NHS - DHF: Sell This Low-Yielding Junk Bond Fund Before The Market Corrects

2024-01-11 15:04:08 ET

Summary

- BNY Mellon High Yield Strategies Fund offers a 7.76% yield, but other junk bond funds have considerably higher yields.

- The DHF closed-end fund has delivered impressive performance in recent months, but the market may have overpriced junk bonds.

- Investors may be better off selling the fund and purchasing higher-yielding peers to reduce risk and potentially maintain income.

- The recent inflation data was much hotter than expected, which hurts the near-term rate cut thesis and makes it more likely that the fund will surrender recent gains.

- The fund's distribution appears to be reasonably safe.

The BNY Mellon High Yield Strategies Fund ( DHF ) is a closed-end fund aka CEF that income-focused investors can employ as a method of achieving their goals of receiving a high level of current income from their assets. Unfortunately, the fund's current 7.76% yield is not as impressive in today's environment as it would have been a few years ago. This is partly because there are other options available in the junk bond space that have considerably higher yields. For example, consider the following:

| Fund |

| Current Yield |

| BNY Mellon High Yield Strategies Fund |

| 7.76% |

| Allspring Income Opportunities Fund ( EAD ) |

| 9.32% |

| BlackRock Corporate High Yield Fund, Inc ( HYT ) |

| 9.61% |

| Credit Suisse High Yield Bond ( DHY ) |

| 9.25% |

| Neuberger Berman High Yield Strategies ( NHS ) |

| 13.59% |

All of these other funds employ a similar strategy focusing on junk bonds. As such, it does not make much sense to own a fund yielding 7.76% when you could own a comparable one yielding 100 to 200 basis points more without really altering the diversification or asset allocation of your portfolio. This does not even include the funds that invest in leveraged loans, collateralized loan obligations, or a mix of the two such as the Ares Dynamic Credit Allocation Fund, Inc. ( ARDC ). Those funds can boast yields that get well into the double digits, but they may be more apt to cut their distributions if and when the Federal Reserve finally switches to a less restrictive policy.

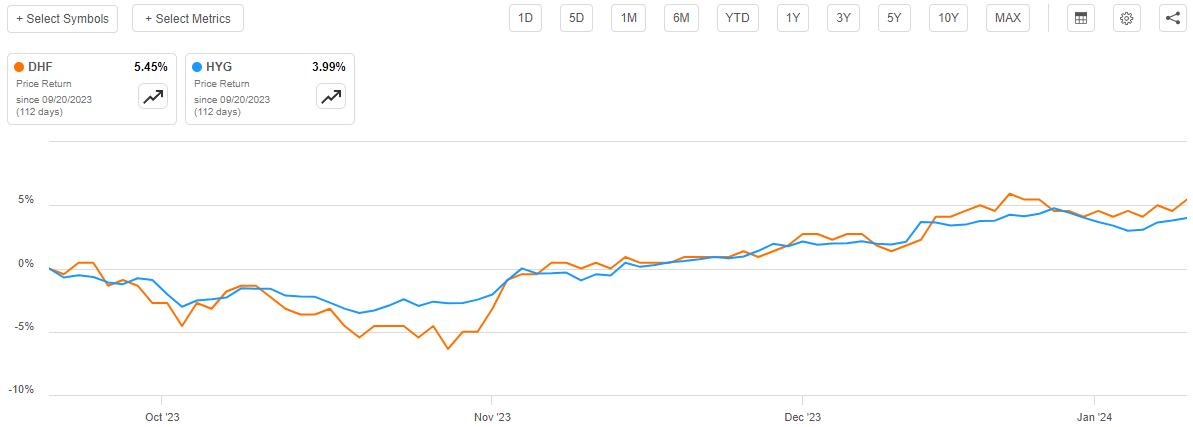

With that said, the BNY Mellon High Yield Strategies Fund has delivered a fairly impressive performance over the past few months. This somewhat helps to offset the rather low yield and could in fact be one cause of it. As regular readers can likely recall, we last discussed this fund in the middle of September of 2023. That was in the middle of a very different market environment than the one that we are currently experiencing. In particular, the market was widely accepted that the Federal Reserve was serious about its "higher for longer" statements and was allowing bond prices to decline and yields to rise. That changed in mid-October when investors became optimistic about the potential for near-term interest rate cuts and started bidding up bond prices. That market bid includes the shares of this fund and resulted in it delivering fairly reasonable share price appreciation since the last time that we discussed it. As we can see here, the shares of the fund are up 5.45% since the date that the previous article was published. This is quite a bit better than the 3.99% gain for the iShares iBoxx $ High Yield Corporate Bond ETF ( HYG ):

