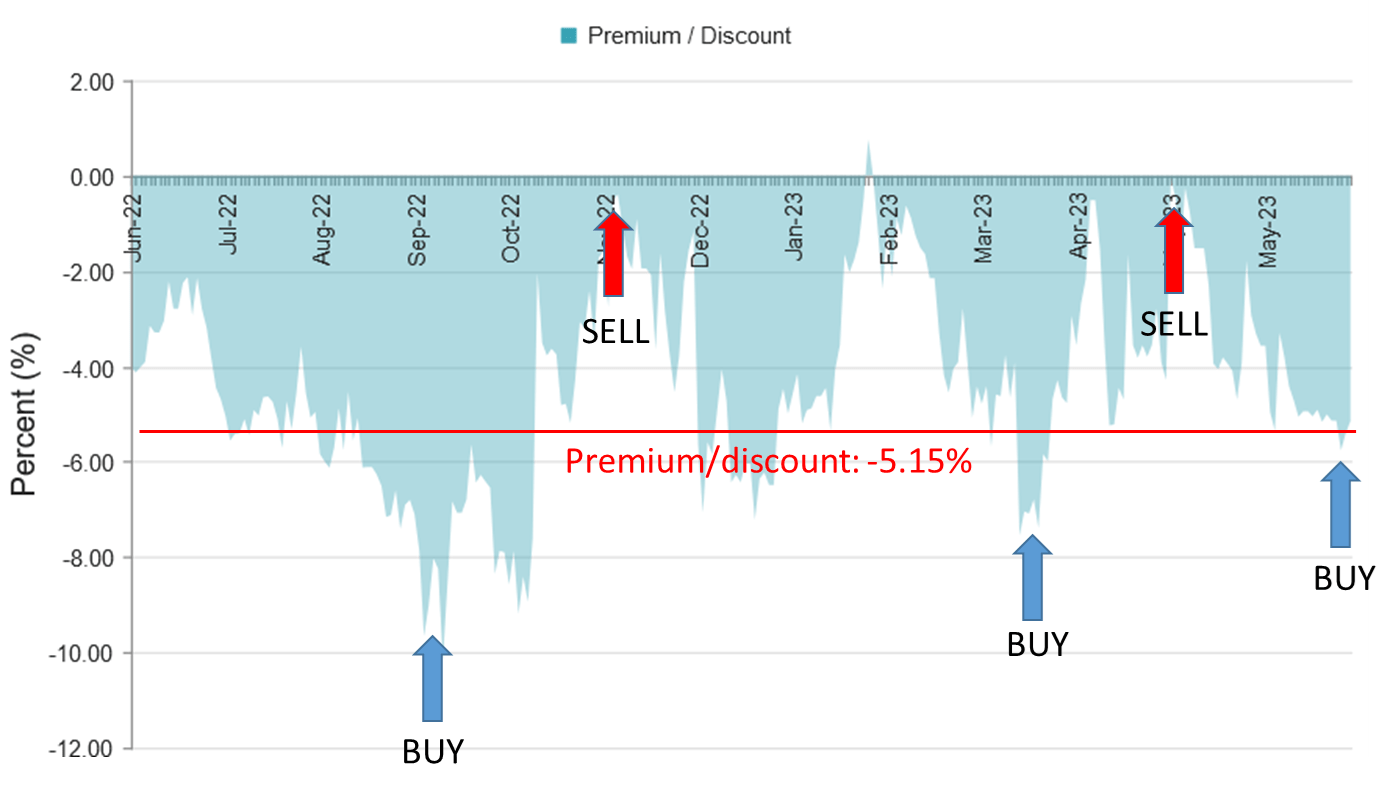

DCF Discount/Premium Chart Reflecting Buy/Sell Alert Timing (CEFConnect)

{kind=link}

Since our last update , the fund has performed respectably. Some of this was from the fund's discount narrowing as it was trading at a nearly 8.5% discount at the time.

DCF Performance Since Prior Update (Seeking Alpha)

The Basics

- 1-Year Z-score: -0.78

- Discount: -6.06%

- Distribution Yield: 5.49%

- Expense Ratio: 1.78%

- Leverage: 27.61%

- Managed Assets: $166.5 million

- Structure: Target Term (anticipated liquidation on or about December 1st, 2024)

DCF's investment objective is to "seek to provide high current income for today's yield-challenged market." Of course, with rates rising rapidly, a yield-challenged market isn't so prevalent anymore. To achieve this, the fund is essentially a multi-sector bond fund. They will invest in a "dynamic, multi-asset portfolio designed to access multiple sub-investment grade credit opportunities for enhanced yield potential with active risk management."

