DELHY - Deliveroo: Resilient Demand But The Stock Has Run Up Too Much

2023-10-22 07:52:46 ET

Summary

- Deliveroo's share price has risen 45% since January, much of which followed its Q1 2023 update, with its decent GTV outlook and the expectation of adjusted EBITDA profit for the first time.

- However, it has broadly corrected following its H1 2023 trading update, where it reduced its GTV outlook. Softening in growth from 2022 was apparent too.

- While the company has seen resilient demand over 2023 so far, as evident in its latest trading update, price upside looks unlikely on elevated market multiples compared to peers.

Since I last wrote about the food delivery app Deliveroo ( DROOF ) in January, its share price is up by 45%. At the time I had given it a Hold rating after its massive drop in the past year, with the anticipation that if it continued to show sustained sales growth, it could see an uptick.

Price Chart (Source: Seeking Alpha)

{kind=link}

So did the expectations actually play out? The stock has clearly gained a whole lot since I last checked. That’s exactly what I dig into here, with a focus on its latest trading update released this week.

What's behind the sharp price rise?

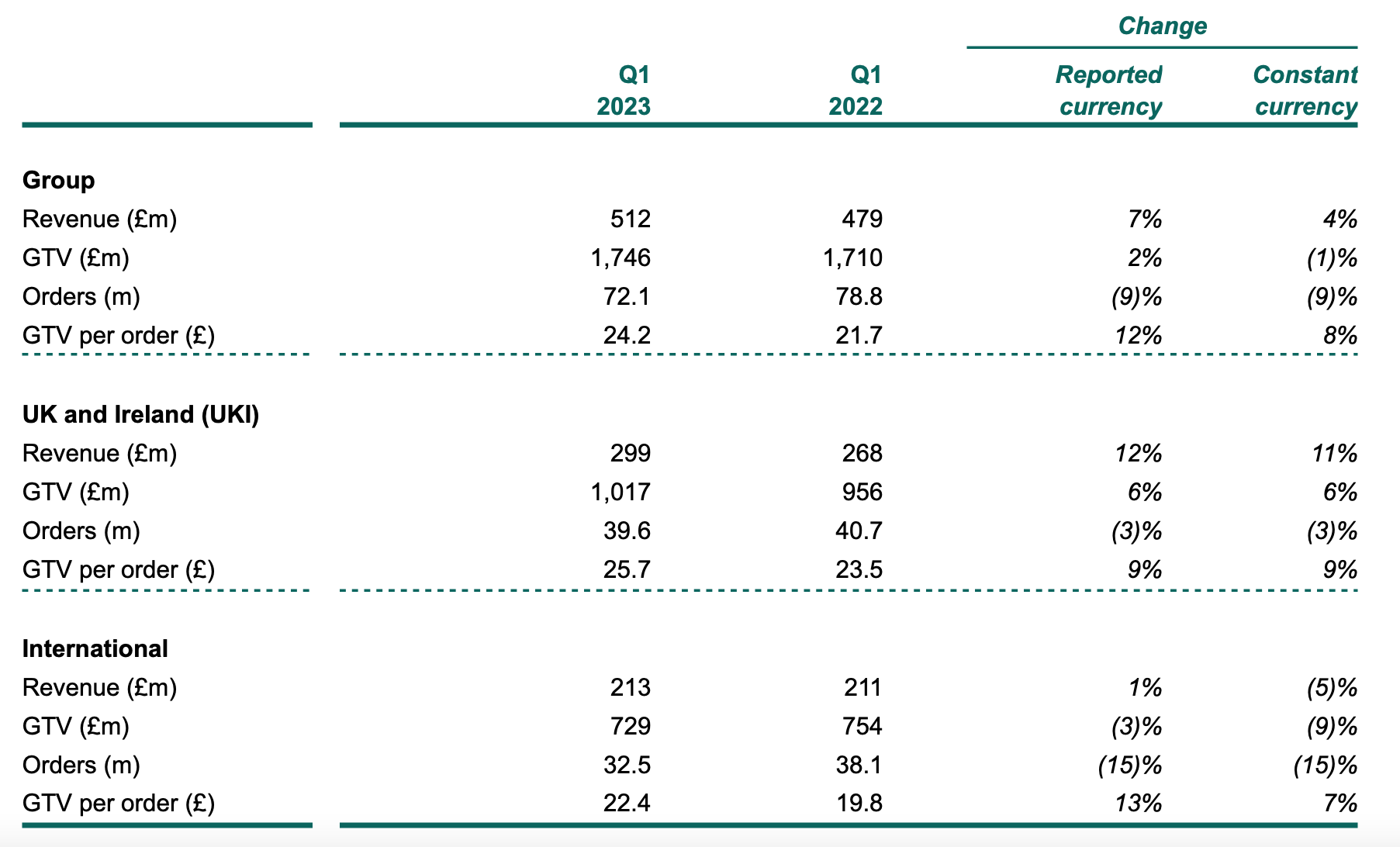

But first, a look at what's led to the big price rise over the year so far. Deliveroo saw a big jump in April (see chart above) following its first quarter (Q1 2023) trading update. The actual Q1 figures weren't impressive, for sure. They showed a come-off in both revenue growth and gross transaction value [GTV], which is the total sales inclusive of commissions, but net of refunds, compared to 14% revenue growth and 9% GTV growth for the full year 2022 .

Key Metrics, Q1 2023 (Source: Deliveroo)

{kind=link}

But the company's guidance was noteworthy. It expected “low- to mid-single digits” GTV growth, which wasn't too bad considering the likelihood of continued weakness in the consumer economy this year. The real highlight, however, was that it expected to turn adjusted EBITDA positive for the first time, with the projection of GBP 20-50 million.

