SHOO - Deckers Outdoor: Limited Upside After Strong Rally

2023-06-15 11:52:34 ET

Summary

- Deckers Outdoor has had an excellent run over the past year or so, with strong growth fueling share appreciation.

- Growth should continue this year, but this doesn't mean the company makes for a compelling prospect at this time.

- Shares look pricey and likely have limited upside from here.

At first glance, the shoe market may not seem to be all that appealing. But if you find the right company at the right price, you can generate attractive upside. One firm that has, historically speaking, fit this description is Deckers Outdoor ( DECK ), an enterprise most famously known for its ownership of the UGG brand name. Even though some of the company’s product lines have been showing signs of weakness over the past year or so, the business as a whole continues to expand at a rather attractive pace. Given how much shares have increased in recent months, I would argue that investors would not be unwise to take a more cautious approach to the stock. But in the long run, I do still believe that the company should do quite well for itself.

An explosive brand leads the way

For shareholders of Deckers Outdoor, the past several months have been truly remarkable. Since I wrote my last bullish article on the company back in November of last year, shares have spiked 45.9%. This compares to the 17.2% rise seen by the S&P 500 over the same window of time. However, my bullish stance on the company has been in place far longer than that. When I first rated the company a ‘buy’ back in February of 2022, I considered the company undervalued and a growth prospect. Since then, this stock has generated a return for investors of 74.2% compared to the 0.9% rise experienced by the broader market.

