DBI - Despite The Pain Shares Of Caleres Are Still Logical To Consider

2023-11-15 21:58:06 ET

Summary

- Caleres, a specialty retailer in the footwear market, has seen a decline in revenue and profits due to cautious consumer spending and lower store traffic.

- Despite the negative financial performance, CAL stock is still cheap compared to similar firms, making it a solid prospect for investors.

- Management forecasts continued revenue and earnings growth in the coming years, which could lead to an attractive upside for the stock.

Generally speaking, I try and stay away from the clothing and apparel market. I find it to be highly competitive, with low margins, and you are stuck dealing with the fickle and ever-changing attitudes of consumers. But there is one niche in this space that I do find intriguing. And that is in the footwear market. One company that I have seen do incredibly well over the past couple of years in this space is Caleres ( CAL ), a specialty retailer most well-known for its ownership of the Famous Footwear brand.

Since I last wrote a bullish article about the company in October of last year, shares have seen upside of only 2.7% compared to the 19.8% increase seen by the S&P 500 over the same window of time. But I have been following the company for longer than that. Since my first bullish article on the company in March of that same year, shares have seen upside of 29.4% compared to the 0.4% rise the S&P 500 exhibited. So in the grand scheme of things, I seem to be doing alright. The big question investors would be wise to ask, however, is how much additional upside might be warranted after such a meaningful amount of upside in such a short window of time. Given how cheap the stock is, not only on an absolute basis but also relative to similar firms, I would argue that it is still a solid prospect at this time. Though investors would be wise to keep a close eye on fundamentals since the picture is changing in a negative way for the firm.

The picture is worsening, but that's okay

When it comes to the retail footwear market, Caleres is a rather sizable company. According to management, the firm boasts a 22% market share in the shoe chain space, with that market share growing to 28% when focused on only kids' shoes. The company boasts 860 stores in operation and it generates a rather impressive 14% of its revenue from online activities. In recent quarters, growth achieved by the company has come under pressure even though financial performance up until the current fiscal year has been very solid.

{kind=link}

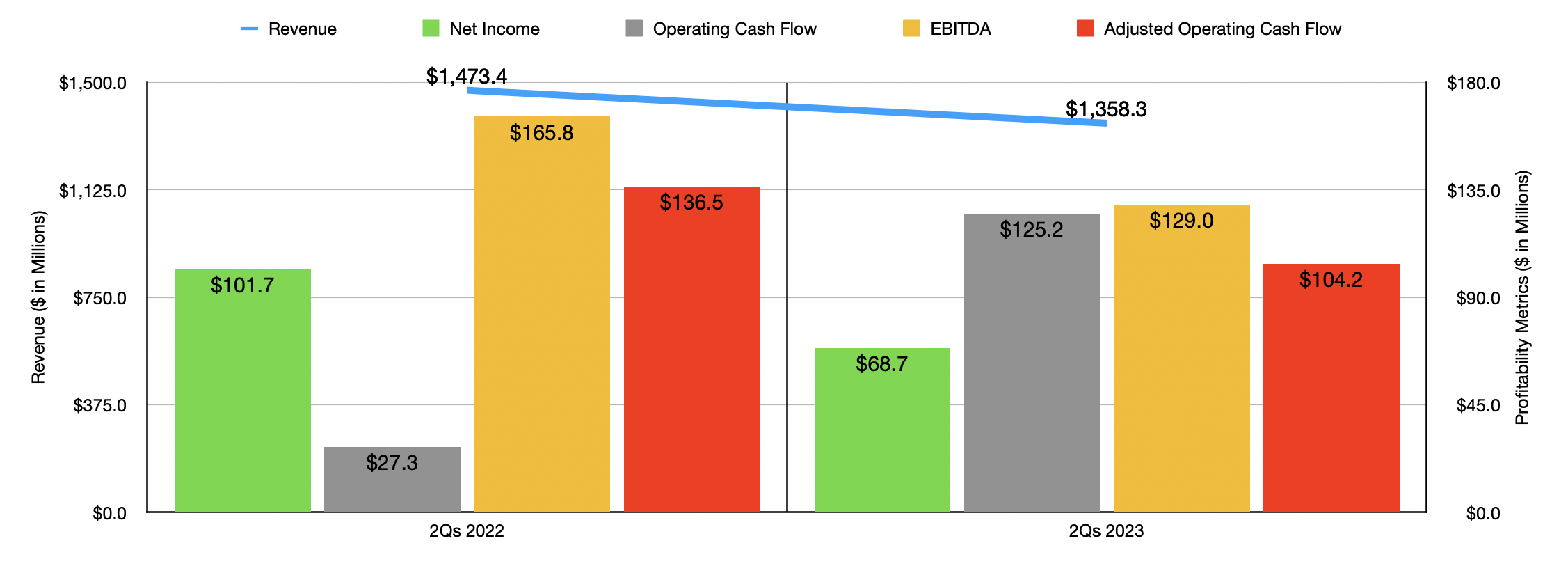

In the first half of the 2023 fiscal year , for instance, the company reported revenue of $1.36 billion. That's 7.8% lower than the $1.47 billion the company reported the same time last year. Management blamed this decline on 'cautious consumer spending' that resulted in a reduction in traffic in its retail stores. In fact, comparable store sales in the first half of this year were 6.3% lower than they were at the same time last year. This decline in revenue is something that the company will likely continue dealing with for the rest of 2023. I say this because management is currently forecasting revenue of $2.80 billion for the year. That's down from the $2.97 billion generated in 2022. As bad as this is, it becomes worse when you consider that this year will be one of the years in which the company has an extra operating week. If it weren't for that, revenue would be even lower year over year.

