PROSF - Desert Lion Capital June 2022 Commentary

- Desert Lion Capital is managed by Rudi van Niekerk who is a South African citizen. Due to a growing interest from US and other international investors, Desert Lion Capital was launched to meet the needs of non-South African investors.

- Desert Lion Fund returned -7% for the month of May, compared to -12% by the JSE All Share Index.

- ZAR is extremely undervalued at current levels and there is high probability of ZAR strength (or commodity weakness) on the horizon.

- I don’t know when returns will manifest, but when they do, they are likely to do so in chunks.

Performance

| JAN |

| FEB |

| MAR |

| APR |

| MAY |

| JUN |

| JUL |

| AUG |

| SEP |

| OCT |

| NOV |

| DEC |

| YEAR TO DATE |

| Desert …Lion (1) |

| FTSE/JSE ..ALSI (2) |

| Delta |

| 2019 |

| 1.4% |

| - 1.2% |

| 2.9% |

| - 0.9% |

| - 10.7% |

| 0.8% |

| 6.1% |

| 3.3% |

| 3.9% |

| 4.8% |

| 4.7% |

| 0.1% |

| 2020 |

| - 7.7% |

| - 14.4% |

| - 25.8% |

| 2.0% |

| 3.5% |

| 6.9% |

| 3.4% |

| 5.6% |

| 10.3% |

| 13.2% |

| 9.6% |

| 12.5% |

| 11.2% |

| - 1.0% |

| 12.2% |

| 2021 |

| 10.9% |

| - 2.4% |

| 6.9% |

| - 2.5% |

| 2.7% |

| - 2.1% |

| - 1.2% |

| - 3.3% |

| - 5.7% |

| 5.9% |

| - 4.6% |

| 6.1% |

| 9.6% |

| 14.6% |

| - 5.0% |

| 2022 |

| 0.4% |

| - 0.0% |

| 2.0% |

| - 7.3% |

| - 6.0% |

| - 7.1% |

| - 17.1% |

| - 12.3% |

| - 4.8% |

| Cumulative – inception to date (3) |

| 5.9% |

| 4.3% |

| 1.6% |

| Annualized – inception to date (3) |

| 1.8% |

| 1.3% |

| 0.5% |

| Notes to Performance 1 Performance represents the Fund’s Standard Class and is representative of an annual management fee of 0.75%; fund expenses of 0.5% p.a.; 6% non-compounding hurdle; performance fee of 25% of profits exceeding the 6% hard hurdle; high water mark applies. 2 FTSE/JSE All Share Index (“ALSH” or “J203”) converted to USD returns. 3 Net results to a Limited Partner in the Standard Class as of April 1, 2019 inception. Individual returns will vary by class and date of investment. PAST PERFORMANCE IS NOT A GUARANTEE OF FUTURE RESULTS. |

Dear partners and friends,

The Fund returned -7% for the month of May, compared to -12% by the JSE All Share Index (J203). Over half (-4%) of this month’s negative return was driven by currency movements with the stronger USD/weaker ZAR. I recently wrote about foreign exchange exposure in our May 2022 commentary and will revisit the topic briefly here with some great charts.

The first half of the 2022 calendar year was not kind to investors. Unless you held the majority of your capital in energy or U.S. dollar cash, there was almost nowhere to hide. International equity markets are down significantly. The S&P 500 index dropped -21%. Even bonds, the traditional safe haven during market drawdowns, went down with other markets in unison. For example, the iShares 20 Plus Year Treasury Bond ETF was down -22% for the year through June.

Our portfolio positioning is focused on risk management (companies with robust fundamentals, limited or no debt, trading at valuations that provide good margins of safety), skewed towards shorter duration assets (strong cash generation today that is sustainable and growing), and antifragile to endure and capitalize on a variety of uncertain outcomes (e.g., inflation, stagflation, recession, commodity cycle, financial repression, resumption of growth).

Thoughts on currency

The ZAR weakened by more than 10% against the USD over the past quarter. When extreme riskoff sentiment permeates markets, we often see a subsequent retreat to the USD as a liquid safe haven, leading to USD strength against most currencies. Emerging markets bore the brunt of the sell-off and liquidity withdrawal. The JPMorgan Emerging Market Currency index has now dropped below 50 for the first time since it was initiated in 2010, when it was worth 100.

{kind=link}

Dollar-denominated emerging market bonds are back to their lows of the COVID pandemic market crash.