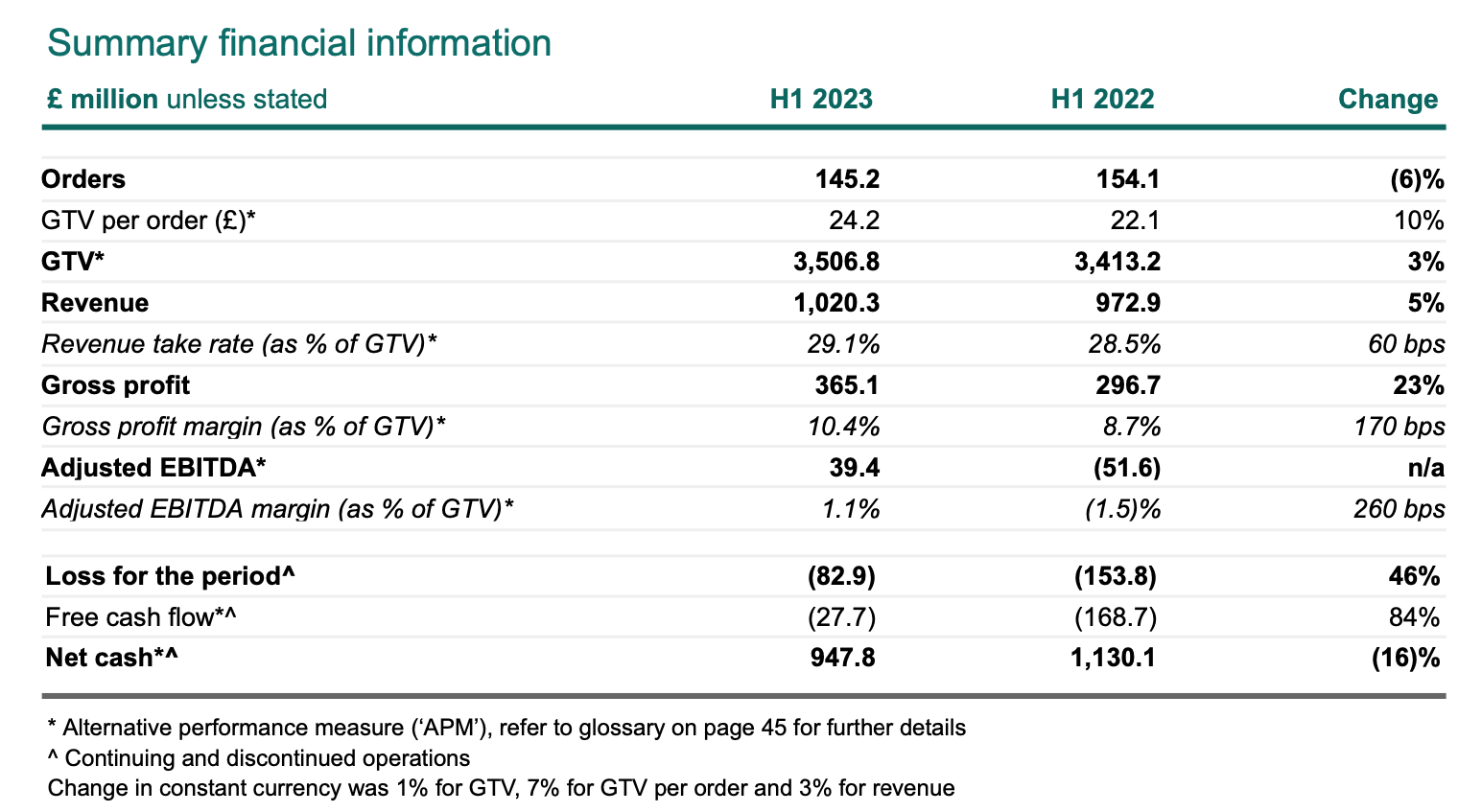

Better-than-expected macro trends as growth, particularly as its big UK market remained resilient and inflation softened across markets, likely continued to support the stock. Until the release of its first half (H1 2023) results, that is. While it increased its adjusted EBITDA projections to GBP 60-80 million, both GTV and revenue growth softened.

Key Metrics, H1 2023 (Source: Deliveroo)

{kind=link}

The trading update

The stock has broadly corrected since its H2 2023 results. But can the latest trading update change Deliveroo's recent fortunes in the stock market? Let's find out.

