DPSTF - Deutsche Post Q2 Earnings: Resilient Volumes And An Updated Guidance

2023-08-01 07:50:02 ET

Summary

- Deutsche Post's Q2 earnings were in line with expectations, allowing the company to slightly update its FY23 EBIT guidance.

- Deutsche Post saw very resilient volumes, which helped it to offset some of the economic weakness.

- The company's e-commerce segment continues to be a growth driver, with potential for further expansion.

- Deutsche Post continues to be valued below its peers, unjustified.

- With a potential acquisition on the books, a resilient performance in H1, and a strong growth outlook, I maintain my bullish stance on the company.

Investment thesis

I reaffirm my buy rating on Deutsche Post ( OTCPK:DHLGY ) stock and update my revenue and EPS estimates following the company’s Q2 earnings, which came in line with my expectations and allowed the company to slightly update its FY23 EBIT guidance. Deutsche Post is successfully navigating a challenging macroeconomic environment, driving solid continued cash flows while investing in future growth.

As my investment thesis has not changed much since my previous article on the company, this is what I wrote back then:

Deutsche Post is one of the global logistics leaders in the world as it works on multinational package delivery and supply chain management. It is one of the three largest carriers in the world, only behind FedEx ( FDX ) and UPS ( UPS ) in market cap. However, it has the largest workforce of the three with a little over 550,000 employees worldwide. Yet, despite this strong competitive position, shares continue to be valued much below that of its two closest peers on every single metric. Moreover, the company offers a superior dividend yield. It has a solid balance sheet with no short-term debt and plenty of cash, despite incredibly high investments over the last several years.

These solid investments have also positioned the company favorably towards the growing e-commerce market which management views as one of the primary long-term growth drivers for the logistics giant. Therefore, Deutsche Post is very well positioned for steady growth over the next decade, driven by its strong share in the global freight industry and focus on e-commerce. Yet, near-term headwinds look tough, with inflation and lower consumer spending impacting volumes worldwide. Also, 2022 was a peak year for the company, and revenue is expected to be down from this high for the next couple of years. So, while the company is very well positioned to benefit from long-term growth trends in the freight industry, the industry outlook is not looking so rosy for the next couple of years.

This quarter, the company once more showed a strong performance in its e-commerce segment, which remains one of the most important growth drivers for the company after already doubling the segment's share of total revenue over the last two years. In addition, the company is seeing resilient volumes across the board with some signs of a stabilization and recovery in the second half.

The company’s long-term positioning remains favorable, which is why I remain bullish on the company and its long-term outlook.

In this article, I will take you through the latest important developments and update my estimates and view on the company accordingly.

Deutsche Post increases the FY23 EBIT outlook as volumes hold up well

Deutsche Post was cautious in its guidance at the start of the year as it was expecting quite a slowdown in demand due to a worsening macroeconomic outlook. Record-high inflation and lower consumer spending in retail and e-commerce were already expected to substantially impact the performance of Deutsche Post as these would cause lower volumes for sure, especially as the years before were record years for the company due to a boost in volumes as a result of the COVID-19 pandemic.

Still, despite the high base level due to non-recuring factors and the significant economic slowdown, Deutsche Post believed revenues would remain far above FY19 levels, which was good news for investors. Also, the company expected to report resilient EBIT levels as its asset-light business model would allow for flexible Capex spending.

