DNOPF - Dino Polska: Buying Walmart At An Early Stage But In Poland

2023-10-17 18:00:24 ET

Summary

- Dino Polska is a Polish retail chain that operates a network of grocery stores in little urbanized areas of the country.

- Its substantial growth has been accompanied by a clear strategy of standardization and cost optimization.

- Valuation multiples are at historic lows, providing a rare opportunity to buy a high-quality company at a reasonable valuation.

Investment Thesis

Many of us would have wished to invest in companies as robust and profitable as Walmart, Costco, or Kroger during their early stages. However, in developed countries, it is challenging to come across businesses that can compete with these giants, which have been thriving for decades and are already in phases of slow growth and high valuations because the market already knows about the quality of the business.

Poland, on the other hand, presents a unique scenario. Despite being part of the European Union and adhering to capitalist policies, the country has only recently emerged from the devastation caused by wars and the constraints of the communist regime. In this context, we encounter a country experiencing economic prosperity, which gives rise to opportunities like Dino Polska ( DNOPY ) —a supermarket chain that, despite its modest size, has become one of the dominant players in the country. The company is efficiently managed and seems to have several years of growth potential ahead of it.

This article will delve into the company's business model and some key aspects of its remarkable performance in the stock market. Additionally, we w ill provide a valuation to justify why I consider the company a 'Strong Buy' at its current price s.

{kind=link}

Business Overview

Dino Polska is a Polish retail chain that operates a network of grocery stores. It is one of the largest discount supermarket chains in Poland and its stores offer a variety of food and non-food products, including fresh produce, dairy, meat, and other everyday items. The company has been expanding rapidly in Poland and has gained prominence in the retail industry

The company was founded in 1999 by Tomasz Biernacki who currently holds a 51% stake in the company and serves as a member of the board. In that year, he opened his first local store in the Wielkopolska region, with the goal of providing proximity to customers, along with quality and variety in food, cleaning, and household products.

As of now, the company operates 2,272 stores, with a stronger presence in the western regions of the country, where population density is lower. Part of the company's strategic plan involves establishing a presence in cities with a maximum of 5,000 inhabitants, aiming to address previously unmet demand. In the following image, you can observe Poland's most populated cities, which clearly highlights the higher population density in the southern part of the country.

Flickr

If we examine the map of Dino Polska's locations, it becomes evident that the southern region of Poland has one of the lowest concentrations of stores. The initial idea was to establish a presence in areas with smaller populations, creating an underserved niche that larger supermarket chains might avoid due to limited growth opportunities. However, for a company like Dino Polska, it provided an opportunity to strengthen its brand and expand.

Since 2014, the company has been opening new stores at an impressive annual rate of 23%, a pace rarely seen in large supermarket chains like Walmart or Kroger. What's even more significant is that there remains a sizable, sparsely populated area in the eastern region of Poland where the company can continue to grow at similar rates.

{kind=link}

Cost Control

A key aspect of the thesis is the company's emphasis on maintaining tight control over its costs to enhance margins and deter competition, thereby making it challenging for competitors to compete on price. Some fundamental aspects of this strategy include the following:

Store Format Standardization : For this matter, I will cite the strategy as specified by the company in its financial reports .

Dino Polska’s operating strategy is based on a standardized store design, equipped with parking places for its customers and supplied with fresh products every day of the week. The sales floor area in most stores is approx. 400 square meters. Each store offers its customers approx. 5,000 stock keeping units (SKUs), for the most part well-known branded products and fresh products as well as a meat counter manned by store staff.

The idea behind this approach is to reduce design and construction costs through a standardized format, thus increasing the predictability of expenses associated with opening new stores, which allows for more precise investment planning.

Investing in Agro-Rydzyna: Since 2003, the company has established relationships with a meat processing plant named Agro-Rydzyna, aimed at streamlining the supply of meat products and maintaining uniform product standards. Over time, Dino has continued to invest in facility improvements to enhance quality, production capacity, and cost-efficiency.

Investing in Krot Invest: In 2013 , Dino's founder, Mr. Biernacki, established a dedicated company, Krot Invest, focused on constructing Dino Polska stores. This approach, similar to the previous point, simplifies the construction process by ensuring uniformity. Additionally, the company prefers to own the land for its stores, rather than renting, which not only optimizes costs but also conceals real estate assets on the balance sheet.

All of these points underscore the founder's grand vision, and, most importantly, demonstrate that the increase in margins has not occurred by chance.

