HELKF - Diageo And Brown-Forman: Like Them Both But For Different Reasons

Summary

- Diageo plc and Brown-Forman Corporation, the two famous alcoholic beverages producers, are both market leaders in certain areas. Because of their solid and reliable earnings, their stocks never seem to be cheap.

- In this detailed comparative analysis, I will discuss the two companies' businesses, growth prospects, and profitability.

- I will also compare their balance sheets, highlight key risks, and evaluate dividend track records and reliability.

- Finally, I will value the two companies' stocks (both are down nearly 20% from their 52-week highs) and outline my own positioning and next steps.

Introduction

As an investor who greatly admires Peter Lynch and his strategies, I always wonder how many investment cases in Diageo plc ( DEO , DGEAF ) and Brown-Forman Corporation ( BF.A , BF.B ) have their origins in a bottle of Johnnie Walker and Jack Daniels, respectively. The two companies are among the top players in the alcoholic beverage space and their stocks are seemingly never cheap. Only in early 2020 did shares of both companies briefly trade at discount valuations, as bars seemed to be closed for good and travel-related restrictions dealt another blow to the companies' sales.

High inflation, rising interest rates (and thus higher discount rates for stocks), and a looming recession have generally lowered investor interest in equities. BF and DEO valuations, while still relatively high, have come down significantly - both are down nearly 20% from their 52-week highs. This raises the question of whether now is the time to open a position in either company, and more importantly, whether either is the better long-term investment.

In this article, I will compare the brand portfolios of the two companies, their geographic footprints, their growth records, the quality of their balance sheets, key risks, and current valuations. My regular readers know that I am a dividend investor by nature, so the analysis would be incomplete without an assessment of dividend safety and track record.

Overview Of Diageo And Brown-Forman

Diageo is the world's largest Scotch whisky company, with an estimated market share of around 38%. The company owns a wide range of blended and single malt whiskies, including Johnnie Walker, J&B, Bell's, Buchanan's, Oban, Talisker, Lagavulin, and Singleton. I am not really a fan of pure-play brewery stocks (e.g., Heineken ( HEINY , HINKF ) or Anheuser-Busch InBev ( BUD , BUDFF )) for a variety of reasons, but I very much welcome Diageo's ownership of Guinness, the world's leading Irish stout brand. All in all, Diageo's portfolio is well rounded, with well-known vodka, rum, gin, mezcal and cream liqueur brands in addition to its broad portfolio of blended and single malt Scotch whisky and stout. More recently, the company has also branched out into the hard seltzer category - a business that, while not yielding premium margins, is nonetheless important to capture interest of younger adult customers and should help raise brand awareness of Diageo's premium offerings. In this context, it seems worth noting that Diageo is also working with other companies, such as The Vita Coco Company , to bring convenient ready-to-drink alcoholic beverages to market.

Diageo operates globally, generating approximately 40% of its net sales in fiscal 2022 in North America, 21% in Europe, 19% in Asia Pacific, 11% in Africa and 10% in Latin America. With net sales (after excise taxes) of £15.4 billion in fiscal 2022, it is significantly larger than Brown-Forman (net sales of $3.9 billion in fiscal 2022). However, BF also operates globally, with 51% of its fiscal 2022 net sales outside the U.S. - 29% in developed markets (countries in Western Europe), 18% in emerging markets (mostly Mexico, Poland and Brazil), and the remaining 5% in travel-retail, unbranded products, and bulk.

Primarily due to its smaller size, Brown-Forman cannot compete with Diageo when it comes to the breadth of its brand portfolio . However, Brown-Forman owns the world's best-selling whiskey brand with Jack Daniel's. Jack Daniel's is available in a variety of styles, such as RTD, Tennessee Honey, No. 27 Gold, 10-Year-Old and Double Oaked. Brown-Forman also owns well-known bourbon whiskey brands such as Woodford Reserve, Old Forester and Coopers' Craft, as well as Scotch whisky brands Benriach and Glen Dronach. The company also owns tequila , vodka and gin brands and recently announced the purchase of the Diplomático rum brand. First and foremost, however, Brown-Forman is a whisk(e)y company, with 79% of sales in fiscal 2022. Similar to Diageo, Brown-Forman has also entered the ready-to-drink business (see its portfolio here ), and the most significant announcement in this regard is that the company plans to launch a Jack Daniel's mixed with Coca-Cola as a ready-to-drink cocktail. The drink will contain about 5 percent alcohol by volume, depending on the market, and will be available as a sugary or sugar-free version.

