DFSV - DFSV: Worth Shortlisting Not A Buy Due To Factor Disadvantages

2023-10-22 23:06:37 ET

Summary

- DFSV is a mostly solid small-cap echelon-focused actively managed ETF. As it frequently happens with funds looking promising on the surface, there are a lot of nuances beneath it.

- My analysis showed that mid-caps, not their smaller counterparts, have an outsized impact on the fund's performance due to the weighting schema.

- While attractively valued, DFSV's portfolio is burdened by a meaningful share of low-quality stocks, a mix that I believe is worth avoiding in the current macro situation.

- DFSV’s past performance was close to excellent, but I would stop short of a Buy rating because of factor disadvantages this vehicle has.

Small-cap funds favoring relatively cheap but financially sound stocks have always been of interest to me. And today, I would like to discuss yet another representative of that league, the Dimensional US Small Cap Value ETF ( DFSV ).

DFSV is a mostly solid small-cap echelon-focused ETF, but as it frequently happens with funds looking promising on the surface, there are a lot of nuances beneath it. For instance, my analysis showed that mid-caps, not their smaller counterparts, have an outsized impact on the fund's performance due to the weighting schema. Besides, while attractively valued, DFSV's portfolio is burdened by a meaningful share of low-quality stocks, a mix that I believe is worth avoiding in the current macro situation.

What is DFSV's strategy?

Since its inception in February 2022, DFSV has been managed actively. In the summary prospectus , it is clarified that

The Portfolio, using a market capitalization weighted approach, is designed to purchase a broad and diverse group of the readily marketable securities of U.S. small cap companies that the Advisor determines to be value stocks.

Regarding holdings, it is said that

The Portfolio may emphasize certain stocks, including smaller capitalization companies, lower relative price stocks, and/or higher profitability stocks as compared to their representation in the small-cap value segment of the U.S. market.

Regarding the valuation and profitability parameters assessed, the following clarification is provided:

An equity issuer is considered to have a low relative price (i.e., a value stock) primarily because it has a low price in relation to its book value. In assessing relative price, the Advisor may consider additional factors such as price to cash flow or price to earnings ratios. An equity issuer is considered to have high profitability because it has high earnings or profits from operations in relation to its book value or assets. The criteria the Advisor uses for assessing relative price and profitability are subject to change from time to time.

As of writing this article, DFSV had a diminutive turnover of only 4% , which implies that it keeps the portfolio relatively stable despite its active mandate.

Is DFSV truly a small-cap ETF?

Unfortunately, I do not think so. There are nuances. For example, the median market cap in its portfolio was about $793 million as of October 20, as comes from my analysis. The issue here is that even though there are only about 271 mid-cap companies in its basket, they have an outsized impact on the weighted average figure, which stood at $3.05 billion, well above the traditional small-cap threshold of $2 billion. At the same time, the share of stocks with a sub-$2 billion market cap was only around 33.6%. There are even micro and nano caps in this mix (with market values below $300 million), but they had a microscopic weight of approximately 1.82%.

The weighting schema is obviously to blame. For more context, the fund's largest 100 holdings in its 1,027-strong portfolio account for around 41.5% of the net assets; in this group, there are no small caps at all.

Nevertheless, this is not a DFSV-unique issue. For example, I have already reviewed this problem typical for most 'small-cap' ETFs in the June note on the Roundhill Acquirers Deep Value ETF ( DEEP ).

The good: DFSV's strategy has an edge over a few peers

Over its relatively short trading history, DFSV has already delivered rather solid results. This is evident from the analysis of its performance compared to a few of its small-cap peers I covered in the past, namely the following:

- Roundhill Acquirers Deep Value ETF ( DEEP ),

- Invesco S&P SmallCap 600 Pure Value ETF ( RZV ),

- Invesco S&P SmallCap High Dividend Low Volatility ETF ( XSHD ),

- iShares US Small Cap Value Factor ETF ( SVAL ),

- SPDR S&P 600 Small Cap Value ETF ( SLYV ),

- Invesco S&P SmallCap 600 Revenue ETF ( RWJ ),

- Pacer US Small Cap Cash Cows 100 ETF ( CALF ),

- iShares Core S&P Small-Cap ETF ( IJR ),

- iShares Russell 2000 Value ETF ( IWN ),

- Avantis U.S. Small Cap Value Fund ( AVUV ),

- VictoryShares US Small Cap High Div Volatility Wtd ETF ( CSB ),

- Schwab U.S. Small-Cap ETF ( SCHA ).

