DCP - DCP Midstream: Stock Might Plateau At Current Price Given Peak In Demand For Oil

Summary

- DCP Midstream is a midstream oil & gas firm that operates in both gathering & processing and logistics & marketing business segments.

- Although revenue and net profits are at a higher growth rate, I believe it is not sustainable in the next couple of years.

- The whole midstream oil & gas sector has been performing very well the last couple of years.

- The firm is a market leader in natural gas liquids (NGLs) and the demand for NGLs looks sustainable.

- I rate the stock a Hold for the reasons stated below.

Investment Thesis

DCP Midstream (DCP) had performed well during the last couple of years. Given geopolitical conditions and strong demand for energy, the midstream sector as a whole had a great couple of years. However, the question for a long-term investor like me always has been: Are the revenues sustainable, does the demand for oil persist, given better accessibility of sustainable alternatives? A report Global Energy Perspective 2022 by McKinsey says this is the case for the industry as a whole, but not for DCP. Additionally, the report says demand for natural gas is going up by 10% in the next decade and that DCP is a leader in the natural gas liquids (NGLs) segment.

What the company does

DCP Midstream LP is a midstream company that provides a suite of gathering, processing, transporting & storing natural gas and natural gas liquids (NGLs). Headquartered in Denver, Colorado, it operates in 9 states in the United States along with Mexico and Canada.

The Fortune 500 company is a joint venture between Phillip 66 (PSX) and Enbridge (ENB). It operates mainly in 2 business segments, logistics & marketing (transportation and marketing of natural gas, NGL, and crude oil) and gathering & processing (transportation of natural gas from wellheads to market centers, and storage of natural gas). By operating in both business segments, DCP Midstream can provide a full suite of midstream services, making it one of the largest gatherers and providers of natural gas liquids (NGLs) in the United States.

Recent Corporate Performance

Although the firm had a history of cyclical revenue and profit growth, in recent years the firm has reported strong numbers in both revenues and profits. Net income has reported a staggering 160% growth in the last reported year. Recent year-on-year revenue growth reported is 34%. However, this revenue growth is similar to the median revenue growth of its peers. This indicates that the midstream industry as a whole has seen an increase in revenues, largely due to various geopolitical and macro factors. Given how DCP Midstream performed, it could be evidence that the firm has found itself a moat (a competitive advantage).

However, it looks like that is not the case. This begs the obvious question of why net profit growth is huge compared to the growth in revenue. This is because of a myriad of factors ranging from a decrease in their operating expenses to a sudden increase in non-operating income (a one-off item on the income statement).

Strengths

The main strength of DCP Midstream as a business is its extensive network of assets including pipelines, processing plants & storage facilities. This position helps the firm retain the leadership position it has in the natural gas liquid segment and keeps competitors at bay. Looking at the business segments, the firm has almost equal revenues generated from its 2 business segments. This provides the firm with a healthy diversification of its assets.

On the balance sheet, DCP has lower financial leverage (debt to the total value) of 40% compared to the average debt to the total value of peers of 60%. This shows the firm has less solvency risk compared to its peers. Although the cash on the balance sheet of $1 million is alarming in 2021, recent filings reported cash in hand of around $93 million. The present current ratio, which measures the liquidity risk of the firm, is 0.68. This means that DCP Midstream can cover 68% of its short-term liabilities with its short term assets.

Due to the surge in the revenues the firm has seen since 2021, the operating cash the firm has generated has increased. The cash flow from investing activities reveals that the firm has decreased its investments compared to the pre-pandemic era.

Weaknesses

With the trend toward cars running on electricity, the attention now given to carbon emissions, and alternative energy sources increasing, it is a pressing issue to question the future of the oil and gas industry. What sectors are going to use oil and gas for energy, and what sectors can move to alternative energy sources? According to the report Global Energy Perspective 2022 by McKinsey, with the demand for alternative energy sources on an uptrend, demand for oil will peak during the next 2 years. However, for the next decade, the projected growth of demand for natural gas is 10%. This certainly is a positive thing for DCP as they are some of the largest distributors of natural gas & NGLs. However, it would be wise if DCP starts exploring and investing in renewable energy given the rapidly changing energy landscape.

Looking Forward

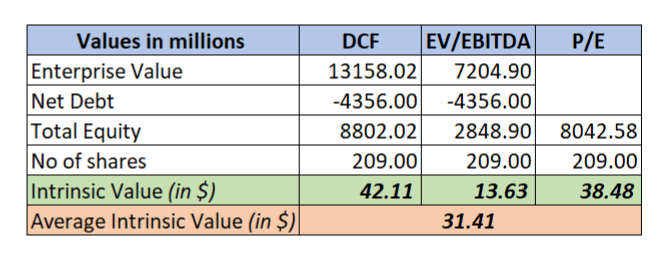

I have valued the company based on discounted cash flow ((DCF)) and comparable company multiples valuations. The average intrinsic stock price based on the above methods is around $31 compared to the $42 the stock is currently trading at.

Looking at the P/E multiples, the firm is trading at 8.9x as compared to the sector median of 8.5x. According to this method, the firm is slightly over-valued.

Whereas, looking at the EV/EBITDA multiples, the firm is trading at an EV/EBITDA multiple of 8.5x compared to the sector median of 6.8x. The stock price is overvalued based on comparable company EV/EBITDA multiples.

My assumptions for the DCF valuation are:

-

24-month Beta: 0.65

-

Cost of equity: 7.8%

-

Cost of debt: 6.4%

- Weighted Average Cost of Capital ((WACC)): 7.2%

Created by the author using data from company filings. (Self)

{kind=link}

Conclusion

Although DCP Midstream has posted great performance in recent years, I am not convinced that the firm will perform nearly as well in the coming 2 years, due to the reasons mentioned above. It would be exciting if the firm starts exploring investing in renewable energy, but that is not a given. Additionally, my intrinsic valuation of the stock price suggests that DCP is overvalued. Furthermore, the stock price appears to have plateaued, based on my analysis. For the reasons stated above, I rate the stock a Hold.

For further details see:

DCP Midstream: Stock Might Plateau At Current Price Given Peak In Demand For Oil