DB - Deutsche Bank: Downgrade To Buy As Profit Waiting To Improve In Q3

2023-10-10 13:11:39 ET

Summary

- Deutsche Bank gets slight downgrade to Buy rating from Strong Buy in June.

- Strengths: undervaluation, revenue YoY growth, capital and liquidity position, share price still appears cheap, price outperformed S&P 500.

- Offsetting factors: no steady quarterly dividends and YoY drop in profitability.

- The downside risk of loan-loss provisions increasing has been addressed.

Analysis Summary

Today I'll be covering Deutsche Bank ( DB ) , in the financials sector, subsector of diversified capital markets.

According to its Seeking Alpha profile , it trades on the NYSE, is globally based in Frankfurt Germany, and offers corporate and investment banking, and asset management products and services to private clients, corporate entities, and institutional clients worldwide.

I think it fitting to mention that it has a major US presence, with a huge building right on Wall Street. While visiting one of their trading desks there some years ago, it was evident just how large of an operation they have in New York, and just blocks away from the stock exchange.

One of its listed peers is State Street ( STT ), another firm I have covered on this portal before.

My last coverage of Deutsche Bank was over 4 months ago in early June, when I gave it a strong buy rating. Since then, the share price went up 2.10% , so I would say I called it correctly back then. However, the question then became would it hold up after my updated rating methodology this fall?

Deutsche Bank - price since last rating (Seeking Alpha)

In today's article, it turns out I gave this stock a buy rating, due to having more strengths in my review than offsetting factors, to be exact 5 strengths and 2 offsetting factors. This is a slight downgrade from the strong buy rating I gave it last time, but still bullish.

Its strengths include undervaluation, revenue growth, capital and liquidity strength, cheap share price vs moving average, outperformance vs S&P500.

Its offsetting factors include lackluster dividend growth and YoY drop in net income and EPS.

A downside risk to my bullish outlook is a trending increase in provisions for credit losses, which will be discussed at the end.

Methodology

My updated rating methodology as of October 2023 is to analyze the stock holistically across the following 7 categories of equal weight, and if it has more strengths than offsetting factors it gets a buy rating, otherwise will get a hold or sell rating:

dividends, valuation, revenue growth, net income and EPS, capital and liquidity, share price vs moving average, performance vs S&P 500.

All data sources come from publicly available info such as the most recent quarterly report and company presentations, Seeking Alpha data, and media reports. The next anticipated quarterly earnings release, according to Nasdaq data , is expected on Oct. 25th for fiscal 2023, Q3. The most recent one was on July 26th for fiscal Q2.

Dividends

When it comes to dividends , the firm does not pay a regular quarterly dividend and the last annual one seems to have been back in May, so new investors would have to wait quite a while to get the next one, if the company decides to pay it.

{kind=link}

Further, the 10 year dividend growth chart is lackluster at best, in my opinion, not showing a steady growth trend as I have seen in some financial stocks lately.

{kind=link}

Based on the evidence, I consider the category of dividends an offsetting factor for this stock, on the basis of lack of steady quarterly payouts and lackluster dividend growth over the last decade.

Valuation

To simplify analyzing the valuation, I have chosen a single metric to focus on, and that is the price-to-earnings ratio (P/E) , both the trailing and forward P/E, as it tells me what the market is pricing this stock at in relation to its earnings.

My portfolio goal is to find a valuation lower than or close to the sector average, but not too much higher. Sometimes a stock is undervalued but otherwise has strong fundamentals, so that is a company I want to uncover.

Deutsche Bank - PE ratio (Seeking Alpha)

In the case of this stock, the trailing P/E is 4.26, which is 54% below the sector average , and the forward P/E of 6.34 is 32% below the sector average.

Hence, I would consider this stock considerably undervalued compared to its industry, both on a trailing and forward basis.