It is clear that both companies have solid brand portfolios, that they convey a strong sense of quality and exclusivity through their focus on aged spirits, and that they follow current trends while staying true to the image and heritage of their brands. Diageo, as the larger company (also in terms of market capitalization - $101 billion vs. $31 billion as of January 5, 2023), is better diversified and owns several leading brands, but Brown-Forman's Jack Daniel's franchise should not be underestimated either. Both companies benefit from economies of scale and are diversified internationally. However, investors who want to participate in the growth of emerging markets (particularly in Asia and Africa) are better served by Diageo. Conversely, investors who want to avoid the heightened risks of these markets should appreciate Brown-Forman's focus on developed markets.

Past Growth, Future Expectations And Profitability

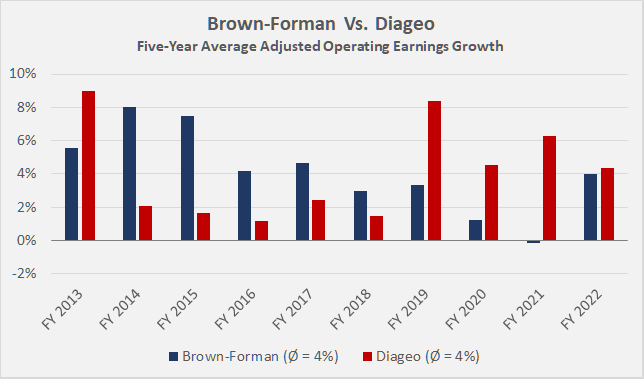

Figure 1 compares the net sales growth of the two companies over the last ten years, based on five-year average growth rates. Since both companies are growing both organically and through acquisitions, the average sales growth of 3% per year does not seem excessive. However, both Diageo and Brown-Forman are routinely optimizing their brand portfolios by divesting unprofitable assets and focusing on high-margin businesses. This has largely resulted in slightly better operating profit growth (adjusted for impairments), averaging 4% over the past decade for both companies, again based on five-year average growth rates (Figure 2).

Figure 1: Five-year average net sales growth rates of Brown-Forman [BF.A, BF.B] and Diageo [DEO, DGEAF] (own work) Figure 2: Five-year average adjusted operating earnings growth rates of Brown-Forman [BF.A, BF.B] and Diageo [DEO, DGEAF] (own work)

{kind=link}

{kind=link}

Long-term average operating profit growth rates of around 4% are certainly not bad for companies in mature businesses. As an aside, earnings per share growth have been even better due to regular share repurchases - Brown-Forman reduced its outstanding shares (net of shares issued due to exercised options) by almost 11% over the past decade, while Diageo repurchased about 8% of its shares on a net basis, resulting in boosts to earnings per share of 12% and 8%, respectively.

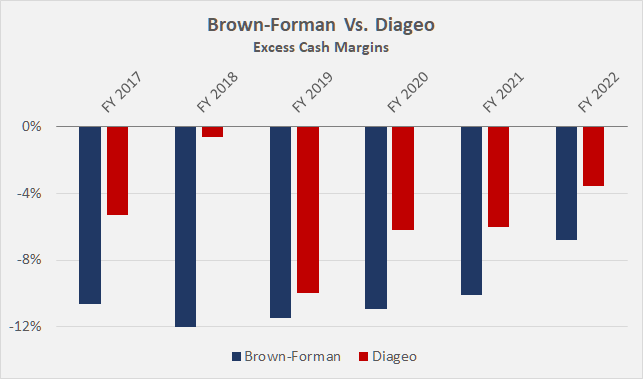

However, my regular readers are accustomed to the fact that I am not a fan of adjusted earnings per share and instead focus on cash flow. Cash flows are much more difficult to manage and provide a pretty transparent view of a company's earnings power. Operating and free cash flow ((FCF)) growth at Brown-Form and Diageo is in line with operating profit growth, but when looking at cash flow conversion, Diageo does slightly better, as evidenced by its less negative excess cash margin. The fact that neither company shows a meaningful trend (Figure 3) suggests that earnings quality is intact at both companies.