On the bottom line, the picture has been even worse. Net profits plunged from $101.7 million to $68.7 million. The drop in revenue certainly didn't help. However, the company was also negatively affected by a jump in selling and administrative costs from 36% of sales to 38%. That increase, according to management, was driven mostly by deleveraging of expenses caused by lower net sales. Unfortunately, other profitability metrics for the company have also worsened. Operating cash flow did skyrocket from $27.3 million to $125.2 million. But if we adjust for changes in working capital, we would see a decline from $136.5 million to $104.2 million. Meanwhile, EBITDA for the company fell from $165.8 million to $129 million.

If management is correct, earnings per share this year should come in at between $4.02 and $4.22, while adjusted earnings per share should be between $4.10 and $4.30. I would say that the adjusted earnings are a more appropriate measure of the company's success. At the midpoint, this would translate to $144.1 million in profits. No guidance was given when it came to other profitability metrics. But based on my own estimates, adjusted operating cash flow should be around $193.6 million while EBITDA should come in somewhere around $218.9 million.

{kind=link}

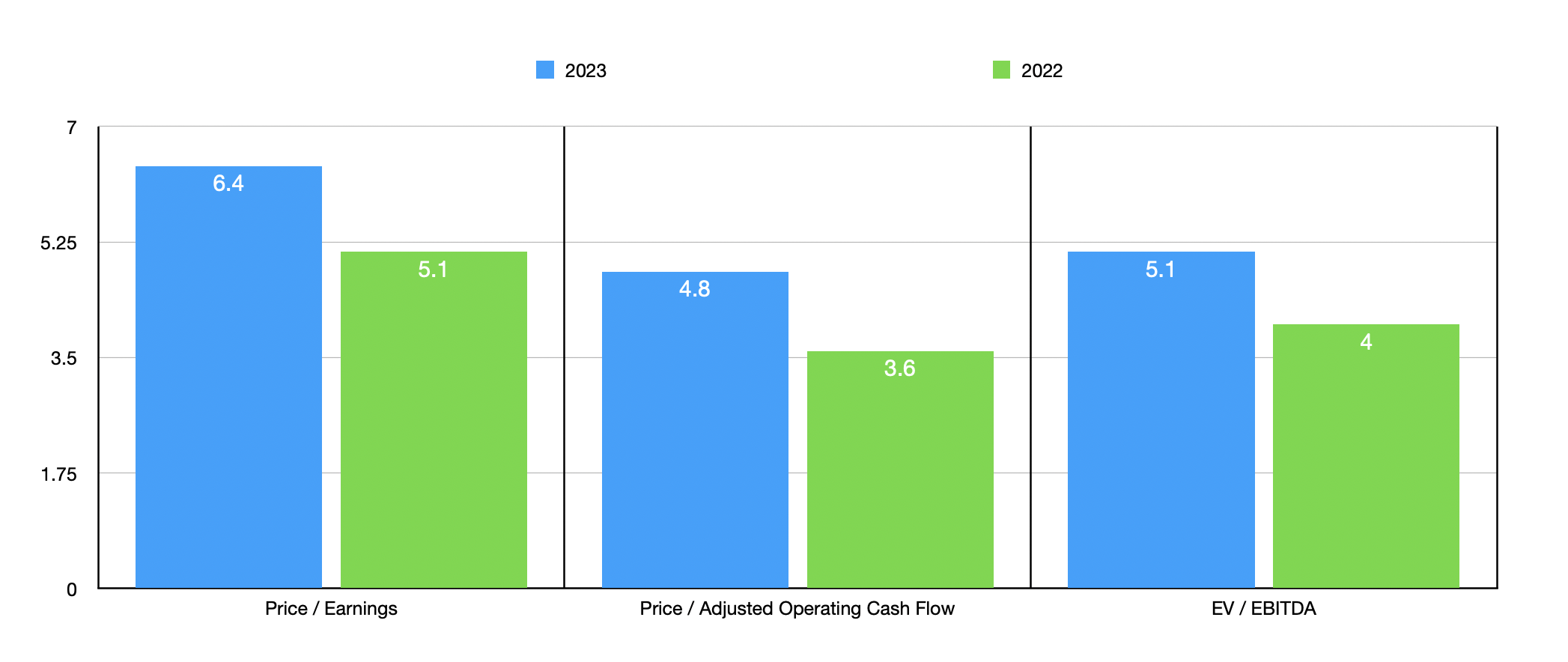

Using these estimates, I would like to point you to the chart above. In it, you can see how shares are priced both on a forward basis and using data from 2022. Naturally, shares are more expensive on a forward basis because of the aforementioned issues. But in the grand scheme of things, the stock still looks quite attractive. In the table below, I also compared the company to five similar firms. On both a price to earnings basis and price to operating cash flow basis, only one of the five companies was cheaper than Caleres. Using the EV to EBITDA approach, this number increases modestly to two.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Caleres |

