INGEF - Different World Same Problems

2023-10-15 09:00:00 ET

Summary

- U.S. equity markets remained turbulent while benchmark interest rates retreated as investors weighed shocking geopolitical developments in the Middle East against inflation data showing an energy-driven reacceleration in price pressures.

- Posting a second week of modest gains following a four-week skid, the S&P 500 advanced 0.5%, but gains remained "top-heavy." The Mid-Cap 400 and Small-Cap 600 each posted weekly declines.

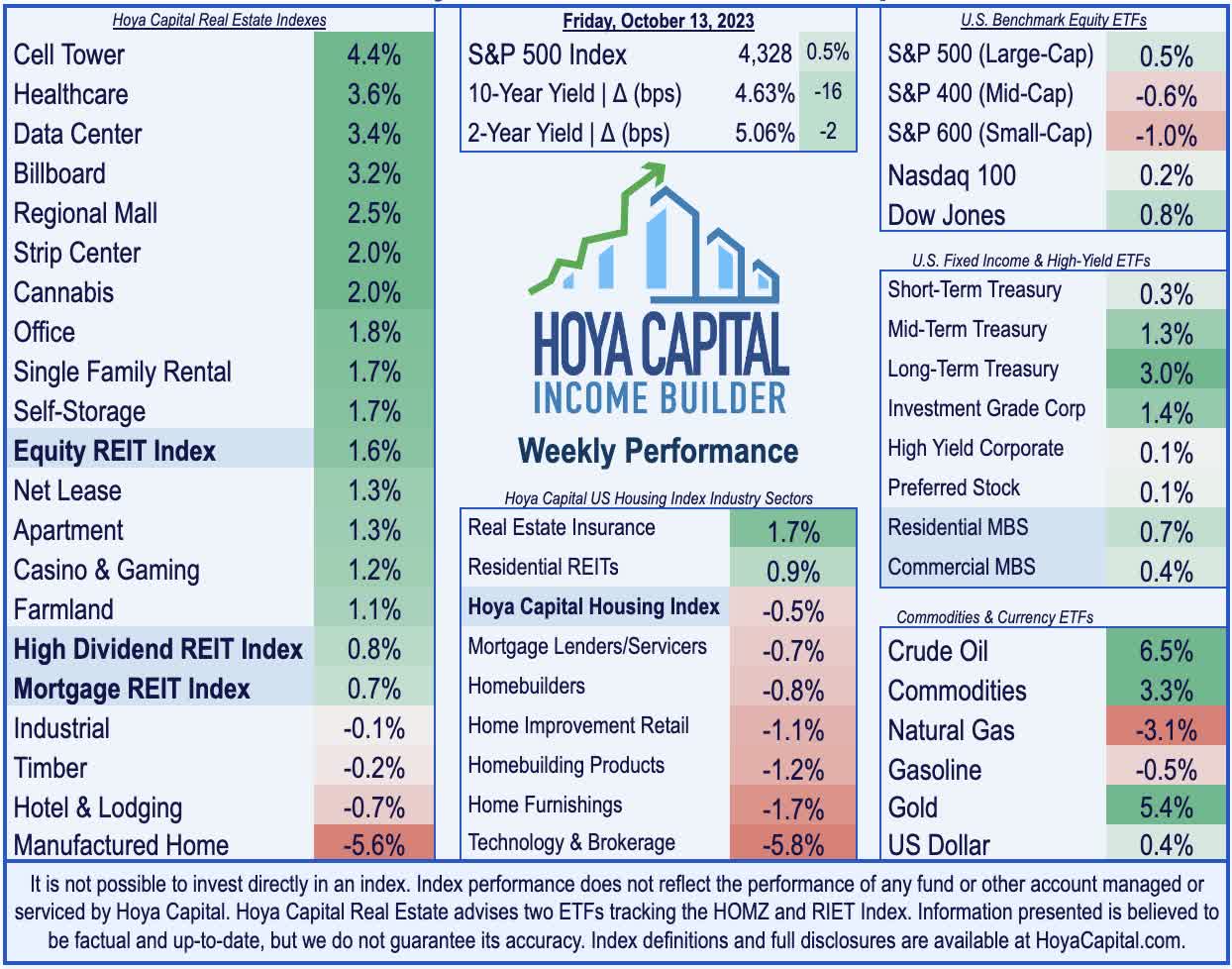

- Yield-sensitive segments rebounded this week as benchmark interest rates retreated from multi-decade highs. Ahead of the start of earnings season next week, the Equity REIT Index advanced 1.6%.

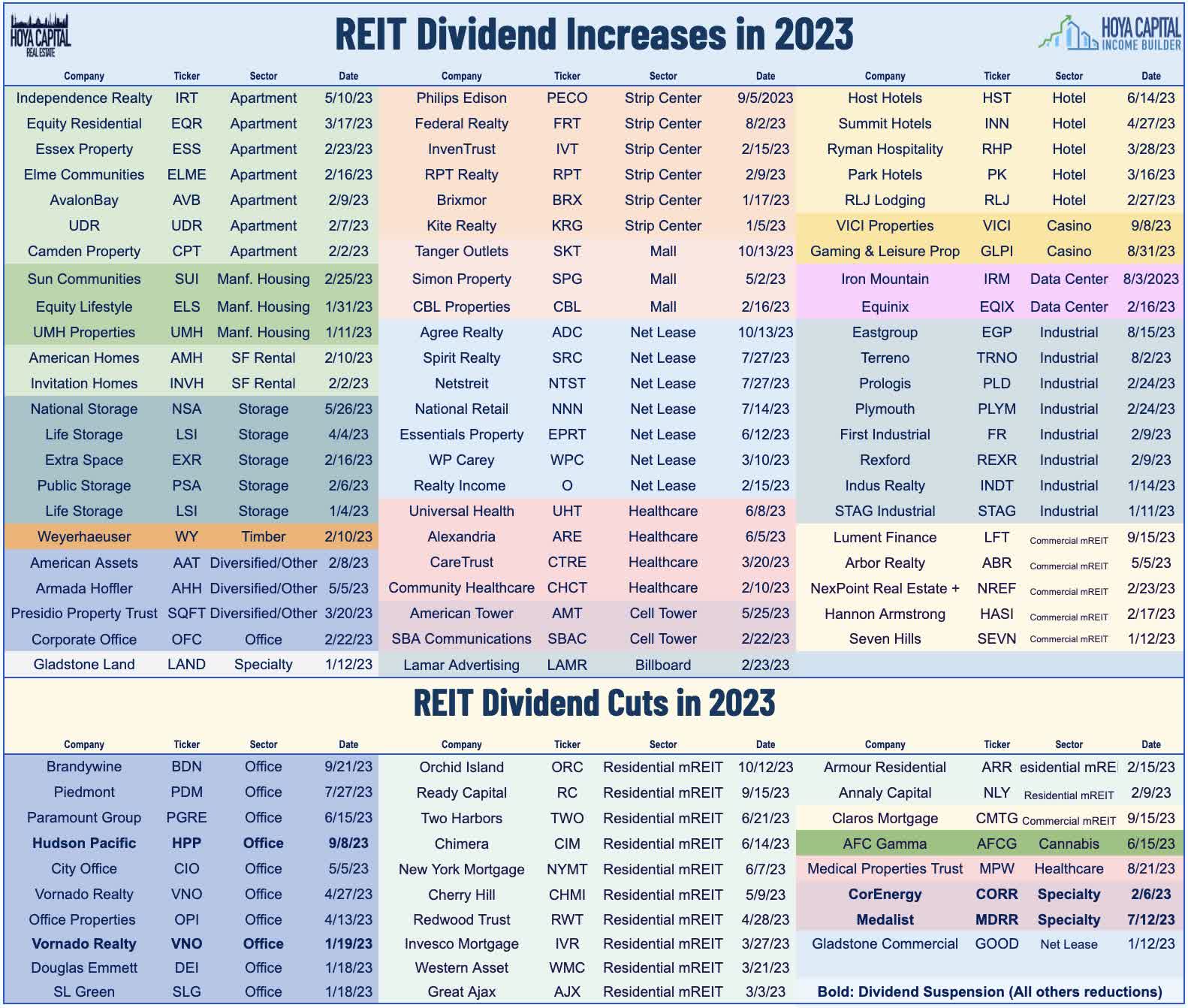

- A pair of REITs raised their dividends for the second time this year: Agree Realty and Tanger Factory Outlet. We've seen 68 REITs raise their dividend this year, while 28 REITs have lowered their payouts, including a reduction from Orchid Island this week.

- The closely-watched CPI and PPI inflation reports showed a disappointing reacceleration of inflationary pressures driven by a resurgence in oil prices. "Super Core" inflation, however, moderated to 2.5-year lows.