{kind=link}

This price appreciation could improve the fund in the eyes of many investors. After all, it has the same effect as the distribution when it comes to increasing your overall wealth. When we combine the share price appreciation and the distribution, investors in this fund have benefited from an 8.34% total return since my previous article on the fund was published. That is much better than the 6.10% total return of the index over the same period.

Unfortunately, there are a growing number of signs that the market has overpriced junk bonds right now since a pivot by the Federal Reserve is not imminent nor is it likely to be of the same magnitude that the market has currently priced into the securities that are held in this fund's portfolio. As such, it may be best to sell out of the fund today and take the gains. I do not recommend removing junk bonds from your portfolio entirely, so it might actually be best to sell off this fund and use some of the proceeds to purchase one of its higher-yielding peers. In so doing, an investor can both reduce their risks and potentially keep their income the same. That is something that we should all be able to appreciate.

About The Fund

According to the fund's website , the BNY Mellon High Yield Strategies Fund has the primary objective of providing its investors with a very high level of current income. This certainly makes a great deal of sense considering the fund's overall strategy. Unfortunately, the fund does not provide an actual description of its strategy on its website or in its fund documents. At least, it does not provide one as in-depth as most of its peers. Rather, all the fund provides is this:

{kind=link}

CEF Connect does not offer a better description of the fund's strategy, as it sometimes does for those funds that do not provide such a description on their websites. CEF Connect simply states this:

The fund's primary investment objective is to seek high current income. The fund will also seek capital growth as a secondary objective, to the extent consistent with its objective of seeking high current income.

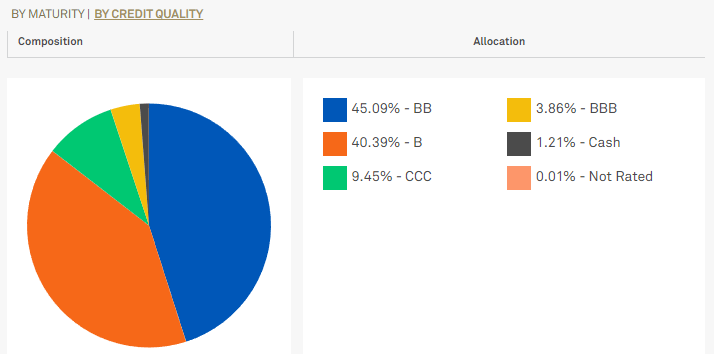

The only thing that we can derive from these two sources is that the fund focuses on investing in debt securities issued by entities in both the United States and Western Europe. Thus, it is a global bond fund. Technically, the descriptions that are provided do not prevent the fund from investing in variable-rate senior loans or similar assets, but for the most part, this is a junk bond fund. We can see this quite clearly by looking at the credit ratings that have been assigned to the securities in the fund's portfolio. Here is a high-level summary:

{kind=link}

An investment-grade security is anything that is rated BBB or higher. Cash and cash equivalents are also considered to be investment-grade, for obvious reasons. As we can clearly see, this only describes 5.07% of the fund's assets. Thus, everything else in the portfolio is speculative-grade debt. These securities are colloquially called "junk bonds." It seems very likely that 0.01% of the fund's assets that are unrated are also junk bonds because most entities that have strong enough balance sheets and financial statements to get an investment-grade rating will generally opt to have their debt-rated in order to save money on interest payments. Thus, we can conclude that the BNY Mellon High Yield Strategies Fund is a junk bond fund. That makes sense considering the fund's name, as "high-yield bond" is a friendly way of saying "junk bond."

