DHIL - Diamond Hill International Fund Q2 2023 Market Commentary

2023-08-23 11:10:00 ET

Summary

- Diamond Hill invests on behalf of clients through a shared commitment to its valuation-driven investment principles, long-term perspective, capacity discipline and client alignment.

- Our portfolio outpaced the MSCI ACWI ex USA Index in Q2 due largely to strength in our holdings in Sweden, Poland and Mexico, as they handily outpaced benchmark peers.

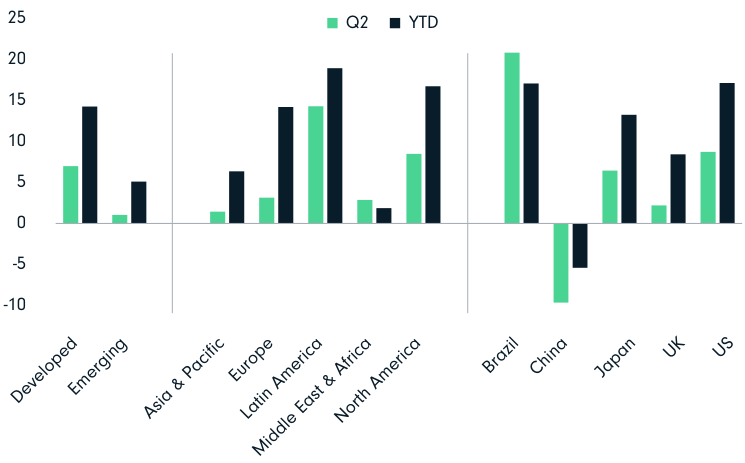

- Global stocks rose over 6% in Q2 2023, bringing YTD gains to roughly 14%, with developed markets outperforming emerging markets.

- Latin American stocks led the way in Q2, while China's market declined.

- Global technology stocks, industrials, and financials were the top-performing sectors, while communication services and real estate declined.

Market Commentary

Markets were broadly positive in Q2 2023, with global stocks rising over 6% (as measured by the MSCI ACWI Index), bringing YTD gains to roughly 14%. US dollar-based returns were marginally lower than local returns as the USD strengthened slightly during the quarter relative to major global currencies. Developed markets handily outpaced emerging markets in Q2, rising 7% versus 1%, respectively, and bringing YTD totals to +15% versus +5%, respectively.

Latin American stocks led the way in Q2, up over 14%, tied to sharp bounces in Brazil (up nearly 21%), Peru (up over 13%) and Colombia (up more than 12%). Having started rate hikes — and therefore, largely tamed inflation — before much of the developed world, there is broad anticipation the region’s central banks are on the cusp of an easing cycle, boosting sentiment. In Europe, Poland (+25%), Hungary (+25%) and Greece (+24%) had particularly positive quarters, while the larger economies — Germany (+4%), France (+4%), the UK (+2%) — experienced more moderate gains as inflation remains a concern and the European Central Bank has signaled it is not yet done raising rates. In the Asia Pacific region, China’s market declined (-9%) as the anticipated economic bounce following its full economic reopening has yet to fully materialize. However, India (+12%), Japan (+6%), Taiwan (+5%) and Korea (+5%) were in the black in Q2.

From a sector perspective, global technology stocks in the MSCI ACWI ex USA Index notched another quarter at the top (rising nearly 7%), followed by industrials (+6%) and financials (+5%). Reversing some of its YTD gains, the communication services sector declined (-4%), as did real estate (-2%) amid an overall rising global interest rates environment. Materials declined a relatively modest -1%.

The macro picture has also been consistent in 2023, with inflation, central bank policy and ongoing geopolitical tensions dominating headlines. In June, UBS completed its acquisition of embattled Swiss-based Credit Suisse (a bank with over 170 years of history), closing the largest bank deal since the 2008 financial crisis. While we remain vigilant in assessing the fundamental health of all our portfolio holdings, we believe the worst is behind us on this front for the time being.