Real Estate Weekly Outlook

U.S. equity markets remained turbulent this week while benchmark interest rates retreated from multi-decade highs as investors weighed shocking geopolitical developments in the Middle East against a mixed slate of inflation data showing an energy-driven reacceleration in price pressures. Deadly terrorist attacks on Israel over the weekend 'flipped the script' for financial markets - at least temporarily - and changed the tune of some Fed officials, who expressed a noticeably less hawkish tone this week. Market-implied probabilities of another Federal Reserve interest rate declined back below 30% - down from highs last week that approached 50%.

{kind=link}

Posting a second-straight week of modest gains following a four-week skid, the S&P 500 advanced 0.5% this week, but gains this week were notably "top-heavy," consistent with the theme throughout the year. The Mid-Cap 400 declined 0.6% on the week, while the Small-Cap 600 posted declines of 1.0%. Yield-sensitive segments of the equity market rebounded this week as benchmark interest rates backed off from multi-decade highs. The Equity REIT Index advanced 1.6% on the week, with 14-of-18 property sectors in positive territory, while the Mortgage REIT Index advanced 0.7%. Homebuilders remained under pressure this week, however, after Freddie Mac data showed that 30-year mortgage rates climbed to the highest since December 2000 this week despite the retreat in benchmark rates.

{kind=link}

'Risk-off' was a theme across financial markets this week as tensions in the Middle East appeared likely to intensify further in the coming weeks - and potentially drag other nations into the conflict - following the terrorist attacks on Israel last weekend. Echoing the commentary earlier in the week from Fed officials Jefferson and Logan, Atlanta Fed President Bostic and Fed Governor Waller each described a "wait and see" approach before taking further actions on rate hikes. This softer commentary came alongside the release of minutes from the September FOMC meeting, which showed that "a majority of participants" judged that "one more increase" in the target federal funds rate at a future meeting would likely be appropriate. The 10-Year Treasury Yield dipped 16 basis points on the week to 4.63%, while the 2-Year Treasury Yield slipped 2 basis points on the week to 5.05%. Crude Oil ( USO ) prices surged over 6% this week, surging late in the week after Saudi Arabia paused diplomacy with Israel, potentially disrupting oil trade relations with Western allies. Gold ( GLD ) posted its strongest week since March, while the US Dollar ((USD)) extended its winning streak to a 13th-straight week.

{kind=link}

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

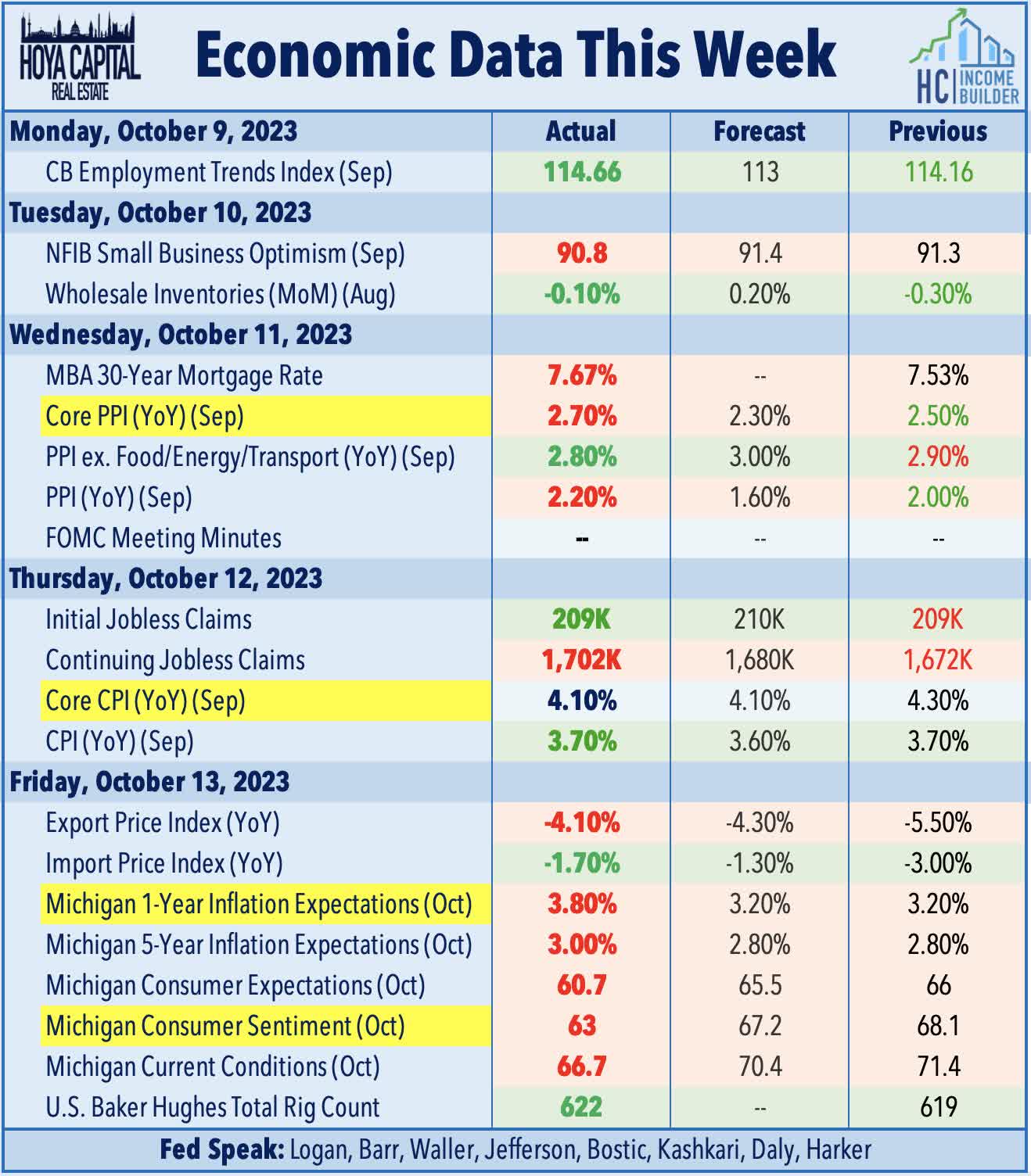

All eyes were on the Consumer Price Index report this week, which showed a disappointing reacceleration of inflationary pressures in September driven by a resurgence in oil prices - the key "swing" inflation input - along with sticky shelter inflation. Headline CPI increased 0.4% on the month and 3.7% from a year ago, which was slightly above consensus estimates of 0.3% and 3.6%. Core CPI - which excludes food and energy - increased 0.3% on the month and 4.1% on the year, both in line with expectations. The Shelter Index jumped 0.6% in September - the largest monthly jump since February - driven by a 4.2% reported jump in hotel room rates, which followed a 3.6% reported dip in the prior month - a result of the timing of Labor Day weekend. The CPI ex-Shelter Index - the metric we watch most closely - increased to 1.99% from last year, a third-straight sequential acceleration after dipping below 1% in June. The upward impact of Shelter on the broader CPI index has dissipated in recent months, however, as the 12-18 month lags in the index methodology are just now beginning to pick-up on the rent cooldown seen in late 2022.