{kind=link}

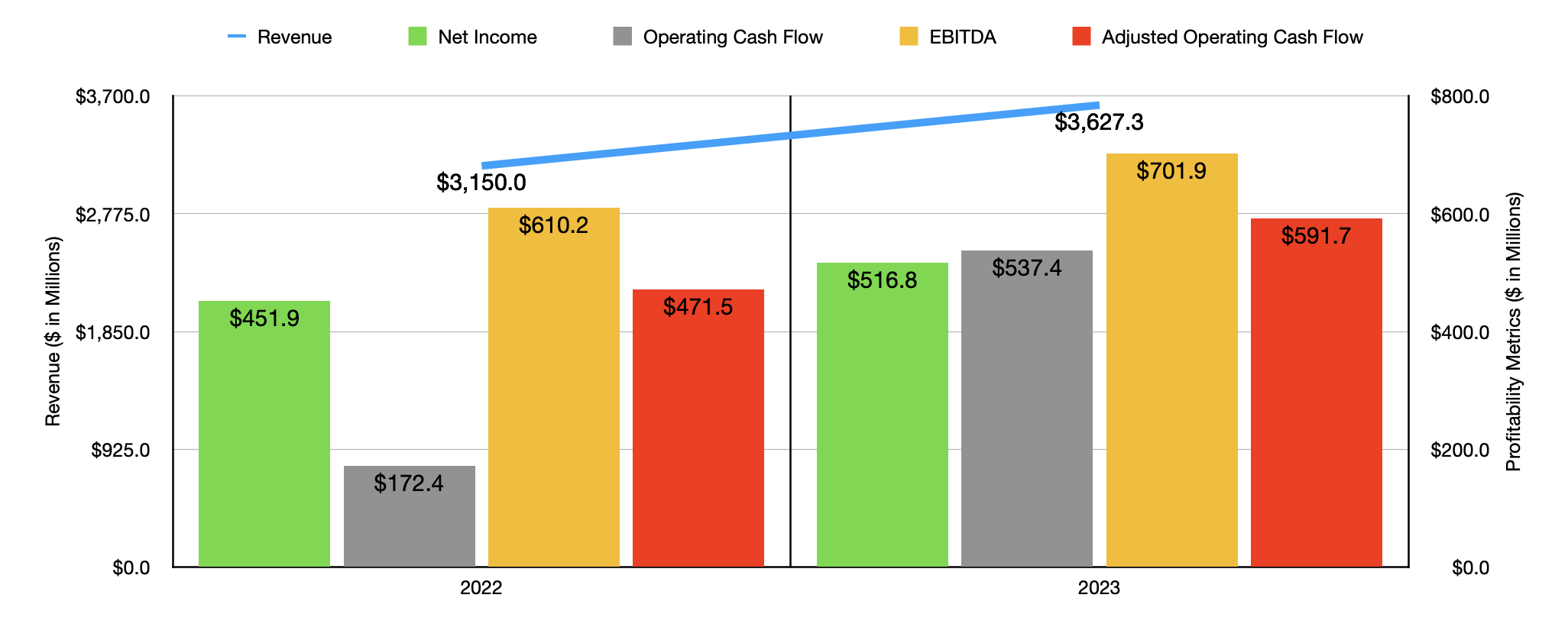

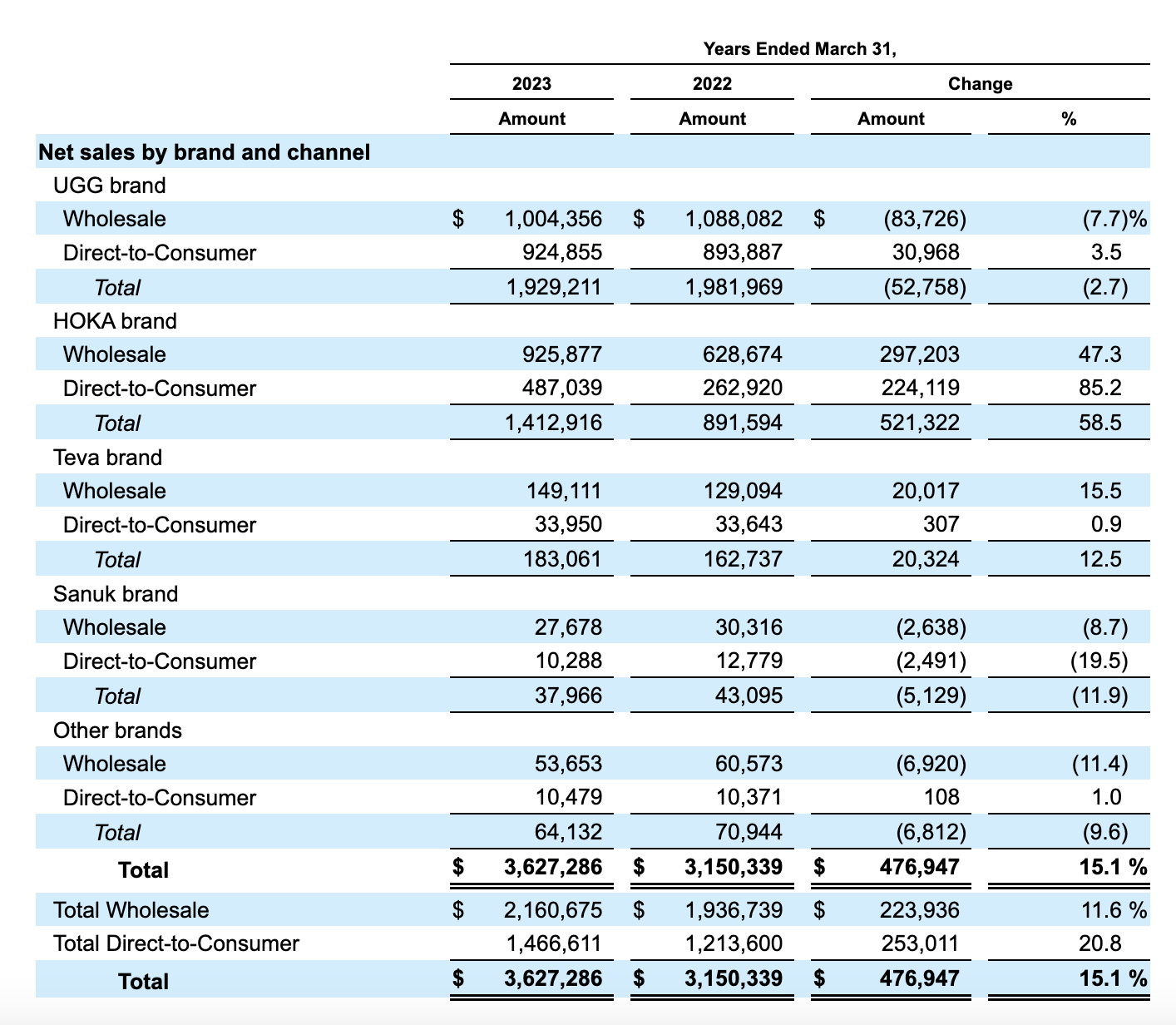

To understand why Deckers Outdoor continues to fare so well, we need only look at financial results covering the 2023 fiscal year . During this time, revenue came in at $3.63 billion. This represents a substantial increase of 15.1% over the $3.15 billion the company reported during the 2022 fiscal year. When you look deeper, you start to see some interesting things. For starters, international growth, while still accounting for a minority of the company's revenue, grew far faster than domestic growth did. International revenue expansion for the year was 19.7% compared to the 13.1% seen here at home. Outside of this, you can also see some very interesting results on a brand-by-brand basis.