Figure 3: Excess cash margins of Brown-Forman [BF.A, BF.B] and Diageo [DEO, DGEAF], calculated by subtracting adjusted operating earnings from operating cash flows and dividing my net sales (own work)

{kind=link}

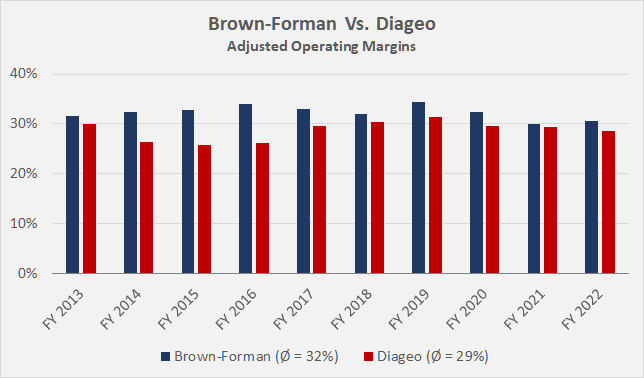

As indicated in the previous section, both companies have high margins. Adjusted operating margins are fairly similar at around 30%, but Brown-Forman slightly outperforms Diageo, likely due to its smaller business and less complex organization (Figure 4). However, Diageo's better cash flow conversion means that its FCF margin (after normalizing FCF for working capital movements and stock-based compensation expense) is in line with Brown-Forman at around 20%.

Figure 4: Adjusted operating margins of Brown-Forman [BF.A, BF.B] and Diageo [DEO, DGEAF] (own work)

{kind=link}

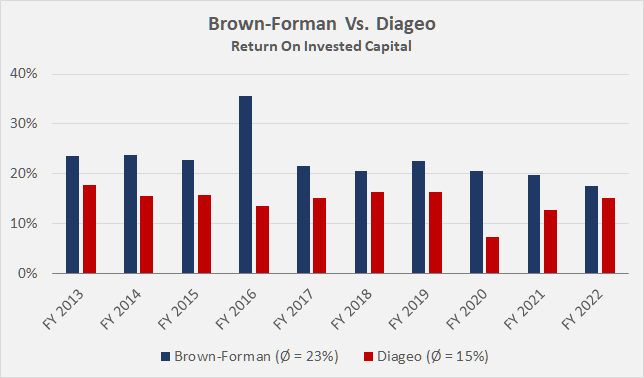

The aforementioned less complex organizational structure and, more importantly, somewhat leaner asset base lead to a historically better return on invested capital ((ROIC)) at Brown-Forman. However, the decline in recent years should be kept in mind and is at least partially due to declining asset turnover (0.8x to 0.6x over the last decade) and working capital inefficiencies. Brown-Forman's cash conversion cycle has increased from 330 days to 450 days over the last ten years, primarily due to an increase in inventory days (314 days to 422 days). The same is true for Diageo, albeit to a lesser extent (inventory days increased from 350 to 400 days), but the U.K. company more than offset this increase by lengthening payment terms with suppliers (days payables outstanding increased from 90 to more than 140 days over the past decade). Diageo's management has done a remarkable job of maintaining a constant return on invested capital of around 15% (Figure 5), well above its Capital Asset Pricing Model ((CAPM)) derived weighted average cost of capital ((WACC)) of currently around 7.1% . Brown-Forman's excess ROIC is currently around 10% (WACC of 7.7% ), still better than Diageo's (8% for fiscal 2022). However, when better cash flow productivity is taken into account, the difference becomes practically irrelevant. The important takeaway is that both companies continue to generate solid excess returns on their invested capital - both on an operating income and cash earnings basis. However, Diageo appears to be somewhat better managed for its size, but at the same time it obviously benefits from a better position relative to its suppliers and better economies of scale.

Figure 5: Return on invested capital of Brown-Forman [BF.A, BF.B] and Diageo [DEO, DGEAF] (own work)

{kind=link}

Turning back to sales and earnings growth, both companies continue to navigate these arguably challenging times very well.

Fiscal 2022 (ended June 30, 2022) was another great year for Diageo. Sales recovered well from the lockdown-plagued period, and the company benefits from solid pricing power thanks to its mostly premium brands. Diageo's North America in fiscal 2022 were up 17% year-over-year ((y/y)). Sales in other regions grew even faster (Latin America, Europe and Africa - up 46%, 26% and 19% y/y, respectively) or slightly weaker (Asia Pacific, up 16% y/y), which is understandable given China's still-strict lockdown policies. North America is also Diageo's strongest market in terms of operating margin (40%, down 268 bps y/y), followed by Latin America (35%, up 631 bps y/y), Europe (32%, up 684 bps y/y), Asia Pacific (25%, up 22 bps y/y), and Africa (19%, up 662 bps y/y). Obviously, there is a lot of room for margin expansion in emerging markets.

