DB - Deutsche Bank: Not Much Upside Ahead

2024-01-07 09:50:40 ET

Summary

- Deutsche Bank's recent financial performance has improved, but its shares remain cheap due to low profitability.

- The bank's revenue and earnings have generally beaten street estimates, supported by rising interest rates and growth in corporate and private banking.

- However, Deutsche Bank's net interest margins have remained relatively unchanged, and its cost-to-income ratio is still high compared to peers. The bank may struggle to achieve its financial targets in the short term.

Deutsche Bank ( DB ) has improved its performance in recent quarter supported by rising rates, a trend that is expected to reverse in the near future. While its shares remain cheap compared to other European banks, this is justified by the bank’s low profitability level.

As I’ve covered in a previous article , Deutsche Bank is historically one of the European banks trading systematically at a low valuation multiple, measured by its price-to-book value multiple that is usually at a deep discount to the sector’s average multiple. This is to a large extent justified by the bank’s fundamental issues, but its financial performance in recent years has clearly improved, something the market has not given much credit for in recent months.

Since my last article on Deutsche Bank, its shares are up by more than 12%, a performance that is very close to the European banking sector, but slightly below the market (S&P 500 index) during the same period.

Article performance (Seeking Alpha)

In this article, I analyze the bank’s most recent financial earnings and update its investment case, to see if it remains an interesting value play or not.

Earnings Analysis

Deutsche Bank has reported an improved financial performance in recent years, supported by better activity levels in the investment banking business following the pandemic, and rising interest rates in Europe since mid-2022. This positive operating trend was maintained during the first nine months of 2023 , especially in the corporate and private banking segments, while the investment banking and asset management activities reported a weaker performance.

As shown in the next graph, the bank has generally been able to beat street estimates regarding both revenue and earnings, showing that its business has performed relatively well in the recent past.

Earnings surprise (Bloomberg)

In 9M 2023, Deutsche Bank’s revenues amounted to €22.2 billion, an increase of 6% compared to the same period of the previous year, supported mainly by rising interest rates. Indeed, over the past few quarters, Deutsche Bank’s corporate and private banking units were the major growth engines, as shown in the next graph.

Revenue (Deutsche Bank)

However, despite strong revenue growth in its corporate banking segment, up by 24.5% over the last twelve months compared to 2021, overall group revenues increased by only 6.9% (last twelve months compared to 2021), showing that Deutsche Bank is not among the banks more geared to interest rates.

This happens because its largest unit was investment banking, which is much more exposed to volumes in the capital markets to generate revenues rather than the level of interest rates. Nevertheless, due to stronger revenue growth both in the corporate and private banking segments compared to investment banking and asset management, the bank’s business mix has changed somewhat in recent quarters.

Indeed, over the last twelve months to the end of last September, its private banking unit has become the largest one within the group, increasing its weight on total revenues to 34%, while investment banking reduced its weight from 37%, to 31%.

Revenue mix (Deutsche Bank)

This gives Deutsche Bank a more balanced business profile and less reliant on capital markets, which is positive for a more predictable and recurring business model over the long term.

On the other hand, while higher interest rates led to higher net interest margins ((NIM)) across European banks with activities more geared to retail and commercial banking, Deutsche Bank’s NIM has remained relatively unchanged in recent quarters, which is not a positive outcome. This is explained both by a slightly lower asset base and rising cost of deposits, showing that Deutsche Bank’s deposit beta is quite high and the bank was not able to gain as much from rising interest rates as other European banks.

NIM (Deutsche Bank)

Moreover, due to the inflationary environment and cost pressures, Deutsche Bank has not reported much operating leverage, given that total expenses in 9M 2023 were €16.2 billion, up by 6.6% YoY. This includes significant restructuring and litigation costs, amounting to some €900 million, thus adjusted for this its cost base increased by only 2% YoY, which is a more acceptable result, but its cost-to-income ratio based on adjusted costs was 73% in 9M 2023, still a very high ratio compared to its peers.

The bank acknowledges that its cost-to-income ratio is quite high and targets a 62.5% ratio by 2025, but based on its track record and the prospects of lower interest rates ahead, I think it’s quite likely that Deutsche Bank will fail to achieve this key financial target in the short term.