If you compare its valuation to that of its peer I mentioned earlier, State Street , that firm's forward P/E is almost 6% higher than the sector, so it is a significantly higher valuation than Deutsche Bank.

What could be driving the low valuation for Deutsche? I think we will have to look more closely at the share price trend and earnings, which I will discuss shortly.

Based on the data, I think this valuation metric is a strength for this stock, as I am preferential usually to undervalued stocks.

Revenue Growth

One topic many analysts and investors look at is the top-line revenue growth, as a metric tracking revenue generated before expenses, to put it simply.

Manageable growth is important, in my opinion, because companies have competition and are striving to capture market share in their sector.

For this company, we can see from the most recent quarterly results that it achieved a YoY increase in total revenue :

{kind=link}

At first glance, I think this is a plus for this company.

In looking further at revenue growth by different segments, we see the following results in the most recent reported quarter:

While interest income YoY did show growth, according to the income statement , which I think is due to the elevated rate environment benefitting this firm's interest-earning assets, it also drove growth in interest expense as well, however the net interest income still was able to claw through and achieve YoY growth:

{kind=link}

Other income such as from the trading desk, selling of assets, and so on, also did well on a YoY basis so it is worth calling out:

{kind=link}

Overall, I think the data shows that top-line revenue YoY growth is a strength for this stock's rating, and also I would say the elevated rate environment will continue to benefit that part of the top-line revenue going forward into Q3.

Net Income and EPS

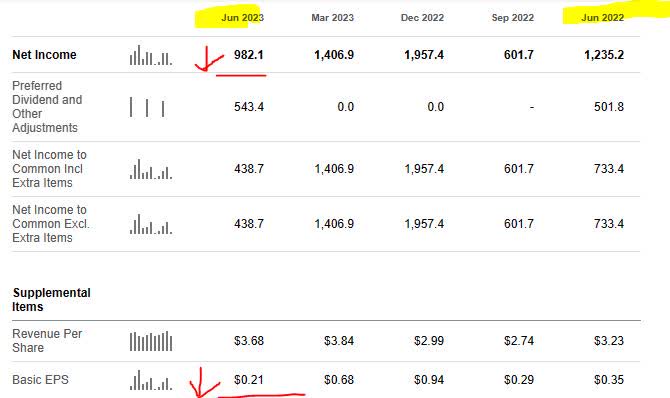

Net income and earnings per share are getting their own section here to make the analysis easier to understand and to separate these results from top-line revenue. However, the bottom-line numbers recently have been less rosy than the top-line figures.

Based on the most recent quarterly results available, profitability seems to have taken a hit in Q2 as this firm achieved a YoY drop in net income and the basic earnings per share "EPS" decreased on a YoY basis .

{kind=link}

I also want to call out the following from the company's Q2 earnings report comments which speaks to elevated tax rates as partly the cause of the headwinds:

Second quarter post-tax profit was € 940 million, compared to € 1.2 billion in the prior year quarter, partly reflecting an effective tax rate of 33%, compared to 22% in the prior year quarter.

Here is how it looked in their Q2 graphic showing the income statement highlights, and pointing to both a YoY and QoQ drop in profit:

Deutsche Bank - YoY profit (company Q2 results)

I think, therefore, that this category of net income and EPS is an offsetting factor for this stock's rating, despite strong top-line revenue growth figures, and this will be an area needing improvement for Q3.

Capital and Liquidity

Here we'll focus on one or more items related to capital and liquidity strength of this stock's parent company.

The following is relevant data from the company's Q2 quarterly presentation :

We can see the CET1 ratio, a key metric tracked in the banking sector, has gone up in Q2 and remains well above regulatory minimums at 13.8%.

Deutsche Bank - CET1 ratio (company Q2 presentation)

Addition data of interest is the firm's forward outlook on returning capital to shareholders:

Delivering on capital distribution plan with share buybacks of up to € 450MM in H2; reaffirming FY 2021-2025 capital distribution plans.