{kind=link}

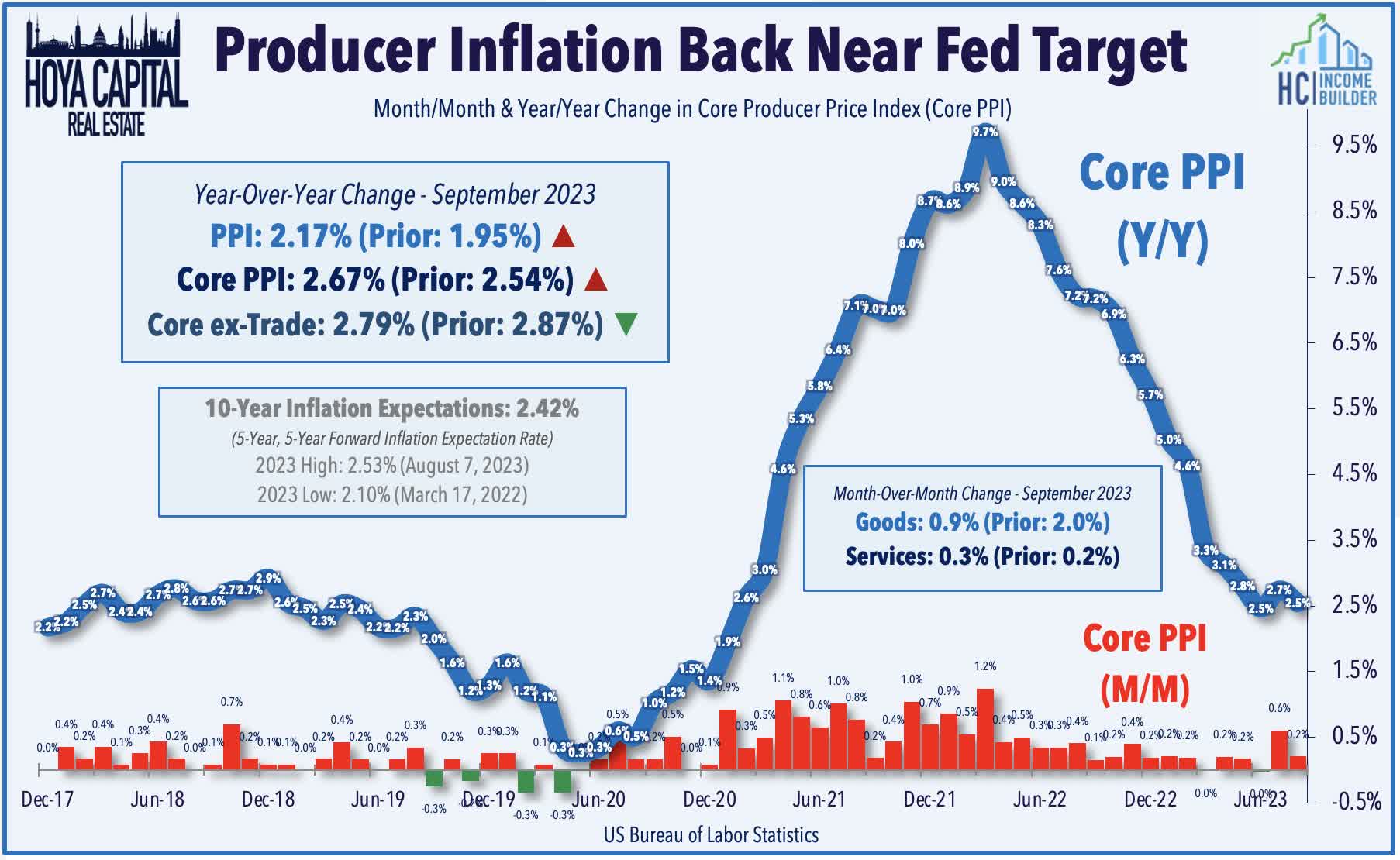

The so-called "Super Core" metric that is closely watched by the Fed - CPI Services ex-Rent Index - has remained on a more consistent disinflationary path, slowing to 2.8% in September - the lowest since March 2021. Earlier in the week, Producer Price Index data showed similarly mixed trends with an encouraging cooldown in services-related inflation offset by a resurgence in goods inflation. After hitting a low of just 0.3% in June, Headline PPI accelerated for a third-straight month, posting a 2.2% year-over-year increase in September. As with the CPI report, the jump in gasoline prices were responsible for the majority of this recent reacceleration, responsible for over 40% of the September increase in the PPI: Goods Index. Core PPI ex Trade - which is generally viewed as a better measure of 'sticky' inflationary pressures - was cooler than expected, posting a 2.8% increase in September, which matched the lowest since February 2021.

{kind=link}

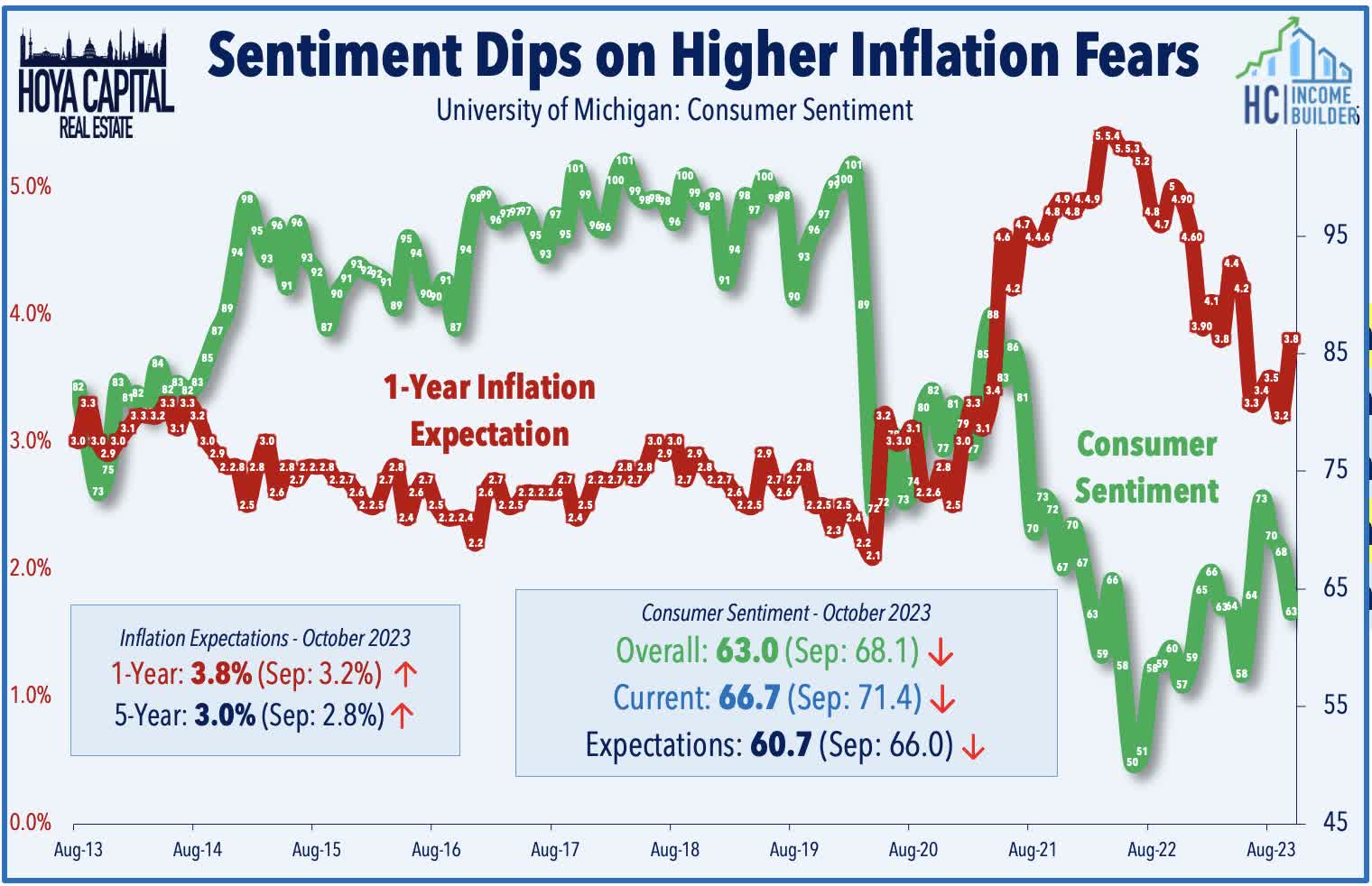

Survey data throughout the week showed a re-intensification of inflation concerns. The Michigan Survey of Consumers showed a sharp decline in consumer sentiment in the preliminary October reading, alongside a jump in consumer inflation expectations. Dipping to the lowest since May, Consumer Sentiment dipped to 63 in October from 68.1 last month. Both sub-indexes - Current Conditions and Expectations - fell by roughly 5 points. Consistent with the historical correlations, the jump in gasoline prices since June has weighed on consumer attitudes and brought a renewed focus on inflation. Americans’ expectations for inflation over the next year jumped to 3.8% in October from 3.2% in the prior month, the highest level since April. Three-year inflation expectations rose to 3% from 2.8% in September. NY Fed data showed similar trends, with one-year inflation expectations rising to 3.7% in September - up from 3.6% in August - while three-year inflation expectations rose to 3.0% - up from 2.8%. The same report showed that Americans have also become more concerned about their personal financial situation in recent months. The average perceived probability of missing a minimum debt payment over the next three months rose to 12.5%, the highest since May 2020. NFIB Small Business Optimism Index, meanwhile, dipped to the lowest since May.

