PUBGY - Dentsu Group: Experiencing A Slowdown No Hurry To Buy

2023-08-23 04:24:41 ET

Summary

- Dentsu Group's Q2 FY12/2023 results show a slowdown in organic growth and weak overseas demand.

- The company has lowered its FY12/2023 guidance and expects continued weak consumer sentiment into FY12/2024.

- The outlook for FY12/2024 is uncertain due to a global economic slowdown and lack of major positive macro catalysts.

Investment thesis

Dentsu Group ( OTCPK:DNTUF ) Q2 FY12/2023 results highlighted an accelerated slowdown in organic growth, weak overseas demand, and lowered FY12/2023 guidance. We are concerned over continued weak consumer sentiment into FY12/2024 and, despite undemanding valuation multiples, rate the shares as neutral.

Quick primer

Dentsu Group is the world's fifth-largest advertising agency by revenue - the market leader is WPP ( WPP ), followed by Omnicom ( OMC ), Publicis ( OTCQX:PUBGY ), and Interpublic ( IPG ). Dentsu is the domestic market leader in Japan with around 30% share, followed by Hakuhodo DY Holdings ( OTCPK:HKUOY ) with around 20% market share.

Key financials with consensus forecasts

Key financials with consensus forecasts (Company, Refinitiv)

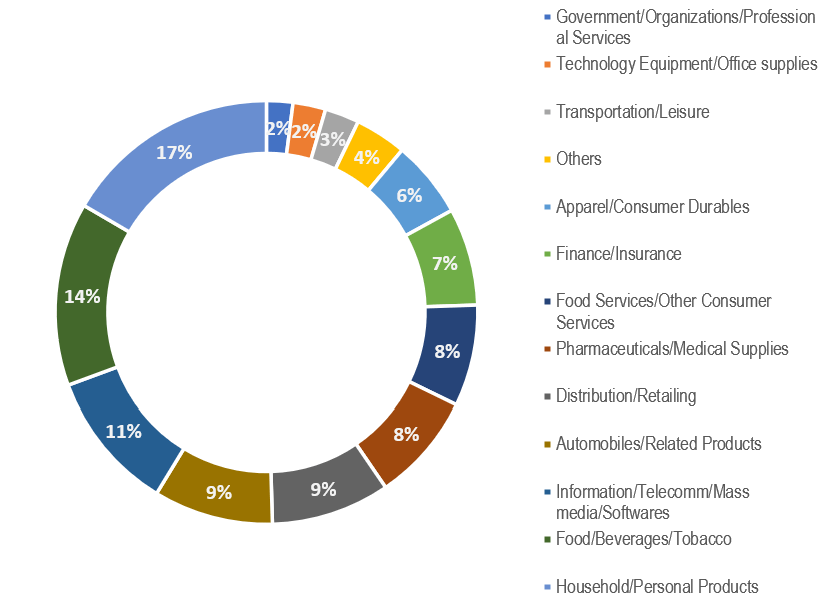

Sales split for Q1-2 FY12/2023 results - by sector

{kind=link}

Sales split for H1 FY12/2023 results - by sector (Company)