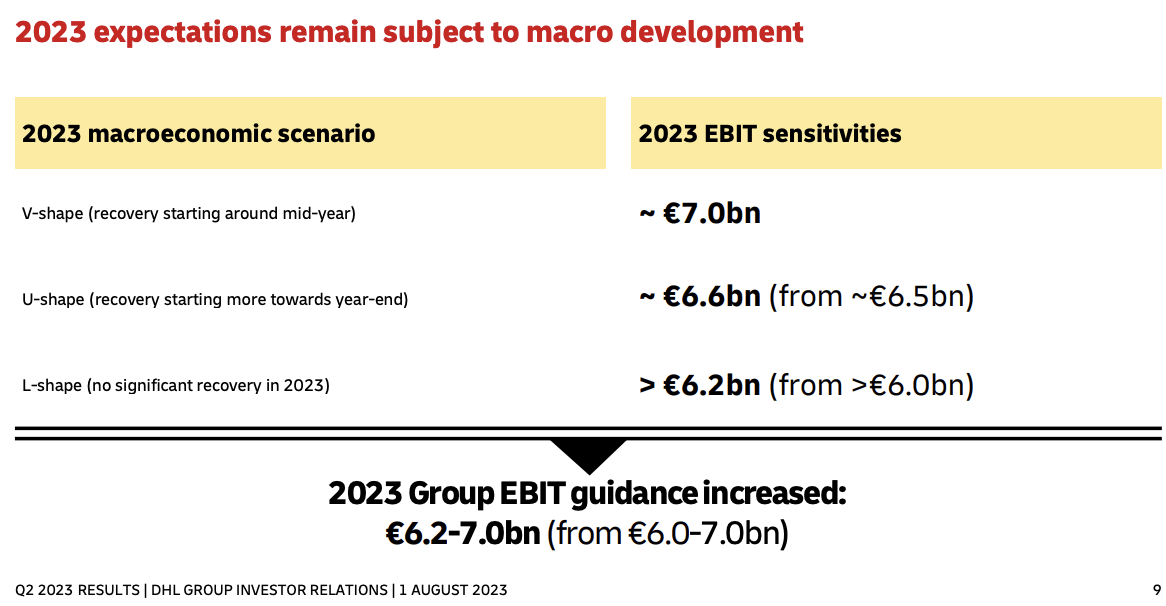

In the first half of the year , the company did not disappoint and even slightly increased its FY23 outlook. Management has seen the general market develop in line with its expectations, resulting in it reaffirming its three macro scenarios for the second half of the year as it is not seeing a consistent recovery yet. Management was already seeing the first signs of a bottom in February/March, which could at least indicate a flattening in the decreasing volume numbers.

{kind=link}

Three economic scenarios for Deutsche Post (Deutsche Post)

The company reported a very resilient performance in the first half of the year as the company reported an EBIT of €3.3 billion, which, annualized, sits above the midpoint of guidance. Yet, the second half of the year has historically been somewhat stronger, primarily due to the boost in shipments in the November and December quarter. Therefore, if market circumstances remain the same as guided by management, an FY23 EBIT of €6.6 billion to €6.8 billion seems achievable.

{kind=link}

Deutsche Post Q2 performance (Deutsche Post)

Yet management has chosen to stay somewhat more conservative and has upgraded its guidance to a FY23 EBIT expectation of between €6.2 billion and €7 billion, up from the previous €6-7 billion. This should even be achievable without a meaningful recovery in GDP in the second half of the year and does not even incorporate a second-half improvement.

At the midpoint of the guidance, EBIT now shows a decline of 21.8% YoY, while my midpoint estimates point to a YoY decline of 19.4% YoY. Of course, these declines are still significant, but we must keep in mind that the business remains very cyclical and that it is lapping tough comparable quarters due to the number of tailwinds the business saw in 2022.

Meanwhile, the long-term outlook is solid, with management dedicated to driving top and bottom-line growth above the GDP level, driven by e-commerce and outsourcing, which provide structural growth tailwinds across the cycle. Moreover, management maintains its FY25 targets, which point to an EBIT of above €8 billion and a return to the FY22 highs. Also, management believes it should be able to keep its FCF levels above €3 billion through 2025 by being cost-efficient and maintaining stable margins.