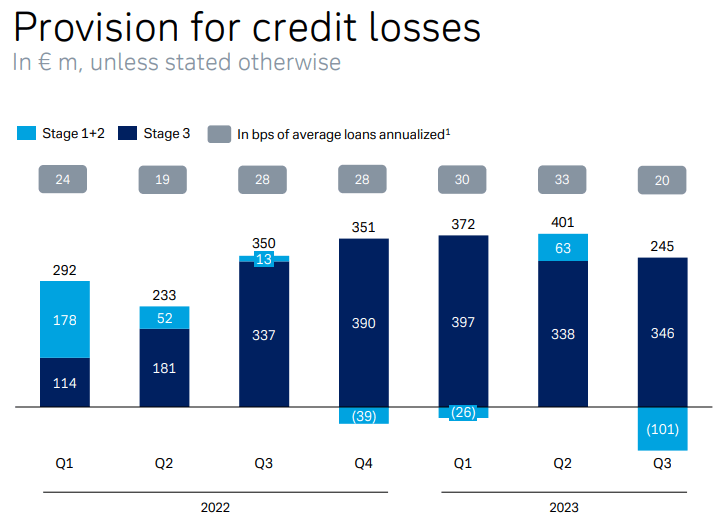

Regarding asset quality, it remained quite good in recent quarters, while some deterioration was expected due to an economic slowdown in Europe, higher interest rates, and higher energy costs in Germany that were likely to pressure small and medium-sized companies in the country. Despite this background, the bank’s credit quality has remained solid, as the bank’s provisions were relatively stable over the past few quarters, as shown in the next graph.

{kind=link}

For the full year, the bank expects its cost of risk ratio to be around 25-30 basis points, which means provisions in Q4 are not expected to much different compared to the previous quarter, a strong signal that Deutsche Bank is not seeing higher loan defaults in recent months.

Despite the benefit of higher revenues, higher operating costs plus non-recurring effects, namely litigation and restructuring costs, led to a lower net income in 9M 2023 compared to the same period of last year. Its net profit was slightly above €3 billion in 9M 2023, and its reported return on tangible equity (RoTE) ratio was 7% (vs. 8.1% in 9M 2022).

As I’ve discussed in a previous article on BBVA ( BBVA ), I expect interest rates to decline gradually during 2023 and inflation is clearly slowing down and the economic outlook in Europe is not great, thus interest rates are expected to be turned into a headwind for Deutsche Bank in 2024. This obviously does not bode well for its revenue and earnings growth ahead, plus provisions are also expected to increase somewhat given that there is a lag between the time interest rates start to rise and its negative impact on credit quality.

This doesn’t seem to be reflected currently on street estimates , given that Deutsche Bank’s revenues are expected to grow to €29.4 billion in 2024 (vs. close to €29 billion in 2023), something that may be difficult to achieve if interest rates decline significantly over the coming months. Regarding provisions for loan losses, current estimates expect a slight increase in 2024, which seems sensible, to more than €1.4 billion in the year (vs. €1.2 billion in 2023).

This means that for Deutsche Bank to report earnings growth in 2024, it needs to cut costs in a meaningful way, something that in the past has failed to do several times, thus it’s quite likely that Deutsche Bank’s net income and profitability level will decline in 2024, compared to the previous year.

Conclusion

Deutsche Bank remains one of the cheapest banks in Europe, measured by its price-to-book value multiple of only 0.38x, compared to more than 0.8x book value for the European banking sector. While at the beginning of 2023, rising interest rates were a strong tailwind for revenue and, potentially, earnings growth, the bank’s performance has not been impressive, and its shares have not re-rated as I was expecting.

Now that rates seem to have reached a peak and can, probably, come down over the next few quarters, Deutsche Bank’s upside potential seems limited right now, given that there aren’t much catalysts for a higher share price in the near term and its cheap valuation is justified by Deutsche Bank’s structurally weak profitability level.

For further details see:

Deutsche Bank: Not Much Upside Ahead