The fund is leveraged, and when including the leverage expense, the total expense ratio comes to 4.18%, as reported in their last semi-annual report . Most CEFs have seen their borrowing costs rise as interest rates have increased, and DCF is no different. The average interest rate on the loan was 5.56% vs. 2.25% at the end of their last fiscal year. As the Fed has increased interest rates further, this has only climbed higher since the last report. Overall, the total expense ratio saw a significant increase from the 2.87% total expense ratio seen previously.

Besides the potential upside of utilizing leverage, there is the downside of potentially greater losses and higher volatility as well. Another risk to consider is that the fund is quite small, which can translate into fairly poor daily trading volume. That would make it difficult for larger investors to buy and sell.

Discount Presents An Opportunity For Term Funds

Even though the discount narrowed materially since our last update, this can still present an opportunity for potential alpha relative to any non-term fund that invests similarly. The idea is that the discount should be realized on December 1st, 2024 when the fund is anticipated to terminate. As we move closer to the termination date - unless notified in advance that the term will be extended - we would expect this discount to only narrow further.

The idea of a target term fund is to return the original NAV to investors. This isn't a guarantee but only an attempt to do so. In the case of DCF, the original NAV was $9.835. That would require quite a significant move from here of 22.5%. However, this is also while paying out a distribution to investors. Meaning that the returns would have to be even greater in around a 1.5-year time frame. Therefore, I don't expect the fund to meet its target upon liquidation.

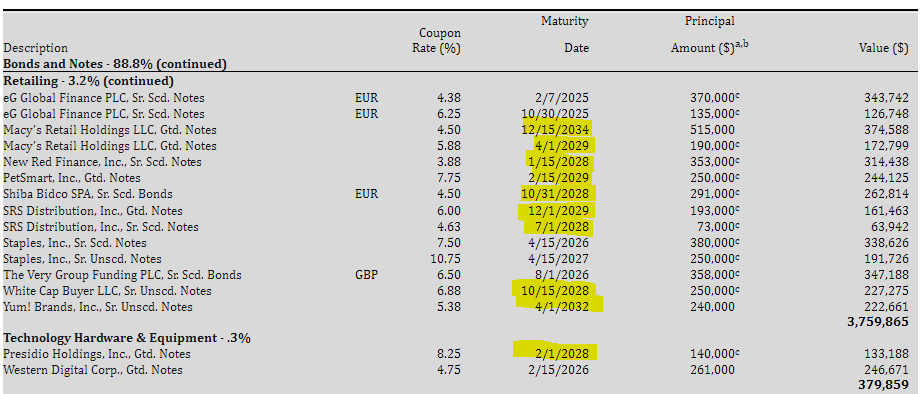

One potential way to bolster NAV would be to see its portfolio mature as we head into the termination date. However, with an average portfolio maturity of 5.34 years, they are positioned well beyond the December 1st, 2024 target. In looking through the maturity of their holdings, you can find holdings that mature later in the 2020s and some well into the 2030s.

DCF Snapshot of Holdings With Maturities Beyond Anticipated Termination (BNY Mellon)

{kind=link}

If the fund expects that there could be a material gain from extending the term of the fund, the Board may do so without shareholder approval. The first extension can be "for one period of up to six months by a vote of the Fund's entire Board of Directors."

To go out beyond that one-time extension, the fund states in its prospectus that it may do so, or at least attempt to do so. For an extension beyond the initial six months, it would then require shareholder approval.

The Fund’s Termination Date may not be extended for more than one period of up to six months without an amendment to the Fund’s Charter approved by a majority of the Fund’s entire Board of Directors, 75% of the Continuing Directors (as defined in the Fund’s Charter) and the affirmative vote of the holders of at least 75% of the outstanding voting securities of the Fund. The Fund retains broad flexibility to liquidate its portfolio, wind-down its business and make liquidating distributions to Common Shareholders in a manner and on a schedule it believes will best contribute to the achievement of its investment objectives.

With a maturity schedule well beyond the anticipated date, this could be one way they justify an extension.