Q2 was a challenging quarter for Deutsche Post

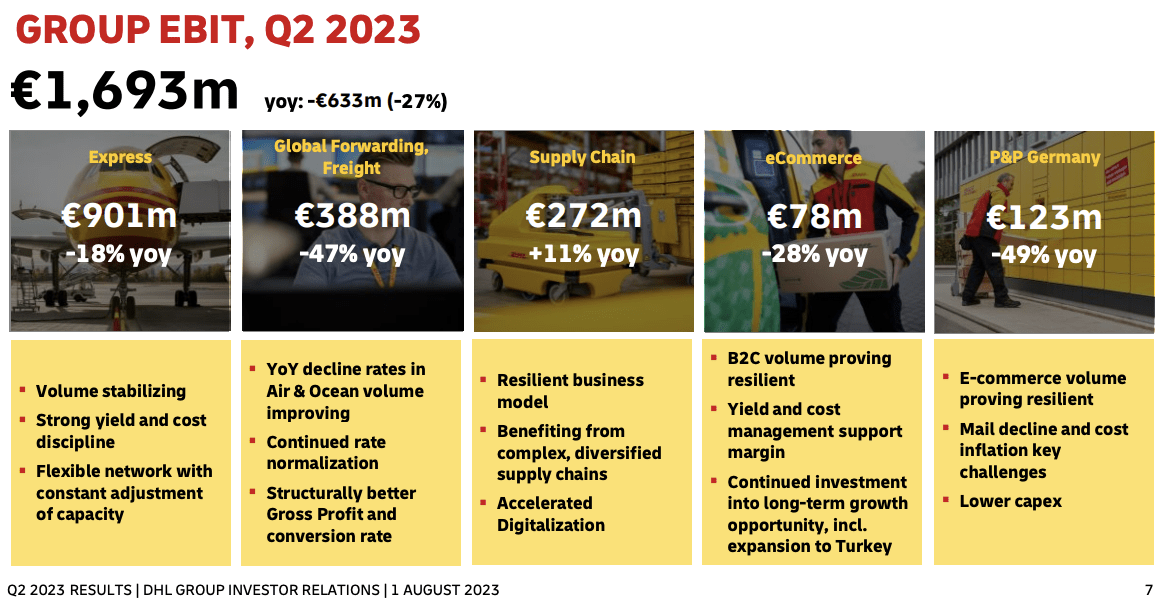

Looking closely at the Q2 results , Deutsche Post reported Q2 revenue of €24 billion, down 16.4% YoY. This brought the H1 revenue total to €41 billion, down 12% YoY, a decline which is not even close to what we have seen in previous down cycles. Deutsche Post is in much better shape compared to the last severe economic slowdown in 2007 with the DHL divisions dominating the business mix today and Deutsche Post having transformed from a German postal company to a global logistics leader, making it much less sensitive to local and highly cyclical business segments. This is highlighted in these quarterly results, which continue to outperform expectations and show very resilient volumes.

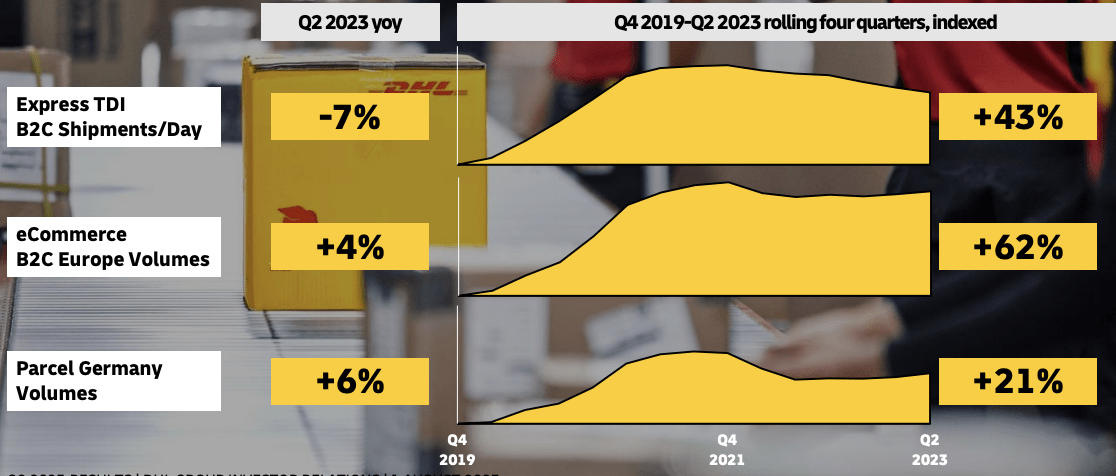

During the first half of the year, management has seen extremely resilient volumes, as highlighted in the graph below. Deutsche Post is seeing a clear uptick in volumes or at least a flattening of the decline. Q2 showed clear moderating trends.

{kind=link}

Volume development for Deutsche Post (Deutsche Post)

Let's look at the company’s individual segments' performance in Q2. We can indeed see that e-commerce was one of the best performing as it already started to show YoY growth in volumes of 4%, despite the macroeconomic headwinds. Revenue remained flat, though, and the EBIT margin also decreased as the company is still heavily investing in expanding its e-commerce networks.

These numbers make me also quite optimistic about the potential growth once an economic recovery is fully underway. Mordor Intelligence believes the e-commerce industry is poised to grow at a CAGR of 15.2% through 2027, which should bode well for Deutsche Post. Today, the segment still only accounts for 6.3% of the company’s total revenue, even after doubling this percentage over the last 2 years. Moreover, with the outlook for the e-commerce market this strong, I expect this segment to keep increasing as a share of total revenue and to become a real growth driver for the company.

