DCPH - Deciphera Is A Buy In Expectation Of A Significant Comeback

2023-06-18 07:02:37 ET

Summary

- After a period of bad news, DCPH has slowly inched back into a positive period.

- They have a lot of good news and some upcoming catalysts.

- Current prices make it quite attractive.

Here’s a simple scenario - I covered Deciphera ( DCPH ) in 2019, 2021, 2022 and in March 2023 - and the stock is down 70%, 70%, up 55% and holding steady, respectively, from the dates of these four coverages. What does that tell you? That the stock saw better times 3-4 years back, went down, made a comeback, and is holding steady in the last few months. But let us see if that quick take is validated by the facts on the ground.

Deciphera is a developer of novel cancer therapies. Its lead asset ripretinib, branded QINLOCK, was approved for 4th line advanced gastrointestinal stromal tumor (GIST) in 2020. The asset made $40mn in the first year of approval, and in Q1 2023, net product revenue in the U.S. was $24.6 million. Peak sales for the product was pegged at $1.6bn at that time, but like I have noted before, if QINLOCK is to reach anywhere near that, it has to get approval in higher line GIST. As the company noted in its earnings call :

…this additional indication would double the QINLOCK peak revenue potential to $350 million to $400 million in the U.S. alone.

This is where the company is struck. Despite positive data in an earlier trial, the molecule failed to differentiate itself well from 2nd line GIST approved sunitinib in a phase 3 trial. The failure was clear, however, where Deciphera may have miscalculated was that sunitinib was approved in 2006 on the basis of a trial which saw a 24.1 week PFS. Lately, however, GIST 2nd line disease burden has reduced after imatinib failure. That means, sunitinib mPFS has likely increased. This was predicted in an article I quoted in my previous coverage, and this is exactly what came to pass. The Sunitinib arm saw a PFS of 8.3 months, while ripretinib had a PFS of 8 months. Had it compared itself with historical sunitinib data, ripretinib would have succeeded. However, it did the right thing, and look what happened.

Not that ripretinib was an utter failure. Despite this hiccup, the molecule actually did better than sunitinib in certain areas that matter. In a specific subset, 2L GIST patients with a KIT exon 11 mutation, ripretinib had a median survival of 8.3 months compared to 7 months for sunitinib. Response rate in this subpopulation was also higher in ripretinib, with 23.9% and 14.6% rates, respectively. Most importantly, ripretinib had an unequivocally better safety profile. As I wrote earlier :

Grade 3/4 AEs were 41.3% for Qinlock compared to 65.6% for Sutent. Treatment emergent AEs were 26.5% for Qinlock and 55.2% for Sutent. Qinlock also saw fewer dose reductions, interruptions or treatment discontinuations because of side effects.

These and various other positive factors, highlighted in my previous article, led NCCN to include ripretinib in their 2L GIST guidelines. It has been included as a Preferred Regimen for Second-Line GIST Patients intolerant to Sunitinib. This, along with its highly differentiated safety and efficacy in the KIT 11 mutational subset, has improved ripretinib’s chances in 2L GIST. In January, the company presented ctDNA data that clearly showed its superior profile in this patient population; and based on this data, they will begin enrolling in a pivotal phase 3 study called INSIGHT in this patient population, where they have a breakthrough therapy designation. All of this is why the stock has improved so much in the period between my last two articles.