Brown-Forman's fiscal 2022 (ending April 30, 2022) was similarly successful, with overall sales growth of 14% y/y. The strong upturn in travel retail (up 65% y/y) is hardly surprising, but obviously not very significant (see above). Still, sales growth of 10% in the U.S., 12% in developed markets and 24% in emerging markets is definitely a sign of strength. Brown-Forman does not report operating profitability on a segment basis. However, as seen earlier in Figure 4, Brown-Forman was able to slightly improve its adjusted operating margin in fiscal 2022, confirming that the company is in a similarly strong position to Diageo, which is hardly surprising given its top-selling brands. Fiscal 2023 is also off to an excellent start for the company, which recently raised its full-year sales guidance to the high-single digit range . Inflationary pressures have moderately weighed on gross margins in the first half of fiscal 2023, at around 130 basis points. In this context, it seems worth noting that Brown-Forman, like Diageo, operates at a luxurious long-term average gross margin of 60%.

For the coming years, net sales growth expectations are relatively similar for both companies: 6.3% on average for Diageo and 6.6% for Brown-Forman . Of course, given the very uncertain macroeconomic environment, I would not overinterpret these forecasts. What is important is that both companies are in a strong position to continue to deliver good results through innovative product offerings and collaborations with third parties, by exercising their pricing power, and by continuing to rationalize their operations. Their successful efforts towards premiumization of their offerings (see related interviews with BF’s CEO Lawson Whiting and Diageo’s CEO Ivan Menezes ) beautifully underline the earnings power of these companies in inflationary periods, provided that middle class households continue to be able to maintain their standard of living.

Balance Sheet Quality

Brown-Forman and Diageo are both consumer staples companies and therefore relatively insensitive to economic cycles (see discussion of risks below). Because of their relatively stable earnings and cash flows, these companies can also hold larger amounts of debt without getting into trouble. Of the two companies, Diageo carries significantly more debt on its balance sheet than Brown-Forman . Comparing net debt to free cash flow is an illustrative way that shows the hypothetical time period for repaying a company's debt if it were to suspend dividend payments and share repurchases. With net debt of £14.2 billion at the end of fiscal 2022, and using the four-year average of normalized free cash flow ((nFCF)) to smooth out one-time events in fiscal 2020 and 2021, Diageo would need 5.4 years to repay all of its debt - far from unmanageable, but substantial. In this context, Brown-Forman appears much more conservative at just 2.1 years. Diageo's interest coverage ratio, at 7 times four-year average nFCF before interest, is also weaker than Brown-Forman's 9.5 times. Pension liabilities can be found on both companies' balance sheets, but they are not significant.

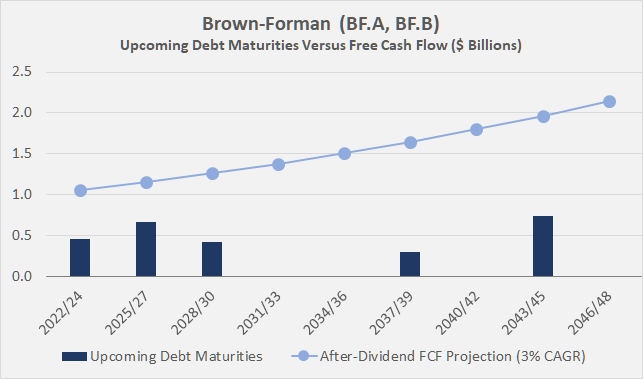

I would argue that Diageo's leverage is still well under control and the company is very capable of maintaining such leverage given its size and portfolio strength. An interest coverage ratio of 7x is anything but worrisome for a blue-chip consumer staples company. However, considering that interest rates are still rising and will likely remain elevated for a significant period of time, it is important to review the maturity profiles of the two companies. Since large companies typically refinance their debt rather than repay it, a left-skewed maturity profile carries the risk of refinancing transactions at unfavorable interest rates given the current environment. Unsurprisingly, the conservative nature of Brown-Forman is also reflected in its maturity profile. Figure 6 illustrates that the company is in a very reassuring position - it could repay its debt at maturity out of free cash flow and even continue to pay its dividend. Share buybacks, of course, are a different story and are not included here. The rising interest rate environment is not an issue for the company, also because of Moody's A1 investment grade rating (A+ S&P equivalent) with a stable outlook from January 2020. Standard & Poor's currently rates Brown-Forman's long-term debt at A-, which is two notches lower.

Figure 6: Debt maturity profile of Brown-Forman [BF.A, BF.B] at the end of fiscal 2022 in three-year buckets, compared to its four-year average normalized free cash flow after dividends (own work)

{kind=link}

Diageo's maturity profile (Figure 7) is left skewed and the company will need to refinance at least some of its debt at maturity. The company is in a less comfortable position than BF, but I doubt that the current interest rate environment will have a material negative impact on Diageo's debt servicing ability after reviewing the coupon rates on its upcoming maturities. Also, the long-term debt rating of A3 by Moody's (A- S&P equivalent) with a stable outlook unchanged since November 2019 is quite reassuring. Finally, the five-year credit default swap spread for Diageo is very low at around 35 basis points. At the height of the COVID-19 pandemic, the spread increased to around 70 basis points, about half of what it was during the Great Financial Crisis. Unfortunately, I have not found CDS data for Brown-Forman but I obviously do not expect its insurance premiums to be more expensive than those for Diageo's debt.