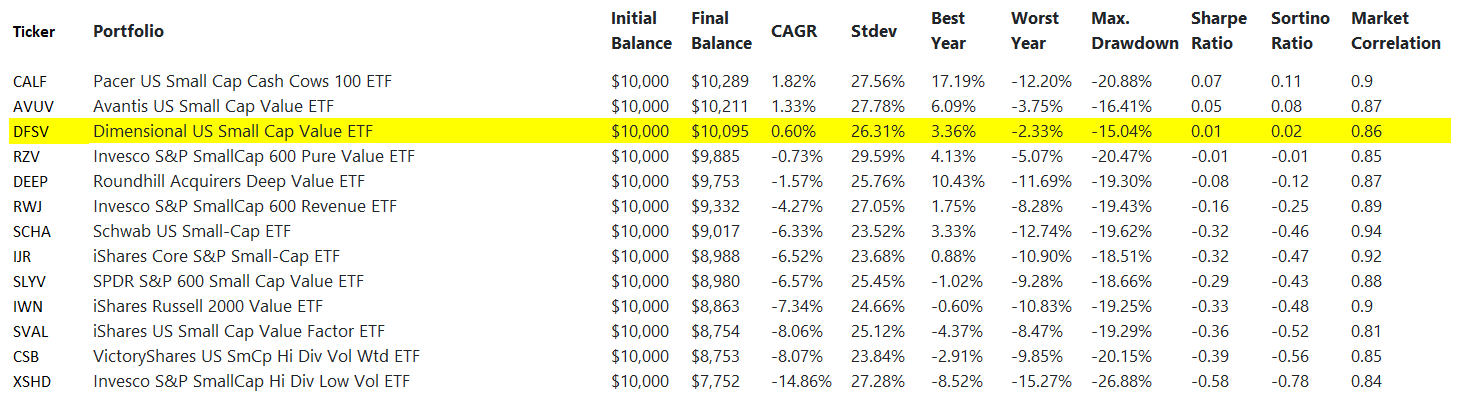

As the table below shows, over the March 2022–September 2023 period, DFSV delivered the 3rd-strongest annualized return in this group, trailing only AVUV and CALF, which both achieved low-single-digit CAGRs.

Data from Portfolio Visualizer

{kind=link}

Importantly, DFSV also easily beat IWN, which tracks its benchmark , the Russell 2000 Value Index, delivering an annualized return of 7.94% higher.

Other advantages include one of the highest risk-adjusted returns in the cohort (Sharpe, Sortino ratios), as well as the maximum drawdown of just around 15% vs. the median of 19.3%. Investors focused on diversification would also likely appreciate its market correlation of only 0.86, one of the smallest in the selected peer group.

Next, it is worth mentioning that it outperformed the iShares Core S&P 500 ETF ( IVV ), a bellwether barometer, over the period concerned as well, delivering a CAGR of 19 bps higher. This result was achieved even despite DFSV underperforming IVV this year (by almost 10% in the first nine months), primarily thanks to the sizable differences in 2022 performance (March–December). More specifically, while the bear market dragged IVV down by around 11%, DFSV declined by only 2.33%.

The bad: valuation advantages come with quality nuances

My dear readers might call me too zealous when it comes to factors. Nevertheless, I am of the opinion that the current macro environment is too challenging and uncertain to compromise on value and quality.

Overall, there is a lot to like about DFSV's factor profile, but the quality issue currently makes it impossible to create a Buy thesis. To elaborate on that, let us take a closer look at the following data:

| Metric |

| Holdings as of October 19 |

| Market Cap |

| $3.05 billion |

| EY |

| 8.99% |

| EPS Fwd |

| 3.8% |

| PS |

| 1.397 |

| Revenue Fwd |

| 6.3% |

| ROA |

| 4.7% |

| ROE |

| 11.9% |

Calculated using data from Seeking Alpha and DFSV; based on the analysis of 1,000 holdings (~99.75%)

- First, we see that DFSV has a lot to offer in terms of value. Its earnings yield of almost 9%, supported by the financial sector (its key allocation, 24.7% as of September 30), is already telling.

- However, the challenge here is that around 15.8% of the holdings are unprofitable and thus have negative EYs, which skews the figure.

- A possible solution is to look at the Price/Sales ratio. Interestingly, a P/S of about 1.4x tells the same story.

- Another solution is to leverage the Quant ratings. The share of stocks with a B- Quant Valuation grade or higher is close to 57%, which is an indubitably strong result.

- Unfortunately, valuation advantages come with a soft quality. While only ~48% have earned a B- Profitability rating or higher, close to 14% have a D+ rating or worse.

- The fund also does not offer much regarding capital efficiency exposure as the weighted-average figures above illustrate.

- Small ROA is especially disappointing. For better context, DEEP had a 9.7% ROA and 64.5% share of highly profitable companies as of the June article, even despite its WA market cap being below $1 billion (small size correlates with more comfortable valuations and, unfortunately, softer quality).

- On the positive side, even though 15.8% failed to turn a profit in the last twelve months, less than 7% of the companies are cash-burning.

- Ultimately, growth characteristics are barely spectacular. To be frank, this is something to expect from a value-seeking fund. To give a bit more color, the forward revenue growth rate of just 6.3% is mostly the consequence of almost 23% of the holdings that are forecast to deliver lower sales. But the bigger issue is earnings contraction, which pundits anticipate for 41% (360 companies).

Investor takeaway

In sum, even though I was impressed by DFSV's performance, I believe it does not deserve a Buy rating today. It has multiple advantages, including impressive breadth and depth of exposure. It is obviously superior to IWN, as its past performance has illustrated, even despite higher fees, 31 bps vs. 24 bps . It also trounced numerous peers and even the market proxied with IVV. Alas, DFSV is a small cap in the name only. Next, its valuation is attractive, but quality leaves a lot to be desired. This is a mix I am not bullish on.

For further details see:

DFSV: Worth Shortlisting, Not A Buy Due To Factor Disadvantages