EXPD - Deutsche Post AG: Q4 Earnings Report Confirms The Bull Thesis

2023-03-09 19:50:20 ET

Summary

- Deutsche Post AG published its Q4 2022 and full year 2022 numbers today and announced a dividend hike.

- For the full year, Deutsche Post revenue grew 15% to €94.4B while EBIT increased by 6% to €8.4B.

- Management made clear that Deutsche Post profited significantly from higher air and sea freight rates, which won't continue this year as rates are about to normalize.

- This year's outlook is below last year's results, but still reasonable compared to the current valuation Deutsche Post stock trades at.

- Considering the outlook, chance, risk segment, and valuation, I rate Deutsche Post AG as a buy.

Thesis

Deutsche Post AG ( DPSTF , DPSGY ), the world's greatest carrier, published its full-year 2022 numbers today, which looked fantastic. Revenue grew by over 15% to €94.4B, and EBIT grew by 6% to €8.4B. Both are all-time highs for the Company. Accordingly, the dividend was raised , and the share buyback program was raised from €2B to €3B.

According to Deutsche Post AG management, the economy won't favor them in 2023 as it did in 2022. They, therefore, lowered their guidance to an EBIT of €6-7B. Even though the guidance is substantially lower than last year's results, the stock's valuation and the long-term outlook give us further upside potential. Accordingly, I rate Deutsche Post AG stock a buy.

Q4 2022 results

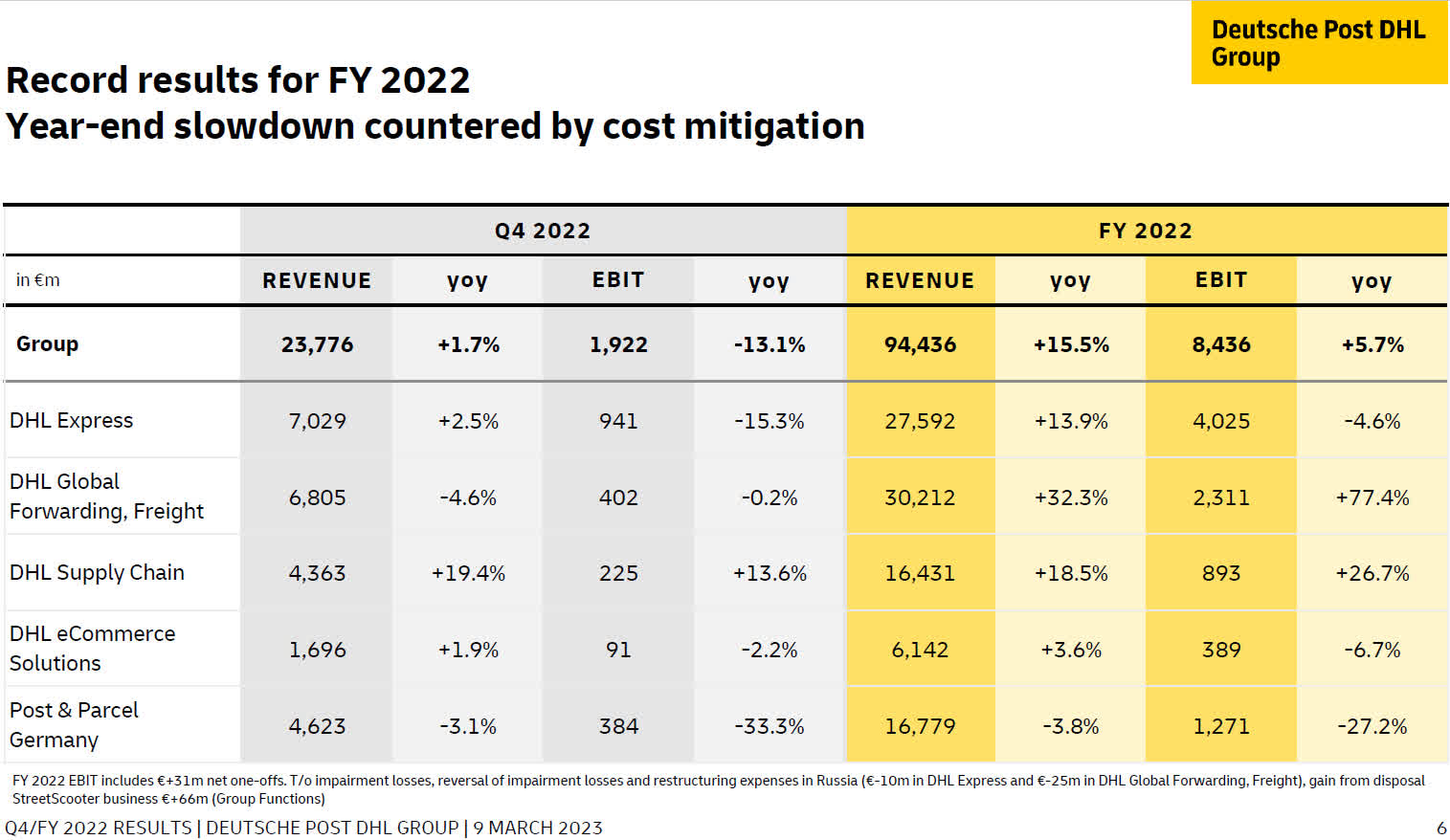

Deutsche Post's results were primarily driven by its international business, as the following chart shows:

{kind=link}

DHL Global Forwarding, Freight was responsible for 32.3% of revenue and 77.4% EBIT growth. While revenue increased in every segment but Post & Parcel Germany, EBIT growth decreased in three out of five segments. Considering this, it's even more impressive that DHL Global Forwarding, Freight grew by 77%, and DHL supply chain grew by 26.7%.