Key Ratios

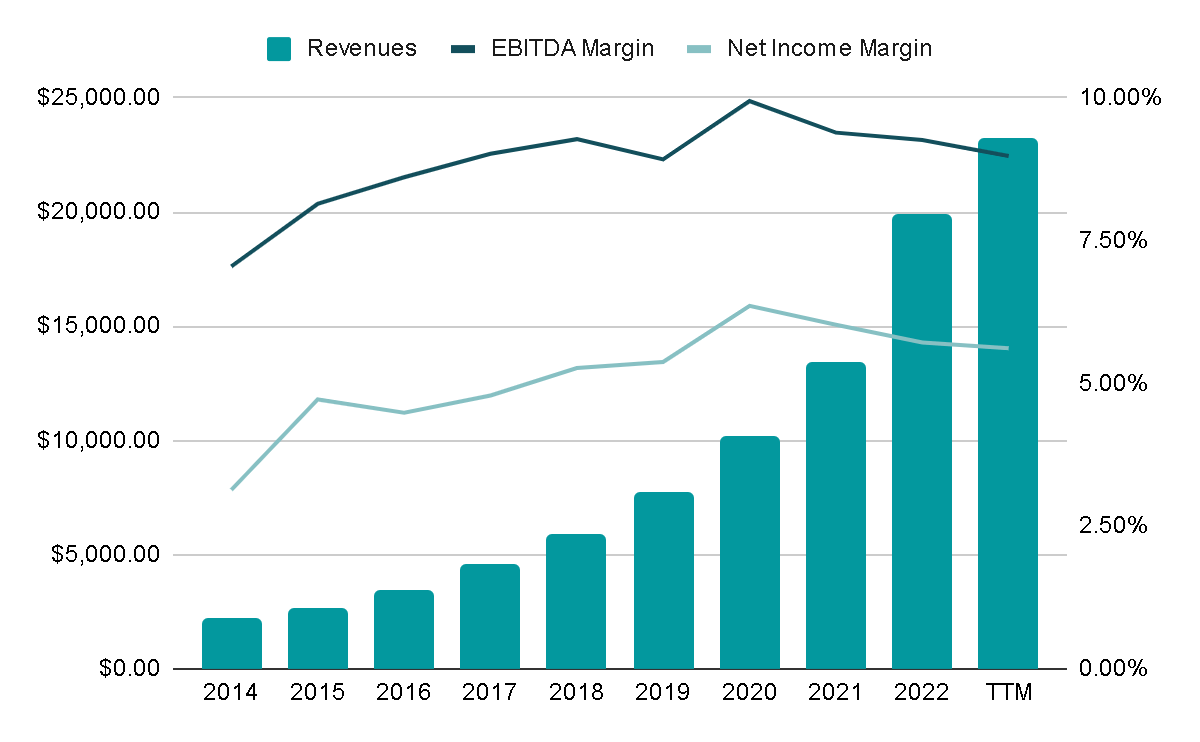

The company's growth has been remarkable. Since 2014, revenues have increased at an annual rate of 32%, while EBITDA has grown by 37% and Net Income by 42%.

As previously mentioned, effective cost control and the benefits of increased scale have contributed to raising the EBITDA margin from 7% in 2014 to its current 9%. I believe this level of margin can be sustained, and there is potential for further expansion in the future.

{kind=link}

The growth in sales can be attributed to two key factors: the expansion of new stores and increased revenue per store.

The first factor has been growing at an annual rate of 23%, and I believe it has the potential to maintain double-digit growth in the coming years. This is supported by examples from comparable companies like Biedronka, which operates almost 3,400 stores across Poland, while Dino still has room for increased penetration in many regions.

The second factor, revenue per store, has seen an annual growth of 7.5%. This growth can be achieved by adjusting prices in line with inflation or by encouraging customers to make larger purchases during each visit.

{kind=link}

Year after year, the company has reduced its leverage, and the current Net Debt/EBITDA ratio stands at 0.56x. This low ratio is attributed, in part, to the company's ownership of the vast majority of its stores, eliminating the need for leases.

{kind=link}

I find it highly relevant to share the Capital Allocation for the past five years, as it provides insight into the nature of the company.

Supermarkets are traditionally linked to characteristics like slow growth, debt, and dividend payments. However, in Dino's case, its Capital Allocation resembles that of a high-growth company. Approximately 77% of its capital has been directed toward organic growth, primarily through the expansion of new stores and investments in meat plants.

Similarly, the company relies on Cash From Operations as its primary source of financing. This approach is highly favorable in the long term as it keeps interest expenses on debt low and allows for the continued expansion of margins.

