DPSTF - Deutsche Post: My Bullish Thesis Remains Intact

2023-11-09 11:30:00 ET

Summary

- Deutsche Post has demonstrated resilience in its operational performance despite challenging economic conditions and external headwinds.

- The company's ability to maintain respectable cash flows, manage costs effectively, and deliver a dividend yield of over 5% is commendable.

- The company's forward-looking guidance, positioning in the e-commerce market, and strong market share position it favorably for long-term growth.

- Investors can expect revenue growth at a long-term CAGR of mid-single digits and high-single-digit EPS growth.

- With a current share price trading at a discount to historical averages and peers, Deutsche Post presents an attractive investment opportunity with the potential for solid returns.

Investment thesis

I reaffirm my buy rating on Deutsche Post ( DHLGY ) stock and update my revenue and EPS estimates following the company’s Q3 earnings. I Last covered the shares back in August. I rated the shares a buy and concluded the following:

Solid investments have positioned the company favorably towards the growing e-commerce market which management views as one of the primary long-term growth drivers for the logistics giant. Therefore, Deutsche Post is very well positioned for steady growth over the next decade, driven by its strong share in the global freight industry and focus on e-commerce.

Furthermore, Deutsche Post has demonstrated a resilient performance in the face of challenging macroeconomic conditions during the first half of 2023. Despite a declining net profit margin and worsening margin profiles in some segments, Deutsche Post maintains its commitment to returning cash to shareholders while looking for cost savings to drive a higher FCF result.

The long-term outlook for Deutsche Post remains positive, with management focused on driving growth above GDP levels, supported by structural growth tailwinds in e-commerce and outsourcing. The company's e-commerce segment remains a key revenue driver and has shown strong growth potential.

Despite challenging economic conditions and external headwinds persisting, Deutsche Post has demonstrated resilience in its operational performance in Q3. The company's ability to maintain respectable cash flows, manage costs effectively, and deliver a dividend yield of over 5% is commendable. While the weak macroeconomic environment has impacted its financials, there are positive signs of a bottom forming in both B2C and B2B volumes.

Deutsche Post's forward-looking guidance, positioning in the growing e-commerce market, and strong market share position it favorably for decent long-term growth. I believe investors can expect revenue growth at a long-term CAGR of mid-single digits and high-single-digit EPS growth.

With shares currently trading at a discount to historical averages and peers, it presents an attractive investment opportunity. Based on the valuation and prospects, a price target of €46 per share is reasonable, making it a compelling buy for investors, offering the potential for solid returns.

Headline numbers look worse than they are as Deutsche Post operationally remains resilient

Deutsche Post released its Q3 results early this morning, November 8, and delivered revenue and EBIT roughly in line with expectations, showing a resilient underlying performance and impressive cost flexibility. Shares are up around 3% at the time of writing. This seems fully deserved after the share price plummeted by nearly 20% over the last three months, primarily in response to weak economic data, potentially suggesting weakness persisting for longer. If so, this would also pressure Deutsche Post as a weak macroeconomic environment leads to decreasing B2C and B2B transport volumes, as we have seen in recent quarters.

This weak macroeconomic environment has been pressuring Deutsche Post’s financials in the first six months of the year and has continued to do so in Q3. Deutsche Post posted Q3 revenue of €19.4 billion, down 19.3% YoY. This was worse than the 16.4% YoY decline reported in the previous quarter and shows a continued revenue deceleration from the 12% decline in the first half of the year. This is what management said :

Global trade has continued to normalize after the pandemic-related boom and the recovery of the global economy has so far failed to materialize, also against the backdrop of higher interest rates and geopolitical crises.

The overall Q3 performance was in line with management’s expectations and reflected a challenging operating environment plagued by high inflation, high interest rates, and decreased consumer spending, which altogether impacted demand for the company’s transportation services.

However, it is worth pointing out that the company was also facing several additional external headwinds in Q3, including high fuel surcharges, FX headwinds, and normalizing freight rates. These had a negative €1 billion impact on reported revenue. Excluding this impact, revenue would be down just 15% YoY, much better reflecting the company’s underlying operational performance, which actually improved slightly sequentially, creating much more room for positivity here.

