DPSTF - DHL Group: Still Being Cautious And Maintaining 'Hold' Rating

2024-01-19 00:07:54 ET

Summary

- DHL Group - similar to UPS and FedEx - is reporting declining revenue as well as lower operating income and EPS.

- Management also lowered expectations, and it could be possible that the declining revenue is also the harbinger of a recession.

- DHL Group could be seen as fairly valued, but I would be rather cautious at this point.

It has been almost two years since I published my last article about back then named Deutsche Post AG which changed its name to DHL Group (DHLGY), ( DPSTF ) in July 2023 (we will talk later about the fact why renaming the company makes sense). In my article in March 2022, I called Deutsche Post a stable business with a tempting dividend yield of 4.2% but rated the stock as a "Hold".

After some ups and downs in the meantime, the stock price is now almost the same as it was when my article was published, but when including dividends the total return was 11% and the performance was more or less in line with the S&P 500 (SPY) which increased about 14% (not including dividends). In my article, I wrote a conclusion:

Deutsche Post is a solid investment with a high dividend yield. Even when calculating with cautious assumptions for the years to come, the stock is fairly valued or slightly undervalued and we can expect an annual return around 10%. And finally, Deutsche Post could surprise and continue to grow with a higher pace than in the years before COVID-19.

In the last few quarters, we saw rather declining revenue than increasing revenue - and hence let's take a closer look at DHL Group to determine if it is still a "Hold" or if we must change our outlook.

Disappointing Results

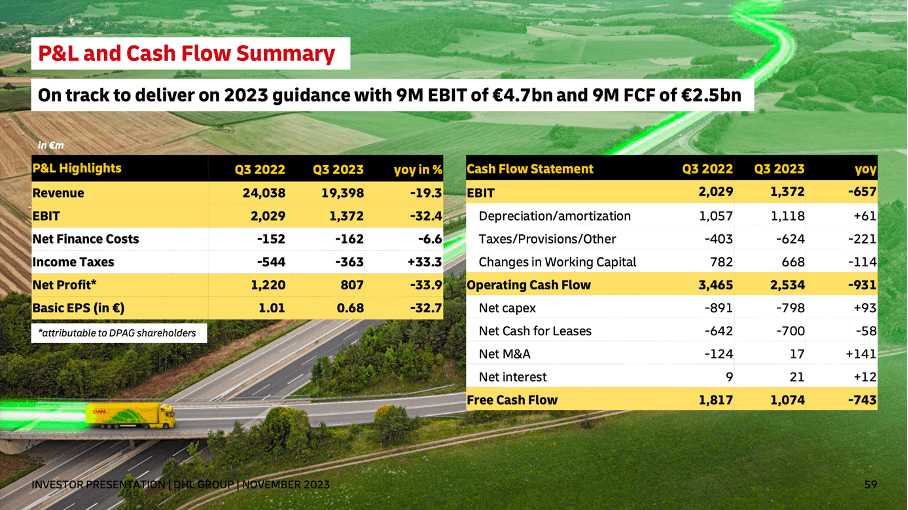

As always, we start by looking at the last quarterly results, which were not great. As mentioned above, revenue declined recently, and it was a rather steep decline. Compared to €24,038 million in the same quarter last year, DHL Group reported a revenue of only €19,398 million in Q3/23 - resulting in 19.3% year-over-year decline. EBIT also declined 32.4% YoY from €2,029 million in Q3/22 to €1,372 million in Q3/23 and diluted earnings per share declined from €0.99 in the same quarter last year to €0.68 this quarter - resulting in 31.3% YoY decline. Finally, free cash flow declined 40.9% YoY from €1,817 million in Q3/22 to €1,074 in Q3/23.

DHL Group November 2023 Roadshow Presentation

{kind=link}

To get the bigger picture, we can also look at the results for the last nine months, but the results are not really better. Revenue declined 14.5% year-over-year from €70,660 million in the first nine months of 2022 to €60,410 million in the first nine months of this year. EBIT declined 27.8% YoY from €6,514 million to €4,703 million and diluted earnings per share declined 31.2% YoY from €3.24 in the first nine months of 2022 to €2.23 in the first nine months of 2023. Free cash flow can be seen as the only glimmer of hope as the amount increased from €2,285 million to €2,507 million - an increase of 9.7% year-over-year.