While the US is seemingly nearing the finale of its tightening campaign, global monetary policy is a more mixed bag. The UK faces ongoing stubborn inflation, seemingly decreasing the likelihood it is as close to the end of its hiking cycle as the US may be. Similarly, the European Central Bank likely has a way to go as inflation has proven sticky in major economies like Germany’s. In contrast, many emerging markets economies seem on the cusp of considering pausing rate hikes, if not beginning to cut. For example, Hungary trimmed rates (which remain high) during the quarter as it struggles to rein in inflation while not hampering too much economic activity. A notable exception is Turkey, which significantly raised rates (650 bps) following President Erdogan’s May reelection — presumably in a bid to convince markets the country will begin seriously addressing its economic challenges. Whether investors find the effort credible naturally remains to be seen.

With everything going on in the macro background, we believe now is a great time to invest abroad. This is not because macro uncertainty is abating; on the contrary, it’s because of the uncertainty and negative headlines that selective, bottom-up investors can find opportunities. There has been disappointment over China’s reopening, political turmoil in Peru and Brazil, pseudo-campaigning in Mexico and India ahead of elections, an ongoing war in Russia, and continued tensions between China and the US. But this is par for the course in international markets — uncertainty is constant. It’s in environments such as these that we find some of the most attractive long-term investment ideas. It’s also why we believe owning a carefully curated portfolio of companies — rather than a benchmark — is critical to longterm success in non-US markets. What is the point of owning an international index that includes so many mediocre companies if macro concerns keep you up at night? Our approach is to be selective and own only those businesses we believe offer the greatest potential for long-term growth.

Exhibit 1 - Q2 2023 Total Returns for Major Markets ((USD)) (%)

{kind=link}

Performance Discussion

Our portfolio outpaced the MSCI ACWI ex USA Index in Q2 due largely to strength in our holdings in Sweden, Poland and Mexico, as they handily outpaced benchmark peers. On the downside, our lone holding in Italy meaningfully underperformed the benchmark’s holdings. From a sector perspective, we benefited from the outperformance of our holdings in the consumer staples, communication services and health care sectors. Conversely, our financials holdings, while positive, trailed, thereby weighing on relative performance.

On an individual holdings’ basis, top contributors to return in Q2 included Spotify Technology ( SPOT ), FEMSA ( FMX , Fomento Economico Mexicano) and Dino Polska ( DNOPY ). Sweden-based digital music services provider Spotify continues adding new users despite having materially pulled back on customer acquisition spending over the last several months — a decision which is allowing profits to flow through to investors and providing a boost to investor sentiment on the company’s long-term economics. Though the valuation has increased, we continue to see compelling upside potential over time if the company continues executing on its user growth and profitability ambitions.

Mexican multinational beverage retail company FEMSA has fully liquidated its long-term financial stake in Heineken, allowing the company to fully monetize the holding and reflect it in the company’s valuation. We are monitoring to see whether the company will return some portion of the Heineken stake to owners via dividends or a share buyback.

Polish supermarkets operator Dino Polska has executed well and maintained its price discipline amid a highly inflationary Polish environment. As consumers trade down from more expensive retailers to discounters — which Dino effectively is — the company is taking market share from competitors. It is also benefiting from slightly elevated demand given the high number of Ukrainian refugees who have fled to Poland. Meanwhile, management has wisely chosen to temporarily pull back on new store growth to avoid undue balance-sheet strain in the higher-cost environment. Though the valuation has risen, we continue to see upside as the macroeconomic and inflationary environments normalize and the company is able to resume new store growth.

Other top Q2 contributors included Fairfax Financial Holdings ( FRFHF ) and Nintendo ( NTDOY ). Fairfax is a Canada-based global property and casualty insurer and reinsurer. As the company continues improving its underwriting, profitability has likewise improved, as has book value per share. Japanese video game developer Nintendo has benefited from a better-than-expected sales cycle for its Switch gaming console, contributing to positive operating profits in Q2. Its Super Mario Brothers movie was also a box office hit, setting several all-time records and providing a boost to the brand’s value and customer acquisition potential.