GTV and Orders

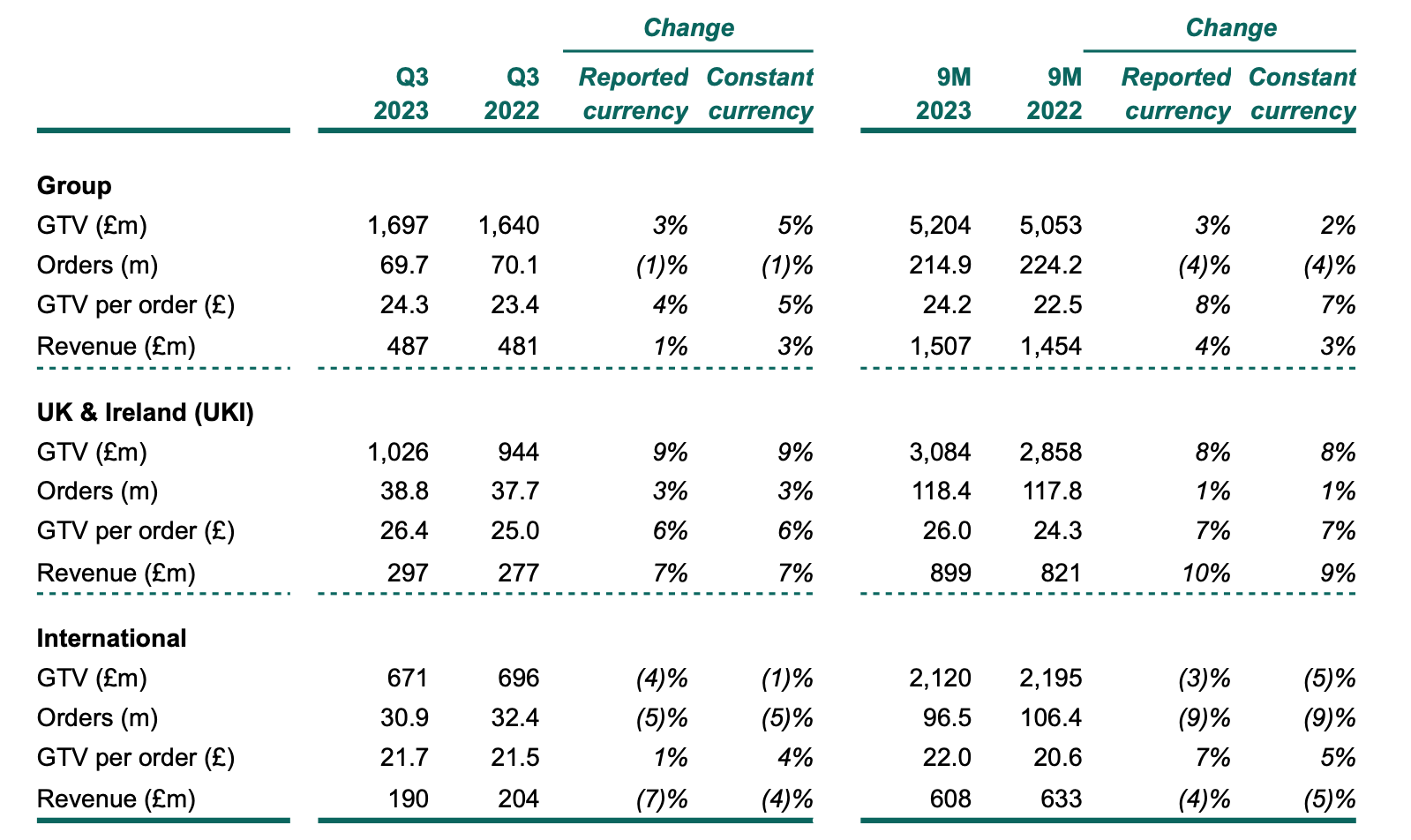

The first point to note is that GTV has seen a 3% year-on-year [YoY] growth in the third quarter of 2023 (Q3 2023) in reported currency. This is down from the 8% rise seen in Q3 2022, but it’s entirely due to the exchange rate effect, stemming from the substantial 41% of its GTV sourced from international operations for the first nine months of 2023 (9M 2023).

In constant currency terms, the GTV has grown at 5%, the same as last year. In other words, Deliveroo has seen sustained growth in demand. Almost the same trend shows up in GTV per order (see table below), even as orders themselves continue to decline by 1%, the same as last year.

Key Metrics, Q3 2023 (Source: Deliveroo)

{kind=link}

Interestingly, the company notes that the trend has continued despite a softening in food price inflation over this time, which would imply that the extent of the rise in restaurant food prices would have softened as well. This is one to look out for in the future as inflation in the category hopefully declines further over time.

The GTV growth spurt is marked in Q3 2023, with the number actually being smaller for 9M 2023 at 2% in constant currency (9M 2022: 6%). Orders also declined by a sharper 4% at this time (9M 2022: 6% growth). The 9M 2023 performance is a mixed bag, though, as GTV per order is actually up by 8% in reported terms (9M 2022: 1%).

This implies that while there are less frequent orders, the size per order is higher. This may well allude to affordability, as customers with a higher spending power are more likely to order right now.

Revenue growth

The company has added its revenue performance to the trading update this time, a departure from Q3 2022 when it only focused on GTV and orders. Revenue growth is at 4% in reported terms for 9M 2023 and at 1% in Q3 2023, dragged down by contracting international revenues while being stabilised by good growth in UK and Ireland revenues (see table above).

