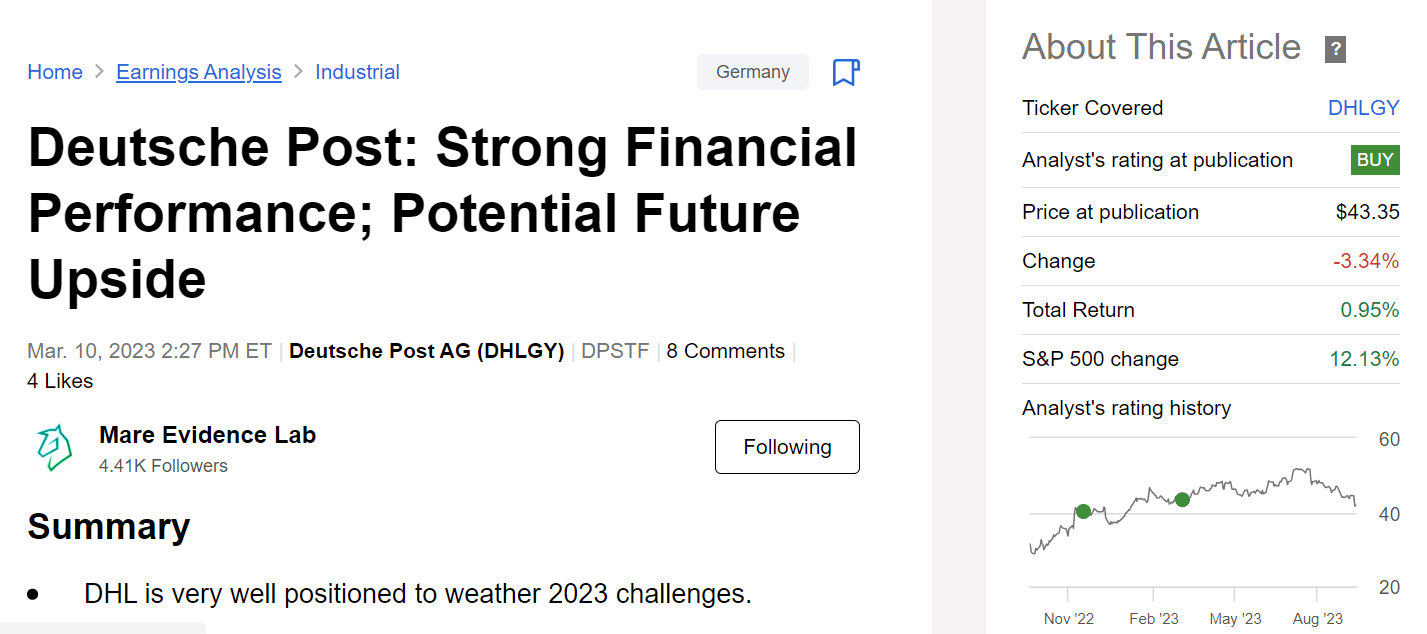

DPSTF - DHL Group Is A Solid Buy

2023-09-24 20:54:02 ET

Summary

- We see DHL as a strong buy opportunity due to its resilient performance and further growth opportunities.

- DHL's name change reflects its focus on digitalization and logistics, which could lead to investment monetization.

- Solid balance sheet, ongoing buyback, and a tasty DPS make DHL a long-term opportunity.

Since our last update on Deutsche Post AG (DHL Group (DPSTF) (DHLGY)), the company is back to an exciting stock price entry point ( Fig 1 ). Our internal team anticipates macroeconomic challenges in 2023, but we firmly believe the company is set to A New Normal . Here at the Lab, given the solid company's execution, we believe that the Deutsche Post conglomerate discount has grown and is not justified. In a nutshell, in our analysis, we have analyzed DHL's valuation compared to its historical average, and we find out that the company has traded at a 40% sum-of-the-part discount in the five-year pre-COVID-19 period. Despite a significant improvement in organic FCF generation today, DHL has widened its discount to approximately 60%. For this reason, we decided to move DHL as a strong buy opportunity. This is based on 1) resilient performance vs. a soft MACRO environment and 2) further growth opportunity.

