DJIA - DJIA: JEPI Has A Frenemy And It Highlights JEPI's Risks

2023-05-05 11:25:53 ET

Summary

- I continue to be skeptical of JEPI, based in part of potential risks I see in how it is constructed. I think DJIA is a simpler alternative.

- JEPI's size has made it vulnerable, and DJIA offers much greater transparency.

- I rate DJIA, one of my most recent purchases in my own account, a Buy.

I understand all the excitement about JPMorgan Equity Premium Income ETF ( JEPI ), especially within the Seeking Alpha audience. It has performed well, spins of a hefty yield, invests in relatively stable businesses, and is backed by the financial firm that is increasingly becoming the bailout chief, picking up the crumbs of weakened regional banks. What could go wrong?

Here's what could go wrong. Inside of funds: mutual funds, hedge funds, or ETFs, some of the biggest risks in history were obvious, but did not become newsworthy until after the fact. Put another way, just because an ETF carries potentially high risk, that doesn't mean that risk will ever be realized. But if it is, watch out. Think tech stocks in 2000, financial stocks in 2008, bonds in 2022 and now, JEPI over the next couple of years.

That's why I was thrilled to discover Global X Dow 30 Covered Call ETF ( DJIA ) ETF. I consider it to be JEPI's "frenemy," a combination of its friend (peer) and its enemy (competition).

No, DJIA it not perfect. And my aim is not to trash JEPI at the expense of DJIA, or even Amplify CWP Enhanced Dividend Income ETF ( DIVO ), which I'd place in the same peer group of covered call ETFs. My main reason to favor DJIA for my own money is simple: it's simple. And by that I mean transparent. It owns the 30 stocks in the Dow Jones Industrial Average, at the same weightings as that index does, plus a covered call position bought in the public market. On the other hand, JEPI's success has been a double-edged sword. At more than $25 billion in AUM, it cannot maneuver as easily as it did back in August of 2020, when its asset base stood around $70 million. That's right around where DJIA is today. These "under-followed" ETFs are my favorite ones to cover, my niche at Seeking Alpha, if you will. And DJIA fits the criteria, including its straightforward construction.

This article is primarily about DJIA, but I did want to include some insight as to why I bought that ETF instead of the 800-pound gorilla in the group. I rate DJIA a Buy, in part because I now own it personally.

KISI: Keep It Simple, Isbitts!

Consider this from DJIA's website:

DJX US 05/19/23 C340

That's the full security description of the covered call position line item within DJIA as of May 2, 2023. It shows that the fund was short call options on DJX, which is the CBOE symbol for options on the Dow Jones Industrial Average. That covered call option expires on May 19, at which point DJIA will roll it over and collect more call option premium. The strike price is $340, which as of this writing is about 2% above the value of the Dow, thus leaving a little room for price appreciation.

Now, isn't that simple? I know what I own, and I know what Global X is going to do next. They are going to continue holding the Dow stocks in their proper weights, and write covered calls monthly. That's all my simple brain prefers to accept when it comes to covered call ETFs.

DJIA has only been around for about 14 months, and JEPI is coming up on its 3-year anniversary. So neither ETF has a track record that has been tested in a wide variety of market climates. That's another reason I like the "know what you own at all times" aspect of DJIA. While many investors dismiss the Dow Jones Industrial Average as old fashioned, I like the fact that it is a collection of 30 venerable companies that tend to be the sector leaders that others follow. In other words, there's a lot of equity market coverage with those 30 names. So getting those, plus a monthly covered call overwrite, is OK by me.

JEPI has outperformed DJIA during the period of their common existence. But how much does that matter in a market that changes its mind by the moment, and during a period that saw a "tail risk" event of sorts, in the form of the sharpest Fed rate hike cycle of our lifetime.

And when it comes to dividend yield from that covered call activity, combined with the dividends from the stock holdings themselves, DJIA is not far behind JEPI so far. I will accept a little less yield in exchange for more transparency and simplicity.