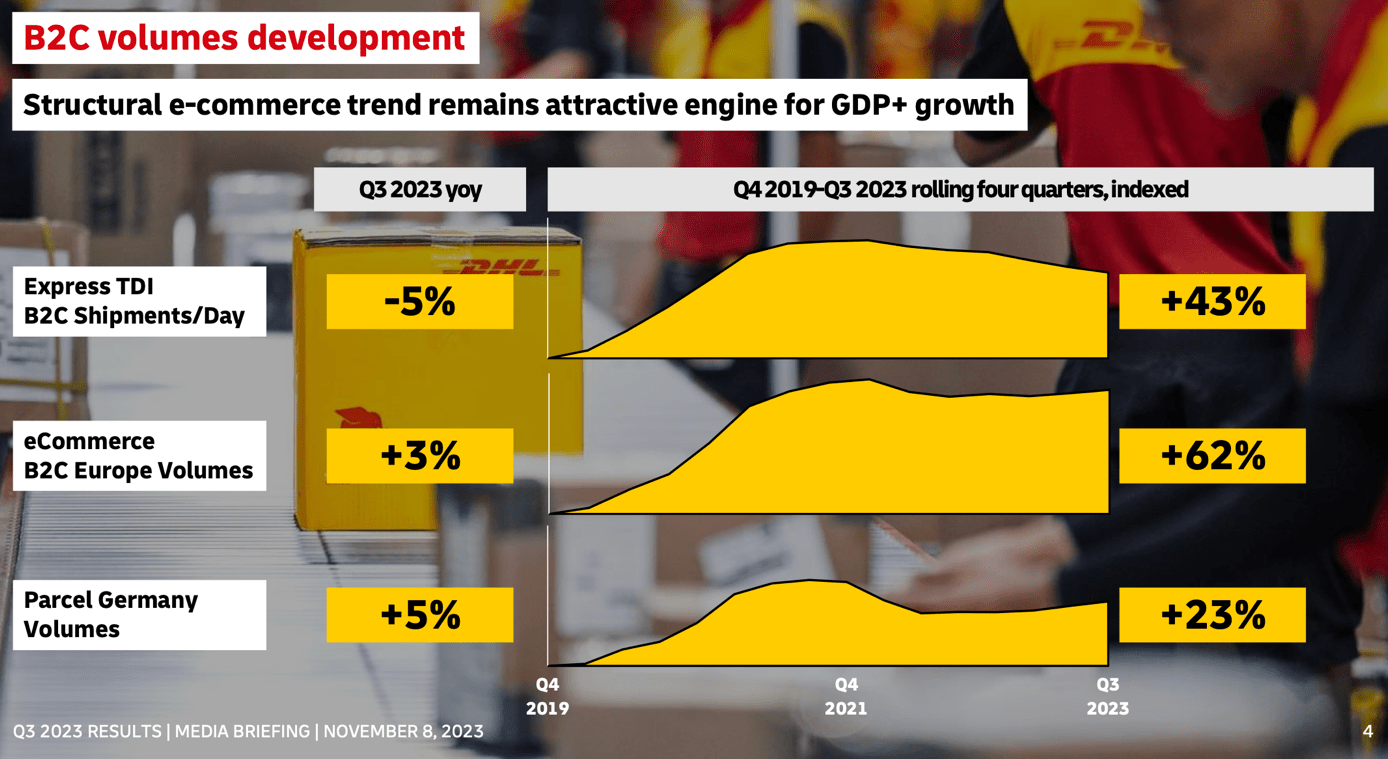

Looking at overall volumes, there is even more room for positivity as a clear bottom is forming for Deutsche Post in both B2C and B2B volumes. As for the B2C volumes, Deutsche Post continued to face a weak consumer spending environment, leading to a decrease in express B2C shipments daily, down 5% YoY. However, this seems to be improving from the previous quarter when this was down 7% YoY, indicating that a bottom might indeed be in.

This thesis is further strengthened by the flat sequential growth rates of low-single digits for both European e-commerce and parcel Germany volumes. Furthermore, as highlighted below, these volumes are still up significantly from 2019 levels and remain resilient. In B2B volumes, Deutsche Post has also confirmed a bottom in the volumes as these rebounded from a low in Q4 last year and are now trending flat.

{kind=link}

A recovery in volumes is still staying out and is taking longer than I anticipated. Of course, looking at the economic indicators over the quarter, this was expected as global economies continue to struggle for traction, and a recession is still a likely scenario. According to management, it is seeing inventories come down globally, but a significant restocking has yet to happen as companies worldwide remain careful in this macroeconomic environment. This is what is delaying a recovery.

