DCF - DCF: When Term Funds Get Lucky

Summary

- BNY Mellon Alcentra Global Credit Income 2024 Target Term Fund is a fixed income closed end fund.

- The CEF has a defined maturity date of December 1, 2024 (subject to certain extensions).

- Markets tend to bottom before a recession ends, so odds are in the favor of both equity and high yield debt markets bottoming out in 2023 at some point.

- There can be a very nice trading set-up for this CEF later this year during the next market risk-off leg, with any substantial widening of the discount to NAV.

- This article covers CEFs.

Thesis

The BNY Mellon Alcentra Global Credit Income 2024 Target Term Fund ( DCF ) is a fixed income closed end fund. We have covered this fund before, with our initial analysis here . Given its term structure, we decided to re-visit the vehicle, especially in light of other term funds due in 2023, and our views on what the collateral manager should do in those cases.

The CEF has a fully covered distribution, and runs global high yield risk via its holdings. What makes this CEF stand out from the fixed income cohort is its term structure:

The fund’s investment objectives are to seek high current income and to return at least $9.835 per Common Share to holders of record of Common Shares on or about December 1, 2024 (subject to certain exte nsions). The fund will normally invest primarily in credit instruments and other investments with similar economic characteristics. Such credit instruments include: first lien secured, floa ting-rate loans, as well as investments in participations and assignments of such loans; second lien, senior unsecured, mezzanine and other collateralized and uncollateralized subordinated loans; corporate debt obligations other than loans; and structured products, including collateralized bond, loan and other debt obligations, structured notes and credit-linked notes.