Lowering Expectations

When looking at the updated full-year guidance, management is lowering expectations - especially for the mid-term (next few years). For fiscal 2023, DHL Group is expecting EBIT to be in a range of €6.2 billion to €6.6 billion (from previously expecting €7.0 billion at the upper end). Free cash flow is expected to be around €3 billion - however, this is excluding about €500 million for merger and acquisition. In my opinion, mergers and acquisitions are one way to use free cash flow and I would therefore not exclude this amount from the reported free cash flow.

Management commented:

So as you know, we started the year with three macro scenarios. The L, the U, and the V-shaped recovery scenario. The V-shaped scenario had assumed that there would be a recovery starting around midyear.

That has obviously not materialized, and that is why we have crossed out the V-shaped scenario. That leaves two potential outcomes for the development in the rest of the year. If we were to see no recovery in the remaining weeks of 2023, we would be in the L-shaped scenario.

And on that basis, we would still anticipate to deliver at least €6.2 billion in EBIT. Should there be a late pronounced peak, and in the U-shape scenario, we would expect to end at around €6.6 billion.

DHL Group November 2023 Roadshow Presentation

{kind=link}

DHL Group also lowered its mid-term guidance and is now expecting EBIT for 2025 to be in a range of €7 billion to €8 billion (compared to more than €8 billion before). And cumulative free cash flow for the years 2023 till 2025 is now expected to be in the range of €9 billion to €10 billion (compared to €1 billion more in a previous guidance).

Light vs. Shadow

When interpreting these statements, we also must ask the question if these numbers are just the harbinger of difficult times. And during the last earnings call it became obvious that management hoped for a quicker recovery, which did not happen so far:

So, we see this still as an ongoing market correction and also the aftermath of rising interest rates, which seems to have a longer drag on the macroeconomic environment than some might have expected. So, that might well take another one, two quarters until we see a substantial revival in freight volumes.

Rates, particularly on the ocean side on the spot market seem to have bottomed out, but at least on most trades that obviously longer-term contracts are still in place. So that will again, probably take another one, two quarters until that also the contract kind of renewal then reflects the new reality.

Other statements make it clear that management expected a quicker recovery and is rather surprised by how grim the situation is:

Now, looking towards the midterm guidance, we had to take into account the factual observation that there has been no market recovery yet. So, when you kind of like look at the length of the market downturn with a slow volume growth, that is now lasting even longer than what we experienced in the financial market crisis in 2008 and 2009. So, things are dragging on a bit longer.

At the same time, we are convinced that eventually we will see a cyclical recovery following the current cyclical downturn. So, we do expect to get back into a growth trajectory towards 2025."

One potential interpretation is the world heading towards a global recession and logistics and transportation are among the first sectors to experience weaknesses. And it is also not a great sign that competitors like United Parcel Service ( UPS ) or FedEx Corporation ( FDX ) are also reporting declining revenue in the last few quarters.

Another interpretation of the numbers is some kind of exaggeration during the pandemic years and lockdowns with all its consequences leading to huge freight and logistics volumes, especially in the e-commerce sector leading to revenue growth for logistics companies. And after the years 2020 to 2022 were rather outliers we are now just seeing a return to the mean.

In theory, both statements could be true. This is making it rather difficult to make up my mind what to expect for the years to come. When looking at most studies I could find, they expect the freight and logistics market to grow in the mid-single digits (see here , here , here , and here for example). And of course, these studies almost never expect a declining market and as these studies are looking at the next 5-10 years a potential recession might be balanced out again by better and more successful years.

But we should also not ignore that DHL Group might be hit hard by a steep recession or depression. E-commerce will decline, the freight volume will decline, and management is already pointing out the problems that arise quickly:

So, as already mentioned, in a business like Express, volume decline is putting a certain grind on the profitability of such a fixed asset network. But I think there's also a positive note to that, eventually, volumes will come back. And then we will see the same operating leverage turn into a tailwind again. So, when volume comes back, we will see the reversal of what is now a headwind.