{kind=link}

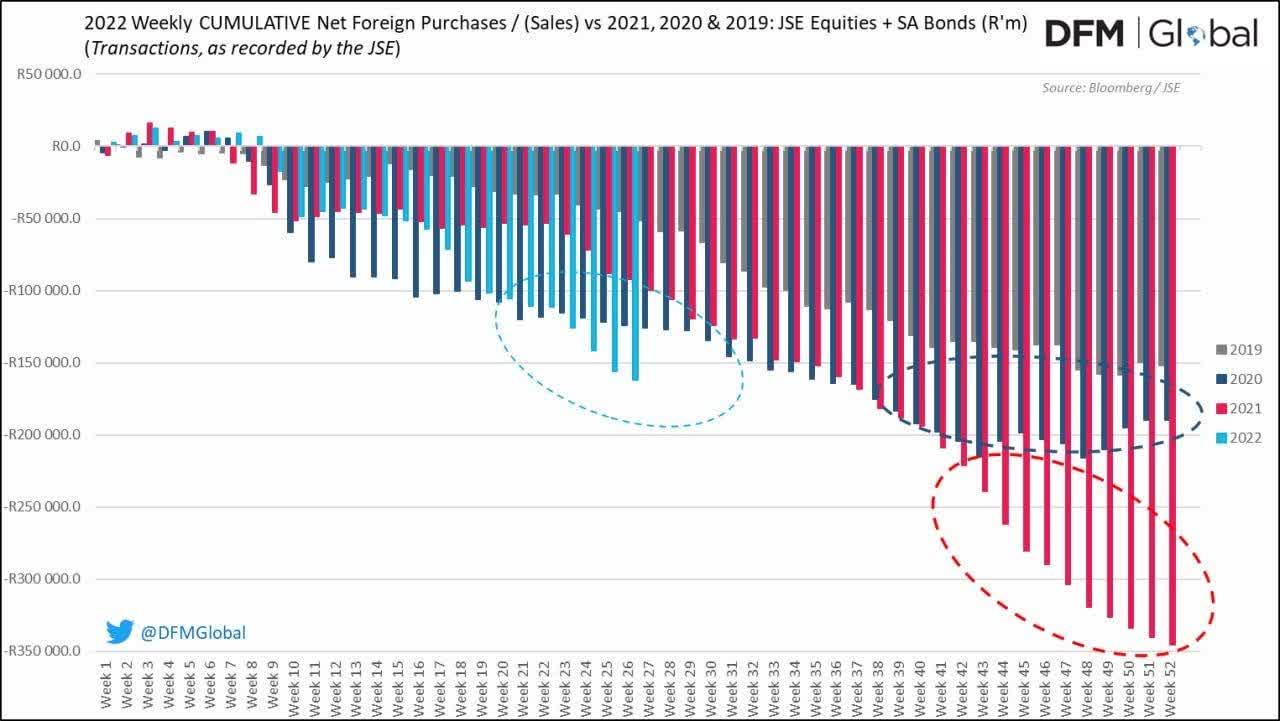

South African markets have not been spared. Cumulative net foreign outflows from South African equities and bonds are set to surpass those of 2019, 2020, and 2021.

{kind=link}

These outflows have put tremendous pressure on the ZAR, despite South Africa’s current account surpluses. South Africa earns most of the USD that boost its current account from commodity exports, which have seen higher prices over recent periods. Foreign demand for South Africa’s commodities typically drives foreign entities’ demand for the ZAR needed to pay the local mining companies, thereby strengthening the ZAR’s value.