Among our bottom contributors in Q2 were Italian financial services company doValue ( DOVXF ) and Chinese e-commerce giants Tencent ( TCEHY ) and Alibaba ( BABA ). Shares of doValue were pressured as results in Q2 disappointed investors, as did its pipeline of new mandates. Further, the company’s CEO departed in the quarter. However, we maintain our long-term conviction in doValue given it is an independent, capital-light credit servicer with little balance sheet risk and is operating in some of the most attractive markets in Southern Europe (Italy, Spain, Greece, Cyprus, Portugal).

Chinese multinational technology and entertainment company Tencent and Chinese e-commerce platform Alibaba declined in the quarter as China’s economic reopening since its lifting of its zero-COVID policy at the start of 2023 has proved disappointing. Chinese consumers have yet to normalize their spending patterns, weighing on consumer-related companies like Tencent and Alibaba accordingly. However, we anticipate this will prove a near-term headwind and maintain our conviction in both companies.

Other bottom contributors included Swatch Group ( SWGAY ) and Ashmore Group (ajmpf). Swatch Group, based in Switzerland, is a dominant player in the watch industry with a broad portfolio of global brands and a vertically integrated business model whereby it supplies movements and key watch components for competitors. Shares were pressured in Q2 given the company’s significant exposure to Chinese consumers, who failed to resume normal spending despite China’s full economic reopening. Ashmore Group is a well-run, UK-based emerging markets debt manager. While we like the company’s exposure to an asset class we think is relatively insulated from the trend to passive investing, shares were pressured in Q2 as sentiment on the asset class abated given growing uncertainty around emerging markets’ economic recoveries and the possibility that the US rate-hike cycle has reached its peak.

Portfolio Activity

We initiated four new positions in Q2, including Epiroc ( EPOKY ), Ferguson ( FERG ), First Quantum Minerals ( FQVLF ) and Capstone Copper ( CSCCF ).

Epiroc is a high-quality Swedish mining equipment/service company that was spun out of Atlas Copco in 2018. The company has strong competitive positions in surface and underground drilling, and a significant share of its sales are derived from high-margin aftermarket services, adding stability to a business operating in a cyclical industry. The company is diversified in terms of metals, geographies and customers. Further, its key segments operate in largely a duopoly with another Swedish firm, so the industry tends to be rational. We believe we were able to buy a well managed company that has a long tailwind of opportunities ahead of it and operates its business with a long-term view at a reasonable price.

Headquartered in the UK, Ferguson is a leading distributor of plumbing, waterworks, HVAC and related products in North America. In an industry where scale is key, Ferguson is a high-quality market leader, which has resulted in a virtuous cycle of share gains and margin expansion that remains in its early innings given a still-fragmented industry. Further, we believe any concerns about a softening macroeconomic environment and its potential impacts on Ferguson are largely reflected in the share price, giving us an attractive entry point.

First Quantum is a Canada-listed copper mining company operating primarily in Panama and Zambia. The business has an excellent track record of operating low-cost mines and building and developing mines in challenging parts of the world. Similarly, Capstone Copper is a Canada-listed copper mining company operating primarily in Chile, the US and Mexico. Capstone has a number of value-added projects and initiatives coming on line in the next 12 to 18 months — especially an expansion of its Mantoverde operation in Chile, which should materially lower operating costs and increase scale there. The CEO has been connected to Capstone’s core Chilean assets for a long time — including prior to Captsone’s ownership of them, which commenced over a decade ago — and believe he will make appropriate long-term decisions in stewarding the assets.

Relevant to both companies, we anticipate meaningful long-term supply challenges in copper in the period ahead, given its heavy and varied use in alternative energy sources. Further, there has been a recent trend toward consolidation and M&A in the copper industry, and we believe both First Quantum and Capstone Copper could present attractive acquisition candidates for large mining companies seeking to increase their copper exposure. We capitalized on an opportunity to take a longer-term view and initiate positions in both companies at discount to our estimates of intrinsic value.

We funded these additions in part the proceeds from the sales of our positions in Spanish bank Banco Bilbao Vizcaya Argentaria and global entertainment company Walt Disney Company. We also exited our position in global consumer health care products company Haleon, which was spun out of GSK in 2022 and had reached our estimate of intrinsic value.