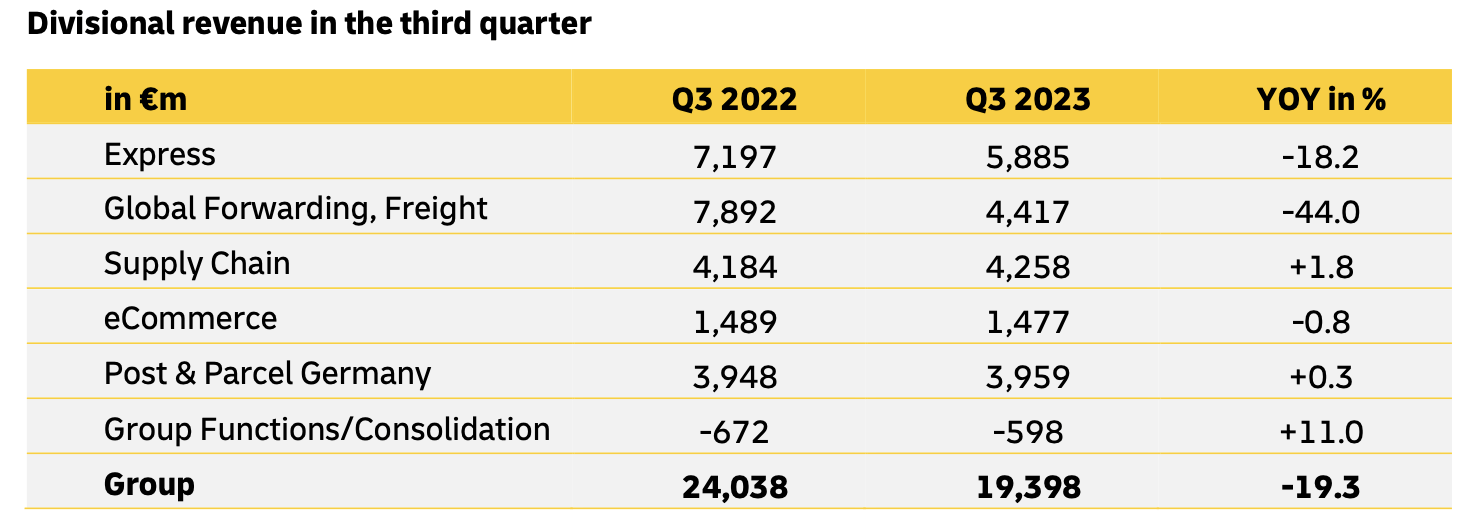

Looking at the separate reporting segments, the two largest segments are impacted the most by the weak macro environment, dragging down the overall performance. The express segment delivered revenue of €5.9 billion, down 18.2% YoY, far worse than the 7.2% decline reported in the year's first half. However, excluding the fuel and currency headwinds, this decline was just 6.4%, actually showing a slight improvement driven by improving volumes, which were down just 2.7%, an improvement from the 4% decline in H1.

Q3 financial data by reporting segment (Deutsche Post)