The fact that this fund is investing in junk bonds is something that may concern more conservative risk-averse investors. After all, we have all heard about the relatively high risk that a junk bond issuer will default and cause investors to lose their money. Back in October, Moody's Investor Service issued a warning that there could be a surge in junk bond defaults this year. As Business Insider explains :

Non-investment grade US companies face growing refinancing and default risks with interest rates expected to stay high and financial conditions for borrowers tightening, according to Moody's Investor Service.

The ratings agency says about $1.87 trillion of junk-rated debt is maturing between 2024 and 2028. That signifies a 27% jump from the $1.47 trillion recorded in last year's study for 2023-2027.

Debt maturing in the next two years accounts for about 18% of the five-year total, Moody's said, though the absolute amount for those two years has surged 25% compared to last year's study, to hit $333 billion.

Moody's analysts expect the US speculative-grade default rate to peak at 5.6% in January 2024, before easing to 4.6% by August 2024.

This could be a problem for the income-focused investors who would normally be interested in purchasing a fund such as this. After all, many income investors are retirees or other people who are dependent on their portfolios for income and naturally do not want to unduly risk their principal.

Fortunately, this fund does appear to be taking some steps to protect its shareholders against the losses that may accompany these defaults. First of all, take a look again at the chart above which shows the credit ratings that have been assigned to the securities in the fund's portfolio. While the overwhelming majority of the fund's assets are invested in junk debt, we can see that 85.48% of the overall portfolio is invested in either BB or B-rated debt securities. According to the official bond ratings scale , companies whose debt has one of these two ratings have sufficient financial capacity to carry their existing debt even in the event of a short-term economic shock. These companies do not have as strong a balance sheet as an investment-grade company, but they should still be able to avoid defaulting on their debt issuances in most situations. As these bonds account for the overwhelming majority of the fund's assets, we probably do not need to worry too much about defaults causing outsized losses in the fund's portfolio.

The fund also has a portfolio in which 304 unique issuers are represented. That should mean that no single issuer accounts for an outsized proportion of the fund's total assets. This is exactly what we see, and it is apparent in the largest positions in the fund:

BNY Mellon

As we can see, the largest issuer only accounts for 1.78% of the fund's total assets. This is not enough for it to have much of an impact on the portfolio as a whole. In fact, if any of these companies were to default on the debt securities that the fund holds, the coupon payments that the fund receives from the other assets in the portfolio would very quickly erase the losses. As such, we probably do not need to concern ourselves with default risk, as the only real threat here is if a large number of issuers were to default in rapid succession. That is certainly possible, but such a scenario would also be a sure sign that the economy as a whole has some very serious problems. It therefore would not really matter what assets an investor is holding in their portfolio as everything would be getting punished. The biggest risk when it comes to this fund is interest-rate risk, and we will discuss that in just a moment.

There have been a few changes to the fund's largest positions list since the last time that we discussed it. In particular, Ford Motor Company ( F ), LifePoint, Inc. ( LFPI ), and Tenet Healthcare Corporation ( THC ) have all been removed from the largest positions list. In their place, we have CHS/Community Health Systems, Inc. ( CYH ), TransDigm Group Incorporated ( TDG ), and Royal Caribbean Cruises Ltd. ( RCL ). The fund also changed the weightings of several of its largest assets, but this does not necessarily represent an intentional change on the part of the fund's management. However, this fund does have a 119.01% annual turnover rate, which strongly suggests that its management is very aggressively and actively changing the bonds that constitute the largest positions. This is, in fact, the highest annual turnover that I have ever seen a fixed-income fund possess. That could be a contributing factor to the fund's low yield relative to its peers, as a substantial amount of trading results in higher expenses. I have pointed this out in a number of previous articles, along with the implication that management needs to generate enough extra profits to cover the trading expenses for this strategy to make sense. This fund's share price has sometimes managed to beat the benchmark bond market index and sometimes fails to do so on a total return basis, depending on exactly which period of time we look at, so the strategy appears to be having mixed results.

The Rationale For The Sell Thesis

As mentioned in the introduction, the market drove up the price of fixed-income assets such as the ones held by this fund over the past three months. The reason for this is that investors are highly optimistic that the Federal Reserve will reduce interest rates this year, and bond prices move inversely to interest rates. Thus, what we have seen in the market is an attempt to front-run the Federal Reserve. However, the market may have taken things too far. As I have pointed out in a few recent articles, the market currently expects that the effective federal funds rate will decline by 1.384 percentage points in 2024:

{kind=link}

That would require five or six 25-basis point cuts to the federal funds rate by the Federal Open Market Committee at its next eight meetings. Currently, the market believes that there is a 62.9% chance that the first interest rate cut will come in March.