Figure 7: Debt maturity profile of Diageo [DEO, DGEAF] at the end of fiscal 2022 in three-year buckets, compared to its four-year average normalized free cash flow after dividends (own work)

{kind=link}

Of course, as mentioned earlier, Brown-Forman will most certainly also refinance its debt as it matures (it is not ideal to work with 100% equity-financed assets). While Diageo's leverage is far from worrisome, the different maturity profiles and overall debt levels and interest coverage ratios confirm that Brown-Forman is more conservatively managed - an aspect that, as a long-term investor, I value highly and am willing to reward with a slightly higher valuation multiple (see final section).

Key Risks

The risks underlying an investment in Diageo and Brown-Forman are broadly similar. I will not go into risks related to supply chain issues, workforce challenges, or inflationary pressures, as these are very visible right now.

As producers of alcoholic beverages, the two companies are not what I would call cyclical, but in a severe recession, with rising unemployment and less disposable income, the companies' focus on premium brands will likely lead to declining sales and earnings as consumers shift to discount brands. I own Diageo in a diversified portfolio built with Maslow's hierarchy of needs in mind. As a result, I do not mind the somewhat higher earnings volatility compared to companies that sell low-dollar, everyday products, such as Procter & Gamble ( PG ) or PepsiCo ( PEP ). By comparison, Diageo appears to be the riskier choice from an earnings volatility perspective (see FAST Graphs charts in the valuation section below), while Brown-Forman's earnings and cash flow growth are remarkably stable.

Diageo is based in the United Kingdom, and therefore the British pound is the company's reporting currency. A U.S. investor, therefore, is taking on currency risk. Personally, I also maintain a globally diversified portfolio from a currency perspective, so I actually welcome a portion of my dividend income being paid in British pounds, but ultimately it comes down to the risk tolerance of the individual investor. In theory, all living expenses should have a corresponding income in the same currency. Therefore, Brown-Forman seems to be a better choice for risk-averse investors with living expenses in U.S. dollars, but of course, it is important to remember that the company generates half of its net sales outside the U.S. and thus in foreign currencies - there is no free lunch on Wall Street, after all, and hedging foreign currency exposure is a costly and often ineffective endeavor.

Another risk worth mentioning is that both companies export alcoholic beverages and are therefore potentially subject to tariffs. While it seems idle to debate the likelihood and extent of tariffs, but given the increasingly protectionist behavior of governments around the world, this is a risk to consider in one's due diligence.

Since the two companies maintain their pricing power largely thanks to their strong brands, scandals of any kind could damage the reputation of the valuable brands, leading to a decline in sales, profitability and would also go in hand with impairment charges of intangible assets and goodwill.

A risk that is only relevant for investors in Brown-Forman (which can also be seen as a positive aspect) is its ownership structure. Brown-Forman trades as Class A ( BF.A ) and Class B ( BF.B ) shares, with the difference being that the latter are non-voting shares but trade with higher liquidity. The majority of the Class A shares are held by members of the Brown family. Of course, the family has a vested interest in the continued success of the company, but minority investors should understand that they are at the mercy of the Brown family's decisions.

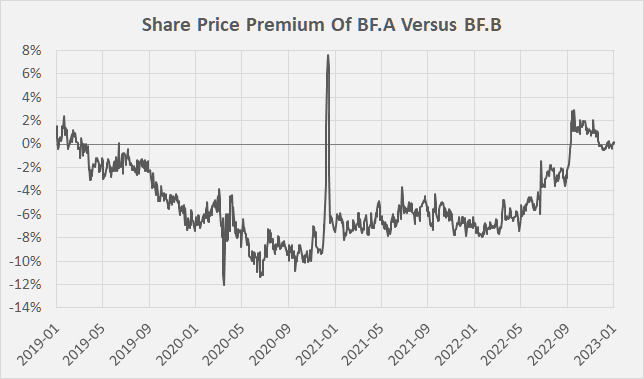

As an aside, the Class A shares trade at a premium or discount at times. Figure 8 nicely illustrates the implications of ETF ownership (owning mostly Class B shares) during times of elevated volatility. Building a position in the Class A shares when they trade at an unwarranted discount is a promising endeavor to realize a small arbitrage profit. I reported on a similar – albeit opposite but ultimately quite profitable – opportunity in May 2022, when preferred shares of German industrial/staples conglomerate Henkel ( HENKY , HELKF ) traded at par with the common shares for a short period. The spread has widened to its long-term average of 10% in recent months.