Source: Annual Report

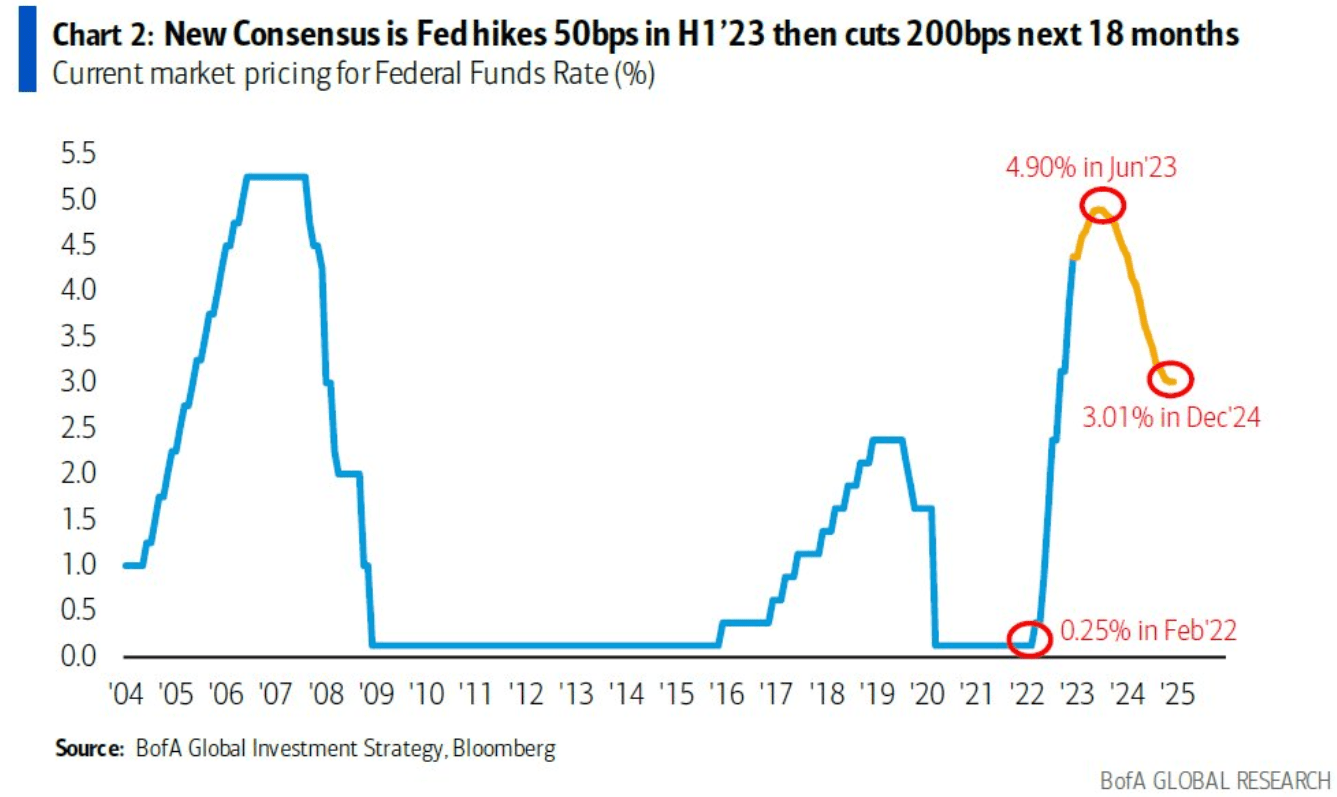

The CEF's collateral is not maturity matched, meaning that the CEF holders run the mismatch between the fund's stated maturity date and a potential risk-off event. On the flip side, the fund shareholders are lucky with the 2024 maturity date, given the consensus 2023 recessionary calls . What does that actually mean? Well, markets tend to bottom before the recession ends, so odds are in the favor of both equity and high yield debt markets bottoming out in 2023 at some point. We do not have a crystal ball to call the exact timing, but it will happen this year. That means 2024 will be a year of expansion and rate cuts:

{kind=link}

When rates decrease, high yield bonds benefit, and DCF will benefit as well. The fund's term maturity date is well set-up to benefit from the rate cut uplift. That gives potential investors a nice set-up - DCF will certainly get a nice uplift in 2024 and will end up closing the gap on any discount to NAV at the end of that year, if not earlier.

To also note that since our original coverage article on the name, the fund sub-adviser has found a new home:

Effective November 1, 2022, BNY Mellon sold its interest in Alcentra NY, LLC (the Sub-Adviser) to Franklin Resources, Inc., a global investment management organization operating as Franklin Templeton ("Franklin Templeton"). Alcentra NY, LLC will continue as a Sub-Adviser on the Fund through a new sub-advisory agreement between BNY Mellon Investment Adviser, Inc. and Alcentra NY, LLC. As of the effective date, Alcentra NY, LLC is no longer an affiliate of BNY Mellon.

Premium/Discount

The discount to net asset value has fluctuated in the 0% to -10% range in the past year:

We can see a nice correlation here with the overall market risk-on / risk-off sentiment. We like what we see here - during the Covid crisis we had a large panic moment when the discount touched unfathomable levels of -20% market levels versus NAV pricing, with the fund swiftly recovering after. During a normalized economic environment this CEF trades flat to NAV. Once the storm of 2023 is behind us, we will see the structure move back to flat NAV, especially on the back of the looming term maturity.

Holdings

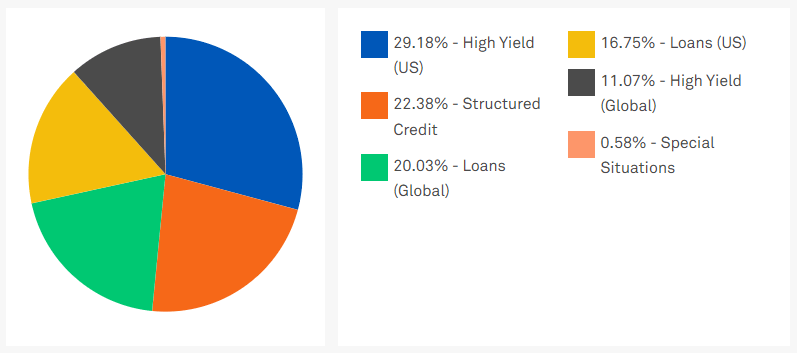

The portfolio is concentrated in high yield:

{kind=link}

The fund has a global reach, with U.S. and Global buckets for high yield credits. The second largest exposure in the fund, namely the bucket called "Structured Credit", is composed of mezzanine CLO tranches.

Mezzanine CLO tranches are basically subordinated or first loss pieces in collateralized loan obligations. If default rates spike substantially in the leveraged loan space these tranches would be the first ones to incur losses / impairments once the equity tranche is exhausted.

