DPSTF - Deutsche Post DHL: Undervalued With Significant Upside Potential

Summary

- Dark clouds hang over as a result of declining demand, volumes and freight rates.

- I believe Deutsche Post should successfully overcome the macroeconomic downturn in tandem with the acceleration of secular growth trends in e-commerce.

- DPDHL stock is trading with at a prominent discount, suggesting significant upside potential.

Deutsche Post DHL Group has proved its expertise in dealing with diminishing demand, depressed freight volumes and rates by delivering a solid third-quarter performance. Global economic uncertainty is dampening B2B segment, while e-commerce driven B2C volumes remain sustainable and are expected to rise. Although the pandemic has set a high watermark for B2C volumes, I believe that the normalization pattern through 2022 against the high base period is hiding a secular shift of consumers’ commerce behavior. This long-term growth driver should benefit Deutsche Post’s ( DPSTF ) global logistics business and underpin FCF generation capacity to power dividend distribution policy. Additionally, strong brand recognition and pricing power should enable the company to successfully pass-on the inflation-induced costs. I am bullish on DPDHL, as I believe the company could extract a positive performance from B2B business even in subdued demand and falling freight rates due to well-positioned logistics business divisions.

Cold ocean

Following two years of elevated freight rates and overstretched capacity, the ocean has cooled rapidly, where the rates are currently consolidated at around $2 200 to ship a 40-ft container. Dark clouds are hanging over economic activity, as the war-related disruptions, energy crisis and inflated input costs cause uncertainty and dwindling demand.

Global container Freightos Baltic Index (Freightos)

The clouds are going to affect logistics companies, especially in B2B segment, as the latter is primarily related to macro factors. However, the volumes should be underpinned by normalizing inflation and energy prices in Europe and alleviation of zero Covid policy in China.

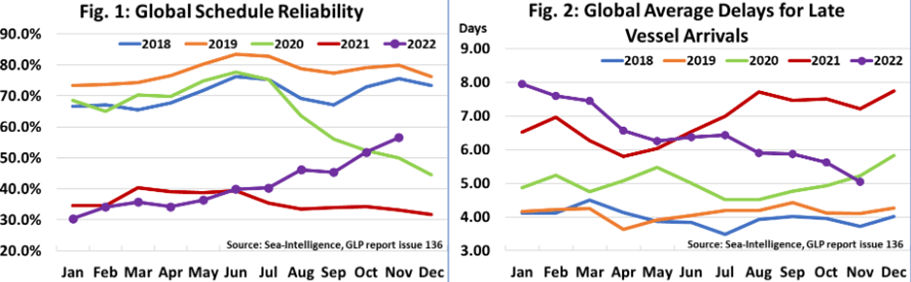

Turbulence in the sky

Low schedule reliability figures of the ocean carriers could encourage the shift of more loads to be shipped by air. Indeed, during the peak of the pandemic, the airfreight industry picked up ocean volumes due to higher prices and disruption in ocean shipping. However, with the port congestion elevation, schedule reliability is expected to improve, which will increase confidence levels among shippers and reduce the need for more-costly air freight.

Global schedule reliability and average delays for late vessel arrivals (Sea-Intelligence)

{kind=link}

Global schedule reliability improved by 4.7% MoM in November 2022 and reached 56.6%. The average delay for late vessel arrivals has also been improving consistently since the start of the year.

The following is a quote from DP DHL Q3 report:

We registered a 10.9% decline in air freight volumes in the third quarter of 2022, primarily on trade routes between China and the United States, due to lower demand and a shift to ocean freight.

Although the lower volumes were covered by high air freight rates (AFRs), the shift to more ocean cargo could exhibit downward pressure on AFRs.

E-commerce growth: secular trends or just a Covid one-and-done deal

While the reasons for the rise of e-commerce during the first year of Covid in 2020 are apparent, in my view, the shift to shopping online is a behavior that almost everyone could evidence in himself. On the one hand, the sales are normalizing and stabilizing compared to the exceptional Covid year, while on the other hand, consumers should be more careful with their spending. The effects of the war in Ukraine, inflation and disrupted global supply chains are a general source of uncertainty that could drive growth numbers back to pre-pandemic levels.

Retail e-commerce sales worldwide (Statista)

Nevertheless, thanks to the development of payments and logistic infrastructure which improves the consumer experience, online sales account for nearly 20% of all retail activity in 2022 worldwide. But the growth is not done, and the share is expected to increase sustainably up to 24% going further. This trend could be underpinned by the shift of consumer’s priorities to online convenience, which would force the process of brick-and-mortar stores closures.

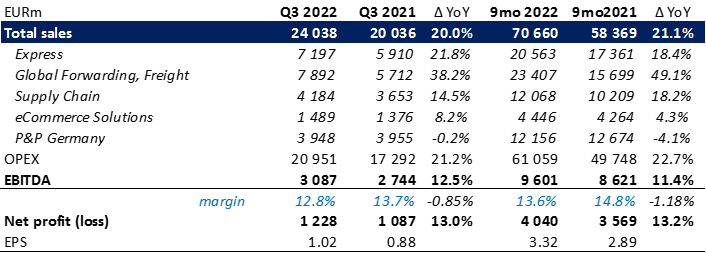

Strong financial results despite dark clouds

Deutsche Post marked a solid 20% YoY consolidated revenue growth in Q3 2022 to EUR 24 billion where all divisions contributed to the positive performance, underpinned by currency effect. The top runner was Global Forwarding, Freight with a 38.2% YoY expansion to EUR 7.9 billion due to higher freight rates and 11.9% increase in ocean freight volumes following the integration of Hillebrand logistics company.