{kind=link}

Mare Past Analysis

Fig 1

{kind=link}

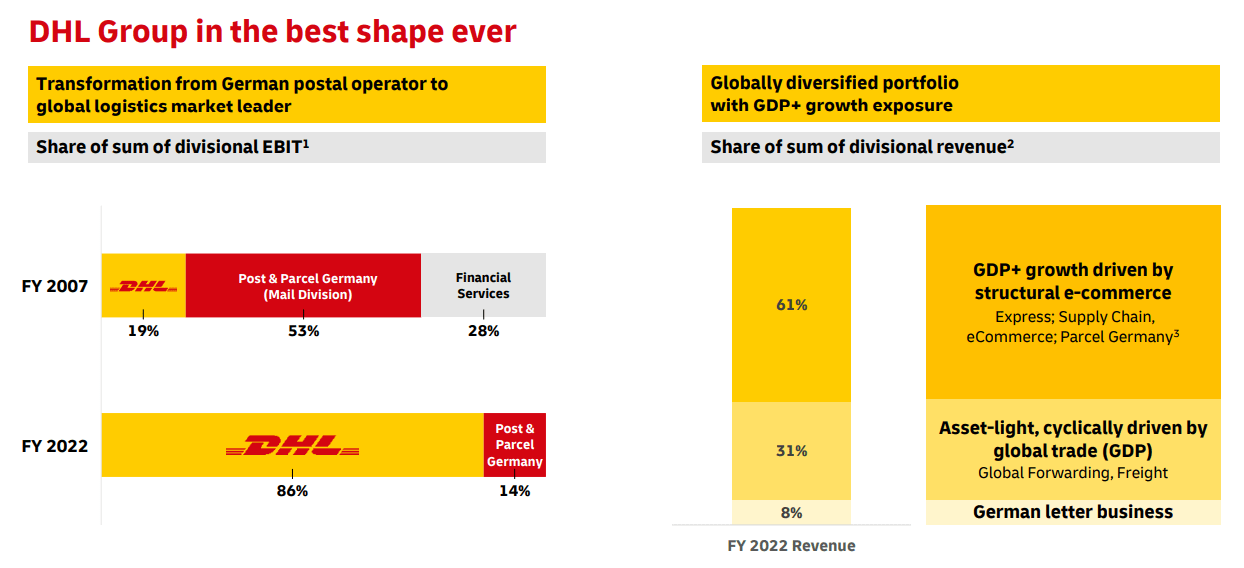

DHL business transformation

Fig 2

First, the Deutsche Post group is now renamed in DHL, which better reflects that the German Post & Parcel division only accounts for less than 10% of the total company's top-line sales. Here at the Lab, given the CAPEX investment, the company has an economic moat vs. competitors and is now in a phase where it might monetize its logistics investments and digitalization.

Why is DHL a buy?

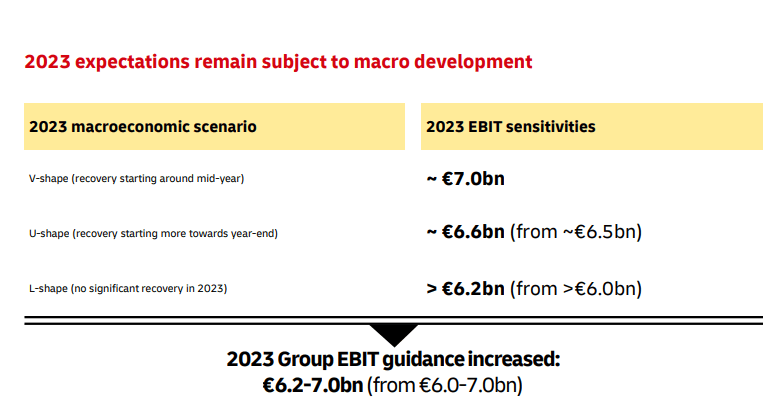

- Post H1 results, in the released outlook, DHL said it is still in the "L-shaped" scenario. This implied a limited volume recovery, but the company raised its lower-end core operating profit to €6.2 billion (from €6 billion - Fig 3). DHL management has always been prudent, and in our year-end estimates, we anticipate an EBIT of €6.72 billion;