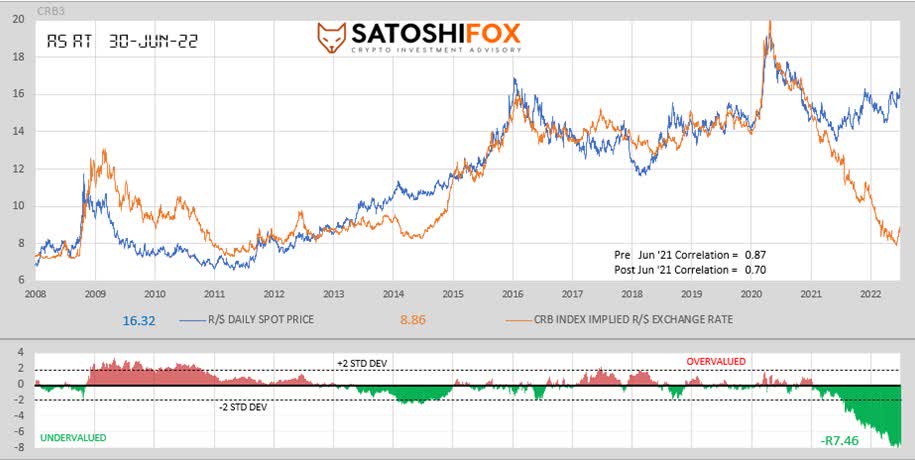

Ironically, this has not been the case over the past year. The magnificent chart 1 below illustrates the recent dislocation in the pricing of the ZAR from its relationship with commodity prices. Clearly, if the ZAR reverts to the long-term relationship, the currency is extremely undervalued at current levels and there is high probability of ZAR strength (or commodity weakness) on the horizon.

{kind=link}

| 1 From Charts ZAR : The Thompson Reuters CRB index explains over 80% of the movement of the Rand (89% before June 2021) in an inverse correlation. This is because South Africa earns most of its Dollars that boost the current account from commodity exports such as coal, iron ore, steel, minerals etc. Foreign demand for our commodities drives demand for Rands from these foreign entities to pay our local mining companies for them and hence strengthens the Rand leading to a lower exchange rate. |

This daily price chart allows us to track the actual ZAR value versus the CRB-implied value taken from the regression equation in chart CRB/R R2. This regression equation is directly applied to daily CRB Index prints to derive an expected ZAR value. If the actual ZAR is much higher than the one expected by the current CRB level, the Rand is considered overvalued. If the actual ZAR is much lower than the one expected by the current CRB level, the Rand is considered undervalued.

The Thomson Reuters/Core Commodity CRB Index is calculated using arithmetic average of commodity futures prices with monthly rebalancing. The index consists of 19 commodities: Aluminum, Cocoa, Coffee, Copper, Corn, Cotton, Crude Oil, Gold, Heating Oil, Lean Hogs, Live Cattle, Natural Gas, Nickel, Orange Juice, RBOB Gasoline, Silver, Soybeans, Sugar and Wheat.

Portfolio company updates

Naspers ( NPSNY )

Naspers and Prosus ( PROSY ) recently published their annual results for the fiscal year ended March 2022. We have long harped on Naspers’ deep discount to its underlying sum of the parts. Earlier this year, the discount dipped as deep as -70%.

I believe part of the discount is due to the market voting with its money against management who have overseen massive value destruction by

- implementing the complex cross-holding Naspers-Prosus structure at exorbitant investment banker fees,

- continuing to invest Tencent proceeds into loss-making new ventures, and iii) being rewarded with eyewatering remuneration packages in the process.

Given this, the recent presentation’s most important message was the signaling that the group is clearly changing course towards unlocking the discount and focusing on shareholder returns.

Naspers/Prosus announced that they are embarking on a massive share repurchase program, whereby they gradually sell shares in Tencent and use the proceeds to buy back Naspers and Prosus shares for as long as the discount persists. The message was clear that they will do “whatever it takes” for “as long as it takes.”

Here is CEO Bob van Dijk responding to a question on the matter:

“…on the last question around capital allocation, I think there are a few considerations here. First of all, given where the discount is, a buyback at scale makes a lot of sense. That’s why the board approved it and that’s why we’re going to allocate this big bazooka program as long as it takes. But I think the world has also changed in the sense that because of rate increases we see the cost of capital go up. I think that’s a reality that just makes the bar higher particularly for external M&A. I think it also means that we need to control our costs, because spending money is more expensive than it was previously. I think the final thing that it means for us, the way I see the next few years, is a period to get our e-commerce business to profitability. That’s the path we’re on.”

The remuneration policy for 2023 is evidence that the board has had enough and is putting its foot down. There will be no increase in base salary for top management in 2023 and no LongTerm Incentives (i.e., no share-based compensation for the year). The only potential performance bonuses relate to Short- Term Incentives, 63% of which are based on closing the discount to NAV. Furthermore, the remuneration policy states, “we believe that a discount reduction only deserves CEO and CFO remuneration if the reduction holds.