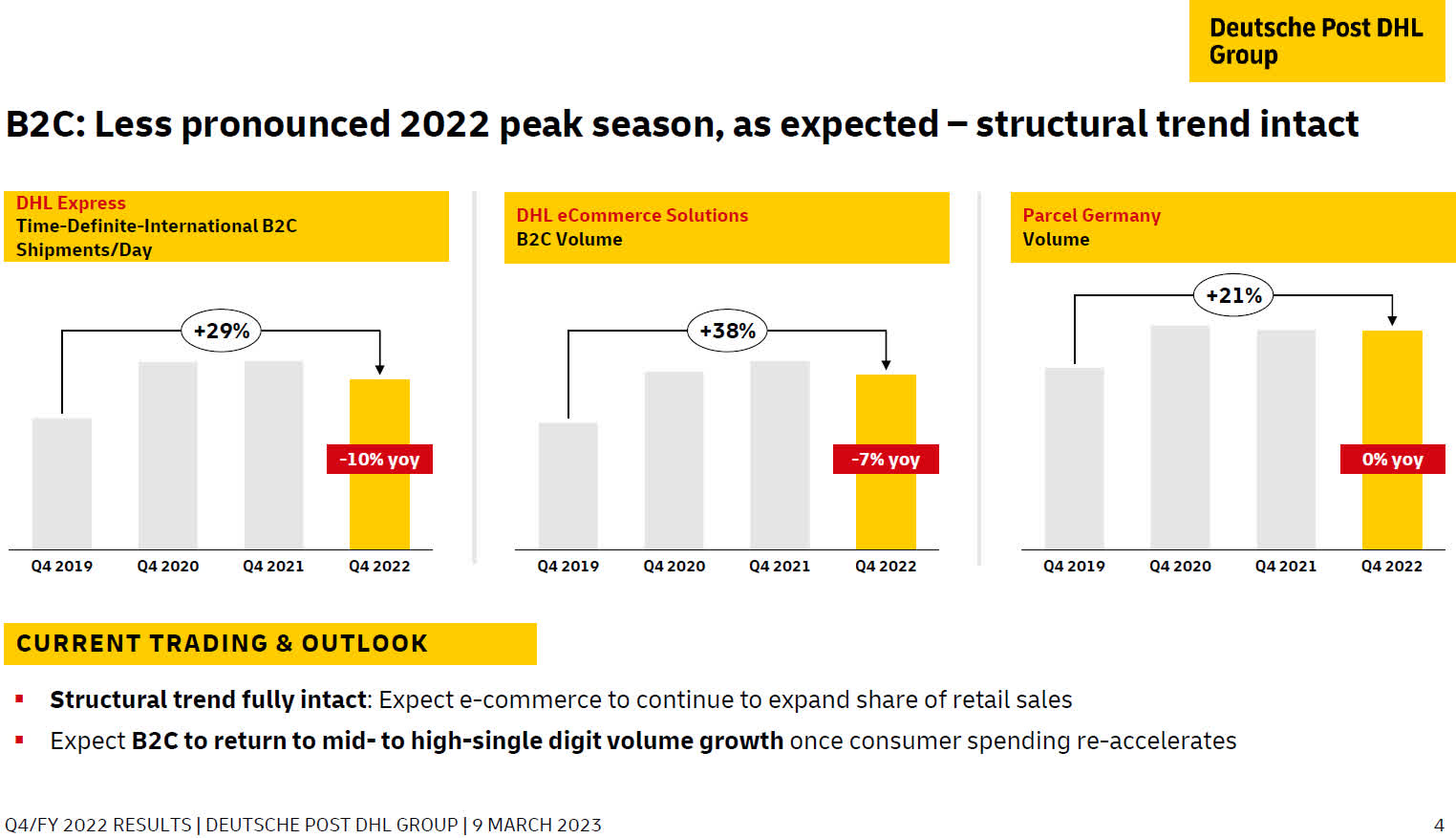

A headwind was declining volume YoY. That isn't surprising, since 2020 and 2021 were exceptionally strong years due to covid related lockdowns. To give a covid-adjusted picture of volumes, the Deutsche Post included the growth from 2019 to 2022 in the following chart:

{kind=link}

A 10% and 7% decline is in line with what I would expect from a normalization back from the covid-related volume spike. Interesting to see is that the parcel volume in Germany is flat YoY. According to the management, the structural trend is fully intact, meaning that e-commerce is further expanding its market share of retail sales. The business-to-customer segment is expected to return to mid-to single-digit growth, up from -7% in 2022. This will be highly dependent on whether we see a severe recession or not. Especially because Deutsche Post operates mostly in Europe.