{kind=link}

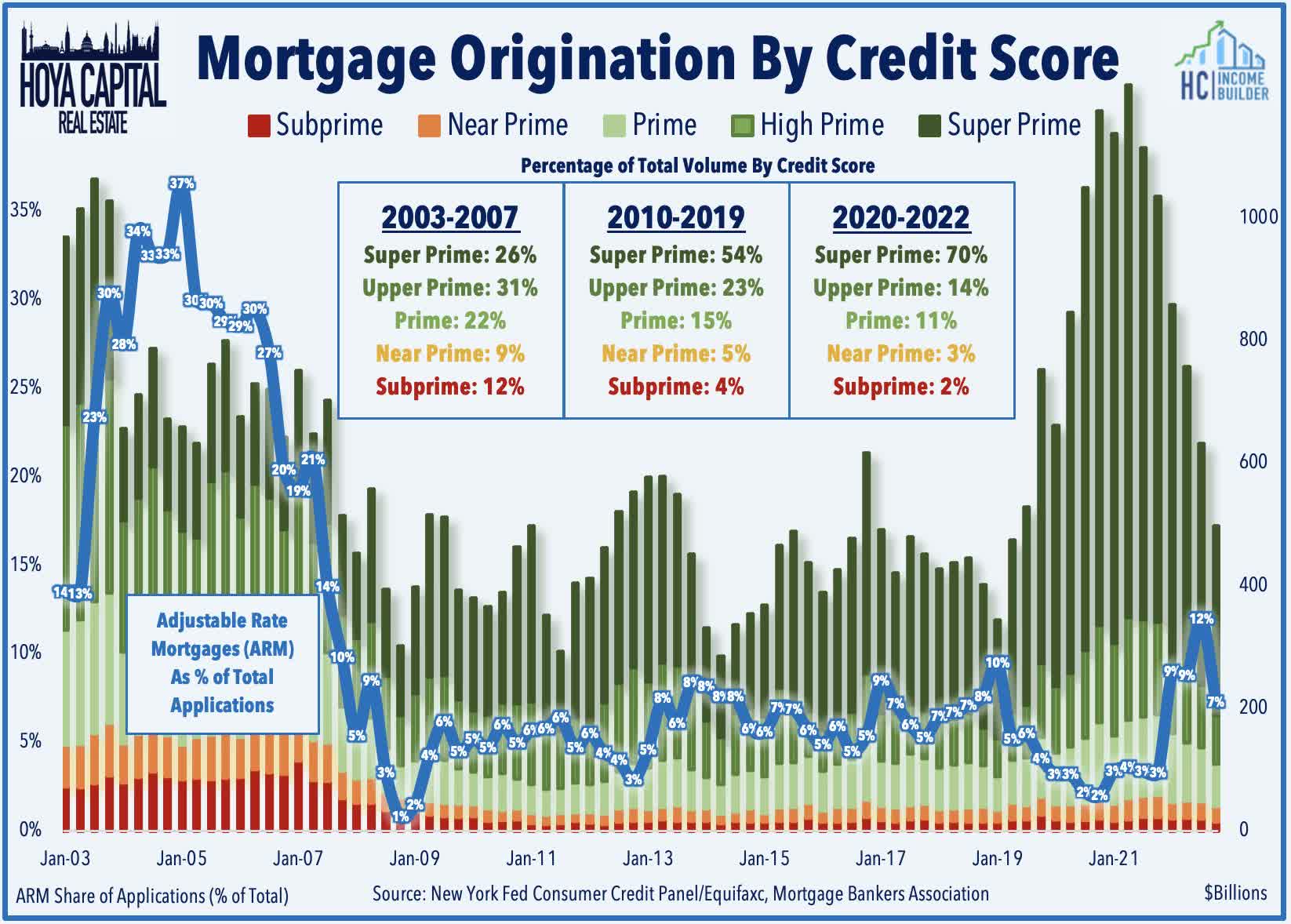

Also of note, the three major housing industry lobby groups - the NAR, MBA, and NAHB - called on the Fed to refrain from further rate increases, citing exacerbated housing affordability. After dipping to 27-year lows last week, mortgage applications rebounded 0.6% from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey. Compared to last year, purchase application volume is lower by 19% while refinance volume is off by 9%. Notably, the report also showed that the level of Adjustable Rate Mortgage ("ARM') applications increased by 15% over the week, bringing the ARM share up to 9.2% of all applications, the highest share since November 2022. Importantly, since 2010, only 5.8% of mortgage originations have been ARMs, compared to the 30% ARM share during the three years preceding the Great Financial Crisis.

{kind=link}

Equity REIT Week In Review

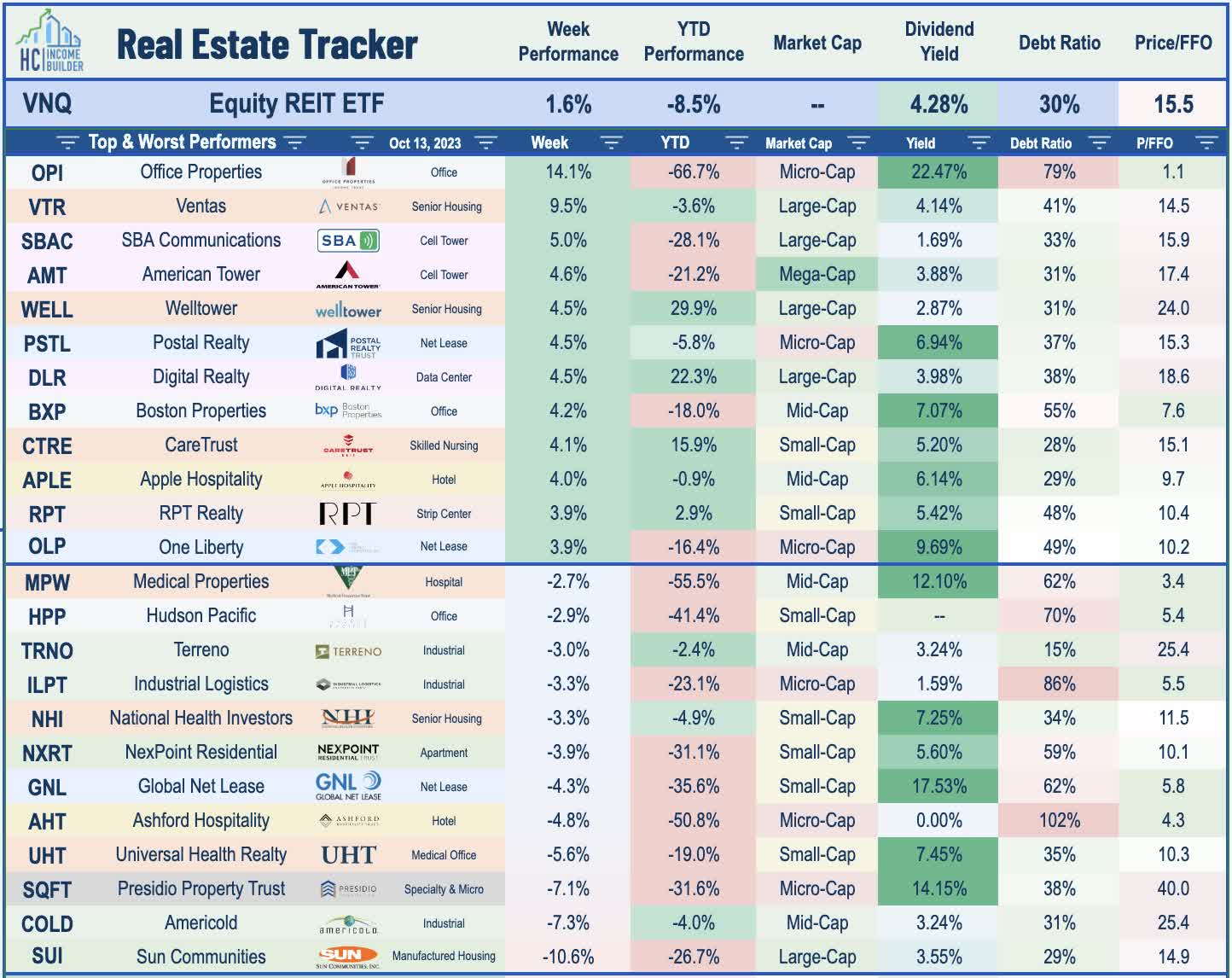

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

REIT earnings season kicks off next week with reports from seven REITs, kicking off on Monday afternoon with results from manufactured housing REIT Equity LifeStyle ( ELS ) reports on Monday. Three industrial REITs report next week: Prologis ( PLD ) reports on Tuesday, while Rexford ( REXR ) and First Industrial ( FR ) report on Wednesday. Office REIT SL Green ( SLG ) and cell tower REIT Crown Castle ( CCI ) also report on Wednesday. Net lease REIT Alpine Income ( PINE ) rounds out the week with results on Thursday. Ahead of the start of REIT earnings season next week, a pair of REITs raised their dividends for the second time this year. Agree Realty ( ADC ) gained 0.5% on the week after it raised its monthly dividend by 1.6% to $0.247/share (5.5% dividend yield). This year's second dividend hike for ADC, the new payout is 2.9% higher than its comparable rate last year. Also hiking for a second time this year, Tanger Factory Outlet ( SKT ) gained 2.5% after it raised its quarterly dividend by 6.1% to $0.26/share (4.5% dividend yield), which is roughly 18% above its comparable dividend a year earlier. We've now seen 68 REITs raise their dividend this year, while 28 REITs have lowered their payouts - nearly all of which have come from either the office or mortgage REIT sectors.

{kind=link}

Manufactured Housing : Sun Communities ( SUI ) dipped 10% this week after it announced that it would sell its 10% stake in Ingenia Communities Group ( OTC:INGEF ) - which owns and operates manufactured housing communities and holiday resorts in Australia. Sun expects the sale to generate a minimum net proceeds of US$100 million, and plans to use the proceeds to pay down variable rate debt - specifically, the variable rate sterling-denominated debt that funded its $1.3B acquisition of Park Holidays in the UK in 2021. Sun initially partnered with Ingenia in 2018 - paying $54M for this 10% stake - and just recently extended a separate joint partnership agreement for seven additional years. In our recent MH REIT report, we discussed how SUI's stumbles this year have been driven primarily by its ill-timed international expansion into the UK last year, which has proven to be a rare strategic blunder for one of the best-performing REITs of the prior decade. While only representing about 10% of its NOI, Sun whiffed badly on its forecasts for UK profitability and funded its acquisition with a floating-rate loan that has seen its reference interest rate more than double since the deal was announced.