It’s worth mentioning that revenue growth has also slowed down marginally from 5% in the first half of 2023 (H1 2023), which is evidently down to slower growth in Q3 2023. But here too, it’s interesting to note that unfavourable exchange rates are at play, since at constant currency, revenue growth is unchanged.

In sum, the trading update essentially shows resilience for Deliveroo so far in 2023, even as exchange rates play spoilsport.

Market multiples

The market multiples, however, aren't as positive. Deliveroo’s forward price-to-sales (P/S) at 1.05x, is higher than that for peers like Just Eat Takeaway (TKAYF) at 0.46x and Delivery Hero (DLVHF) at 0.62x. Even taking Just Eat Takeaway’s weak growth numbers into account, it’s hard to justify Deliveroo’s P/S against Delivery Hero.

I also estimated the forward price-to-adjusted EBITDA (P/AE) ratio for all three based on their 2023 estimates. Deliveroo is much higher priced than its peers at 30.7x, compared to TKAYF at 7.9x and Delivery Hero at 2.7x.

The company’s EV-to-sales at 0.63x, however, compares favourably to DLVHF, which is at 0.98x and not too different from TKAYF at 0.56x. But it could also be a sign of being under-leveraged.

What next?

What the market multiples really say then overall, is that Deliveroo is overvalued right now. This is in contrast with the last time I checked when it was competitively priced compared to peers.

The optimism on the stock is also dying down, in line with the trend in market multiples. While it's a big positive that it turns adjusted EBITDA positive this year, the fact remains that its growth in terms of GTV is poised to stay muted for this year. While its revenue trends are resilient so far, despite weakness in the economy and still high inflation, it's hard to see an upside to the stock in the foreseeable future.

While I believe in the long-term Deliveroo story, I think now is the right time for profit taking for investors who bought it when it was trading much lower. I’m going with a Sell on Deliveroo for now, for all the right reasons.

For further details see:

Deliveroo: Resilient Demand But The Stock Has Run Up Too Much