DIAX - DIAX: Not A Great Volatility Reduction Play

2023-11-12 20:23:37 ET

Summary

- Nuveen Dow 30 Dynamic Overwrite Fund aims to provide attractive total returns with less volatility than the Dow Jones Industrial Average.

- DIAX has delivered below market returns historically but has failed to deliver below market volatility.

- The Fund trades at a significant discount to NAV, but the dynamic nature of options exposure makes it a difficult arbitrage play.

- Investors should consider a diversified risk mitigation strategy including tail hedging, reduced equity exposure, and lower beta equity exposure as alternatives to DIAX.

Closed-End Fund Overview

The Nuveen Dow 30 Dynamic Overwrite Fund ( DIAX ) seeks to offer regular distributions through a strategy that seeks to provide attractive total returns with less volatility than the Dow Jones Industrial Average.

DIAX invests in an equity portfolio that seeks to replicate the price movements of the DJIA as well as selling call options on 35-75% of the notional value of the fund's equity portfolios (with a 55% long-term target).

DIAX currently has ~$550 million of net assets and has a total annual expense ratio of 0.93%. Fund characteristics include 0% effective leverage, a market distribution rate of 8.66%, and a NAV distribution rate of 7.5%.

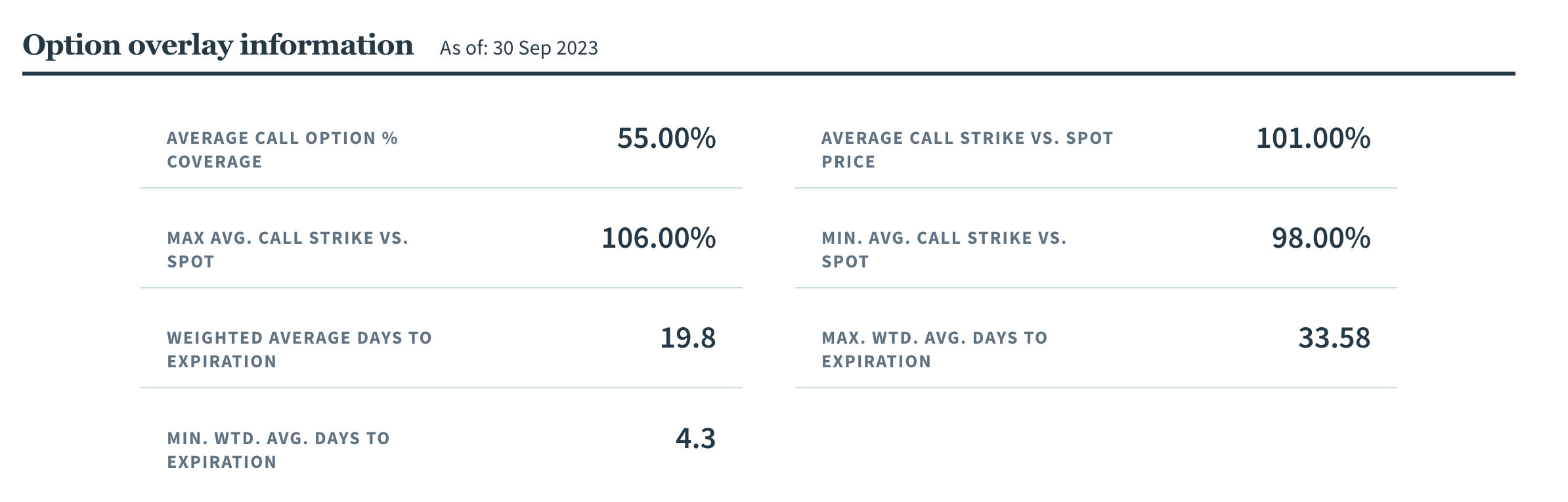

Option Overlay Information

DIAX's option overlay is dynamically managed and not consistent over time. However, the table below shows how the fund's overlay positioning as of Sep 30, 2023.

DIAX currently has call options written on 55% of its exposure which is in line with the fund's long-term target. The average call strike vs. spot price is currently 101%. However, over the past month, the average call strike vs. spot has ranged from 98% to 106%. This suggests there is a fair amount of variability in regards to the actual net long equity exposure at any given time.