{kind=link}

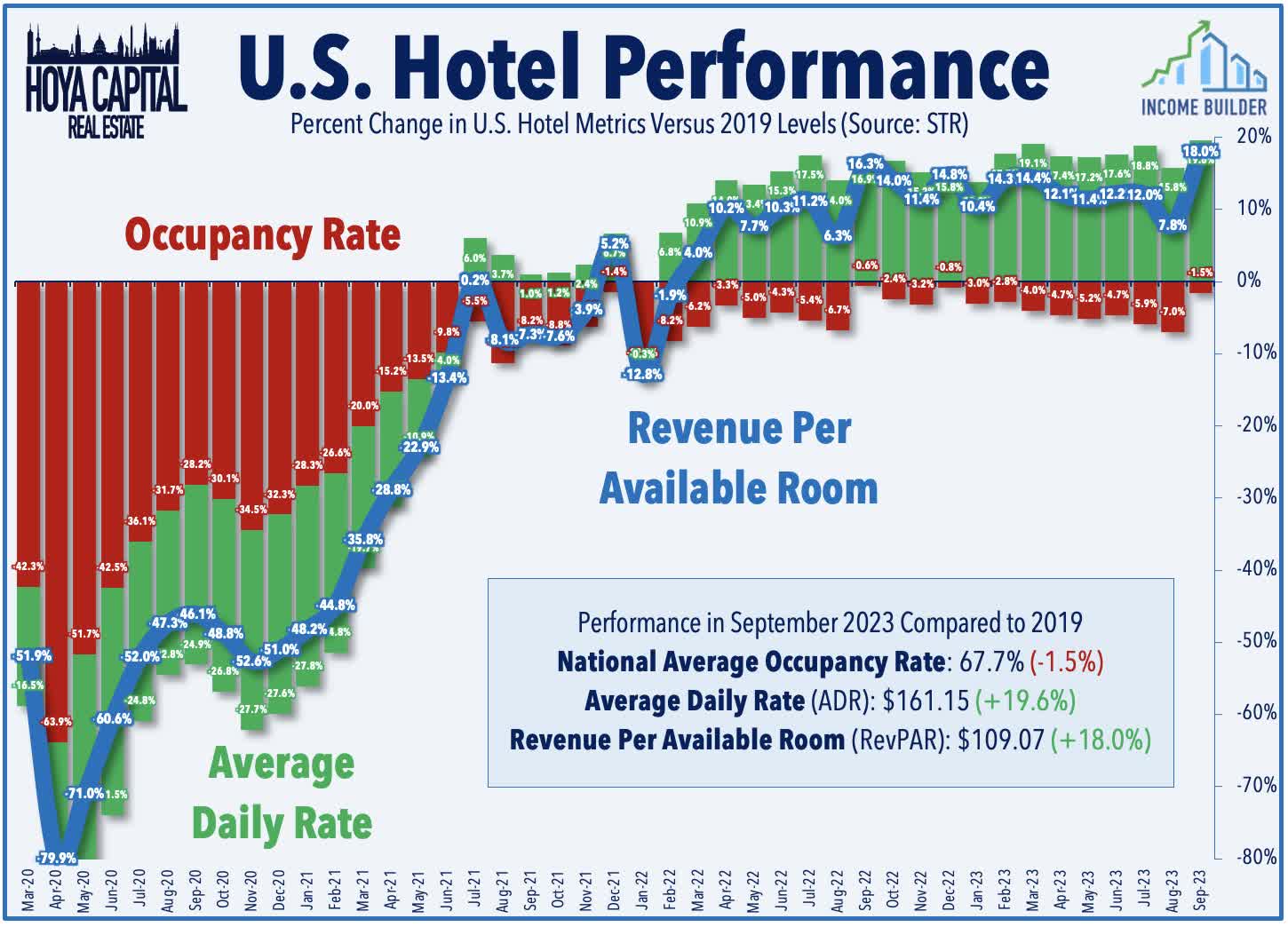

Hotel : Apple Hospitality ( APLE ) rallied 4% this week after it announced two hotel acquisitions in Salt Lake City totaling $91.5M and provided upbeat commentary ahead of third-quarter earnings season, noting “while overall industry transaction volume remains muted, the strength of our operating performance and our relative liquidity position have provided us with unique opportunities to pursue accretive acquisitions and to grow our portfolio.” APLE acquired a 175-room Courtyard by Marriott in Salt Lake City for $48.1M ($275k/key) and a neighboring 159-room Hyatt in Salt Lake City for $34.3M ($215k/key), along with an adjacent parking garage for $9.1M. Recent TSA Checkpoint data shows that domestic travel demand has downshifted slightly in recent weeks after a strong August and September. Throughput climbed to 104.1% of 2019-levels in September - the highest since the pandemic - but has averaged 102.5% thus far in October. Hotel data provider STR reports that industry-wide Revenue Per Available Room ("RevPAR") was roughly 12% above 2019 levels during the third quarter, as a roughly 18% relative increase in Average Daily Room Rates ("ADR") offset a roughly 5% relative drag in average occupancy rates.

