DCP - DCP Midstream Preferred Equity - 8% Yield Via The Series C

Summary

- The DCP Series C Fixed-to-Floating Rate Cumulative Redeemable Perpetual Preferred Units are preferred shares from DCP.

- DCP Midstream is set to be acquired by Phillips 66 as announced earlier this year.

- Phillips 66 is a highly rated A3 company that has no balance sheet constraints or any outstanding preferred equity.

- DCP has already redeemed its Series A preferred shares that were first callable in December 2022, and is set to do the same with its Series C callable in October 2023.

- Post its October call date, DCP.PC would pay out an almost 10% all-in yield, almost double DCP's cost of capital as measured by 6-year senior unsecured yields.

Thesis

DCP Midstream (DCP) is a company that specializes in the gathering, processing, and transportation of natural gas and natural gas liquids. The company is headquartered in Denver, and is a significant player in the midstream energy industry. The company is being acquired by Phillips 66 ( PSX ), which announced in the beginning of the year that it had entered into a definitive agreement pursuant to which PSX will acquire all of the publicly held common units representing limited partner interests in DCP Midstream for a cash consideration of $41.75 per common unit.

Phillips 66 is a large, highly versatile energy player, that got its ratings affirmed upon the first leg of its DCP acquisition:

New York, August 18, 2022 -- Moody's Investors Service ("Moody's") affirmed Phillips 66's existing ratings, including its A3 long-term issuer rating, A3 senior unsecured rating and P-2 commercial paper rating. Phillips 66 Company's A3 long-term issuer rating and senior unsecured rating were also affirmed. The stable outlook is unchanged for both companies. The affirmation of Phillips 66's ratings follows announcements by the company that it has increased its interest in DCP Midstream, LLC through a transaction with its joint venture partner, Enbridge Inc. (Baa1 stable), and separately has made an offer to buy the outstanding common units of DCP Midstream, LP currently held by the public. The transaction with Enbridge, which has been completed, increased Phillips 66's economic interest in DCP Midstream, LP for which Enbridge received cash and an increased economic interest in Gray Oak Pipeline, LLC. The offer to purchase the publicly held common units of DCP is subject to an agreement with the conflicts committee of the board of directors of DCP and customary closing conditions.

Source: Moody's Ratings

DCP Capital Structure

DCP as a midstream player placed debt via senior unsecured notes and preferred equity.