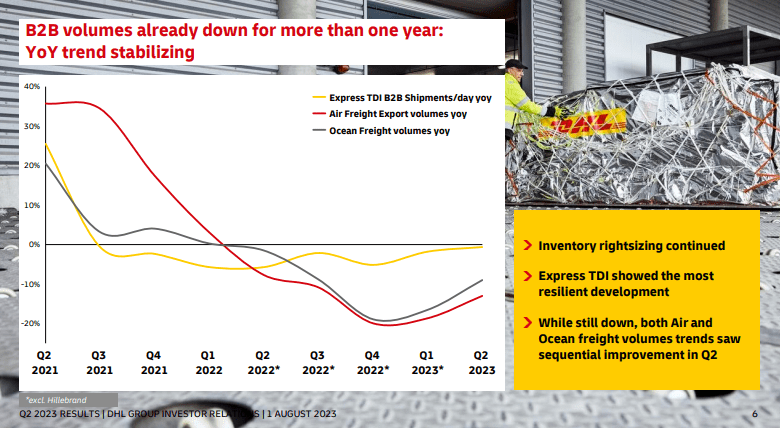

- Given the company's outlook, we see near-term earnings uncertainties but leave our future expectations unchanged. The macroeconomic backdrop is still soft, and the company is exposed to cyclical sectors, especially in the Express and Freight Forwarding segments; however, this momentum is at an inflection point, and volume growth might likely materialize post-Q4 (Fig 4). This is based on the ending of destocking activities and softer competitions. In number, The industry backdrop for DHL Express accounts now for approximately 55% of the company's total EBIT, and pricing power has increased. This is also recorded among US peers like FedEx (FDX) and UPS (UPS), with rigid cost control, lower wage increases, and constructive pricing power. While the Express division trend was at -3.7% shipments in Q2 vs. last year with B2C at -7% and B2B flattish, we see some e-commerce early signs of recovering, and this cannot go unnoticed;

- What is hard to justify and support our thesis is the fact that DHL passed a successful division restructuring program. The company's future operating leverage needs to be priced in. This is coupled with favorable and structural long-term growth drivers such as e-commerce and digitalization;

- In detail, in the last period, the company made significant investments in digitalization to enhance customer and employee experience. This might improve productivity and operational efficiency. DHL might leverage its advanced analytic tools to power B2B and B2C customer portals such as myDHLi , MeinService, and GoGreen . These solutions offer customer new tracking capabilities, and at the same time, the company optimize fuel consumption to provide cost-saving and better warehousing accuracy;

- Looking ahead, here at the Lab, we forecast a 4% revenue growth out to 2025 with an EBIT CAGR improvement of 9% per year, arriving at the €8 billion operating profit target already announced by the company (Fig 5).

{kind=link}

DHL 2023 target

Fig 3

{kind=link}

DHL volume recovery

Fig 4

DHL 2025 target

Fig 5

Conclusion and Valuation

DHL bearish thesis is predominately due to DHL Express EBIT evolution post-pandemic outbreak. Looking at the numbers, this division achieved €2 billion in 2019, with a €4.3 billion pick in 2021. A few investors believe this scenario is not sustainable. In our numbers, we forecast a €3.7 billion in 2023. We think Forwarding and Freight core operating profit still carries higher profits from the pandemic, and DHL earning diversification is now more stale. Having dealt with a softer macro backdrop in this period, the company has already transformed and demonstrated management ability and agility to overcome difficulties in the past quarters. The group is set to deliver EBIT growth on its GDP+ revenue exposures with a better business mix.

Even if we recognized that DHL might lack specific short-term positive catalysts, we see a solid track record in earnings execution and a gradual improvement in the macroeconomic outlook in the 2024-2025 period. Here at the Lab, we decided to raise our estimates thanks to solid H1 results with small divisional changes in the group earnings that led to a Fiscal Year core operating profit of €6.72 billion, 1% higher than the previous forecast. We believe that Wall Street might start to focus on the company's growth prospects, and we forecast an EPS growth of 12% per year by 2025. Again, to support our investment, we report DHL's commitment to buy back shares , representing 5.5% of the current market cap (€3 billion program) and a tasty dividend yield of 4.6%. We derived a target price of €55 per share, introducing a lower holding discount of 30%. This reflects DHL's better reliability in earning delivery. While Wall Street earnings broadly align with company consensus, we view the market's valuation as unjustified. Therefore, we reiterate our overweight target. Going to the downside, Parcel is the primary source of weakness. Secondly, the company's volume decline might continue and result in earning downside from consensus estimates. DHL's focus on digitalization poses higher data and cyber security risks. In addition, we recorded a higher employee turnover and sickness rate.

For further details see:

DHL Group Is A Solid Buy