From its balance sheet , the company ended Q2 with $163.7B in cash, $1.4T in total assets, and $1.3T in total liabilities, leaving $79B in positive equity.

I think that this data adds confidence to this stock's rating, backed up by strong company financial health.

Based on the evidence found, I consider this firm's capital and liquidity situation a strength to its overall rating.

Share Price vs Moving Average

Now we've come to the part where I like to talk about the share price and whether I think it's a buying opportunity right now or not.

First, let's take a look at the share price and 200-day moving average ((SMA)) as of the writing of this article:

The share price of $10.70 is 3.6% below the 200-day SMA which stands at $11.10 . I think this moving average is a good long-term trend indicator which is why I track it.

In my portfolio goal, I am looking for crossover opportunities, where the price crosses below the moving average after a period of bullishness, which I consider a buy signal as long as other fundamentals are strong. However, a buy opportunity could also exist if the price is hovering around the moving average.

The chart shows a crossover already occurred this summer, followed by a bearish trend, so to test the share price against my portfolio goals I created the following simulated trade scenario. I buy 100 shares at the current price, hold 1 year, and want to achieve at least a 10% or better (unrealized) capital gain at that time.

In addition, in anticipation of losses as well, I have set my maximum loss tolerance as -20% (unrealized capital loss).

{kind=link}

The above simulation shows two scenarios, one where the future share price rises +15% above the current 200 day SMA, and the other where it drops -15% below the SMA.

The outcome of both scenarios is that they are in line with my goals for gains and losses, since the first scenario projects a capital gain of 19.3% and the second scenario projects a capital loss of -11.82% in a year's time.

Based on this simulation, I think the current share price is a strength, and presents a value-buying opportunity on this stock.

Though your portfolio strategy may differ, consider this section a general and simplified framework with which to think about this stock in a longer-term sense, in which time one can expect potential gains as well as losses, so establishing a maximum risk tolerance is important.

Performance vs S&P 500

The following is a comparison of the 1-year price performance of this stock vs the S&P 500 index. I have included this metric in my updated rating methodology so as to compare this equity to a major market index that is tracked often, and whether it was able to outperform it or not.

I consider this relevant because it shows the market momentum for this stock. It may be a great company fundamentally, the market reality is that other investors influence the share price based on demand for the stock, so comparing it to this major index could add some clues as to market sentiment.

{kind=link}

The data shows the stock outperforming vs this index , and doing so for the entirety of this period being tracked, which I consider a strength to my rating, as I believe it to indicate a bullish market sentiment for this stock.

Risk to my Outlook

A downside risk to my bullish outlook would be the trend showing increasing provisions for credit losses:

Deutsche Bank - provisions for credit losses (company Q2 presentation)

Since this is an item that anticipates an increase in bad debt, but also can impact business results as it is an expense, it may cause bearishness on this stock among investors and analysts especially if the trend continues in Q3.

A June article by financial media CNBC highlighted a rising trend in corporate defaults, and we know that Deutsche Bank does a heavy amount of business with institutions and large companies.

According to the article:

Corporate defaults rose last month, with 41 in the U.S. so far this year. That's more than double the same period last year, according to Moody's Investors Service.

Companies are defaulting on their debt due to uncertain economic conditions and heavy debt loads. High interest rates have made it difficult to refinance, as debt is more expensive.

However, my counterargument as to why I continue to be positive about this stock is that I think the "rate shock" of the last year is hitting a plateau and leveling off. According to rate-watching tool CME Fedwatch , predictions are 73% that the Fed will keep its policy rate the same after its November meeting and not hike it further.

Also, since Deutsche is one of the Financial Stability Board's listed global systematically critical banks , I think it has the capacity and scale to take a hit on some bad debt and still come back swinging.

In closing, my bullish sentiment on this stock remains and my buy rating stands.

For further details see:

Deutsche Bank: Downgrade To Buy As Profit Waiting To Improve In Q3