{kind=link}

Historically speaking, the breadwinner for the company has been its famous UGG brand. Even today, it accounts for the largest portion of the company's revenue, totaling 53.2% of sales in all. However, its days of attractive growth seemed to be long gone. Revenue actually fell year over year, dropping 2.7% from $1.98 billion to $1.93 billion. This was all driven by a 7.7% decline in wholesale revenue that management attributed largely to stronger orders during the 2022 fiscal year aimed at combating supply chain issues. Actual direct to consumer revenue for the brand increased 3.5% year over year. The biggest weak spot for the company was the Sanuk brand, which saw revenue drop 11.9%. But with total sales coming out at about $38 million, it's a rounding error in the grand scheme of things.

This leaves two primary brands to look at. The first of these is the Teva brand. Robust demand in the wholesale category sent sales up 12.5% year over year. But with total revenue of only $183.1 million, Teva is not all that significant to the company. The real heavy lifter, then, was the HOKA brand. Sales under this category skyrocketed 58.5% year over year, soaring from $891.6 million to $1.41 billion. The direct-to-consumer side of the picture reported an 85.2% revenue spike, thanks to robust demand from consumers. Management attributed a lot of this upside to continued investments in expanding brand awareness. For the year as a whole, for instance, the company said that global brand awareness jumped 30% compared to what it was in the fall of last year. This was driven in large part by the Fly Human Fly campaign that the company launched that focused on storytelling and targeted activations in important cities. The company's efforts have proven to be particularly successful with the younger demographic. In the US, for instance, the brand experience more than double the number of purchasers aged 18 to 34 than what it saw one year earlier.