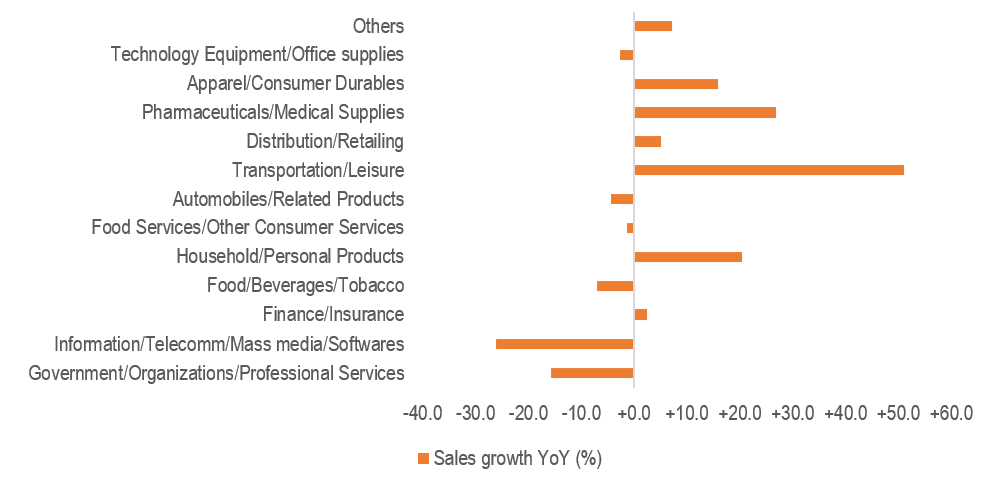

Sales growth YoY for Q1-2 FY12/2023 results - by sector

{kind=link}

Sales growth YoY for H1 FY12/2023 results - by sector (Company)

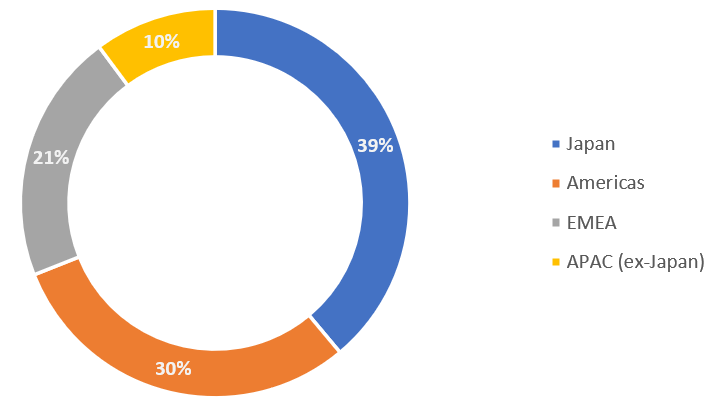

Sales split for Q2 FY12/2023 results - by region

{kind=link}

Sales split for Q2 FY12/2023 results - by region (Company)

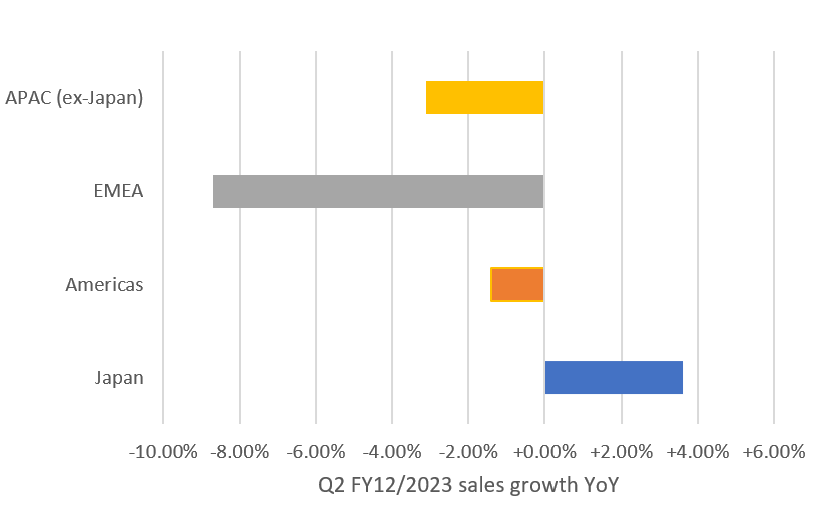

Sales growth YoY for Q2 FY12/2023 results - by region

{kind=link}

Sales growth YoY for Q2 FY12/2023 results - by region (Company)

Updating our view

We have updated our view from July 2021 , rating the shares as neutral. We previously highlighted weak ESG and capital allocation being too focused on M&A with limited returns; this time we will focus on the impact of a global economic slowdown, and whether the outlook is as stable for the prospective 2 years as indicated by the current consensus forecasts (please see Key financials table above) of steady OP growth in FY12/2024 and FY12/2025.