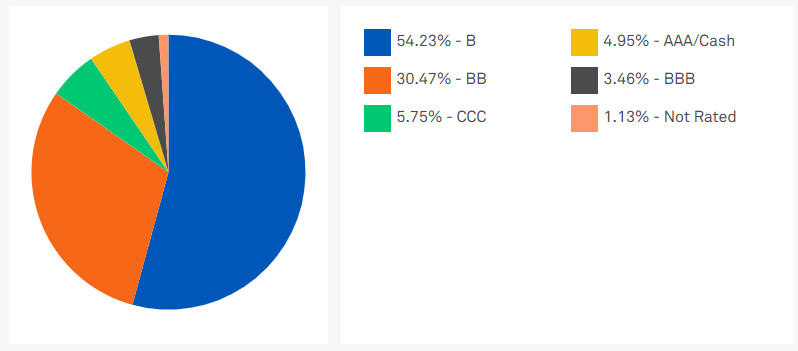

The fund is tilted towards 'B' names, a bit on the riskier side as things stand in high yield:

{kind=link}

Although it takes more risk via being overweight 'B' credits, the fund steers away from the riskiest part of the capital structure, namely 'CCC' credits.

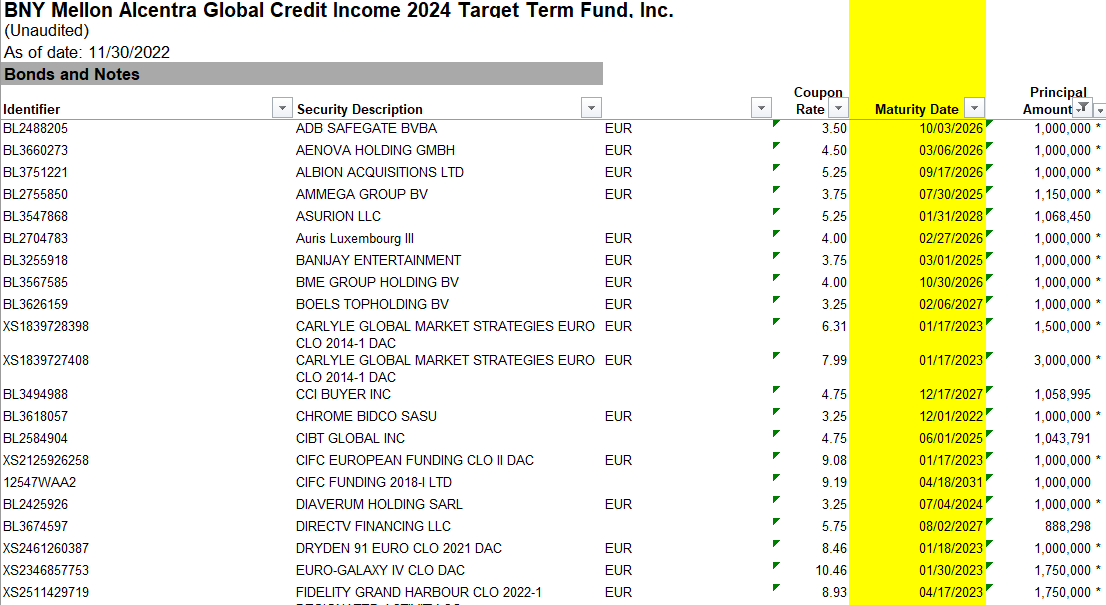

If we look at the collateral pool we will notice the fund does not maturity match its holdings versus its stated maturity date:

{kind=link}

When looking at the 'Maturity Date' column we can see that most positions mature after the 2024 fund termination date. We have selected only some of the largest positions here, but this is fairly representative for the entire vehicle, with at least 50% to 60% of the collateral offering principal paydowns after the stated fund maturity date.

Conclusion

DCF is a fixed income CEF. What is particular about this high yield fund is its December 2024 term maturity date. The fund does not maturity match its collateral, meaning shareholders take basis risk between the underlying collateral prices and the fund's maturity date (i.e. bonds will not pull to par on the fund's maturity date). On the flip side, any discount to net asset value would be fully extinguished on maturity date. The fund is currently trading with a -4.6% discount, but has seen even -10% levels during market sell-offs.

We believe we are currently in a recession, and with markets tending to bottom before recessions end, we expect a bottom in equity and high yield prices this year. That leaves a very nice set-up for the fund, with 2024 expected to be a very positive year for risk assets. Despite its term maturity, the CEF got lucky with the timing of the 2022/2023 recession. Any substantial widening of the discount to NAV for this fund represents a very nice entry point, with expected returns of 20% or more to its stated maturity date.

For further details see:

DCF: When Term Funds Get Lucky