{kind=link}

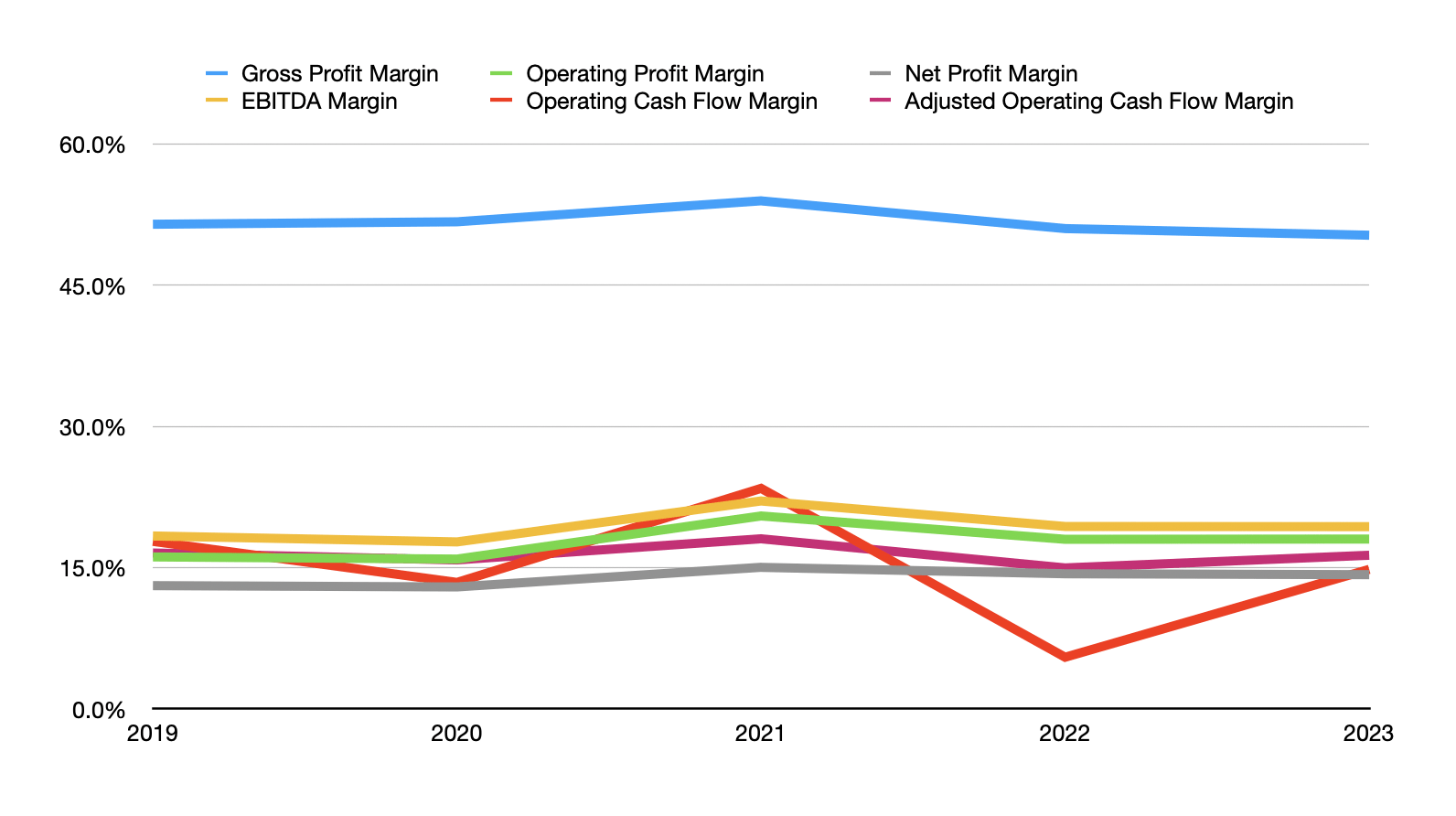

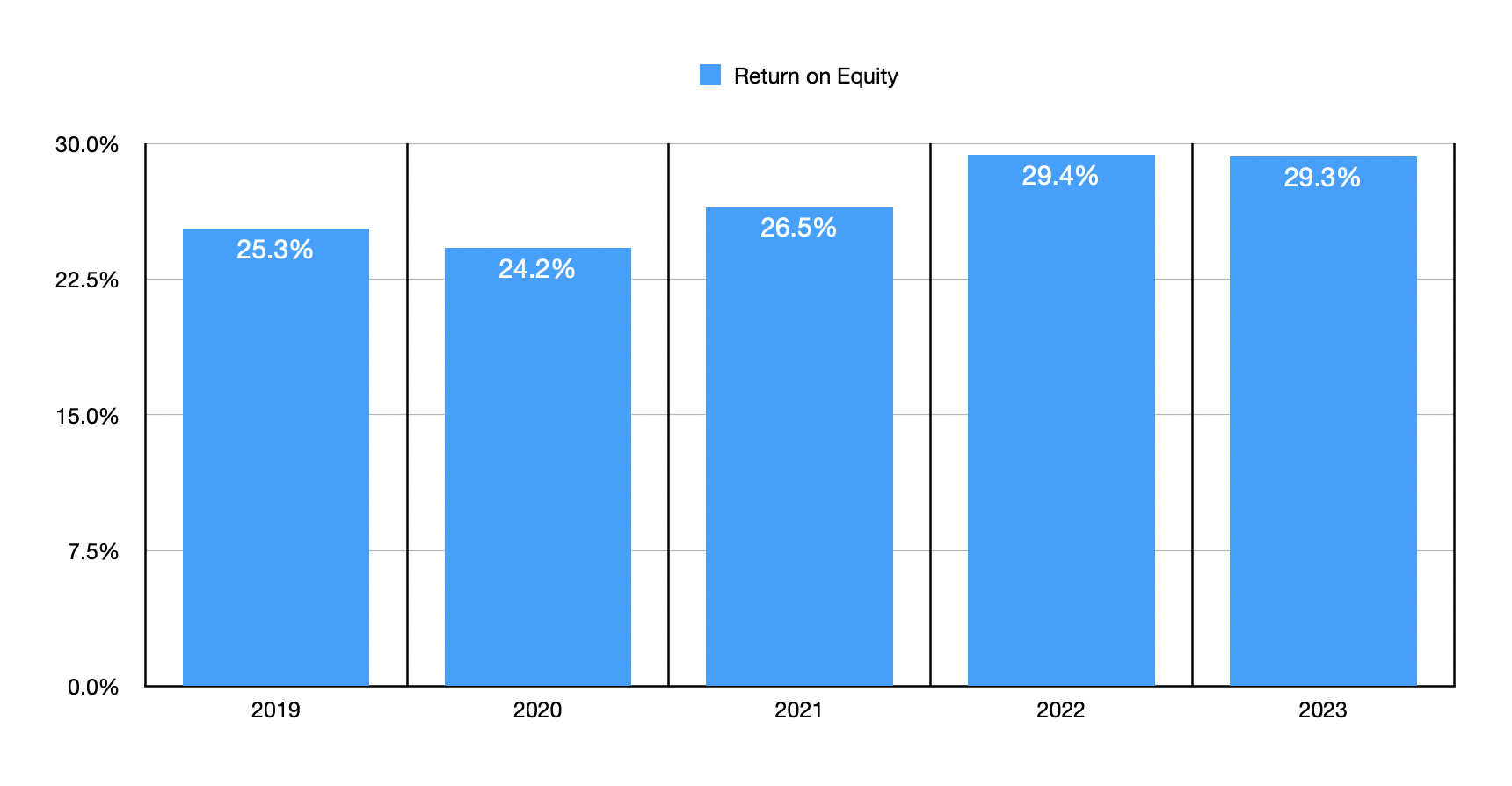

Profitability for the company also jumped during this time. Net income for the business expanded from $451.9 million to $516.8 million. Operating cash flow grew from $172.4 million to $537.4 million. If we adjust for changes in working capital, we would see this number increase more modestly from $471.5 million to $591.7 million. And finally, EBITDA for the firm grew from $610.2 million to $701.9 million. During times of rapid change, such as weakness in some product categories and rapid growth in others, there is a risk that margins can change significantly. In the chart above, however, I dispel this fear. Over the past five years, the various profit margins of the company have remained almost unchanged. Even if some brands were not outperforming others, this would represent a remarkable degree of stability that is rare to see, particularly in the consumer goods space. The one thing that I have noticed, however, is that while margins have remained almost unchanged, the firm’s return on equity has been higher in the past two years. This is visible in the chart below and, frankly, it is an incredibly bullish sign for investors.

{kind=link}

When it comes to the 2024 fiscal year that the company recently began, the picture is also looking up. Overall revenue for the company is expected to come in at around $3.95 billion. That's 8.9% above the $3.63 billion generated during the 2023 fiscal year. This does reflect a meaningful slowing down of the company's growth. But a good portion of this seems to be intentional. Management even said during their recent investor call that their goal for the HOKA brand is to shift from rapid growth to instead prioritizing marketplace management. This doesn't mean we won't see attractive expansion for the brand. In fact, management pegged growth this year for it at around 20%. But that is a noticeable decline compared to what the company saw in 2023.

On the bottom line, earnings per share are forecasted to come in at between $21 and $21.60. Because the company has a history of buying back stock, it's unclear what the full impact will be on a nominal basis. But we do know that, based on the current share count, this would translate to net profits of $569.7 million. Applying that same growth rate to other profitability metrics would result in adjusted operating cash flow of $670.6 million and EBITDA of $795.4 million.

