DPSTF - Deutsche Post: Strong Financial Performance; Potential Future Upside

2023-03-10 14:27:35 ET

Summary

- DHL is very well positioned to weather 2023 challenges.

- Thanks to its FCF generation, the company increased its buyback (now at €3 billion).

- 60% of DHL turnover is exposed to e-commerce growth and 30% versus core logistic operation.

- Earnings will remain significantly above pre-COVID-19 levels. Our buy rating is then confirmed.

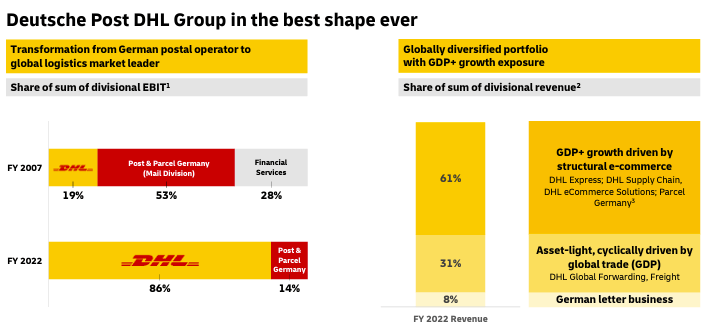

Here at the Lab, we recently commented on PostNL's results, and were not very positive. Indeed, our publication was called: Not The Greatest Q4 Results, and Weak 2023 Guidance . However, after having analyzed Deutsche Post AG (DPSTF) (DPSGY) and as reflected in their current yearly outlook, the company's earnings will remain significantly above record levels from the pre-COVID-19 times (even considering Deutsche Post's lowest 2023 scenario). This fully confirmed our initiation of coverage titled: A New Normal To Price In . In detail, we based our analysis on 1) positive performance in DHL Global Forwarding & Freight division, 2) a lower earnings contribution from Deutsche Post & Parcel segment (see figure below), 3) and a compelling valuation supported by an ongoing buyback and a dividend yield higher than 4.5%.

Deutsche Post's lower contribution from Parcel

{kind=link}

Since our initial buy was released in early May 2022, the company stock price lagged with our internal estimates; however, DHL outperformed the S&P 500 return thanks to its dividend yield.

Mare Evidence Lab's previous publication

{kind=link}

In the mind time, our readers might check our previous analysis of Q2 and Q3 .

Why are we still confident?

- First of all, the company delivered a solid set of numbers (and we are not surprised given the fact they recently raised earnings expectations to €8.4 billion at the core operating profit). Performances were driven by DHL Global Forwarding & Freight division. On a yearly basis, top-line sales reached 94.4 billion and EBIT increased by 6% (in line with management guidance). In detail, our supportive division recorded an operating profit increase of €2.3 billion from €1.3 billion achieved in 2021;

- In 2022, the company heavily invested at a record level of €4.1 billion providing a further CAPEX gap within its closest competitors. In detail, the logistic operator expanded its EV fleet by 7k units and now is at 29k e-vehicles worldwide;

- Despite point 2), FCF reached €4.6 billion and we are not surprised to see a DPS increase at €1.85 per share and an incremental share buyback program of more than €1.0 billion. The total share repurchase volume now amounts to approximately €3.0 billion (€800 was already completed). In addition, thanks to the solid results, Deutsche Post AG is in the low range of its payout ratio (Fig 1);

- What is more important to report is the fact that more than 60% of DHL sales are exposed to e-commerce growth and even if the Air Freight and Ocean division might eventually follow trade cycles, in terms of estimates, we see the company strongly positioned to gain market share with also superior profitability advantages (thanks to its larger scale);

- Going into 2023, there are many uncertainties at the macro level, and the company provided three scenarios analysis: 1) V-shape recovery with an EBIT estimate at around €7.0 billion, 2) U-shape recovery with an EBIT forecast of around €6.5 billion, and 3) L-shape recovery with an EBIT prediction of at least €6.0 billion (Fig 2);

- The company is planning a lower CAPEX expenditure and including maintenance investments, here at the Lab, we forecast an FCF higher than €3 billion. DHL will then comfortably pay its dividend payment forecasted estimated at €2.2 billion;

- Even considering a pessimistic scenario with no significant volume recovery in 2023 (Fig 3), the company foresees an improvement in 2024 with a normalized EBIT earnings level of more than €8bn. Here at the Lab, we believe that the company might be fairly priced in the short term (and its valuation will be supported by a generous buyback and a tasty dividend yield); however, over the long term horizon, still valuing the company with a normalized P/E of 8x, we confirm our target price of €62 per share ($65.5 in ADR).

For further details see:

Deutsche Post: Strong Financial Performance; Potential Future Upside