DNOPF - Dino Polska: The Future Polish King Of Supermarkets

2023-04-14 20:13:14 ET

Summary

- Dino Polska has found an attractive niche and created a fantastic business with great potential.

- The company is a high quality business creating amazing shareholder value.

- It still has room to grow its scale and could even expand to other countries.

- I rate the stock as a buy, and I will probably start a position taking advantage of the recent drop.

Dino Polska ( DNOPY ) is a supermarket chain operating in Poland . The company has an outstanding track record of expanding nationally and still has much potential.

The price has recently dropped, and it is an excellent opportunity to become a shareholder of this wonderful business.

An attractive business model

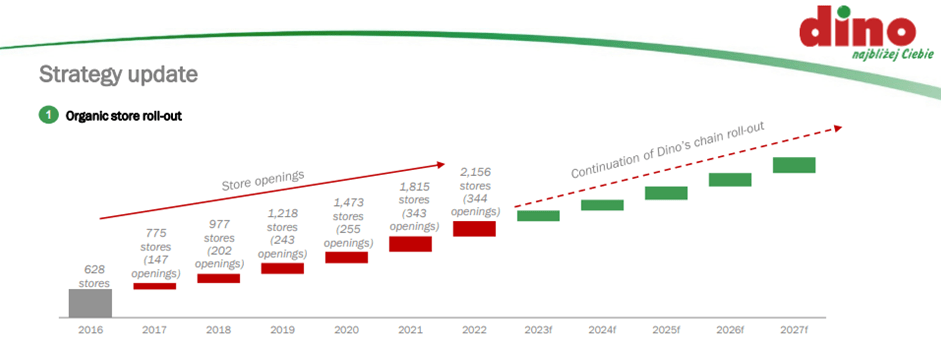

Dino Polska owns all the premises and land on which they operate, unlike most competitors who rent the premises. They operate exclusively in towns or rural populations, with at most 5,000 inhabitants representing 80% of the country's population. The business has steadily grown its store count to become one of the biggest supermarket chains in the country, currently owning 2,150 stores.

Dino Polska stores are all the same: small, equally distributed stores and require the same logistics. In them, you can find a wide variety of products. Almost 39% of sales come from fresh food, 49% from other types of food, and 12% from non-food products. Indeed, each store can satisfy the inhabitants' needs.

The chain specializes in fresh food ( slide 7 ), especially in terms of meat. This is attractive for customers since meat (especially pork and chicken) is the Polish diet's mainstay. Regarding this, in its early days, Dino-Polska bought a meat factory, Agro-Rydzyna. In this way, not only can they offer high-quality fresh meat, but they also save extra costs.

Source: Dino Polska's 2022 Results Presentation

Outstanding profitability in a complex market

When analyzing a retail business, it is essential to study stores' profitability. In general, grocery stores are not the most profitable businesses. They tend to have low margins and be very capital intensive, which harms returns on capital. Nonetheless, some top-drawer supermarket channels, such as Dino Polska, outperform the average , attaining outstanding returns on capital.

Dino Polska's margins are on top of the line: 24% Gross Margin, 8% EBIT Margin and 6% Net Margin. Comparing those numbers with competitors, Dino Polska stands out, as they can operate with lower prices. Various reasons can explain this:

- Owning each of their locations saves them 3% of the margin.

- Thanks to the nature of the business, they hardly spend money on advertising.

- Their identical stores make logistics and business running much easier, helping save costs.

- Owning a meat manufacturer saves them some money too.

If we study individual stores' profitability, the result is fantastic. Each store takes an average of 3 years to reach its mature state. They bill around 8M Zloties (or $1.8M) at its maturity state. Gross margins are over 25%, and EBIT margins are around 8%. Assuming a tax rate of 19% (corporate tax in Poland), each store gets an annual NOPAT of 520k Zloties (or $120k) in its mature state. Also, the maintenance CapEx of each store is less than 30k Zloties (or $6k) per year. Considering that each store costs 2.5M-3M Zlotties to manufacture, this leaves us with an implied return on invested capital of around 20%.

In effect, Dino Polska is a high-quality business returning appealing returns on capital. Having these numbers in such a difficult market is commendable, something that only the best companies (ex: Costco and Walmart) have reached.

Strong competitive advantages

One could think that Dino Polksa's moat is not strong enough to ensure long-term growth and profitability, as there are a lot of different supermarket chains. However, as previously seen, its business model takes advantage of numerous competitive advantages.

Economies of scale

This scale allows them to have significant operating leverage and facilitate margin expansion . Once the fixed costs are covered (which correspond to the land purchase), the income grows faster than the costs since its variable costs are pretty low. The scale is a consequence of owning their premises, and buying cheap land.