{kind=link}

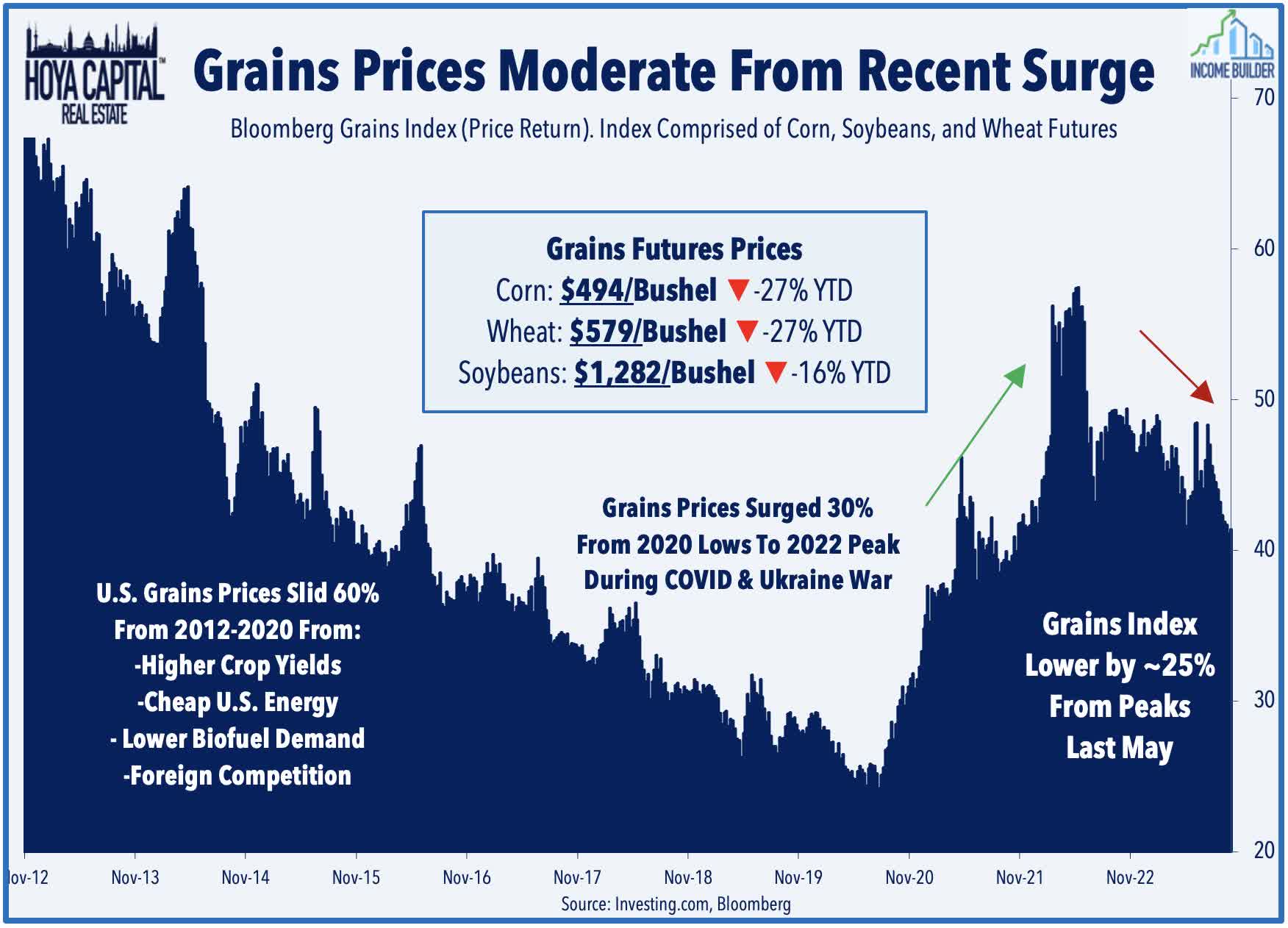

Farmland : Farmland Partners ( FPI ) gained 2% this week after it provided business updates on several topics. FPI announced that it finalized several transactions in Q3, including the sale of 13,500 acres in California, Colorado, Georgia, Illinois, Louisiana, and Kansas for $70M, representing a gain on sale of approximately 17%. FPI also noted that it purchased a 1,523-acre farm in Morehouse Parish, Louisiana for $11M. One of the hottest inflation-hedges last year, farmland REITs have been laggards this year amid a substantial pull-back in commodities prices from their peaks last May. FPI has been hit by a "triple-whammy" of headwinds: lower crop yield in early 2023 due to drought conditions, lower crop price due to normalization effects after a sharp spike early in the Ukraine-Russia war, and significantly higher interest rate expense due to FPI's elevated level of variable rate debt exposure. The Bloomberg Grains Index is about 25% below its recent peaks in mid-2022, with corn and wheat prices hit especially hard this year. The US Department of Agriculture reports that net farm income is expected to decrease by 25.4% relative to 2022 while farm production expenses are projected to increase by 3.3%.

{kind=link}

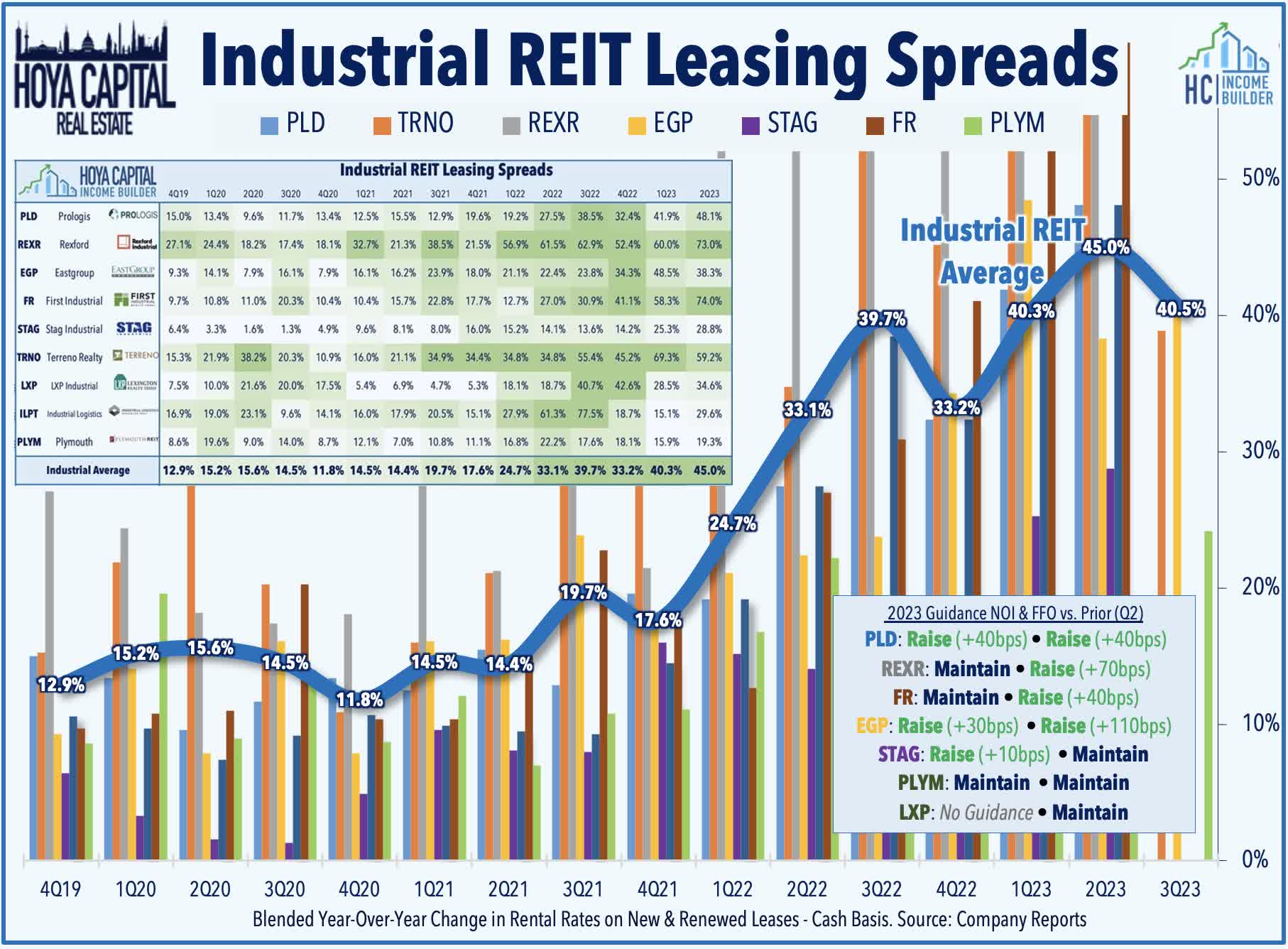

Industrial : Terreno ( TRNO ) was among the laggards this week after it provided preliminary third-quarter operating metrics. Among the highlights, TRNO noted that it achieved cash rent growth on new and renewed leases of 38.9% in Q3 across 500k square feet - a notable slowdown from the 59.2% increase on 800k SF achieved in Q2. Last quarter, industrial REITs warned of a moderation in the recent record-setting pace of rent increases due to increased supply levels and a post-pandemic normalization in demand. TRNO noted that its same-store portfolio was 98.5% leased at the end of Q3 - up slightly from last quarter and above the 98.1% occupancy rate last year. TRNO reported that it has acquired five properties this year for an aggregate purchase price of $410.8M, which secondary equity offerings have funded. TRNO has raised $516M in new equity this year through its secondary offering in February and it's at-the-market program at an average price of $62.23.