In part due to this growth in e-commerce volumes, the supply chain segment of Deutsche Post also reported positive numbers with organic revenue increasing by 5% YoY. New business deals and contract renewals were other factors that boosted this resilient performance. Crucially, this segment has a resilient model due to the long-term contract features allowing it to offset inflation. This caused an expanding EBIT margin to 6%, also driven by further supply chain digitalization.

Meanwhile, the company’s largest segment – Express – saw daily shipments decline by 4% and revenue decline by 7.2% in the first half. Due to this lower revenue level, margins also contracted despite management gradually increasing prices to offset inflation. On a more positive note, for this segment, volumes did stabilize since March but so far are not showing a consistent recovery. Yet, we could start seeing this more pronounced by the end of the third quarter and into FY24.

Another essential aspect to consider here, due to the growing size of the Express business and Deutsche Post’s growth ambitions is the potential for M&A activity. According to the head of Deutsche Post’s freight business, the unit could integrate a large acquisition like DB Schenker’s logistics business, which is rumored to be put on sale soon. Late last year, DB’s management team said to prepare for the possible sale of its logistics business, but there have been no details released thus far. Deutsche Post could be one of the primary candidates to buy the unit, but it already stated that they would have to take a close look at the viability of such an acquisition and exactly how hard it would be to integrate the business. Still, it sure looks attractive, with the unit reporting peak revenues of over €27.5 billion in FY22 and it looks like a good fit for Deutsche Post. It would massively grow its Express segment, giving it a much stronger presence in Europe bringing on many further pricing and synergy advantages. Meanwhile, the value of such a deal is estimated between €12 billion to €20 billion , making it quite a significant acquisition for Deutsche Post. It will be interesting to keep a close eye on this.

The second-largest segment (previously the largest one) – Global Forwarding – saw revenue decline by a much more pronounced 33.5% YoY in the first half, making it the primary contributor to the overall revenue decline for Deutsche Post. In Q2, this decline even came in at above 40%. This decline was primarily the result of declining volumes as air freight volume declined by 13% and ocean freight by 9%. Meanwhile, the margins remained quite strong. This segment is one of the most promising ones in the long-term for Deutsche Post due to its global size and strong EBIT margin which still stands at 7.5% even today. In addition, the growth outlook is strong, with Mordor Intelligence pointing to a CAGR of 4.16% through 2028.

Finally, the Post & Parcel Germany segment reported a flat revenue level of around €4 billion in Q2 and €8.2 billion in the first half of the year. Mail volumes declined by 5% due to the structural shift away from paper mail. Yet, the 8% volume growth in parcel deliveries was able to offset this decline nicely. At the same time, margins fell quite heavily in this segment as a result of high inflation, pressure from collective bargaining agreements, and additional staff costs as wages increased to avoid strikes. The P&P Germany segment has been shrinking as a percentage of total revenue due to the company’s focus on the much more promising e-commerce, express, and forwarding segments and this trend should continue going forward, which I view as a positive development.

Following the results of each of the segments as discussed above, the net profit margin fell to 4.9% from a 2Q22 level of 6.1%, resulting from the lower revenue base. This resulted in an EPS decline of 31% YoY to €0.82. Despite this margin decline, management is sticking to its FY23 free cash flow target of €3 billion after generating €1.5 billion in the first half, which sits comfortably above the dividend obligations of €2.2 billion.

Finally, despite the significant revenue decline and worsening margin profile, Deutsche Post has largely maintained its total cash position on the balance sheet with €3.3 billion at the end of Q2. Yet, at the same time, the debt position has increased by €1.8 billion to €17.6 billion. With the margin improvement expected over the next several years, I believe the balance sheet remains in solid health and should be no reason for concern for shareholders.

Therefore, my outlook for the company’s capital return to shareholders remains unchanged. Apart from a slightly lower yield of below 4%, not much has changed since my previous article when I wrote this:

And there is more good news as management remains fully focused on returning cash to shareholders despite the economic downturn. Deutsche Post will increase its share buyback program by €1 billion to a total of €3 billion, of which €1.3 billion has already been completed as of the end of March. This means Deutsche Post will still buy back €1.7 billion in shares or almost 3% of the current market cap until 2024.