That scenario is unlikely to actually occur. As Zero Hedge pointed out this morning:

In his speech overnight, New York Fed President John Williams didn't quite give the impression that he is in a hurry to cut rates and spoke about the balance of risks. And earlier in the week, Raphael Bostic - who isn't the most hawkish on the Fed's policy committee - reiterated that he is looking at rate cuts starting only in the third quarter.

Thus, even the more dovish members of the Federal Open Market Committee doubt that there will be any need to cut interest rates in March. The failure of the Federal Reserve to cut the federal funds rate in March effectively torpedoes the entire narrative that is baked into bond prices right now and would almost certainly cause the assets that are held by this fund to surrender some of the recent gains that they have experienced.

We could see a potential correction starting today. The Bureau of Labor Statistics released the December inflation data this morning and it was not what the market wanted to see. The headline consumer price index showed a 3.4% year-over-year increase, but the market was assuming that the data would show a 3.2% year-over-year increase. Thus, the actual inflation data came in much hotter than the market expected, which supports the thesis that there is still a lot of work to do on the inflation front. That further weakens the odds for a March cut by the Federal Reserve and strongly suggests that junk bonds are substantially overpriced and due for a correction. This fund's share price will almost certainly suffer in the near term as the market reprices, so investors would be best off reducing their exposure to the fund today.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the BNY High Yield Strategies Fund is to provide its investors with a very high level of current income. In pursuance of this objective, the fund invests its assets into a portfolio of junk bonds that primarily deliver their investment returns in the form of direct payments to their owners. The yield on these bonds tends to be quite respectable in the current market, which should mean that this fund receives a reasonable level of income from the securities in its portfolio. It combines these payments with any money that it manages to earn through the trading of bonds that go up in price when interest rates drop. Finally, the fund pays all of this money to its shareholders, net of its own expenses. We might expect that this would give the fund's shares a very high yield.