Q1-2 FY12/2023 results were a negative surprise

With a weak Japanese yen fanning favorable FX tailwinds YoY with approximately 60% of total sales originating overseas, Q2 FY12/2023 results showed a negative deceleration in organic sales growth of -4.7% YoY, versus -1.6% YoY in Q1 FY12/2023 ( page 31 ). Weakness stemmed from overseas markets, particularly from the EMEA region with organic sales falling -12.7% YoY - there have been issues over integrating its new operations in the DACH region (Germany, Austria, and Switzerland). Americas saw weakness in the tech sector, and APAC remained challenging with China remaining weak.

Performance by market sector for Q1-2 FY12/2023 (see charts for market sector sales breakdown and growth YoY) shows that whilst post-pandemic demand for transportation and leisure remains very strong, technology remains weak as well as staples such as food and beverage. What appears to have caught Dentsu by surprise is the pullback in spending in the finance sector, which although still in positive territory YoY is expected to remain weak.

The company has adjusted FY12/2023 guidance, with sales being lifted marginally by 0.3% (2.6% growth YoY) but adjusted operating profit cut by 4.1% (implied operating margin of 17.0%). While adjusted net profit remained unchanged at JPY122.1 billion, management has commented ( page 2 ) that it will be difficult to meet targets for its current medium-term plan, which is a sales CAGR of 4%-5%, and operating margins of 18.0%.

Outlook for FY2024

The company has reduced expectations into FY12/2024, given the expected slowdown in H2 FY12/2023. Looking forwards, we believe that trading conditions will worsen into the year-end, as we consider the lack of major positive macro catalysts in the short term. The Chinese economy remains weak, interest rates in developed markets are unlikely to be cut, and consumer confidence is not yet on the road to recovery.

With this backdrop, we expect discretionary spending to be relatively slow in FY12/2024, with demand for autos and technology being flat YoY at best. With US consumer credit levels reaching all-time highs in Q2 FY12/2023 , and credit card delinquencies rising to pre-pandemic levels , we are skeptical that advertising budgets will come flooding back YoY. In the UK where Dentsu has a sizable presence, consumer credit growth remained high at 12% YoY in June 2023, despite high base interest rates ( bottom chart on the page ), highlighting limited consumer liquidity.

The outlook for the Japanese economy in 2024 will depend significantly on how the Japanese yen will weaken YoY in our view, with the recent strong growth in GDP being primarily export-led . Even if FX was to remain a tailwind, we do not expect the same degree of positive impact YoY, which places downside risk to the economy and for advertising budgets.

Valuation

On current consensus forecasts, the shares are trading on PER FY12/2024 12.0x. This is not an expensive multiple and is in line with peers such as Omnicom on 11.5x and Interpublic on 12.6x. However, as consensus seem too bullish, we believe the shares are trading at a more expensive multiple (approximately 13.5x), and consequently, we do not the shares as being attractive.

Risks

Positive sentiment may come from the Paris 2024 Olympic events, where advertisers see it as a major opportunity to promote their brands and products. Continuing weakness in the Japanese yen will help keep the Japanese economy on an even keel YoY.

Negative risks stem from advertising budgets being slashed in sectors affected by weak consumer spending, such as technology, autos, transportation and leisure, and financial services. The company may undertake cost-cutting, which would provide a temporary reprieve but may set the business up for limited growth in a market recovery.

Conclusion

The outlook does not look overly positive for Dentsu, with the conclusion being that we believe it is too early to state a recovery is on the way for the advertising market. Although we cannot categorically say when business conditions will hit the bottom, we believe there is no hurry to be investing in this early cyclical business.

For further details see:

Dentsu Group: Experiencing A Slowdown, No Hurry To Buy