{kind=link}

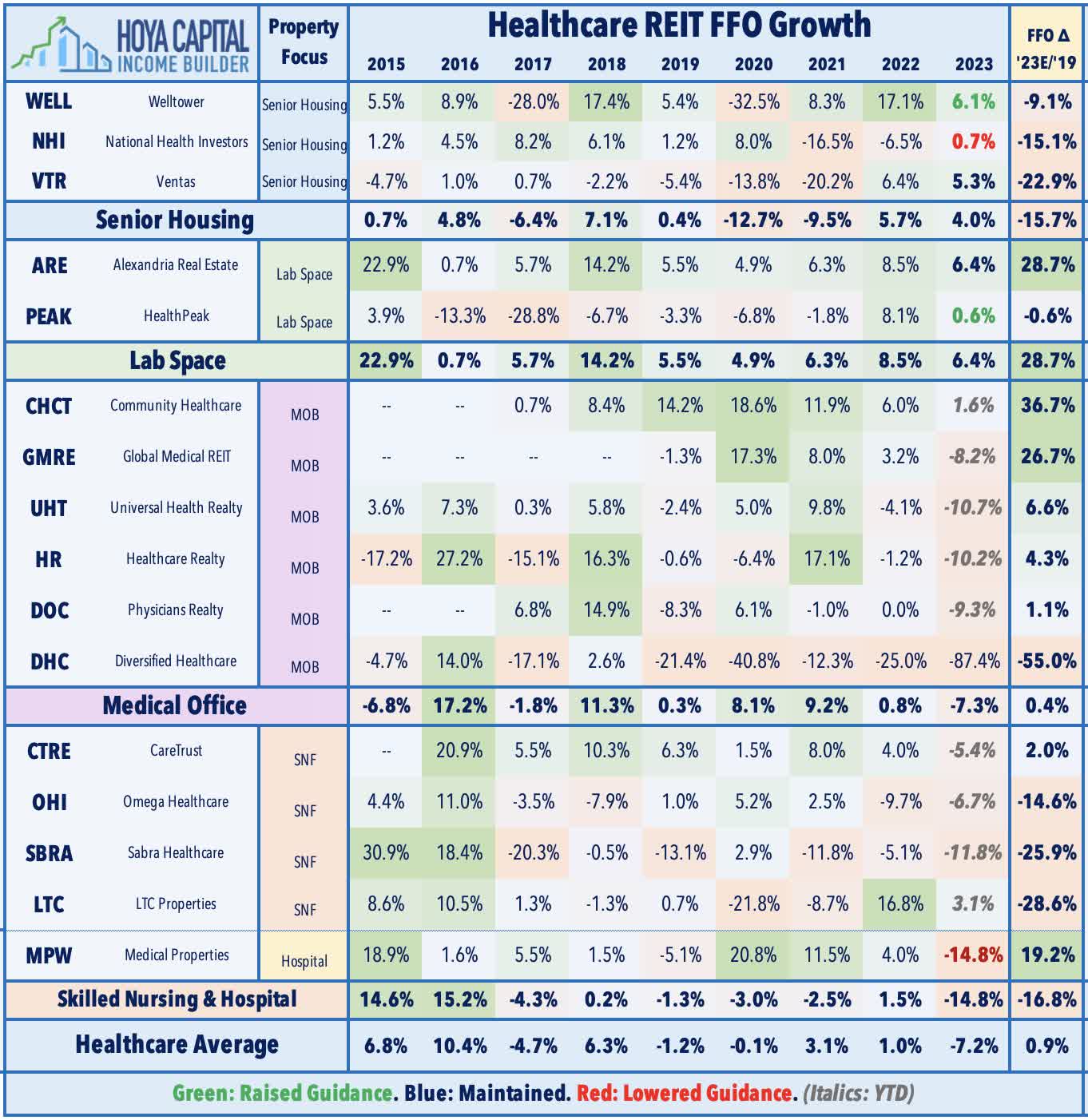

Healthcare : Medical Properties Trust ( MPW ) declined 3% on the week after it announced the closing of the sale of its four remaining Australian facilities to HMC Capital at a 5.7% cash cap rate for around AUD $470 million (approximately $305M), which will be used to reduce the balance of MPT’s revolving credit facility and to increase cash availability. MPW also announced that it has repurchased approximately £50 million of its 2.550% Unsecured Notes due in December 2023 at a repurchase yield averaging 13%. Following these actions, MPT maintains approximately $950 million of liquidity, which the company believes is "sufficient to address all remaining 2023 and 2024 debt maturities before considering anticipated dividend savings and expected proceeds from the sale of three Connecticut facilities leased to Prospect." Last week in Healthcare REITs: Recovery and Relapse , we noted that public-pay segments - Hospital and Skilled Nursing - have seen a re-intensification of tenant operator issues amid pressure from soaring labor costs and waning government support, triggering some missed rents and lease renegotiations.

{kind=link}

Mortgage REIT Week In Review

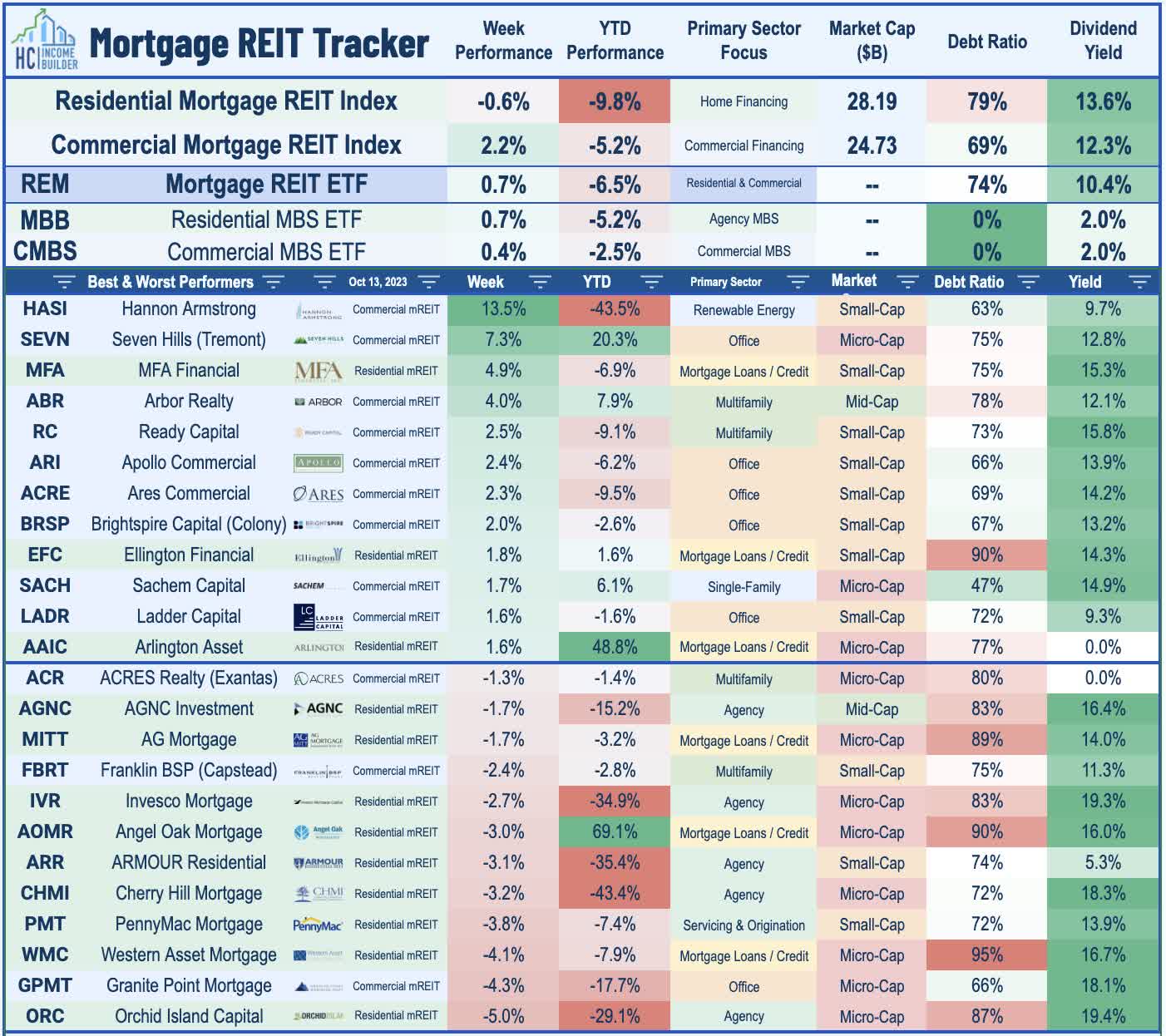

Stabilizing after a three-week skid, mortgage REITs rebounded this week as interest rate volatility - as measured by the MOVE Index - moderated following a surge to the highest levels since May last week. The iShares Mortgage REIT ETF ( REM ) advanced 0.7% on the week, lifted by strength from commercial mREITs. Following a 30% plunge in the prior week, renewable energy-focused Hannon Armstrong ( HASI ) rebounded 13% this week after JP Morgan reiterated its Buy Rating and noted that the selloff appeared overdone, a dip driven in part by the firm's commentary in the prior week in which it slashed its price target. Rithm Capital ( RITM ) gained 0.3% after it sweetened its offer to buy Sculptor Capital ( SCU ) by 8% to $12/share. The revised offer comes after a consortium of investors made a competing proposal to buy Sculptor - the largest U.S. publicly traded hedge fund - and pressured the company's Board to reconsider its approved sale to RITM.

{kind=link}

On the downside this week, Orchid Island ( ORC ) dipped 5% after it trimmed its monthly dividend by 25% to $0.12/share (18.1% dividend yield), becoming the 12th residential mREIT to lower its dividend this year. Each of the other three mREITs that declared dividends this week held their payouts steady: AGNC Investment ( AGNC ), Seven Hills ( SEVN ), and Dynex Capital ( DX ). Book Values remain in focus amid the recent resurgence in interest rate volatility and broader weakness on CMBS and RMBS valuations ahead of the start of third-quarter earnings later this month. The iShares MBS ETF ( MBB ) - an un-levered benchmark tracking RMBS valuations - rebounded 0.7% this week following sharp downward pressure last week. The iShares CMBS ETF ( CMBS ) gained 0.4% this week following a third-quarter decline of 1.2%. Spreads on mortgage-backed bonds ("MBS spreads") - an important input into Book Value models - have trended higher over the past three weeks. Since the end of Q2, RMBS spreads have widened by 13 basis points to 0.71%, while CMBS spreads have widened by 5 basis points to 1.37%. Benchmark interest rates - the other critical input affecting Book Values - have also increased during this period, with the 2-Year Yield higher by 14 basis points.