A distribution network is usually a great asset - as long as volume is stable or growing. Such a distribution network can be the source of a wide economic moat making it very difficult for competitors to enter a market. However, when volume is declining for a longer time, it can become problematic. Of course, a few quarters of declining volume should not be problematic, but it has definitely a negative effect on profitability.

As long as we are weighing up the positive and negative aspects, it is worth mentioning that DHL Group has a stable business model, and we can even argue the company has a (wide) economic moat around its business.

DHL Group November 2023 Roadshow Presentation

{kind=link}

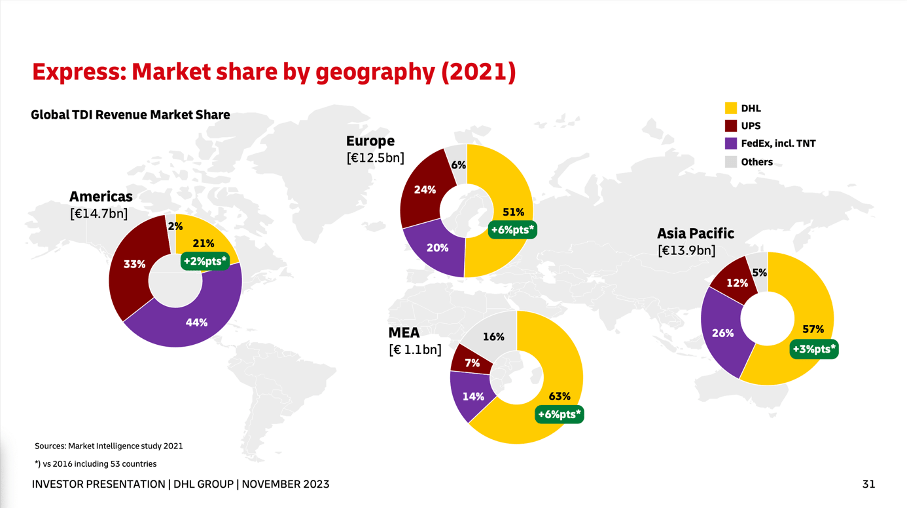

And while the company is still struggling in the American market (despite the company already having a market share of 21%), it is clearly dominating Europe - ahead of UPS and FedEx. Additionally, DHL Group also dominates the Asia-Pacific region with a market share of 57% and the Middle-East-Africa region with a market share of 63%. And of course, the express business is not everything, but it is contributing almost half to the company's overall EBIT.

DHL Group November 2023 Roadshow Presentation

{kind=link}

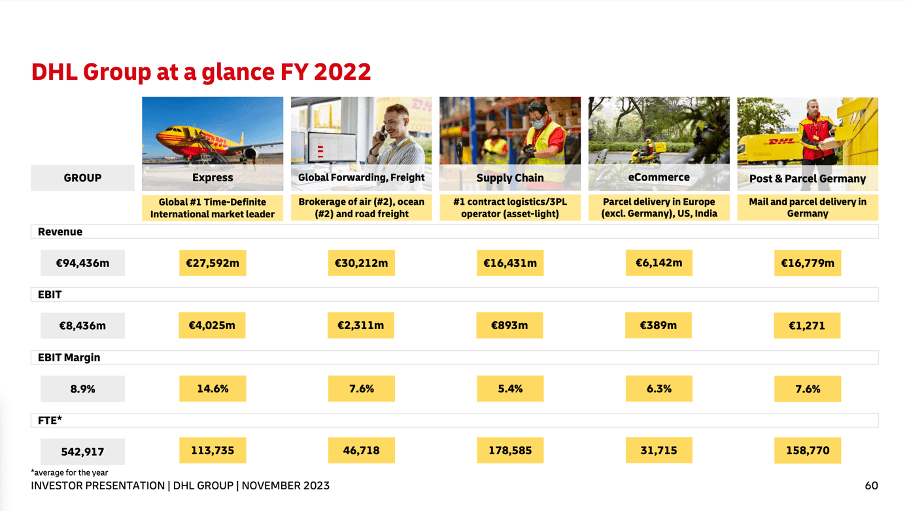

DHL Group is not only dominating the express market, but it is also dominating the post and parcel market in Germany (its original core business), and among business customers in Germany the company has a market share of 62%.