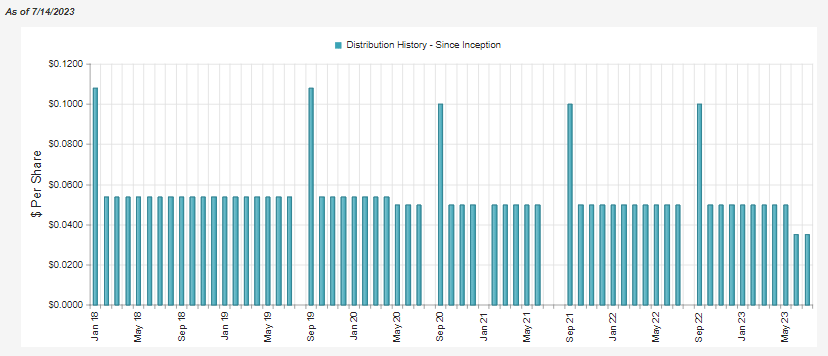

Distribution Cut As Expected

While I don't expect the fund to be able to meet its target, we also noted in our prior update we should expect distribution cuts as we head closer to the term date. This would be in an effort to get at least closer to its target NAV.

This is exactly what has happened, too, as the fund cut its payout from $0.05 to $0.035. So this wouldn't be a play if one's objective is looking for steady distributions, as that isn't likely to be the case. I would anticipate more cuts unless they throw in the towel, realizing that trying to hit their target is a bit of a stretch at this point.

{kind=link}

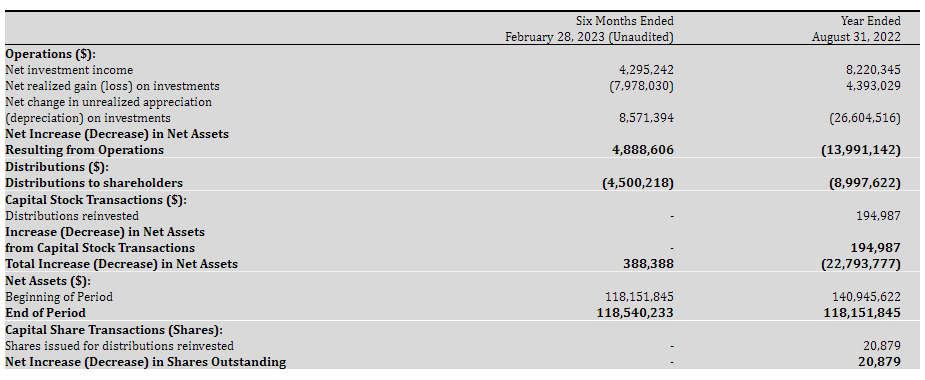

The fund was showing that they lacked distribution coverage with their latest report .

{kind=link}

That said, we've also seen an improvement in net investment income for the latest report. On a per-share basis for the semi-annual report, we see a NII of $0.29 compared to the full prior fiscal year NII of $0.55. If this trajectory continues, we'd see $0.58 NII per share for the current year.

Add in the distribution cut that will see an annualized rate of $0.42, and if this were a perpetual fund, we'd say that is strong coverage at 138% going forward and wouldn't expect cuts. That's why this will likely add to NAV to help bolster it up before its target comes due.

DCF's Portfolio

It should also be noted that this also factors in the higher expense ratio as it is net investment income, after all. Therefore, we know that the underlying portfolio is still experiencing higher income generation over and above the higher costs of leverage that have been coming through in the fund.

This higher income generation would come through investing in floating-rate debt securities, which are present in a large portion of the fund's portfolio. Besides the loan categories, the structured credit allocation will be primarily collateralized loan obligations. CLOs are pooled senior loans themselves and so will offer floating rate exposure.

DCF Sector Breakdown (BNY Mellon)

The fund's portfolio is invested mostly in below-investment-grade credit quality, which isn't that unexpected as it's consistent with the fund's investment policy. It also carries a sizeable allocation of its portfolio to investments outside of the U.S. Again, this is consistent with the fund's investment policy and part of the "global" part of its name implies.

DCF Portfolio Credit Quality (BNY Mellon)

As is usually the case with high-yield-focused funds, they are well diversified not only by investing across a variety of industry exposure but by investing through many different companies, even within the same industry. Expecting each company will operate a bit differently, potentially some better while others fail, is the idea.

For DCF, CEFConnect lists 377 total holdings. In looking at the largest holdings, a couple at the top could be considered fairly weighty relative to the rest of the portfolio. However, by the time we hit the sixth largest holding of the fund, we are already sub-1% weighting levels. That would mean, in general, each individual position has a relatively limited impact on the entire fund.

DCF Top Ten Issuers (BNY Mellon)

Conclusion

DCF is presenting a potential opportunity for some alpha generation relative to non-termed peers. This would come through due to the fund's discount as we head closer to the anticipated liquidation date at the end of 2024.

There are always risks to consider, and one of those is the fact that the portfolio's maturity is a fair bit extended beyond the anticipated termination date. Additionally, an extension of the term date is possible for up to six months without any shareholder having a say in that decision.

For further details see:

DCF: Presenting An Opportunity