In addition, Deutsche Post shares currently yield 4.07% at a payout ratio of only 44%, giving it plenty of room for further increases, even as revenue and free cash flow come in lower than in previous years. The dividend is safe and sustainable, even in a recessionary scenario with management holding plenty of levers to increase its bottom line if it is forced to. Overall, this means that shareholders should expect a yearly return of about 5.5% through dividend and share buybacks over the next 2 years, which is really solid.

Outlook & valuation

Following a relatively resilient first half of 2023, Deutsche Post slightly upgraded its FY23 EBIT outlook. It expects a similar performance in the year's second half, with a structural recovery staying out until the start of FY24.

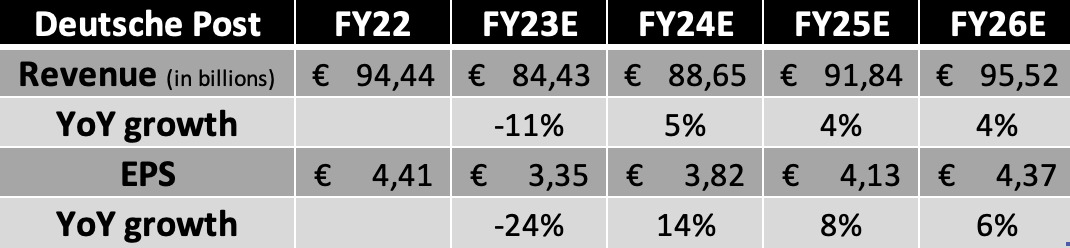

Following this outlook from management, the strong H1 results, and my expectations for the second half of the year, I now project the following financial results through FY26.

{kind=link}

Financial estimates (By Author)

Shortly explaining these estimates, I have maintained my FY23 expectations for both revenue and EPS. The H1 performance was in line with my expectations, and I expect a slight improvement in the second half of the year, resulting in a higher revenue and EPS level than in the first half of the year. I believe we will see an improved performance in both e-commerce and Express, while Supply Chain will also remain resilient.

At the same time, while my FY24 EPS projection has increased slightly, I have lowered the FY25 and FY26 EPS estimates as I expect somewhat less margin improvement than before. Meanwhile, my revenue estimates for these years have increased slightly due to a stronger e-commerce and forwarding outlook.

As a result of these adjustments and the company’s strong share price performance since my previous article, with shares up still 9% even after the drop in share price this morning, shares are now valued at a forward P/E of 13.3x. This is on par with its 5-year average and remains significantly below many of its (American) peers. Meanwhile, I believe Deutsche Post is, in fact, one of the strongest out there, with a solid balance sheet, excellent management team, and impressive company infrastructure.

{kind=link}

Peer comparison (Seeking Alpha)

Based on this peer comparison and the company’s strong competitive position, I continue to believe that a 13/14x P/E is fair for this industry leader. As we are currently dealing with several macroeconomic headwinds that could continue to drag Deutsche Post’s financial performance, I choose to remain slightly more conservative and award the company a 13x P/E.

Based on this valuation multiple and my FY24 EPS, I calculate a target price of €50 (up from €49), leaving an upside of 12% from a current share price of €44.50 following a 5% drop after the earnings release. (Please note, this target price is solely based on its forward P/E and is only for indicative purposes.)

Conclusion

Deutsche Post has demonstrated a resilient performance in the face of challenging macroeconomic conditions during the first half of 2023. Despite a declining net profit margin and worsening margin profiles in some segments, Deutsche Post maintains its commitment to returning cash to shareholders while looking for cost savings to drive a higher FCF result.

The long-term outlook for Deutsche Post remains positive, with management focused on driving growth above GDP levels, supported by structural growth tailwinds in e-commerce and outsourcing. The company's e-commerce segment remains a key revenue driver and has shown strong growth potential.

Based on the company's strong competitive position, solid balance sheet, and excellent management team, a fair valuation multiple of 13x P/E is justified. As a result, I reaffirm my bullish stance on Deutsche Post and project a target price of €50, reflecting a potential 12% upside from the current share price. Going with a 7% return (11% including dividends), I believe a fair value share price sits around €45 per share.

Therefore, I maintain my buy rating at a current share price of €44.50.

For further details see:

Deutsche Post Q2 Earnings: Resilient Volumes And An Updated Guidance