Figure 8: Share price premium of Brown-Forman’s Class A shares [BF.A] in percent compared to the Class B shares [BF.B] (own work)

{kind=link}

Dividend Safety And Track Record

Both companies are very reliable, income-generating stocks. Since its formation in 1997 from the merger of Grand Metropolitan and Guinness plc, Diageo has paid a steadily growing dividend, meaning that by 2023, with 25 consecutive increases, the company will be a dividend aristocrat. U.S. shareholders holding Diageo via ADRs (type 4:1, issued by Citibank ) will, of course, receive four times the regular dividend, but we should note that unlike U.S. companies, Diageo pays its dividend in two installments, split roughly 40/60. There are usually ADR fees for processing the dividends, but the United Kingdom does not impose a withholding tax, unlike most European countries. Of course, this might change going forward.

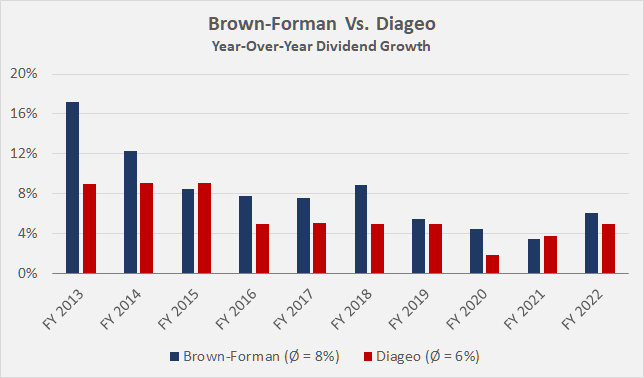

Diageo's long-term average dividend growth rate is 6.2%, but for obvious reasons - and also because of increasing leverage - dividend growth has slowed somewhat in recent years (Figure 9). With a current payout ratio of 65% in terms of four-year average nFCF, there is room for growth, so investors can expect to at least maintain the purchasing power of their dividend income in the future, assuming inflation declines to a 4% to 5% level and stays there for the foreseeable future.

Brown-Forman, as a U.S. company, pays its dividend in four equal installments each year and occasionally pays a special dividend, which I did not include in calculating the company's long-term average dividend growth rate. Over the past decade, management has increased the dividend by an average of 8.2% per year, and the family-run company is obviously very proud of its dividend, as evidenced by a press release issued in the midst of the COVID-19 pandemic, announcing that the 75 th year of consecutive dividend payment. As a long-term investor, such statements - in the midst of troubled times - are music to my ears. With a payout ratio of about 50% of four-year average nFCF, there is plenty of room for growth, especially considering the conservatively managed balance sheet.

Figure 9: Year-over-year dividend growth rates of Brown-Forman [BF.A, BF.B] and Diageo [DEO, DGEAF] (own work)

{kind=link}

If there is one thing that would bother me from the perspective of an income-oriented investor, it is the current low dividend yields. Diageo's current dividend yield is 2.1%, which is still reasonable, but Brown-Forman's is only 1.2%. If the two companies maintain their long-term average dividend growth rates, an investor taking a position today would have to wait 11 years and 15 years, respectively, to earn a yield on cost that represents the current yield of long-term U.S. government bonds of 3.8% (see Figure 10).

Figure 10: Yield on cost projections for Brown-Forman [BF.A, BF.B] and Diageo [DEO, DGEAF], assuming the companies maintain their long-term average dividend growth rates of 8.2% and 6.2%, respectively (own work)

{kind=link}

Valuation And Verdict

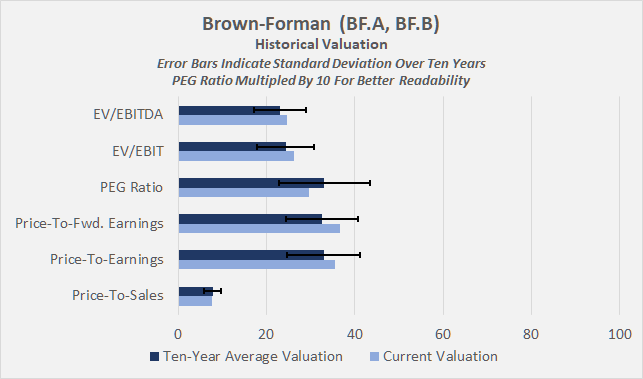

The rather low dividend yields alone indicate that the shares of Brown-Forman and Diageo are not cheap. However, the historical valuations shown in Figure 11 and Figure 12, respectively, indicate that the shares are currently trading at historically average valuations. It is important to remember, however, that these valuations are the result of a very strong bull market and should therefore be taken with a grain of salt.