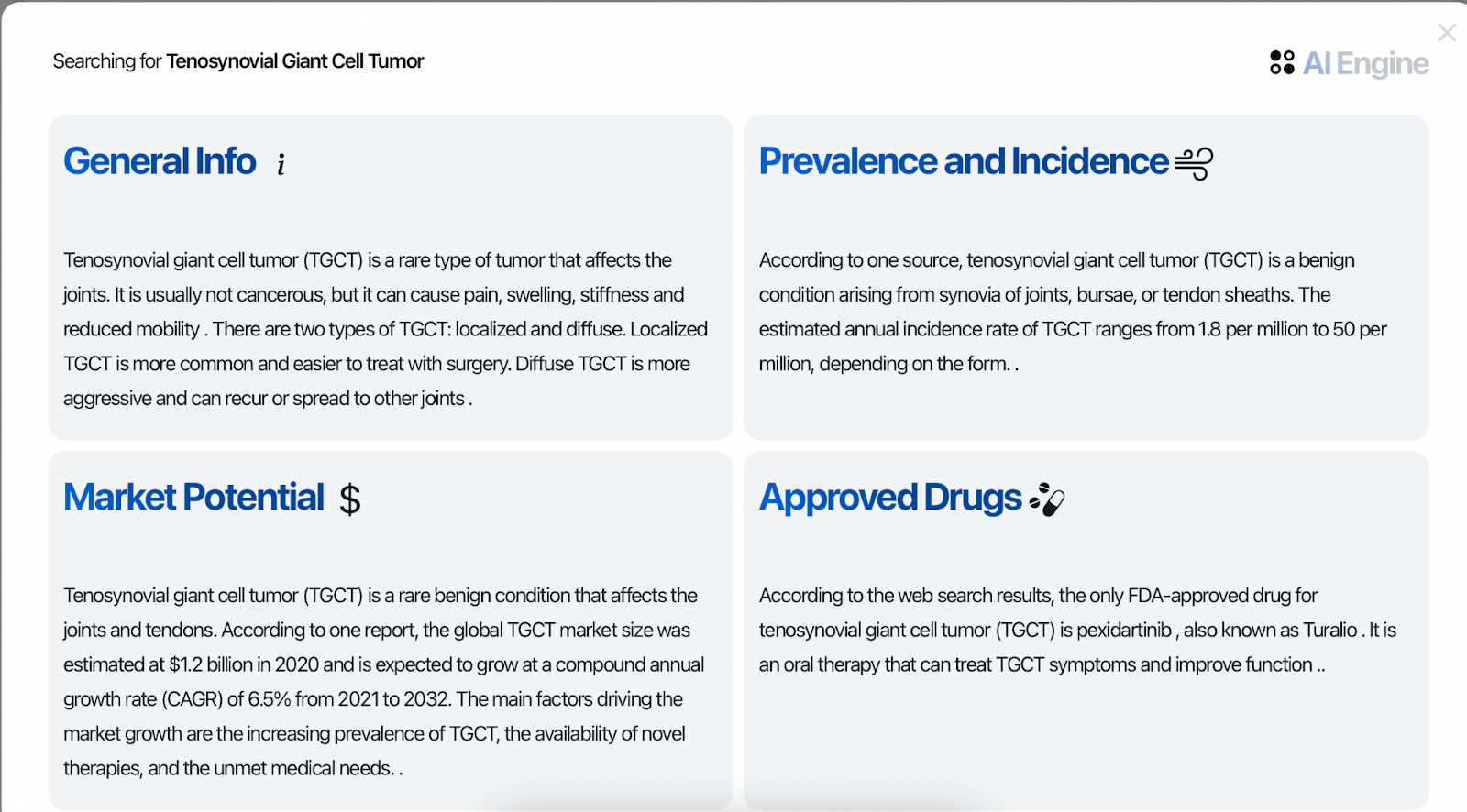

The rest of its pipeline has also progressed well. In February, they completed enrollment in a pivotal phase 3 study of vimseltinib in TGCT or Tenosynovial giant cell tumor, a rare, locally advanced neoplasm; an indication where, in an earlier phase 1/2 trial, the molecule showed positive efficacy data. Topline results from the pivotal trial will come out in Q4. About this indication, our TickerBay tool has this to say:

{kind=link}

The tool gives you a nice overview of any indication - here TGCT - and this tells me the positioning of vimseltinib in the space.

The buoyant spirit of the company was further reflected by the 8 posters they presented on their preclinical assets in April at AACR. I will not discuss these preclinical assets right now, but will simply quote from their earnings call:

We presented new preclinical data on our ULK inhibitor, DCC-3116, in combination with ripretinib in GIST models, and in combination with encorafenib and cetuximab in colorectal cancer models that strongly support two new dose escalation combination studies, which we expect to initiate in the second half of this year.

We also presented the first preclinical data for DCC-3084, a potential best-in-class pan-RAF inhibitor that broadly inhibits Class 1, 2 and 3 BRAF mutations and BRAF fusions. We announced the nomination of our newest development candidate, DCC-3009, a potential best-in-class pan-KIT inhibitor and we showcased our newly announced research program focused on GCN2 kinase, a key target in the integrated stress response pathway.

Financials

DCPH has a market cap of $1.14bn and a cash balance of $426mn, inclusive of the $144mn they raised in January through a secondary offering. US net revenue was $24.6mn in Q1; while international net product sales reached $8.6mn, primarily from Germany and France. Research and development expenses for the first quarter of 2023 were $54.8 million, while selling, general and administrative expenses for the first quarter of 2023 were $31.4mn. At that rate, they have a cash runway of 5-6 quarters, taking into account their increasing revenue.

Smart money holds nearly all of the company stock, with very low retail presence. Keyholders are Brightstar, Redmile, and so on. Insiders made small purchases in the last two months.

Bottom Line

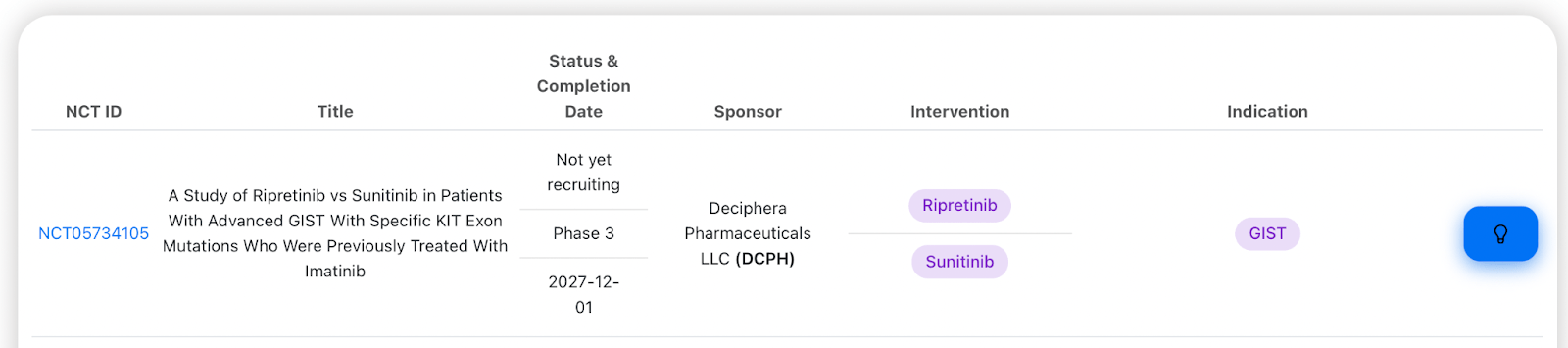

In my last article, I said that DCPH is in the middle of a comeback. The stock has been stagnant, but after today’s research, I still believe they are in the middle of a comeback. The stock will probably stay stagnant for a few more months, presenting an opportunity to buy before the fourth quarter, when they will have pivotal data from their second asset. Ripretinib’s INSIGHT data will take a few more years. Per our TickerBay tool, the completion date is 2027:

{kind=link}

I believe, given the low price and the upcoming catalysts, DCPH is a buy.

For further details see:

Deciphera Is A Buy In Expectation Of A Significant Comeback