DHL Group November 2023 Roadshow Presentation

{kind=link}

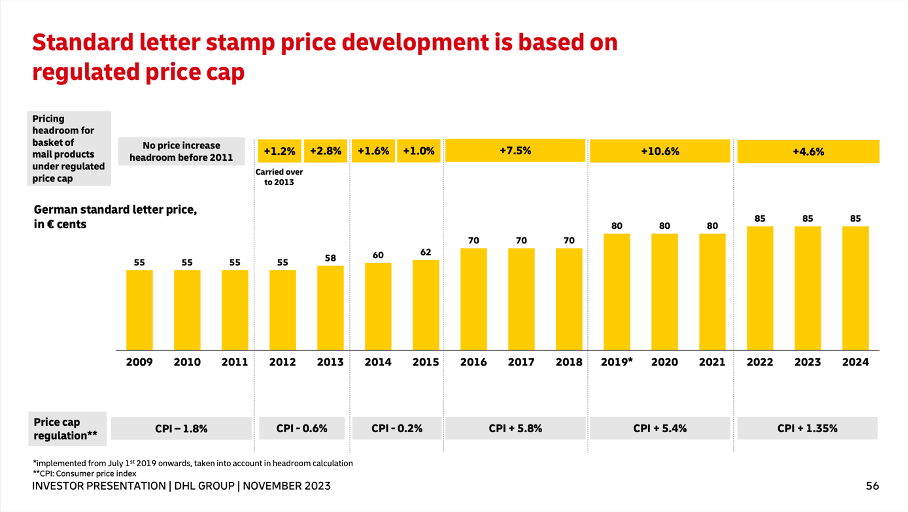

Although the standard letter stamp price constantly increased in the last 15 years from 55 cents in 2012 to 85 cents right now, the Post & Parcel Germany division is contributing less and less to the overall EBIT of the business. In 2007, it was responsible for more than 50% with DHL contributing only 19%. In 2022, DHL was responsible for 86% of the company's EBIT, and Post & Parcel Germany contributed only 14%. That is also the reason why it made sense to use "DHL Group" as the company name instead of "Deutsche Post".

It is rather difficult to reach a conclusion between a solid business model, high market share, and moderate growth expectations on the one hand and the risk of a recession on the other hand. In such a scenario where we don't know what might happen and if we should be bullish or bearish, I would be rather cautious.

Dividend

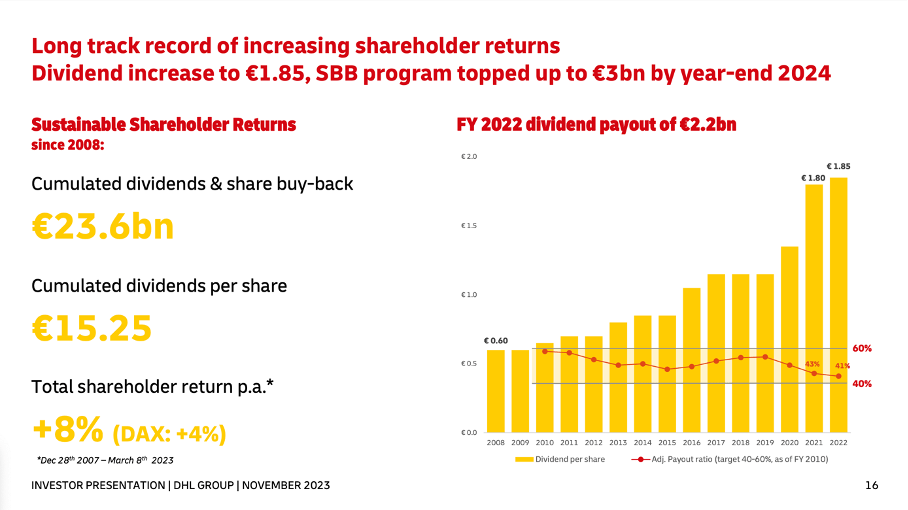

In my last article, I mentioned the dividend of Deutsche Post as a huge incentive to buy. And especially in the last few years, Deutsche Post increased its dividend at a high pace. In the years leading up to 2019, management kept the dividend stable for several years, but between 2019 and 2022 the dividend increased about 60% from €1.15 to €1.85.