This scale allows them to have significant operating leverage and facilitating margin expansion. Once the fixed costs are covered (which correspond to the purchase of the land), the income grows faster than the costs, since its variable costs are quite low. The scale is a consequence of owning their own premises, buying cheap land.

This requires quite a significant investment, which is why many companies rent the land instead of buying it. As seen, the land purchase saves the company about a 3% margin each year. But do the accounts come out? This extra investment would be amortized in about 6/7 years of activity, so it is only profitable if the company can keep its stores open for long periods, which is the case with Dino Polska. Indeed, they have only closed one store in all the years they have been in business.

Entry barriers

Dino Polska's business model is very profitable, which could lead to competitors entering the market. Nevertheless, its business model is quite tricky for traditional supermarkets to replicate.

Dino Polska manages to be very profitable by building stores in towns where other competitors could not be as profitable as them. Located in small towns, supermarket chains with huge stores cannot build them in those towns since the investment would not be worth it. In this way, the company eliminates many of the most renowned potential competitors.

Pricing power and costs advantages

Dino Polska's pricing power and magnificent margins are a strong protection against competitors and inflation. Indeed, the LFL sales grow above the annual food inflation. This growth may be skewed as the company has a lot of new stores growing faster than average. Nonetheless, the company has consistently grown LFL sales above inflation rates. In fact, the gap between LFL growth and inflation is quite large, consistently above 8% (slide 7). As a result, Dino Polska's resilience stands out.

Source: Dino Polska's 2022 Results Presentation

Furthermore, the company can maintain its margins during high inflation periods, cutting down on other operating expenses and hiking prices, avoiding incurring losses. In addition, by having such wide margins compared to other supermarkets, if a business is installed next to Dino's store, they could lower prices without actually making losses to expel the rival from the town.

The past was excellent, but is the growth sustainable?

At the end of 2022, they had 2,156 stores in the territory, when they only had 234 in 2012, almost ten times more in 10 years, a 25% annual growth in the number of stores. Then, since 2014, revenue has grown over 30% annually, and EBITDA and Net Income over 35% annually. Furthermore, EBIT Margins have increased from 5% in 2015 to 8% this year.

We can see that growth has not only come from store openings, but also from organic growth and margin expansion (slide 8).

Source: Dino Polska's 2022 Results Presentation

Without going any further, this year's sales have increased an outstanding 48% y-o-y. LFL sales have grown at a 28%, partially boosted by the 15% food inflation. Inflation has hardly affected the business; the EBITDA margin has decreased by 0.2% y-o-y, resulting in an annual EBITDA growth of 45%. These top-drawer numbers are encouraging, as even though the company scale is wider than ever, growth is still going strong.

However, we must study the market potential, as this growth is impossible to maintain in the long term.

Effectively, Dino Polska's scale is bigger than ever. They are progressively increasing their store density in every region. In the next slide, we can see the detailed progress, as well as the company's objective (slide 5).

Source: Dino Polska's 2022 Results Presentation

Dino Polska's objective is to reach the mark of over 12 stores per 100k inhabitants in the country. The goal has already been successfully reached in a couple of regions, but some regions still have a lot of penetration potential. The actual store density in the entire country is at 5.7, less than half the final objective.

Source: Dino Polska's 2022 Results Presentation

{kind=link}

Poland has 38M inhabitants. Doing the math, store count could easily reach the 4,000 stores mark. If they arrive at their 12 stores per 100k inhabitants objective, they could quickly build a 4,500 stores empire, twice the number of stores. Nonetheless, they still open new stores in regions where the goal has already been achieved, which shows that the 12 stores goal is still conservative.

While growth will still endure, it will probably gear towards more reasonable levels, as store count is already reaching a good number and some stores are already at their mature state. The company will keep opening new stores. I expect them to open around 300 stores yearly, a 15% annual rise. Furthermore, if inflation returns to normality, LFL sales should stabilize.

The company could also expand to neighboring countries, like the Czech Republic. However, this is still uncertain. The business is focused on the national territory. However, it could be a powerful source of growth and would surely increase the company's terminal value.

Valuation

I will use a straightforward valuation method in this case. Dino Polska finances its growth almost entirely with its operating cash flow. Then, doing a DCF would be a mistake.

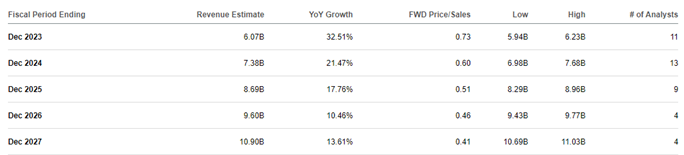

Next year, with over 300 new stores and a 15% LFL sales growth, revenue could increase over 30% y-o-y. Nonetheless, as I have said, growth will progressively decrease. I estimate it will gear towards 12% to 15% in 2027, a very appealing number. Following those numbers, the company would still have room to increase its store count and grow at attractive rates. Those numbers would imply 54M Zloties revenue in 2027.