The above-mentioned special incentive will be held in reserve until 31 March 2024 and remeasured against a claw-back provision.” As shareholders, we are very encouraged to see this alignment codified. We have been acquiring Naspers as it has gotten increasingly cheap over the past year. This is the catalyst we have been waiting for. Although Naspers’ discount has improved substantially since the announcement, shares are still trading at a discount of roughly -50%. There is still a long way to go.

Argent Industrial ( AILTF )

I have discussed Argent in several of our previous letters and commentaries. As a refresher: Argent is an industrial conglomerate with about 24 underlying operating units across South Africa, the U.S., and the United Kingdom. Operations include steel-based trading, steel product manufacturing, security gates and fences, window shutters, bespoke trolleys for traditional and e-commerce retail, fuel storage and dispensing systems, concrete building products, and roll-over protection bars for construction machinery.

Formerly a low return value trap, the company has been undergoing an unnoticed transformation over the past few years. Since a new strategic shareholder stepped in, Argent has been optimizing cash generation, disposing non-performing assets, acquiring high return assets, and buying back shares.

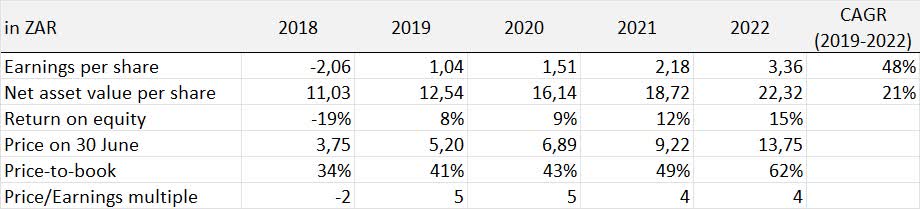

As expected, Argent’s recently reported full year results (for the year ended March 2022) were excellent.

{kind=link}

Over and above the ongoing share buybacks, Argent also declared its first dividend since we acquired our stake in 2019, indicating that these two ongoing programs will return 30% of profits to shareholders annually. Trading at a 4 PE and 62% of book, Argent remains an unappreciated gem.

I asked my colleague, our analyst Hans Koetsier, to do a write-up of his take on Argent, explicitly providing his own view independent of my assessment. His write-up is attached as an appendix to this commentary. We left it mostly unedited to preserve the authenticity. I think he did a great job.

In closing

Risk management and protection against capital loss reign supreme and remain front of mind. We are invested in a portfolio of companies with robust fundamentals, trading at prices that we believe offer sufficient margin of safety. The combination of those two factors equates to embedded upside with lower risk of downside.

I don’t know when returns will manifest, but when they do, they are likely to do so in chunks. Some of our holdings are busy playing out. Naspers’ strong value-unlocking strategy newly in place is already bearing fruit. We had to wait more than a year for the turning point. Other situations have yet to play out. Argent continues to grow earnings per share at way above average rates and their capital allocation is impeccable, but the market is not yet re-rating the price.

Investing demands discipline, patience, and equanimity. As always, I thank you for entrusting Desert Lion with your hard-earned capital. The majority of my wealth is invested in the Fund right alongside you.

All the best,

Rudi van Niekerk

Appendix: Argent Industrial ( Write-up by Hans Koetsier)

Few listed entities manage to pivot from a commodity-type cyclical business into a business that provides sufficient inflationary resistance on its product offering to protect inflation-adjusted returns on capital. Even fewer grow nominal profit after tax at a CAGR of 31% over 4 years whilst maintaining a cash conversion ratio of >100%, dutifully repurchasing 43% of outstanding shares over the same period with effectively no net debt employed in operations.

Almost no business with these characteristics enjoys management with the ability to allocate capital in a manner congruent with shareholders’ interest for prolonged periods of time. If such a business is found, the probability that its operations are focused on an industry as mundane as steel and steel-related products is exceedingly low.

Argent Industrial Limited is an industrial conglomerate with 24 operating units, operative in South Africa (15 units), the United Kingdom (8 units), and, to a lesser extent, the United States (1 unit). These operations include steel-based trading, steel product manufacturing, security gates and fences, specialized trolleys for traditional and e-commerce retail, fuel storage and fuel dispensing systems, concrete building products, roll-over protection bars for construction machinery, and custom-made door and window shutter systems, amongst others.

The product range includes many consumer brands familiar to South African residents, such as Xpanda, Jetmaster, etc. These products inherently enjoy very low risk of technological obsolescence, derisking Argent’s revenue streams, and their largely consumer-facing nature allows the company to pass pricing pressure on to consumers if necessary (e.g., due to inflation).