{kind=link}

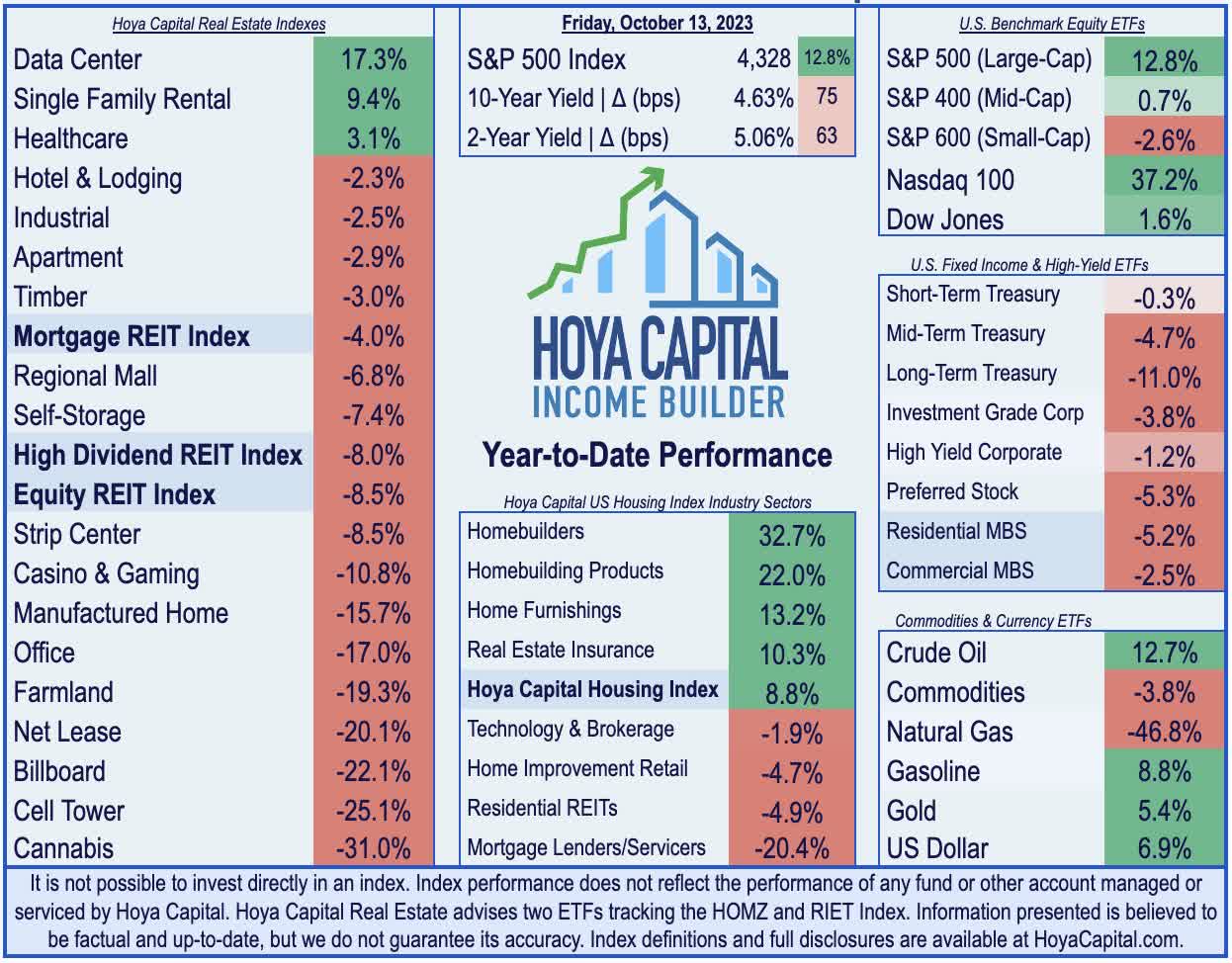

2023 Performance Recap & 2022 Review

Halfway through October, the Equity REIT Index is now lower by 8.5% on a price return basis for the year (-5.5% on a total return basis), while the Mortgage REIT Index is lower by 4.0% (+1.5% on a total return basis). This compares with the 12.8% gain on the S&P 500 and the 0.7% advance for the S&P Mid-Cap 400 . Within the real estate sector, just 3-of-18 property sectors are still in positive territory on the year, led by Data Center, Single-Family Rental, and Healthcare REITs, while Cell Tower and Specialty REITs have lagged on the downside. At 4.63%, the 10-Year Treasury Yield has increased by 75 basis points since the start of the year - up sharply from its 2023 intra-day lows of 3.26% in April - but below the recent 15-year high of 4.81%. Following the worst year for bonds in decades, the Bloomberg US Bond Index is lower again this year, producing total returns of -1.4% thus far. WTI Crude Oil - perhaps the most important inflation input - is higher by 12.7% this year but remains roughly 20% below 2022 peaks.

{kind=link}

Economic Calendar In The Week Ahead

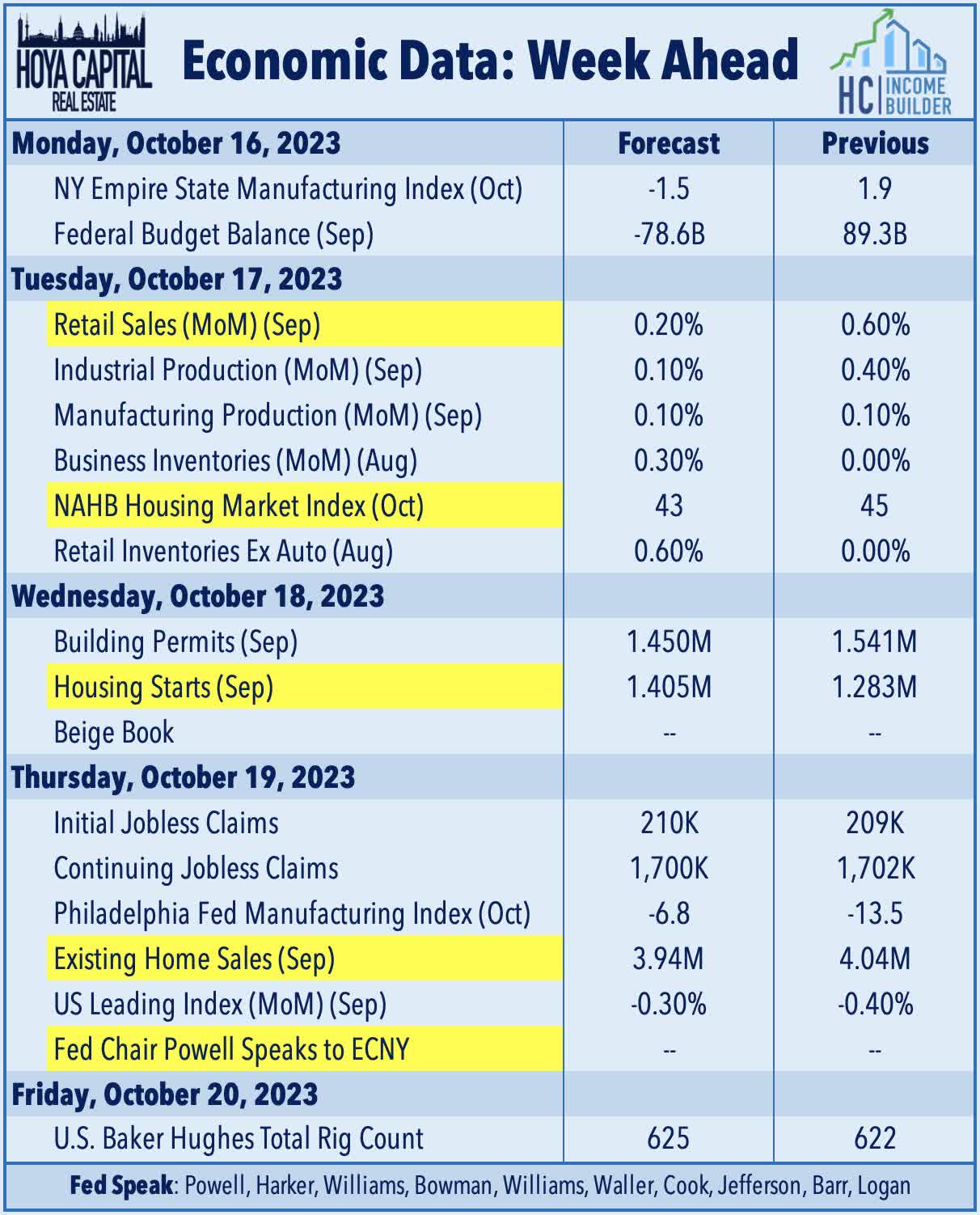

The state of the U.S. housing market will be in focus in the week ahead, which should reveal the effects of the resurgence in mortgage rates over the past several months to nearly three-decade highs. On Tuesday, we'll see NAHB Homebuilder Sentiment data for October, which is expected to decline for a third straight month. On Wednesday, we'll see September Housing Starts and Building Permits data, which is similarly expected to moderate amid a challenging financing environment for both single-family and multi-family development. On Thursday, we'll see Existing Home Sales data, which is expected to show a slowdown in sales velocity in September to a 3.94M annualized rate, which would be the second slowest month for home sales since 1995, eclipsed only by one month - August 2010 - at the depths of the GFC-induced slowdown. Despite the sales slowdown, housing inventory levels have remained near historically low levels this year due, in part, to the "lock-in" effect on existing mortgages and from the counterproductive slowdown in home building, which has kept a floor on home values and rental rates despite the stiff affordability headwinds. We'll also be watching Retail Sales data on Tuesday and another busy week of 'Fed Speak' headlined by comments from Fed Chair Powell to the Economic Club of New York on Thursday.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Different World, Same Problems