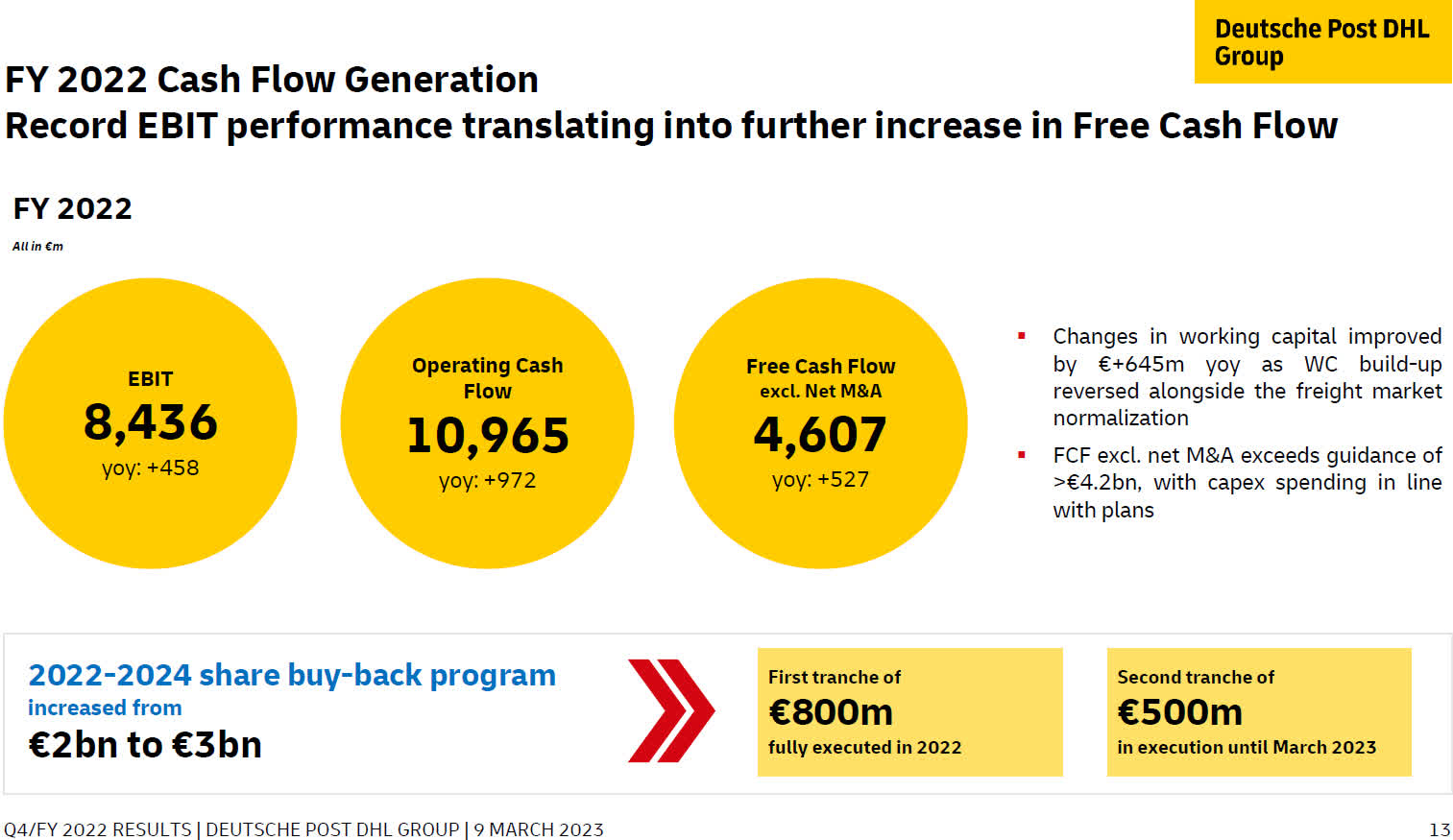

In addition to EBIT, we also care about the cash flow generation, especially because Deutsche Post is considered a dividend stock.

{kind=link}

Deutsche Post did well in turning revenues into cash flow. Operating cash flow increased by 9.7% YoY, while free cash flow grew even more to €4.6B - a 12.9% increase YoY. The management uses the cash flow to increase their working capital by €645M and raise the stock buy-back program from €2B to €3B between 2022 and 2024.

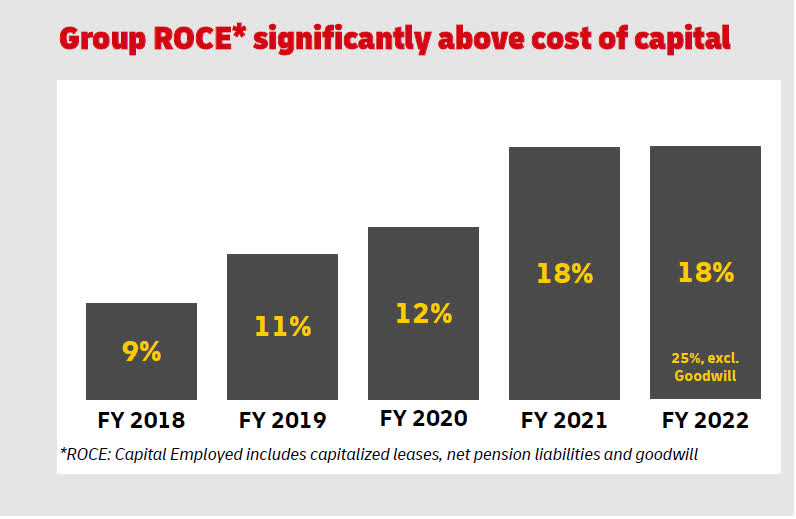

Profitability was flat YoY, so no change to 2021, but still good.