Margins should increase thanks to the scale. Stores reaching their state of maturity would also help in the matter. Then, I expect EBIT Margins to reach the 8.5% barrier by 2027. Taking into account the Polish corporate tax rate of 19%, Dino Polska could earn over 3.5M Zloties by 2027. Seeing that these estimates are close to analysts' estimates is quite comforting too.

{kind=link}

Applying an LTM P/E multiple of 18x leads to an implied 65M Zloties market cap in 2027. We can also use a 15x EV/EBIT multiple, which would imply a 66M Zloties market cap. These are still quite conservative multiples as the company could grow at high single digits or low double digits from 2027 onwards with a 20% ROIC. Furthermore, the average P/E is around 25x, and the average EV/EBIT is around 18x. Finally, the stock has the potential to become a cash cow. In fact, no sooner do store openings reduce, cash flows will be massive.

Considering that the company has yet to issue or buy a single share since its IPO, I expect the share count to stay the same. This is probably related to the founder and CEO owning over 50% of the total share count.

All of this leads to an implied return of 12.9%, still being conservative. If the company expands to other countries, the terminal value would be higher, and returns would be even greater. However, this is still very hypothetical.

Multiple Valuation on 04/11/23, Author's creation

Risks are not neglectable

Dino Polska is a wonderful business with great potential. However, there are still some risks that we must consider.

First, in such a competitive market, there is always the risk of a copycat trying to replicate the business model. Though Dino Polska has great competitive advantages and operates in a niche unattractive to other competitors, you never know.

Source: 2017 Company Presentation

{kind=link}

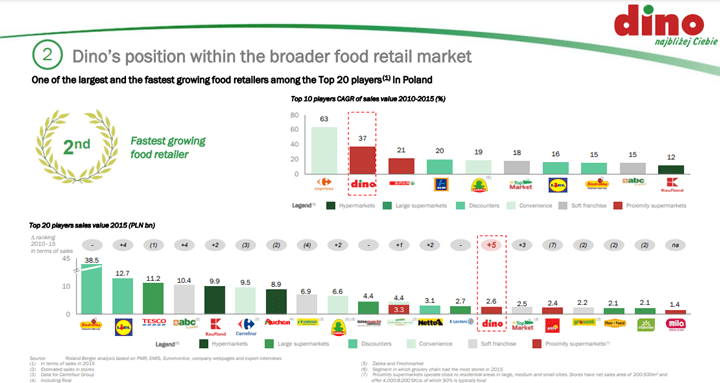

We can see many food retailers in the market. Dino Polska's growth made them grind from the 14th biggest food retailer in 2017 to the 6th at the beginning of 2020 . Updating the data, with the latest years' remarkable growth, Dino Polska should have already become the 4th biggest food retailer in the country.

Effectively, the bigger the scale, the more difficult it is for competitors to replicate the business model. Today, being the 4th biggest food retailer in the country, it is way more complex than years ago.

Moreover, the same scale that protects the business from copycats could endanger its long-term growth. Dino Polska has built over 2,000 stores, representing less than half the targetted stores. In that case, growing at 300 to 400 stores per year, the objective could be reached in 6 to 7 years. Then, if the company can't grow its scale once the target is reached, growth would substantially decrease. In that case, the valuation multiple would suffer damaging contraction, but the growth path would compensate for the contraction, and we would get great returns still.

Furthermore, I think Dino will continue expanding its scale once it reaches its goal. Indeed, in 2020, the plan was to get to 8 stores per 100k inhabitants (slide 5) . The company rapidly understood its potential and increased its objective. In addition, I think that this objective is still conservative. On the one hand, the store count growth is still intact, and the purpose has been more than achieved in some regions (over 14 stores per 100k inhabitants in 2 areas).

Don't buy the OTC ticker

You could buy Dino Polska's OTC. However, I wouldn't recommend it at all. I would only buy Dino Polska's shares if I could buy the original stock, which trades in the Warsaw stock exchange with the ticker DNP (ISIN: PLDINPL00011).

The OTC ticker is too illiquid. As a result, its price could stagnate or suffer sudden changes without other cause than liquidity, not following the price of the original stock. Then, you would incur a much higher risk.

Conclusion

Dino Polska is a high-quality business that can keep growing while creating value for shareholders. Today's price (on 11/04/23) implies a 12.9% return, still being conservative. The company could expand to other countries, and the national potential could increase, as it already happened in 2020.

Because of this, I rate Dino Polska stock as a buy. I will probably start a small position in the following days, taking advantage of the recent drop, and will try to progressively increase my position if the price doesn't skyrocket.

For further details see:

Dino Polska: The Future Polish King Of Supermarkets