{kind=link}

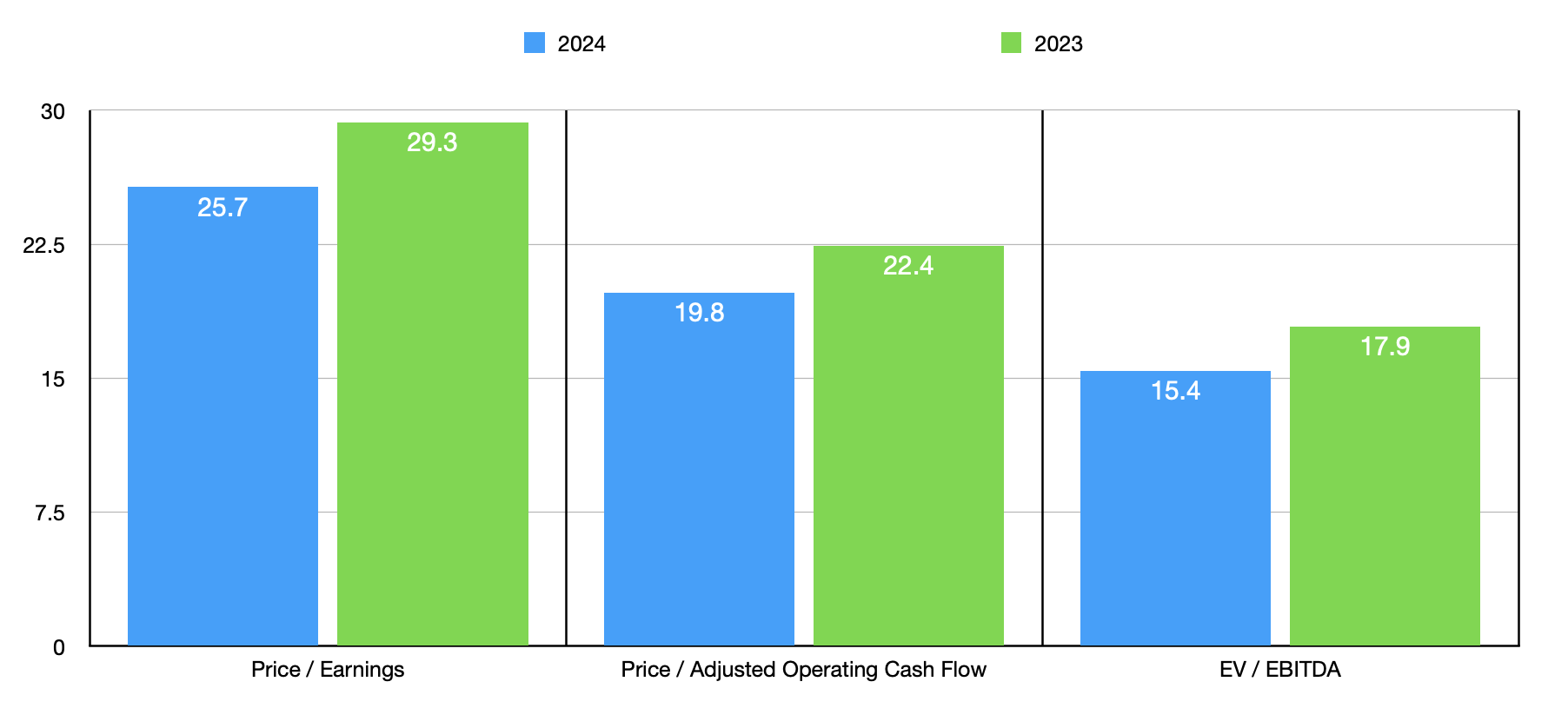

Taking these figures, we can easily value the company on a forward basis. The results can be seen in the chart above. The chart also shows how shares are priced using data from 2023. As you can see, shares do look cheaper on a forward basis. And with no debt on its books and cash and cash equivalents of $981.8 million, the EV to EBITDA multiple of the firm is particularly appealing. But even so, shares do look a bit pricey. This is true both on an absolute basis and relative to similar firms. In the table below, you can see that four of the five companies I compared it to are cheaper than it on both a price to earnings basis and on an EV to EBITDA basis. And when it comes to the price to operating cash flow approach, three of the four companies that had positive results were cheaper than Deckers Outdoor.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Deckers Outdoor |

| 29.3 |

| 22.4 |

| 17.9 |

| Skechers U.S.A. ( SKX ) |

| 20.2 |

| 13.7 |

| 10.5 |

| Crocs ( CROX ) |

| 11.6 |

| 10.5 |

| 9.1 |

| Steven Madden ( SHOO ) |

| 14.8 |

| 9.6 |

| 9.6 |

| Wolverine World Wide ( WWW ) |

| 5.6 |

| N/A |

| 8.2 |

| Nike ( NKE ) |

| 32.5 |

| 37.6 |

| 23.0 |

Takeaway

No matter how you look at it, the past year or so has been fantastic for Deckers Outdoor and its shareholders. The company has performed incredibly well, driven in large part by its HOKA brand. In the long run, I have high hopes that the company will continue to perform nicely. But this doesn't necessarily mean that now is a great time to buy in. Because of the company's balance sheet, it is a safer prospect than many other firms. But shares have turned pricey and, by management's own admission, growth is going to slow some. To some investors and analysts, this may not be a deterrent. In fact, on the same day that I write this, an analyst and his team at Raymond James initiated coverage on the company with an outperform rating. This brought with it a $565 price target, which would imply upside from its closing price on June 14 of 11.5%. It is possible that the company will increase in price from here. But as a value investor, my goal is to be more conservative in my approach to investments. And based on what I see, even though I acknowledge that the company is a fantastic one, I do think the easy money has been made and investors might want to look elsewhere for more attractive prospects. Because of that, I have decided to downgrade the company from a ‘buy’ to a ‘hold’.

For further details see:

Deckers Outdoor: Limited Upside After Strong Rally