DHL Group November 2023 Roadshow Presentation

{kind=link}

However, we should not expect the dividend to increase at a similar pace in the years to come. To be honest, I would also not be surprised if the dividend is kept stable once again. When looking at 2022 results, the company paid out 43% of its earnings (which is an acceptable payout ratio), but when comparing €2,205 million in dividends paid to a free cash flow of €3,067 million, we get a payout ratio of 72%.

For fiscal 2023, management is expecting once again a free cash flow of €3 billion and keeping the dividend stable would result in a similar payout ratio. By the way, management is expecting free cash flow in 2023 till 2025 to be between €9 billion and €10 billion, which would result in a similar payout ratio in 2024 and 2025 as well (when the dividend is kept stable). Considering these assumptions, I don't think DHL Group will raise the dividend - or if it is raised it will only be a slight raise. Even when the dividend is kept stable, investors get a dividend yield of 4.1% which is solid.

{kind=link}

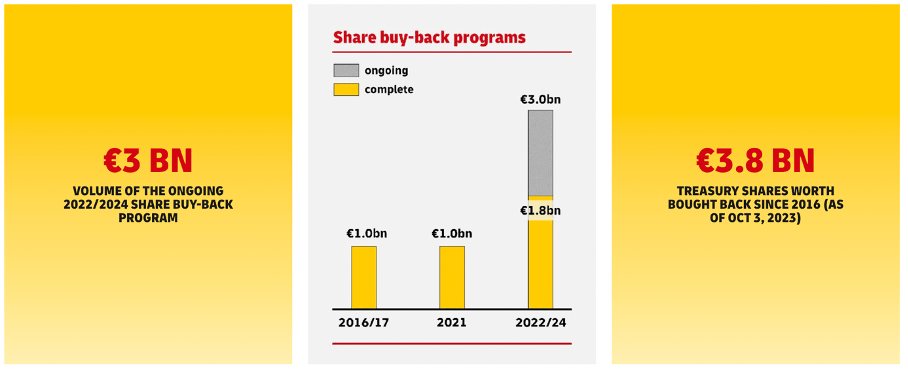

We should also mention that DHL Group is buying back shares - not excessive (similar to many other German companies) but it spent a few billions on share buybacks in the last few years. And the ongoing share buyback program has a volume of up to €3 billion with €1.8 billion already spent so far. As of October 3, 2023, the company bought back treasury shares worth €3.8 billion in total.

Intrinsic Value Calculation

A final step in assessing a business is usually to determine if the stock is fairly valued or not. On the surface, DHL Group seems rather cheap (or at least slightly undervalued). When taking the trailing twelve-month earnings per share of €3.34, the stock is trading for a P/E ratio of 13.4 right now. And for a stable and growing business, this is certainly an acceptable valuation multiple. When looking at the price-free-cash-flow ratio, the stock is trading for 17 times free cash flow when using TTM numbers once again. And when using expected free cash flow for 2023 (€3.5 billion - including M&A) we get a P/FCF ratio of 16.

Both metrics indicate a business that can be called fairly valued or even undervalued, but for a clearer picture let's use a discount cash flow calculation. As a basis for our calculation, we use a 10% discount rate (as always) and we calculate with 1,191 million outstanding shares. We could take about €3.5 billion in free cash flow as a basis, but let's be a little more cautious. Management is expecting free cash flow for the next three years (including FY23) to be between €9 billion and €10 billion and therefore we rather take €3 billion as a basis.

In my opinion, expecting 5% as a long-term growth rate for the years to come is realistic as it is in line with the long-term growth rates DHL Group could achieve in the past and with the expectations of the studies mentioned above. When calculating with these assumptions we get an intrinsic value of €50.38 for DHL Group and the stock would be slightly undervalued at this point.

Conclusion

We could make the argument that DHL Group is fairly valued at this point or even slightly undervalued. However, the scenario above does not really take into account the risk of another major recession or depression. And as I lean rather towards the side of caution and as we don't know what will happen, I will rate the stock rather as a "Hold".

For further details see:

DHL Group: Still Being Cautious And Maintaining 'Hold' Rating