Deutsche Post return on capital employed (ROCE) (Deutsche Post IR)

{kind=link}

For every €1 the Deutsche Post employs, they get €1.18 back. That is significantly higher than before covid, when the ROCE was just 12%. I like to see that profitability held up in a year of high inflation, like 2022, when we had over 10% inflation in Germany.

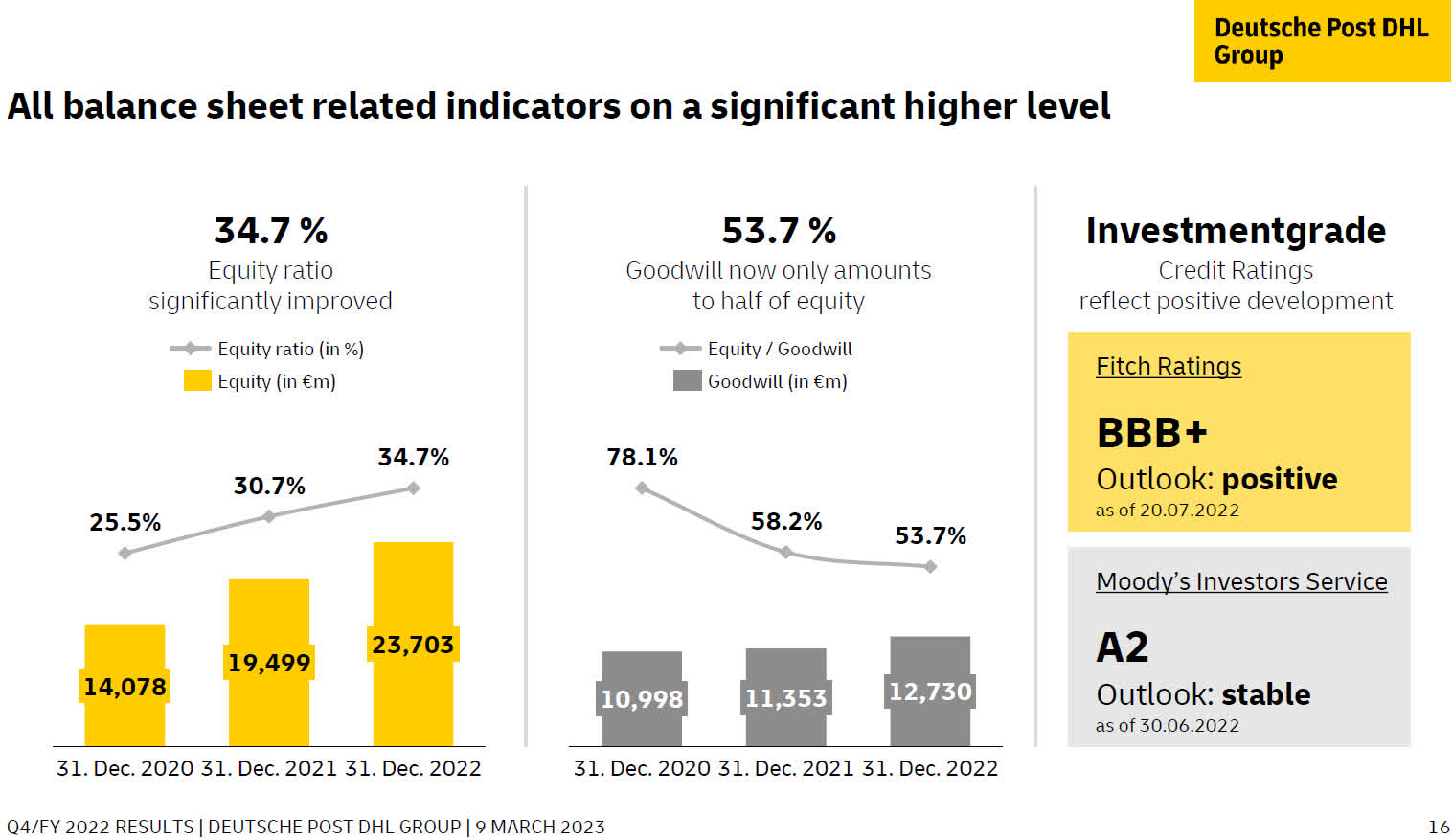

The management's smart use of capital enabled them to better their balance sheet , even though I think the amount of goodwill is still too high. But if the trend continues, this problem should be solved soon.