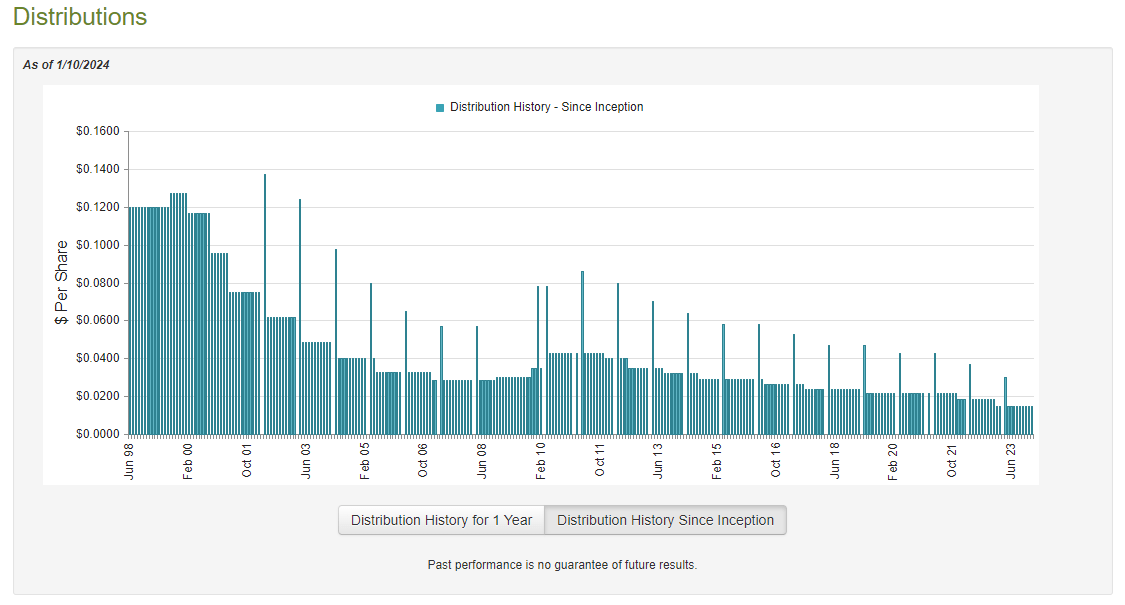

This is certainly the case, as the BNY Mellon High Yield Strategies Fund currently pays a monthly distribution of $0.0150 per share ($0.18 per share annually), which gives it a 7.76% yield at the current price. As mentioned in the introduction, this is a lower yield than can be obtained from other junk bond closed-end funds, although it is still higher than the index funds that invest in the space are able to deliver. Unfortunately, this fund has not been especially consistent with respect to its distribution over the years. As we can see here, the fund's distribution has been steadily decreasing over the past decade:

{kind=link}

This is something that is almost certainly going to be concerning for any investors who are seeking to earn a stable and consistent level of income from the assets that are in their portfolios. It is doubly concerning because this history is very different from the distribution history possessed by many other fixed-income closed-end funds. While there are several funds in the space that have regularly changed their distributions, most of them were able to deliver at least a few increases over the years. This fund has failed to accomplish that task and as such its investors have suffered from regular cuts to their income. This is not exactly what we want to see in an inflationary environment in which we all need more money to pay our bills.

As I have pointed out numerous times in the past though, the fund's history is not always the most important thing for any new investor in a fund. After all, new investors will receive the current distribution and the current yield and will not be affected by any adversity that caused problems for a fund's shareholders in the past. As such, the most important thing for our purposes today is to determine how well the fund can sustain its current distribution.

Fortunately, we have a very recent document that we can use for the purposes of our analysis. As of the time of writing, the most recent financial report for the BNY Mellon High Yield Strategies Fund corresponds to the six-month period that ended on September 30, 2023. The period of time that is covered by this report is quite nice because the market was not exactly friendly to bonds over the summer of 2023. Investors were digesting the strong possibility that they were wrong about the Federal Reserve cutting interest rates in the second half of 2023 so were selling off bonds and driving yields higher. This almost certainly caused this fund to suffer some losses, which will naturally be reflected in this report. This report is also more recent than the one that we had available to us the last time that we discussed this fund, so it will naturally be useful as simply an update.

During the six-month period, the BNY Mellon High Yield Strategies Fund received $11,152,692 in interest and $169,712 in dividends from the assets in its portfolio. This gives the fund a total investment income of $11,322,404 over the six-month period. It paid its expenses out of this amount, which left it with $7,654,620 available for shareholders. That was, fortunately, enough to cover the $6,546,288 that the fund paid out in distributions during the period.

For the most part, the distribution seems to be reasonably sustainable at the current level. The fund was more than capable of covering its distribution out of net investment income, although its net assets did decline a bit due to realized losses. However, in most cases, we do not really need to worry too much about a fund's distribution sustainability if it is fully covered with net investment income. This is doubly true right now since it seems that interest rates and yields will probably remain high for a while.

Valuation

As of January 10, 2024 (the most recent date for which data is currently available), the BNY Mellon High Yield Strategies Fund has a net asset value of $2.68 per share. However, the fund's shares only trade for $2.32 each. This gives the fund's shares a 13.43% discount on net asset value at the current price. That is a smaller discount than the 14.87% discount that the shares have had on average. As such, right now could be a reasonable time to dispose of some shares, as the discount could very easily widen in a market correction.

Conclusion

In conclusion, shares of the BNY Mellon High Yield Strategies Fund have benefited significantly from the market's optimism about near-term cuts to the federal funds rate. However, the market's expectations seem unlikely to actually prove accurate, as even some of the more dovish members of the Federal Open Market Committee are stating that the market's expectations are too optimistic. When we also consider that inflation data is actually coming in worse month-over-month and worse than the market's expectations, the obvious conclusion is that the Federal Reserve will not cut rates in March 2024 and this fund's shares are currently overpriced. As such, it would make sense to sell some or all of your position to lock in current profits. If you wish to retain some exposure to junk bonds, there are other funds available with higher yields that could be purchased to either keep your income the same or higher.

For further details see:

DHF: Sell This Low-Yielding Junk Bond Fund Before The Market Corrects