{kind=link}

High Management Fee

DIAX has a very high expense ratio of 0.93%. To put that into context, the average expense ratio for an actively managed equity mutual fund is ~0.66% and the average equity ETF expense ratio is ~0.16%. Comparably, a somewhat similar product, the Global X Dow 30 Covered Call ETF ( DJIA ) charges a total expense ratio of 0.60% while the S&P 500 Collar 95-110 ETF ( XCLR ) charges a net expense ratio of just 0.25%.

Historical Performance

DIAX launched in April 2005 and has significantly underperformed the Dow Jones Industrial Average since then. Since inception, DIAX has delivered a total return of 191.4% compared to 411.1% delivered by the SPDR Dow Jones Industrial Average ETF ( DIA ) which can be used as a proxy for the index.

While DIAX has delivered a significantly lower total return, it has only delivered higher realized volatility compared to DIA. Since inception, DIAX has realized an average 30-day volatility of 16.71% compared to 15.24% realized by DIA over the same period. The reason for this is that DIAX has experienced significant volatility related to the level of discount to NAV.

The result is that DIAX has delivered significantly worse risk-adjusted performance than DIA. As shown by the chart below, DIAX has realized an average trailing 5-year Sharpe ratio of 0.62 compared to 0.94 for DIA.

DIAX has also performed poorly vs newer options risk reduction products such as DJIA and XCLR (though the return history is fairly short given that these products recently launched.)

Discount to NAV

DIAX is currently trading at a 13.3% discount to its NAV. This represents a significant discount on an absolute basis and on a relative basis to DIAX's historical norm.

Over the past 10 years, DIAX has traded at an average discount to NAV of 5.82%. However, closed-end funds are generally trading at above-average discounts to NAV currently. According to BlackRock, the median closed-end fund is now trading at a discount of 10.7% compared to a 5-year median discount of 7.4%.

Given the relatively liquid nature of DIAX's holdings, it is surprising that the fund trades at such a high discount. However, DIAX is not an easy fund to implement an arbitrage strategy with as the strikes of the covered calls are dynamic and adjusted by the fund managers regularly. As previously discussed the average call strike for DIAX has varied from 98% of spot to 106% of spot over the past months. For this reason, I am not convinced that the discount will narrow in the immediate future as DIAX poses challenges for arbitrageurs.

Alternative Volatility Reduction Techniques To Consider

DIAX is a reasonably well-thought-out closed-end fund that tries to reduce downside risk for investors while allowing for upside participation.

DIAX has proved an inefficient way to reduce volatility as fundholders have experienced additional volatility related to changes in discounts to NAV which has offset the reduction in volatility due to covered call selling.

While DIAX is currently trading at a significant discount to NAV, I am not sure this discount will close anytime soon as the dynamic nature of the covered call exposure and strike level poses challenges for arbitrageurs.

As of this writing, DIAX has underperformed DIA by 219.7% since inception. Simply put, that is a lot of return to give up in order to mitigate risk.

Risk mitigation is generally a good idea and, in my opinion, investors should consider a combination of options including some of the below:

Tail hedging: investors can allocate a small percentage of their portfolio (generally 0-1.5% each year to purchasing deep out-of-the-money put options.) This strategy does an excellent job of protecting the portfolio in the event of a fast market crash .

Reduced equity exposure in favor of other assets: a simple approach to reduce equity risk in the portfolio is simply to reduce the percentage allocated to equities while increasing allocations to other assets such as bonds or gold.

Focus on defensive equities: this approach involves selecting individual securities or ETFs that target lower-risk areas of the market. Typical examples include utility, healthcare, and consumer staple stocks. While these sectors may experience downside in a market sell-off they tend to go down less. I recently highlighted a few favorite defensive blue chip equities and defensive ETFs here:

USMV: A Solid ETF For Volatility Reduction

H&R Block: A Defensive Blue Chip Buy

Elevance Health: A High Conviction Blue Chip Buy

Conclusion

DIAX has failed to deliver on its objectives over the long term resulting in significantly worse risk-adjusted returns than the Dow Jones Industrial Average Index.

DIAX trades at a significant discount to NAV but there is no immediate catalyst to suggest this will narrow anytime soon. Moreover, the dynamic nature of covered call positioning makes it challenging for investors to implement an arbitrage strategy.

As an alternative to DIAX, investors looking to reduce volatility should consider a small allocation to tail hedging, reducing the overall level of equity risk in the portfolio, and focusing on more defensive segments of the stock market.

For further details see:

DIAX: Not A Great Volatility Reduction Play