{kind=link}

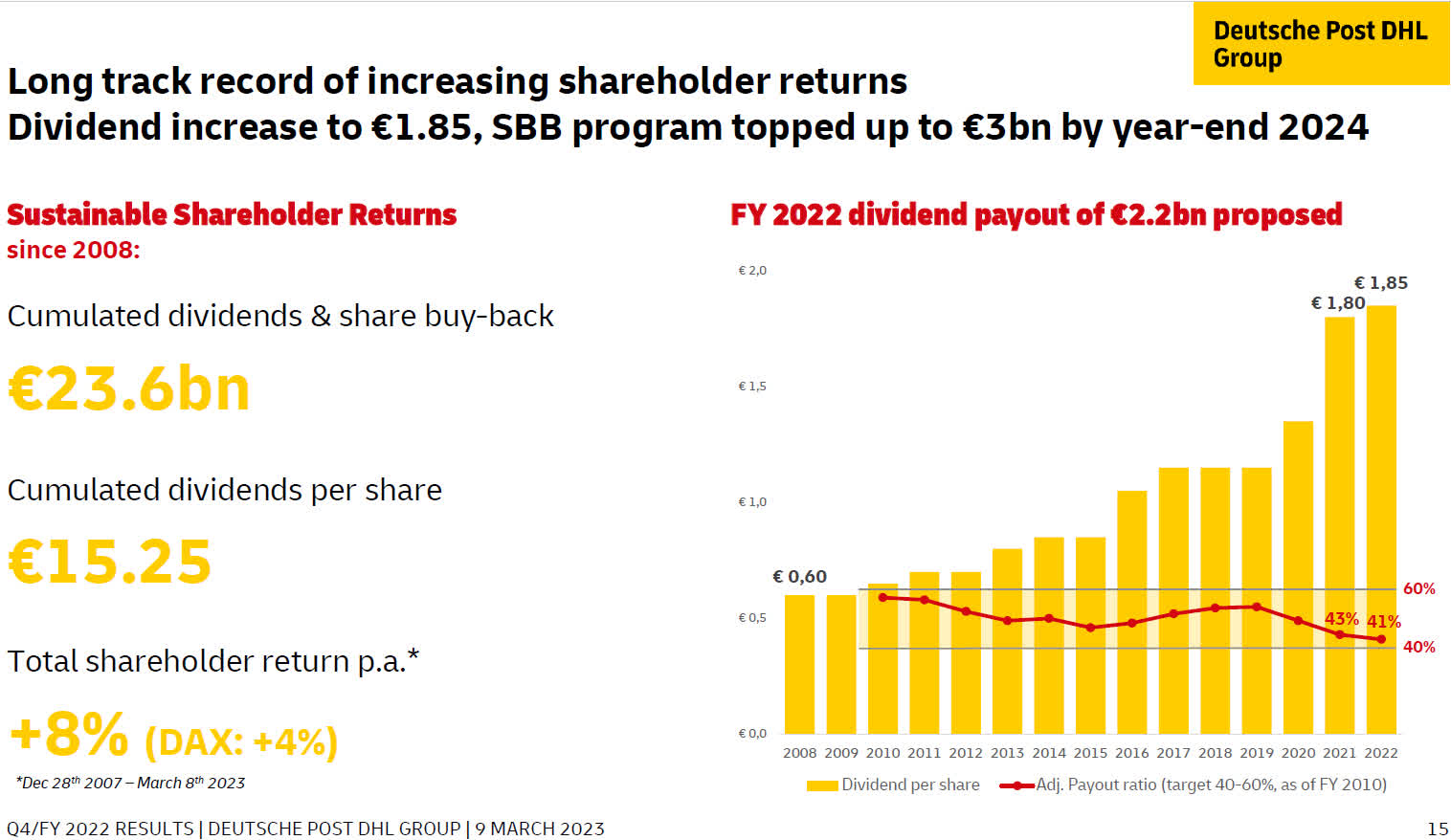

Deutsche Post is a shareholder-friendly company, as you can see in the chart below. Since 2007, an investment generated 8% annual returns, vastly outperforming the other 30 biggest German companies (DAX +4% annually).

{kind=link}

The dividend was raised from 1.8€ to 1.85€ in 2023. While this is just a minor raise of 2.7%, the adj. payout ratio gives room for future dividend hikes. With a payout ratio close to the bottom of the target range, there would be room to raise the dividend even if earnings stagnate.