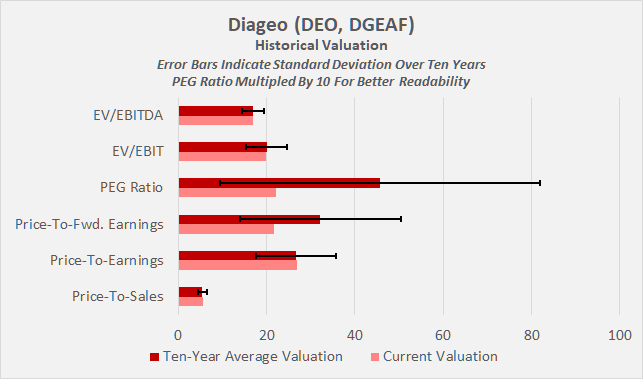

Figure 11: Historical multiples-based valuation of Brown-Forman [BF.A, BF.B] (own work) Figure 12: Historical multiples-based valuation of Diageo [DEO, DGEAF] (own work)

{kind=link}

{kind=link}

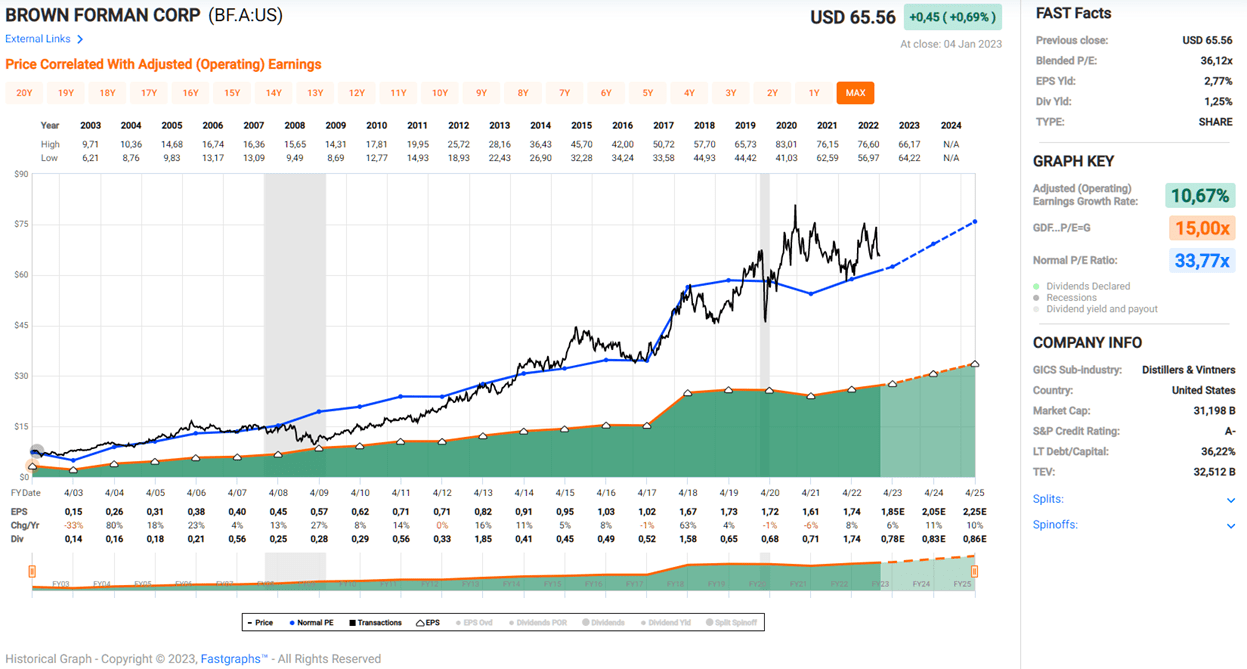

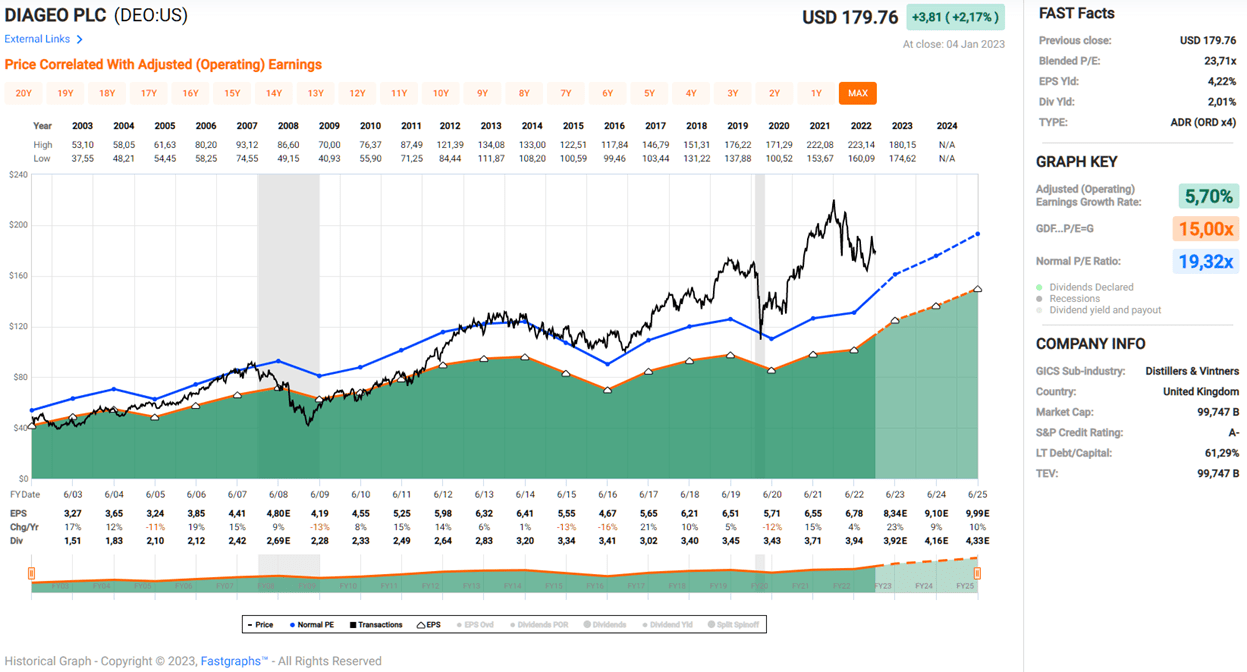

Interestingly, the historical valuations suggest that investors are willing to pay a higher price for Brown-Forman than for Diageo. Looking at the FAST Graphs charts of BF.A and DEO in Figure 13 and Figure 14, respectively, it is noticeable that Brown-Forman saw a significant - and in my opinion, unjustified - multiple expansion in recent years, and its current "normal" price-to-earnings ((P/E)) ratio is a whopping 34. Brown-Forman's current blended P/E ratio of 36 appears very aggressive indeed, and against this backdrop, Diageo, with a blended P/E ratio of 24 according to FAST Graphs appears much more palatable.

Figure 13: FAST Graphs plot of Brown-Forman [BF.A] (taken with permission from www.fastgraphs.com) Figure 14: FAST Graphs plot of Diageo [DEO] (taken with permission from www.fastgraphs.com)

{kind=link}

{kind=link}

Projecting the four-year average nFCF of the two companies into the future, and considering a 7% cost of equity to be appropriate, Diageo would need to grow its cash flow by 4% in perpetuity to justify its current share price of £36.5, while Brown-Forman would need to grow by 4.5% to justify a current share price of $64. Investor service firm Morningstar currently has a three-star rating for both companies and sees the fair value of Diageo and Brown-Forman at £35 and $73, respectively, with uncertainty rated as low and medium, respectively.

Based on my analysis, I conclude that Brown-Forman deserves a small valuation premium due to its more reliable earnings, more conservative balance sheet and stronger dividend history, but early signs of weakening profitability and its ownership structure cloud the picture somewhat. At the same time, Diageo has a brand portfolio that I believe is stronger, and its already solid presence in emerging Asia and Africa is well worth noting. However, it is likely that this exposure and the risks associated with it, as well as the weaker balance sheet and the fact that Diageo is a UK company (Brexit, etc.), will be a factor that is responsible for the valuation gap.

I do not want to be misunderstood here, I consider both excellent companies and in fact I do own a sizable position in Diageo since 2020. However, after taking a closer look at both companies, I would really like to also become a shareholder in Brown-Forman at some point, but the valuation and low dividend yield are aspects I cannot ignore. Brown-Forman is therefore high on my watch list, and I will wait patiently for the company's valuation to settle down to a reasonable level. However, it is hard to imagine that the stock price of such a great company could drop significantly unless there is a severe recession.

Thank you very much for taking the time to read my article. How did you like it, my style of presentation, the level of detail? If there is anything you'd like me to improve or expand upon in future articles, do let me know in the comments section below.

For further details see:

Diageo And Brown-Forman: Like Them Both But For Different Reasons