{kind=link}

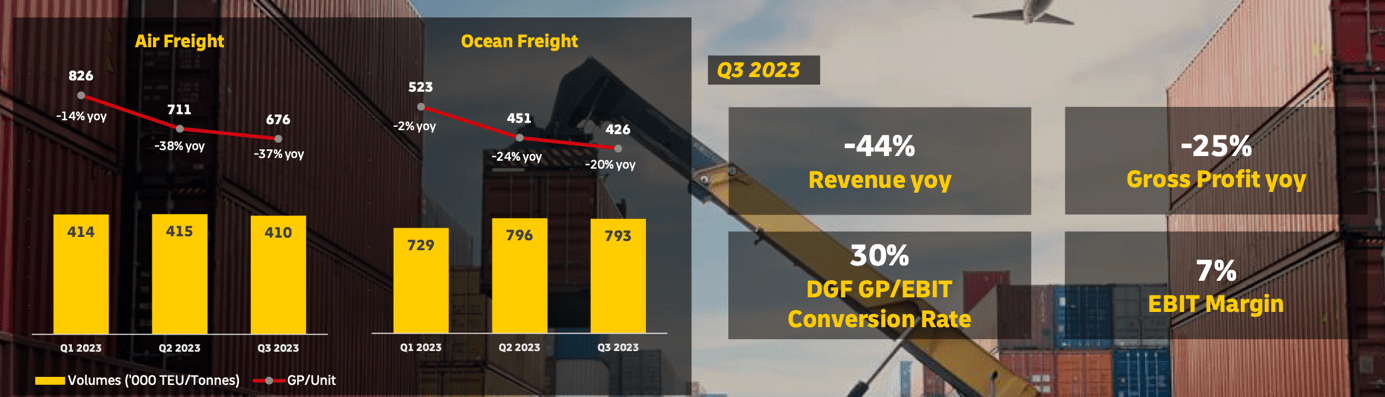

Moving to the Global Forwarding, Freight division, which drove most of the incredible growth during the Covid years, this one saw revenue decline by a whopping 44% YoY to €4.4 billion. Even when excluding the negative FX effect, revenue was still down 40% YoY. Revenue and EBIT in the Global Forwarding, Freight division decreased as expected due to lower volumes in both air and ocean freight and normalizing freight rates.

This segment has performed exceptionally well in recent years due to incredibly high demand during the COVID-19 crisis. This led to elevated freight rates, which are now normalizing due to lower demand, driving a significant decrease in revenue.

Q2 performance of the Global Forwarding, Freight division (Deutsche Post)

{kind=link}

Meanwhile, Supply Chain was the only reporting segment that delivered positive revenue growth of 6.3% to €4.3 billion, and new business, contract extensions, and growing e-commerce business drove this. Nevertheless, revenue in the e-commerce segment was down 0.8%. Excluding the FX impact, revenue was up 3.2% YoY, in line with the growth in e-commerce volumes, which have been growing for three consecutive quarters despite retail weakness.

Finally, the Post and Parcel Germany segment also remained resilient, posting revenue of €4 billion, up 0.3% YoY. This increase was driven by higher prices, which were largely offset by lower volumes of 6.1%.

The bottom line performance was strong, all things considered

Deutsche Post continues to deserve praise for its bottom-line performance. The company has been able to keep cash flows at very respectable levels, driven by cost flexibility and good forward vision from the management team. As a result, management can keep rewarding its shareholders and continue to invest in the business, even in this weak macro environment.

Even as this weighed heavily on the DHL divisions, these could still report very respectable margins and a limited decline in earnings. As a result, the Q3 EBIT of €1.4 billion was down "just" 32.4% YoY, which is far from bad when considering the company barely scaled back investments, saw costs rise due to higher energy and personnel costs, and revenue declined close to 20%. As a result, EPS came in at €0.68, down 33% YoY.

Furthermore, management still reported FCF of €1.1 billion in Q3, bringing the YTD total to €2.5 billion, which is exceptional, all things considered, allowing the company to keep investing and rewarding shareholders.

Shares currently yield a very attractive 5%. The dividend is well covered by FCF at a payout ratio of 70% based on the current FCF consensus for FY23, which is based on slightly depressed cash flows. Based on EPS, the current payout ratio stands at a very safe 56%, which sits within management’s targeted range of 40% to 60% , even based on today’s depressed EPS levels.

With EPS expected to grow at a CAGR of approximately 10.5% through 2025, I believe investors can expect the dividend to grow at a CAGR of around 3% based on a 50% payout ratio, not making it the dividend investors’ dream. Nevertheless, with a yield of over 5%, investors have little to complain about, especially when management still has €1.2 billion remaining under its share repurchase program.

Outlook & Valuation – Is Deutsche Post a Buy, Sell, or Hold?

Deutsche Post continues to guide for an FY23 EBIT of between €6.2 billion and €6.6 billion. Furthermore, the 2025 EBIT is expected to be between €7 billion and €8 billion, depending on the shape of a recovery in 2024. This is down from a previous expectation of above €8 billion as weakness will persist for longer than anticipated.

Meanwhile, the company remains well-positioned for the next growth phase and continues to invest in the business through the cycles to maintain its leading global position. The company’s substantial exposure to the growing e-commerce market allows it to maintain its long-term growth goals of GDP+.

With a market share of 39% in the global parcel market, Deutsche Post remains a primary beneficiary of growth in the freight, forwarding, and express market, expected to grow at a CAGR of 4.6% through 2030 , driven by companies actively sourcing raw materials, components, and finished products from various countries, and the rapid expansion of the e-commerce market.