Outlook

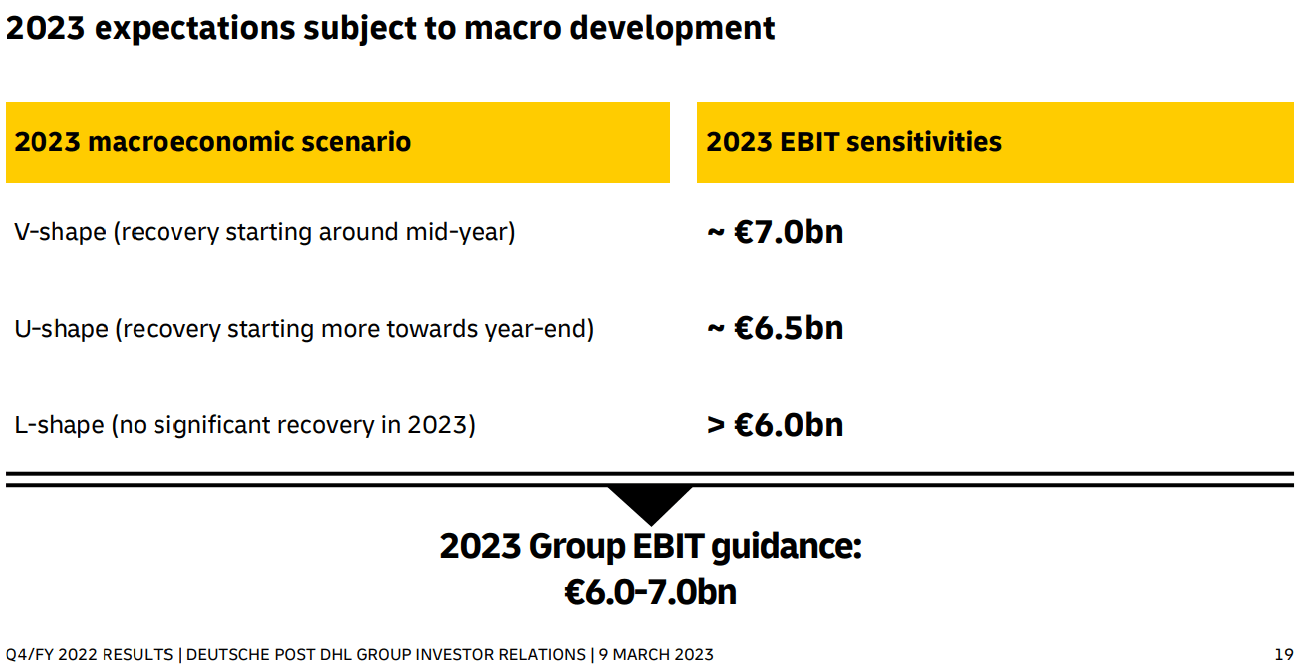

Deutsche Post has three different scenarios regarding how the recovery of the economy could turn out.

{kind=link}

The base case is a recovery towards the end of the year, allowing them to earn €6.5B EBIT. The worst case would bring €6B in EBIT. I think the base case is quite pessimistic. I could see them beating the base and maybe even the best-case scenario if the economy recovers accordingly.

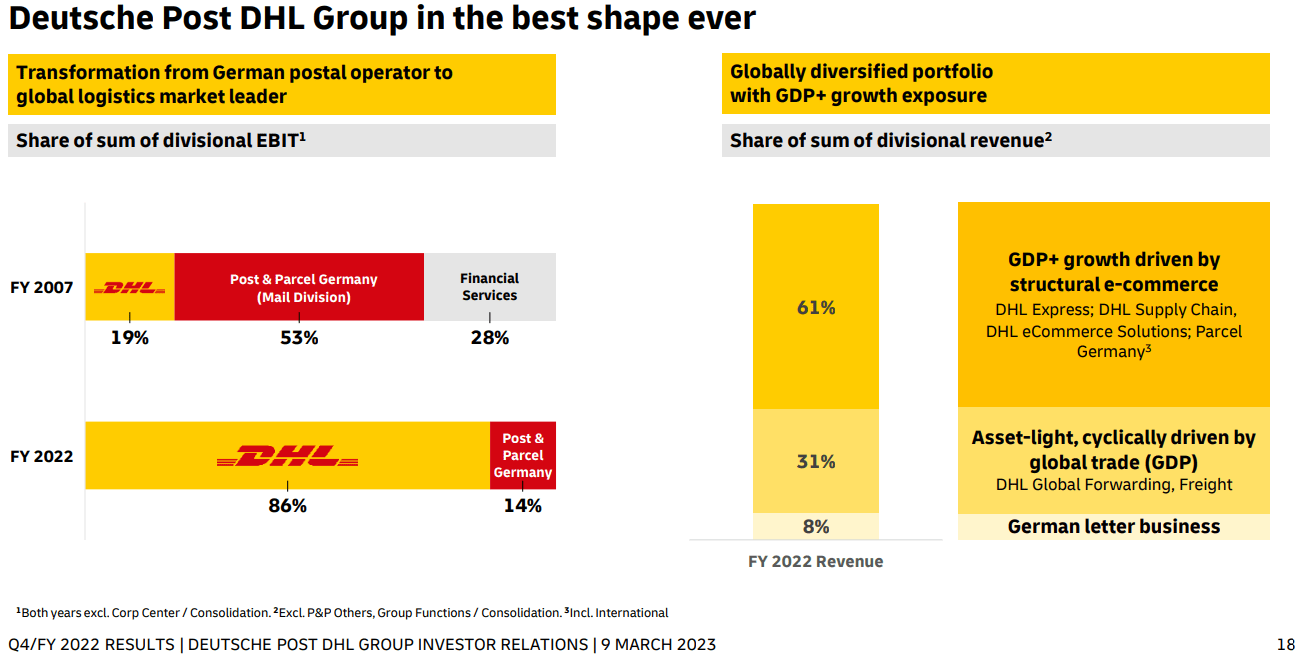

In any case, Deutsche Post is in its best state ever:

{kind=link}

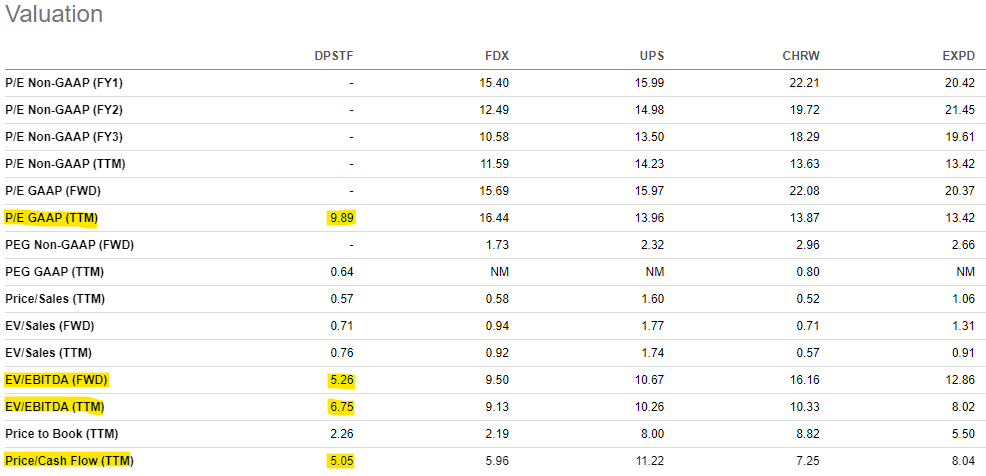

Valuation

Compared to other carriers, Deutsche Post looks fairly valued. It is the cheapest while growing the fastest. I chose FedEx (FDX), United Parcel Service (UPS), C.H. Robinson Worldwide (CHRW), and Expeditors International of Washington, Inc. (EXPD) as competitors. FedEx and UPS come the closest to the Deutsche Post.

{kind=link}

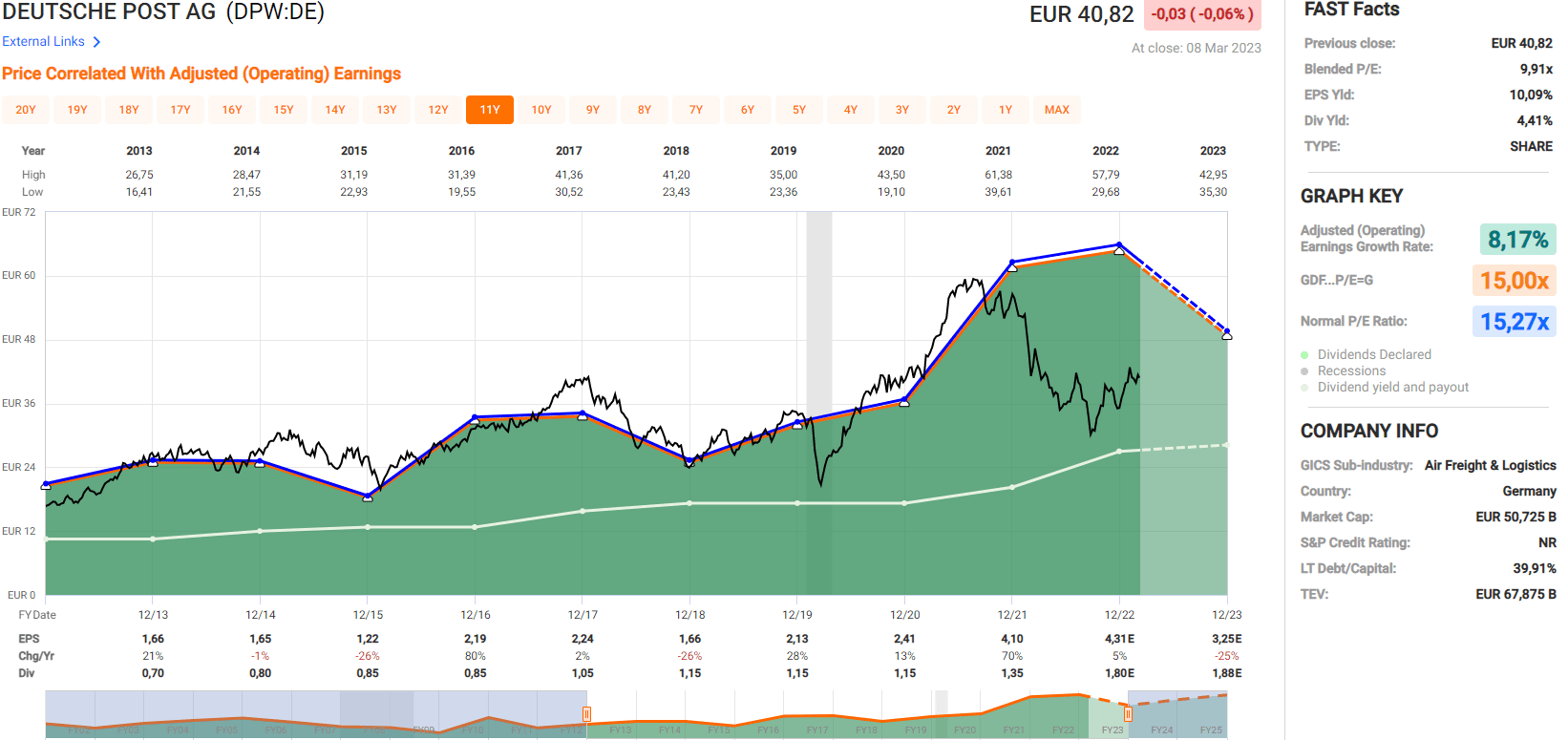

What I like a bit more about assessing a potential under- or overvaluation is comparing a stock's P/E to its own average P/E. In the following, you can see a FAST Graph showing the current valuation in comparison to the historical average:

FastGraph's historical chart (fastgraphs.com)

{kind=link}

In the last ten years, Deutsche Post traded at an average of 15.3x times earnings. The current P/E of 9.9 gives us an undervaluation so severe that we haven't seen it in the last ten years. Assuming that the stock returns to its ten-year mean until the end of 2025, we would get a total return of nearly 22% annually at current share prices. And this is even with the lower earnings result in 2023.