Argent has not always been the beneficiary of a rational capitalists’ approval – the company had a history of persistent low returns on capital and poor capital allocation, and was exposed to wild fluctuations in profit after tax due to its reliance on steel trading and steel prices. In 2018, the company wrote down excessive amounts of intangibles (book value now represents a fair to conservative reflection of the realizable value of net assets) and commenced a program of optimizing cash generation by disposing non-performing properties, businesses, and other assets and acquiring high-return assets in the UK and South Africa.

This project resulted in Return on Average Equity rising from 4% in 2017, to 16% in the most recent 2022 fiscal period - a direct result of earnings-accretive acquisitions that did not require increased capital employed in maintaining operations. The rapid reduction in issued shares (owing to the launch of an aggressive share repurchase program) allowed shareholders to be double beneficiaries of rational capital allocation, initially on an operational level and subsequently on an ownership level. Since 2019, earnings after tax enjoyed a CAGR of 31% whilst EPS has grown by 48% annually.

In short, management followed William Thorndike’s observations in Outsiders almost to the letter.

A prudent, and somewhat cynical observer would do well to heed the warning Keynes issued in a review of Edgar Lawrence Smith’s book, Common Stocks as Long-Term Instruments , that, “It is dangerous… to apply to the future inductive arguments based on past experience, unless one can distinguish the broad reasons why past experience was what it was”. The fact that Argent’s management team was responsible for the historic persistently low returns on capital has not changed, and they do remain stewards of shareholders’ assets.

However, around 2018, a new strategic shareholder stepped in to expound the virtues of what Munger calls the “cancer surgery” approach. This refers to the process of entering an underperforming business with one (or a few) cash cows which has their collective performance diluted by other low-return businesses, and methodically exiting independent operations that have low-returns. Proceeds from these exits are subsequently re-allocated to high-return operations or returned to owners via dividends or share repurchases. Argent has done both and, in the process, diversified their operations to the United Kingdom, thereby hedging currency risk implicit in the emerging market South African Rand (ZAR). Recent history proves this program was a success, but the sustainability of the approach should be scrutinized.

Management has provided shareholders with good results since employing the new strategy, having achieved a tripling in share price over the past 5 years (without enjoying any valuation margin expansion – the company trades at a 4 PE ratio at the time of this writing). Common sense dictates that past results would be incentive enough to ensure continued managerial compliance with the newly instituted policy of rational capital allocation. However, success often breeds complacence.

Therefore, an institutionalized incentive structure is often required to ensure that the program is sustained. The group’s remuneration policy provides long-term incentives to executive management based on what is termed “Group Value Unlock” with the objective “To unlock inherent value within the group companies and properties by selling, partnering or realigning entities to extract funds for offshore acquisition or paid out as dividends.”

Such dividends include cash dividends and share repurchases, of which 30% of annual earnings is set aside bi-annually, exclusively for this purpose. The policy contains provisions which allow executive directors to be awarded for achieving sales values that exceed realizable net asset values as carried on the statement of financial position. In the short term, profitability bonuses are allocated based on reasonable outperformance of profitability targets that we agree with.

The above narrative is unnatural for an analyst tasked with fishing out disconfirming facts and evidence that negates a portfolio manager’s initial investment thesis. Argent is a nightmare for an analyst tasked with uncovering patent or latent weaknesses or risks inherent in the business’ operations. However, there do remain risks associated with the continued success of management’s operational and capital allocation competence.

Argent is trading at a low valuation, which increases the level of managerial conviction shareholders require as justification for purchasing new business units at higher valuations. A loss of focus in the acquisition strategy could have further tangible effects on future returns on employed capital. We maintain a schedule on the performance of all previous acquisitions made since 2018 and, so far, they have all been earnings- and value-accretive.

Furthermore, all UK and SA acquisitions have been in-line with management’s industry expertise. The ability to raise prices of consumer-facing products has not been stress tested; however, management remains adamant that they are positioned well for an inflationary environment.

The collective performance of Argent’s shareholders will be a product of management’s ability to continue to execute on their promises of selling redundant or low-return assets, finding earnings accretive acquisition targets, and continuing with share repurchases at reasonable valuations or, alternatively, by returning excess funds via cash dividends. These metrics will be closely monitored.

{kind=link}

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Desert Lion Capital June 2022 Commentary