As a result, I remain bullish on Deutsche Post’s long-term growth prospects and continue to view it as the most favorably positioned among its peers. Based on this positioning and expected underlying market growth, I believe the company should be able to deliver a long-term revenue growth CAGR of 4-6% and EPS growth to outpace this due to margin improvements and continued share buybacks.

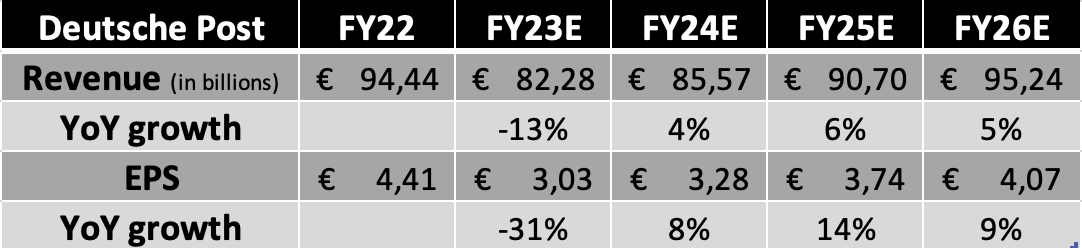

Considering these expectations, the Q3 results, and the FY23 guidance, I now expect the following financial results through FY26, representing my significantly lowered near-term expectations as a slight recovery in volumes will stay out until the end of 1H24. Therefore, I have reduced my FY23 and FY24 financial projections but have largely maintained my long-term expectations as I remain bullish on Deutsche Post’s positioning in the market.

Financial projections (By author)

{kind=link}

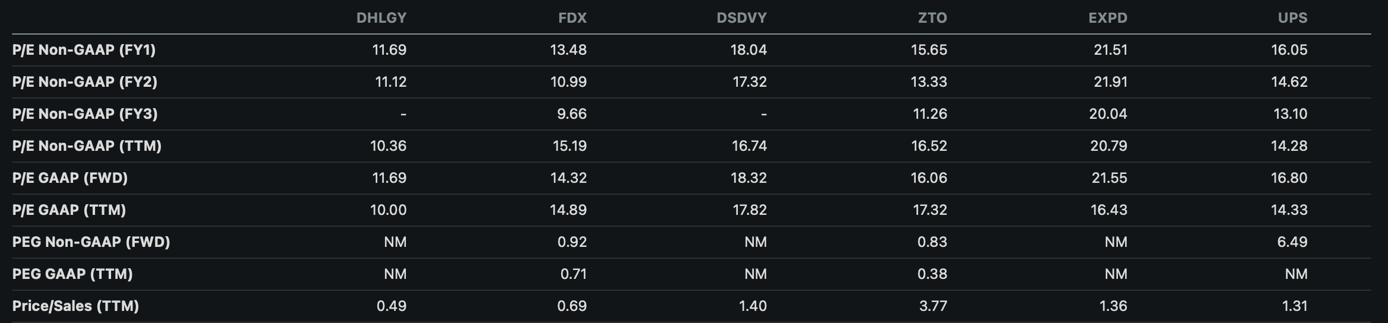

Based on these estimates and a current share price of €38, shares are valued at a forward earnings multiple of 12.5x. This means that shares are trading at a 10% discount to the 5-year average and trading at a 36% discount to the peer average.

Valuation comparison (Seeking Alpha)

{kind=link}

I believe this discount to peers is completely unjustified as Deutsche Post is one of the best positioned among its peers to benefit from the growing e-commerce market and general growth in global freight shipments as the industry leader. Furthermore, the company remains in excellent financial health despite a potential recession and pays the highest dividend among peers. The company clearly is one of the best picks in the industry today. I already believed shares were attractive three months ago at a P/E of 13.3x, but following a 16% drop in the share price, shares now present an even more attractive opportunity, even amid a lowered outlook.

I believe shares deserve to at least trade at a P/E of 14x, which would still put them at a discount to peers but a premium to historical averages. Based on this belief, I calculate a price target of €46 per share. Going with an annual return of 7.5% (12.5% including dividends), I believe fair value sits around €42 per share, meaning shares are currently valued at a discount to the fair value of 10.5%, positioning investors for solid returns.

Driven by this undervaluation and the prospect of solid returns, I maintain my Buy rating on Deutsche Post shares and recommend investors benefit from the current share price weakness.

For further details see:

Deutsche Post: My Bullish Thesis Remains Intact