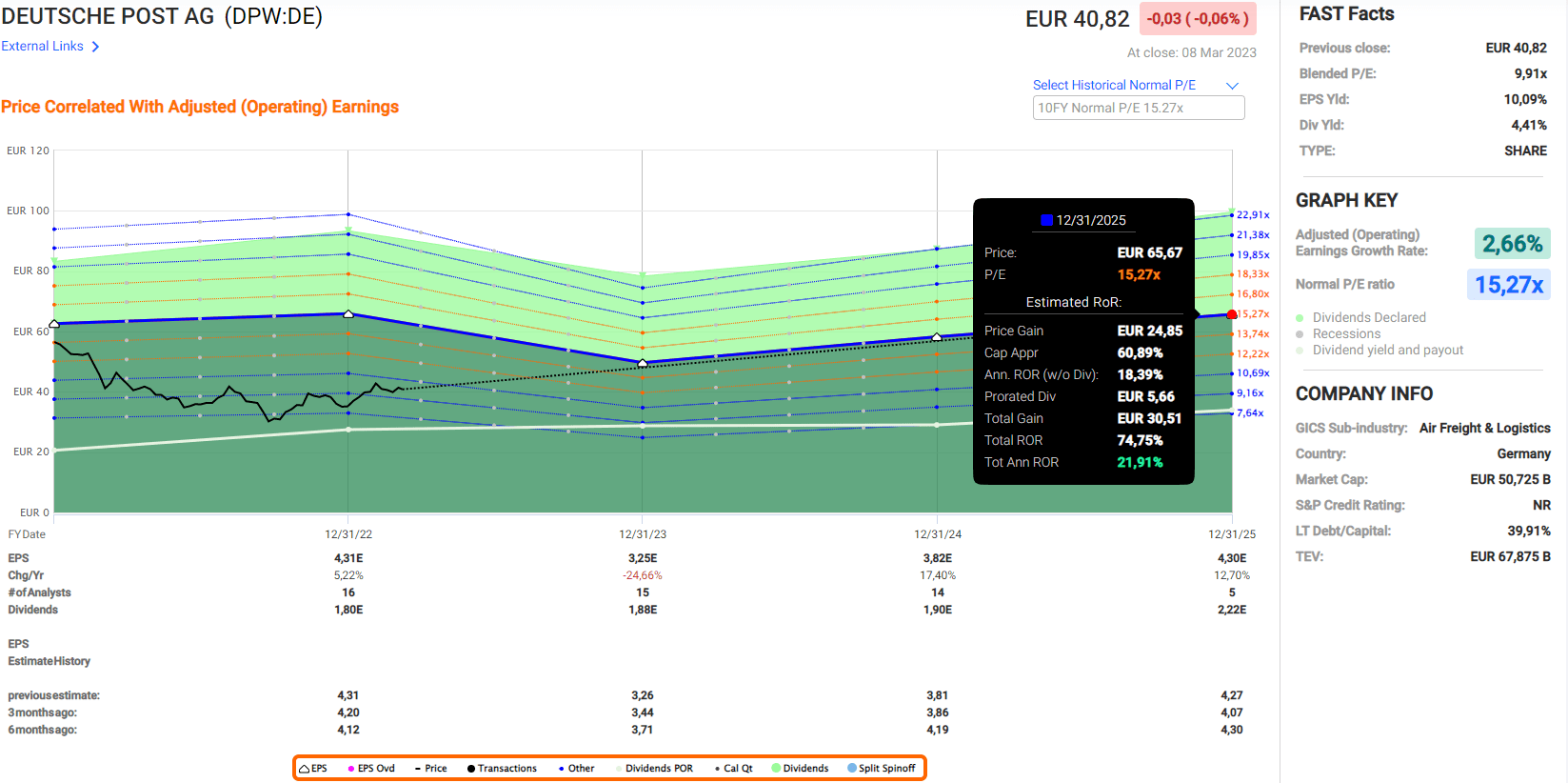

{kind=link}

Even if we apply a margin of safety of 20%, we still get an annual return of 17.6% - vastly outperforming the market.

Conclusion

Deutsche Post AG published excellent full-year 2022 numbers and rewarded its shareholders with a dividend hike and raise of the share buyback program. Apart from that, funds were used to strengthen the balance sheet and raise the working capital. The guidance for the year 2023 is far below the results of 2022, but gives room for a potential beat. The Deutsche Post AG valuation is low compared with peers and its historical averages - and this undervaluation is undeserved, in my opinion. The total return potential is market-beating and leads to me rating it a "buy."

For further details see:

Deutsche Post AG: Q4 Earnings Report Confirms The Bull Thesis