Debt

- 3.875% Senior Notes due 2023,

- 5.375% Senior Notes due 2025,

- 5.625% Senior Notes due 2027,

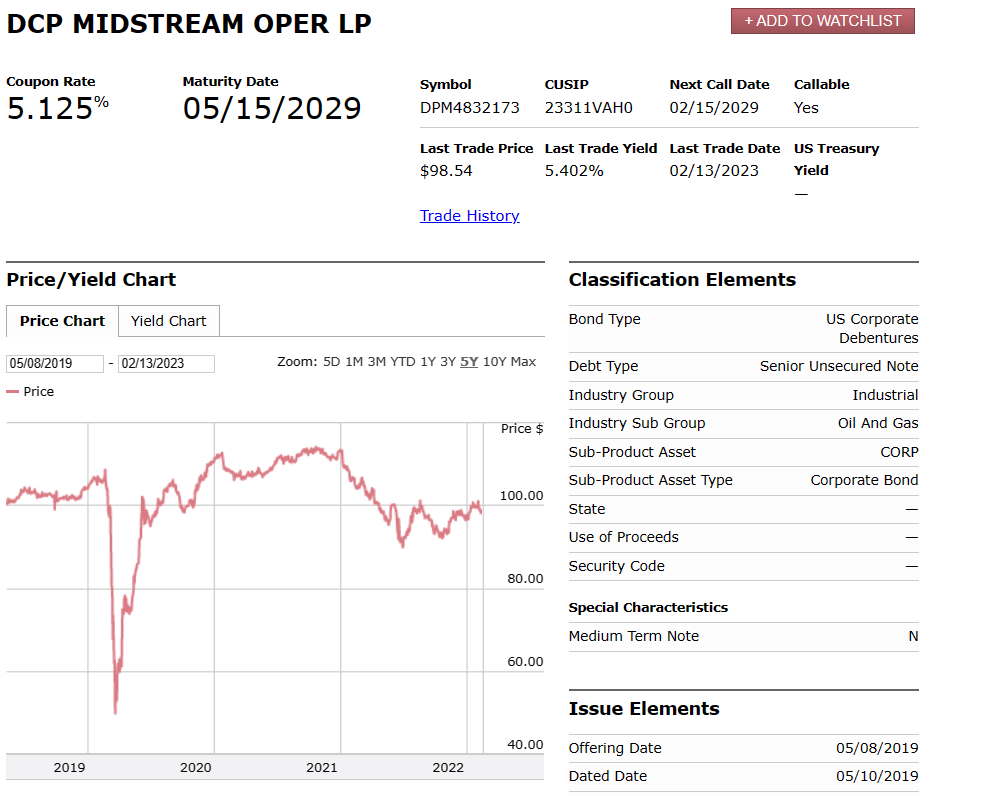

- 5.125% Senior Notes due 2029,

- 8.125% Senior Notes due 2030,

- 3.25% Senior Notes due 2032,

- 6.450% Senior Notes due 2036,

- 6.750% Senior Notes due 2037,

- 5.85% Fixed-to-Floating Rate Junior Subordinated Notes due 2043

- and 5.60% Senior Notes due 2044

Preferred Equity

- 7.875% Series B Fixed-to-Floating Rate Cumulative Redeemable Perpetual Preferred (callable starting in June 2023)

- 7.95% Series C Fixed-to-Floating Rate Cumulative Redeemable Perpetual Preferred Units (callable starting in October 2023)

Midstream companies generally have a high amount of leverage, hence they like to place preferred shares which do not count towards their Debt/EBITDA metrics in various bank lending agreements. We'd like to note that preferred equity generally gets called on the first call date if the funding markets allow for the company to refinancing at the same or lower levels. It is good practice to call on the first call date in order to establish bond-like features. It is also true that operators who run high leverage ratios and where fundamentals are not performing choose not to refinance the preferred shares.

It is not the case here. DCP actually had another class of preferred shares, namely Series A, which had December 2022 as the first call date. The Series A Preferred shares were redeemed by DCP on their December 2022 first call date:

DENVER, Feb. 08, 2023 (GLOBE NEWSWIRE) -- Today, DCP Midstream, LP (NYSE: DCP) reported its financial results for the quarter and year ended December 31, 2022.

Highlights:

- Redeemed the $500 million Series A Preferred Equity in the fourth quarter.

Source: Earnings Announcement

There is no reason to have preferred shares where a consolidated company does not have any debt metric issues, and is a solidly rated investment grade company. We will show you below how expensive the preferred shares are in the new structure, but fully expect series B and series C to be redeemed as well.

How Expensive Are the Preferred Shares?

To put things in perspective for the reader, let us have a look where the new company can now fund itself:

DCP Sen. Unsecured Debt Yield (FINRA)

{kind=link}

We can see from the above snapshot courtesy of FINRA, that now DCP/PSX funds itself in the 6-year tenor at 5.4%, or better said Treasuries plus a spread of roughly 100 bps.

Where are the Series C Preferred Shares trading? At roughly an 8% yield:

DCP.PRC Yield (PreferredStockChannel)

That is 1.5x the cost of the 6-year unsecured debt. That is exorbitant for a company that actually has no rating constraints and thus does not need preferred equity in its capital structure. Phillips 66 currently has no outstanding preferred equity, and there is no reason for this company to have any. We anticipate that the entity will redeem each tranche of legacy DCP preferred stock when it comes due.

Also keep in mind that Series C is set to move to a floating rate schedule:

On and after October 15, 2023, distributions on the Series C Preferred Units will accumulate at a percentage of the $25.00 liquidation preference equal to an annual floating rate of the three-month LIBOR plus a spread of 4.882%.

With the current forward Libor/Sofr curve, that equates to an all in yield in excess of 9.8%! When you can place 6 year debt at 5.4% why pay almost double the cash for legacy preferred equity? The math does not make sense, the capital structure constraints are just not there.

Conclusion

DCP is being acquired by PSX. Due to historic leverage ratio requirements and balance sheet constraints DCP had preferred equity outstanding. The company has already redeemed its Series A Preferred Equity that had a first call date in December 2022. Post the acquisition announcement we can see that DCP's cost of capital has decreased substantially - DCP's Senior Unsecured notes with a 6-year tenor are trading with a 5.4% yield only. The Series C Preferred Equity is set to reset in October to an all-in yield close to 10%, or almost double the senior unsecured cost of capital when measured on a six year horizon. That is untenable and not practical for a company such as PSX which has no preferred equity nor does it have any balance sheet or rating constraints to have such a form of funding. We anticipate the Series C Preferred Shares from legacy DCP to be redeemed in October 2023, hence we view them as a safe, 8% yielding short term holding.

For further details see:

DCP Midstream Preferred Equity - 8% Yield Via The Series C