Author's Representation

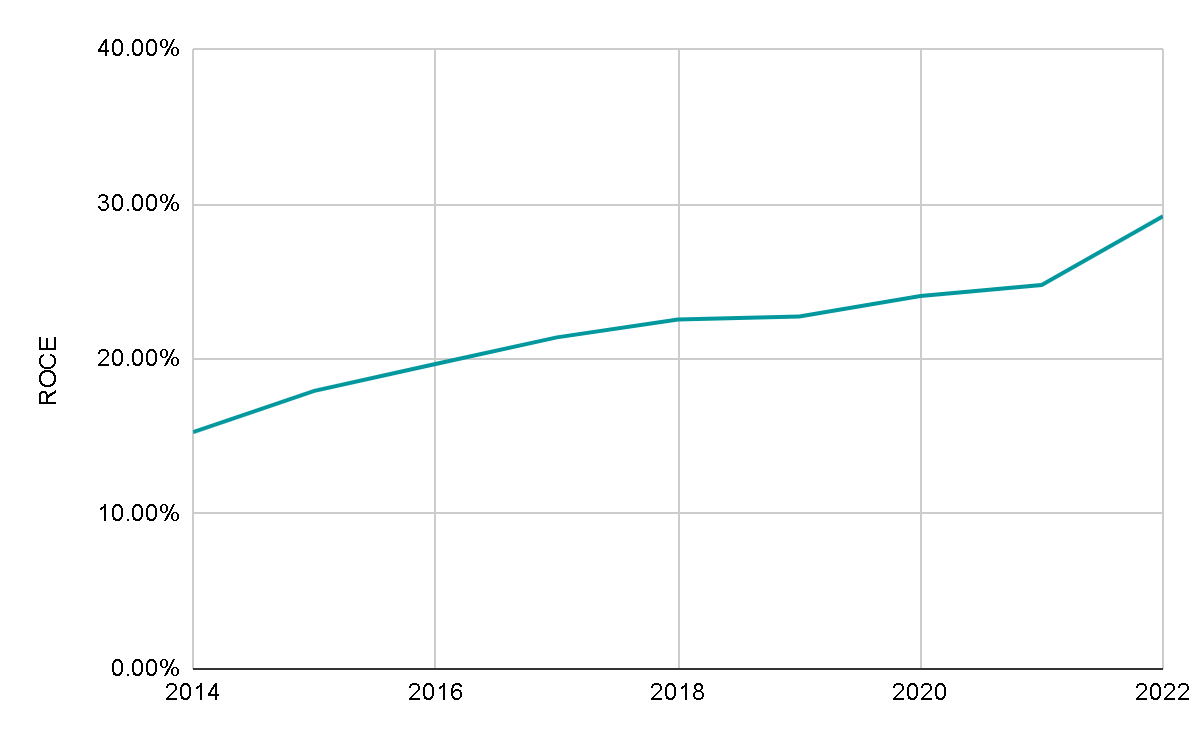

As previously noted, the primary allocation of capital is directed towards growth. When we examine the Return on Capital Employed (ROCE), it becomes evident that the company is highly profitable in its investments. In fact, this ratio has been consistently increasing each year and currently stands at around 30%.

{kind=link}

Valuation

Returning to the two key variables, I believe that the company can maintain its pace of opening between 300 and 350 new stores annually, consistent with recent years. This trend is evident in H1 2023, with the company already having opened 116 new stores, or 297 when considering the Year-over-Year comparison.

As for Revenue Per Store, I anticipate that it can continue its historical growth rate of 7%. Typically, the company raises its prices slightly above inflation, making a 7% Compound Annual Growth Rate over the next five years achievable. The 10% growth projection for this year is based on the fact that, in the first half of 2023, this metric increased by more than 10%. Therefore, I anticipate that for the second half of the year, it may show slightly slower growth.

This would mean that total revenues would grow 20% CAGR.

{kind=link}

During the first half of the year, the EBITDA margin has been around 8.5%, and the Net Income at 5.2%. To err on the side of caution, I will start from this base, and in the subsequent years, I anticipate that these margins may experience slight increases.

Regarding valuation multiples, I have chosen to maintain a conservative approach, setting the exit multiple lower than the average of the past few years, which is PER 35x and EV/EBITDA of 20x.

Based on these assumptions, this would yield a 5-year annual return of 17.6% from the current price of 366 Polish zlotys. This expected return appears quite favorable, especially considering that there are factors that could potentially drive the return even higher, such as an increase in the valuation multiple, further margin expansion, or accelerated sales growth.

{kind=link}

{kind=link}

Final Thoughts

At first glance, the company may not seem like a bargain when viewed from the perspective of the Price-to-Earnings Ratio or any other valuation metric. However, when we consider the growth in both sales and profits, it becomes evident that a company with these characteristics could justify valuation multiples of 25x, and even 30x, if the growth aligns.

In terms of risks , the most obvious, but worth mentioning, is that being located in Poland entails less geopolitical stability than in other regions of developed countries. However, I believe that this could be offset by the business model, which involves an essential consumer product, such as human food. This generates stable revenues regardless of economic crises, inflation, or geopolitical tensions.

Taking all of this into consideration, along with the current valuation, I have chosen to assign a ' Strong Buy ' rating.

For further details see:

Dino Polska: Buying Walmart At An Early Stage, But In Poland