Market Outlook

Given equity markets’ positive returns in Q2 and 2023 to date, market participants have seemingly moved past the recent bank failures; however, the full effects of these failures have not yet been felt. For example, if banks pull back on lending to improve their capital positions, it could negatively impact economic growth. Balancing the potential economic impact of higher interest rates with still-elevated inflation levels continues to complicate global central banks’ monetary policy decision-making process.

We expect continued uncertainty and volatility across markets as global economies strive to tame inflation and promote economic progress. As we mentioned, uncertainty creates opportunities, and we are actively searching for opportunities around the globe that can be capitalized upon when the price and time are right. In fact, our team has traveled to Japan, India, Mexico, France, the UK and the Nordics this year to research several businesses. As with any research trip, our objectives are clear. First, we want to identify new businesses that might have a place in the portfolio one day. Secondly, we wish to refine our intrinsic value estimates based on what we learn. Lastly, we want to eliminate companies or management teams that we don’t want to invest in. As always, our primary focus is on achieving value-added results for our existing clients, and we believe we can achieve better-than-market returns over the next five years and beyond through active portfolio management.

| Period and Annualized Total Returns (%) |

| Since Inception (30 Dec 2016) |

| 5Y |

| 3Y |

| 1Y |

| YTD |

| 2Q23 |

| Expense Ratio (%) |

| Class I ( DHIIX ) |

| 8.56 |

| 5.67 |

| 12.09 |

| 17.55 |

| 13.58 |

| 3.84 |

| 0.86 |

| MSCI ACWI ex USA Index |

| 5.94 |

| 3.52 |

| 7.22 |

| 12.72 |

| 9.47 |

| 2.44 |

| — |

| Click here for holdings as of 30 June 2023. Risk disclosure: International investments involve special risks, including currency fluctuation, lower liquidity, different accounting methods, tax policies, political systems and higher transaction costs. These risks are typically greater in emerging markets. Small- and mid-capitalization issues tend to be more volatile and less liquid than large-capitalization issues. The views expressed are those of Diamond Hill as of 30 June 2023 and are subject to change without notice. These opinions are not intended to be a forecast of future events, a guarantee of future results or investment advice. Investing involves risk, including the possible loss of principal. Past performance is not indicative of future results. Investment returns and principal values will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The Fund’s current performance may be lower or higher than the performance quoted. For current to most recent month end performance, visit Diamond Hill. Performance assumes reinvestment of all distributions. Returns for periods less than one year are not annualized. The quoted performance for the Fund reflects the past performance of Diamond Hill International Fund L.P. (the “International Partnership”), a private fund managed with full investment authority by the fund’s Adviser. The Fund is managed in all material respects in a manner equivalent to the management of the predecessor unregistered fund. The performance of the International Partnership has been restated to reflect the net expenses and maximum applicable sales charge of the fund for its initial years of investment operations. The International Partnership was not registered under the Investment Company Act of 1940 and therefore was not subject to certain investment restrictions imposed by the 1940 Act. If the International Partnership had been registered under the 1940 Act, its performance may have been adversely affected. Performance is measured from 30 December 2016, the inception of the International Partnership and is not the performance of the fund. The assets of the International Partnership were converted, based on their value on 28 June 2019, into assets of the fund. The International Partnership’s past performance is not necessarily an indication of how the fund will perform in the future either before or after taxes. Fund holdings subject to change without notice. Index data source: MSCI, Inc. See Diamond Hill - Disclosures for a full copy of the disclaimer. Securities referenced may not be representative of all portfolio holdings. Contribution to return is not indicative of whether an investment was or will be profitable. To obtain contribution calculation methodology and a complete list of every holding’s contribution to return during the period, contact 855.255.8955 or info@diamond-hill.com. Carefully consider the Fund’s investment objectives, risks and expenses. This and other important information are contained in the Fund’s prospectus and summary prospectus, which are available at Diamond Hill or calling 888.226.5595. Read carefully before investing. The Diamond Hill Funds are distributed by Foreside Financial Services, LLC (Member FINRA). Diamond Hill Capital Management, Inc., a registered investment adviser, serves as Investment Adviser to the Diamond Hill Funds and is paid a fee for its services. Not FDIC insured | No bank guarantee | May lose value |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Diamond Hill International Fund Q2 2023 Market Commentary