| 6.4 |

| 4.8 |

| 5.1 |

| Shoe Carnival ( SCVL ) |

| 6.8 |

| 9.6 |

| 3.8 |

| Boot Barn Holdings ( BOOT ) |

| 13.0 |

| 7.1 |

| 8.2 |

| Designer Brands ( DBI ) |

| 4.9 |

| 2.1 |

| 4.0 |

| Skechers U.S.A ( SKX ) |

| 14.5 |

| 6.5 |

| 7.9 |

| Steven Madden ( SHOO ) |

| 15.3 |

| 9.2 |

| 10.0 |

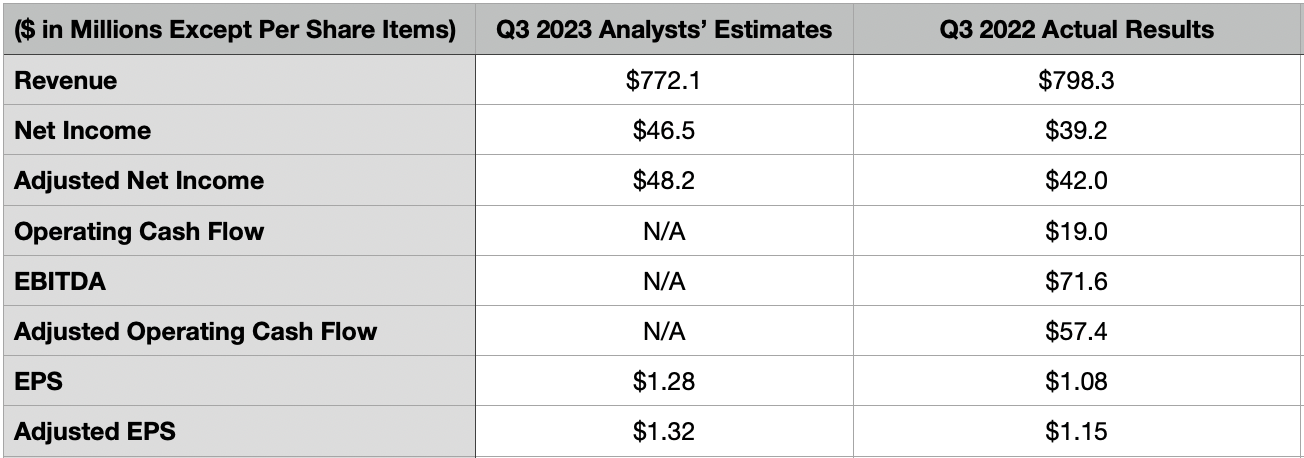

Of course, it's important to keep in mind that conditions can change. And on November 21st of this year, management is expected to announce financial results covering the third quarter of the company's 2023 fiscal year. That would be the ideal time for some change to be announced if it is going to be. Luckily, we have forecasts provided not only by analysts but also by management. Analysts, for starters, believe that revenue will come in at around $772.1 million. This wouldn't be surprising when you consider that management is forecasting a revenue drop in the low single digit range from the $798.3 million the company reported in the third quarter of last year.

{kind=link}

In terms of profits, analysts anticipate earnings per share of $1.28 and adjusted earnings per share of $1.32. That would stack up against the $1.08 and $1.15, respectively, that the company generated in the same quarter of last year. This is interesting because I would not anticipate a drop in revenue to correspond with higher profits. And yet, management also remains optimistic. They are forecasting earnings per share of between $1.25 and $1.30, with adjusted earnings coming in at between $1.30 and $1.35 per share. In the table above, you can see what each of these estimates it would translate into based on the company's current share count. Management did not provide guidance when it came to other profitability metrics. Neither did management. But the important ones that investors should be paying attention to when earnings do come out can be seen in the aforementioned table.

Takeaway

Based on the data provided, I understand why investors might be souring on Caleres. Revenue, profits, and cash flows have all taken a beating recently. In the near term, that could continue to weigh on the stock. But the good news is that shares are still very cheap and management believes that they can continue to grow revenue through 2026 at an annualized rate of between 3% and 5%, with earnings per share growing at an annualized rate over the same window of time of between 11% and 13%. Even if half of that growth occurs, shares are cheap enough to warrant attractive upside. And because of that, I have decided to keep the business rated a 'buy' for now.

For further details see:

Despite The Pain, Shares Of Caleres Are Still Logical To Consider