Financial results in Q3 2022 (company reports)

{kind=link}

The Express business line followed with a 21.8% YoY growth to EUR 7.2 billion, reflecting higher fuel surcharges in all geographic regions. Going forward, supply chain direction registered 14.5% YoY growth on the back of strong Americas region; eCommerce solutions contributed to the group’s top-line with an 8.2% YoY growth, while Post & Parcel Germany remained flattish (-0.2% YoY) due to decrease in letter mail business.

Operating expenses increase of 21.1% YoY outperformed the revenue growth, mainly due to elevated transport costs and resulted in a slight EBITDA compression by 85 bps to 12.8%. As a result, Q3 net profit attributable to Deutsche Post shareholders came in at EUR 1.3 billion, which corresponds to EUR 1.02 per share, compared to EUR 0.88 per share in the year-ago quarter.

In light of the solid performance, the management also released updated guidance, where free cash flow is now expected to reach EUR 4.2 billion in 2022 (up from 3.5 billion).

Valuation and expectations

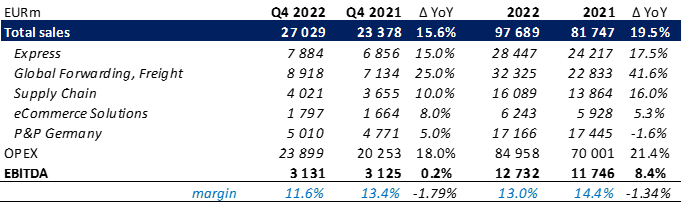

Let’s begin with the forecasts of total sales and EBITDA for Q4 and 2022 year:

Q4 and 2022 full-year expectations (company reports, author’s estimates)

{kind=link}

Segment-wise, DHL GF&F is assumed to expand the most (+41.6%) due to resilient shipments and still high freight rates; DHL Express is forecasted to mark 17.5% growth on a strong TDI product line; for DHL Supply Chain, I expect 16% growth due to lower share of cyclical customers; DHL eCommerce should increase by moderate 5.3% as a result of normalizing e-commerce activity; P&P Germany is forecasted to decrease by 1.6% due to contraction of conventional letter mail volumes. With the above expectations, total sales should reach EUR 97.7 billion and mark 19.5% growth in 2022. I expect 21.4% OPEX expansion to result in full-year EBITDA of EUR 12.7 billion, while fuel surcharges should limit EBITDA margin decrease to 13%.

To the estimated EBITDA, I decided to apply sector EV/EBITDA forward trading multiple, derived from Deutsche Post’s main competitors in the face of FedEx Corporation ( FDX ), United Parcel Services ( UPS ), ZTO Express ( ZTO ), Expeditors International of Washington ( EXPD ), DSV A/S ( DSDVY ) in order to arrive to the fair value.

Peer valuation (seekingalpha, author’s estimates)

DPSTF is trading currently at EV/EBITDA forward multiple of 5.2x, which represents a significant discount of around 39% to the sector’s median of 9.0x, derived from the main comps. Applying my estimate of EBITDA to the peers' median multiple should yield an enterprise value of EUR 114.6 billion. Net of interest-bearing and pension liabilities, the implied equity value should be EUR 94.9 billion, which corresponds to EUR 78.8 per share and implies 78% upside potential. I believe such valuation will reflect DP DHL’s ability to respond successfully to a macroeconomic downturn, while flexible adjustment of networks and prudent cost management will provide for strong cash flow generation capability. Additionally, since the completion of the first share buyback tranche of EUR 800 million, the company decided to proceed with another EUR 500 million until March 2023. The buyback procedure is set to last to the end of 2024, and will support the upside potential of the stock until a total volume of up to EUR 2 billion is reached.

Risk factors

As the economy is expected to slow down, shipments are anticipated to follow suit, which will affect the B2B segment, especially. Extended period of low economic growth will exacerbate this negative effect. Another significant risk for the company is the slowdown in consumer spending in online stores. An increase in fuel costs is a risk as well. The recent shift from Covid policy in China could result in a faster than expected rebound in its economic growth and boost fuel prices. Brent Crude is trading around EUR 85/bbl, and despite DPSTF has an effective fuel surcharges in place, the degree of the risk depends on how much of that rise is passed on to consumers.

Conclusion

In my view, DP DHL is a Buy, as the company commands well-positioned logistics business divisions amid continuing global economic uncertainties. However, China’s economic recovery will be a positive sign for global economic activity in 2023. Additionally, the development in digital payments, supply chains and connectivity, especially in emerging markets, will be a strong driver for e-commerce business. I believe Deutsche Post could build on its strong balance sheet to overcome negative economic prospects and benefit from still strong business momentum in B2C segment.

For further details see:

Deutsche Post DHL: Undervalued With Significant Upside Potential