Ycharts and Seeking Alpha

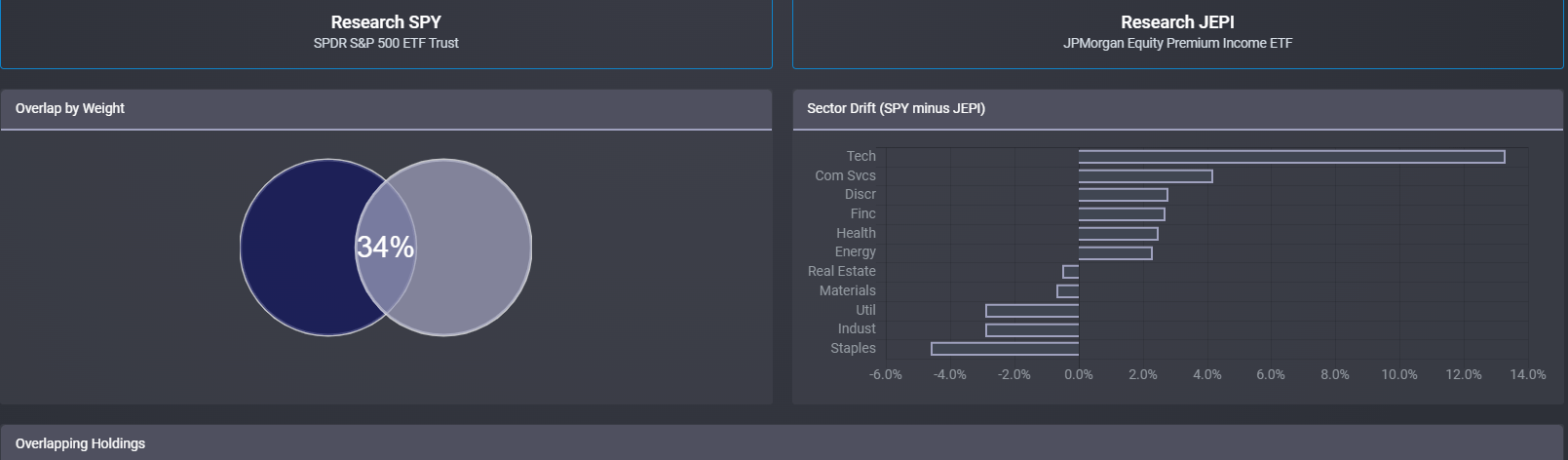

The 2 ETFs have some overlapping holdings, and JEPI's current portfolio looks more like the Dow than the S&P 500 to me. Given that the S&P 500 is the index it claims to try to match up against, and that its covered call writing targets the S&P 500, that seems off to me. But this article is primarily about DJIA, the new kid on this covered call ETF block, so I'll leave that alone for today.

{kind=link}

What I won't leave alone

Here's what I just cannot ignore when I consider JEPI's amazing success in gathering assets, and its solid past performance. Below is from that ETF's marketing material. It talks about "selling options," and we know that's a primary driver of its returns.

JPMorgan.com

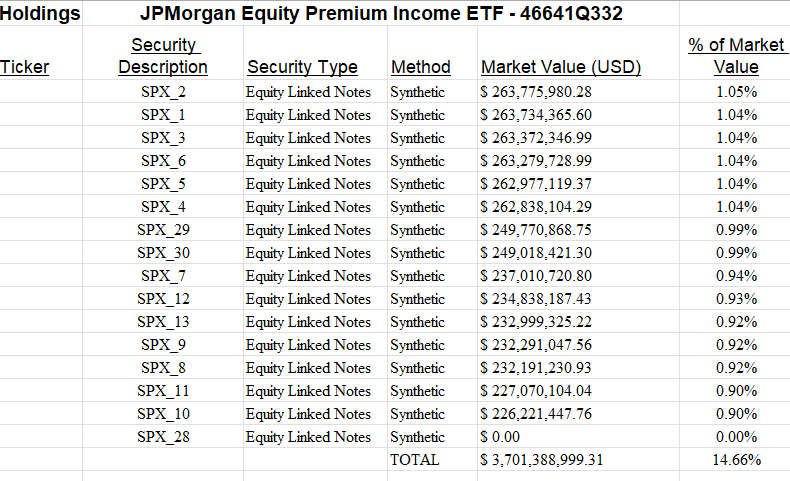

Now, consider this, from JEPI's holdings list at JPMorgan.com, as of May 2, 2023:

{kind=link}

I see $3.7 billion of "equity linked notes," or ELNs. Those make up nearly 15% of JEPI's assets. What are ELNs? Here's how they are explained in the Summary Prospectus for JEPI:

Equity-Linked Notes Risk. When the Fund invests in ELNs, it receives cash but limits its opportunity to profit from an increase in the market value of the instrument because of the limits relating to the call options written within the particular ELN. Investing in ELNs may be more costly to the Fund than if the Fund had invested in the underlying instruments directly. Investments in ELNs often have risks similar to the underlying instruments, which include market risk. In addition, since ELNs are in note form, ELNs are subject to certain debt securities risks, such as credit or counterparty risk. Should the prices of the underlying instruments move in an unexpected manner, the Fund may not achieve the anticipated benefits of an investment in an ELN, and may realize losses, which could be significant and could include the Fund’s entire principal investment. Invest ments in ELNs are also subject to liquidity risk, which may make ELNs difficult to sell and value. A lack of liquidity may also cause the value of the ELN to decline. In addition, ELNs may exhibit price behavior that does not correlate with the underlying securities. The Fund’s ELN investments are subject to the risk that issuers and/or counterparties will fail to make payments when due or default completely. Prices of the Fund’s ELN invest ments may be adversely affected if any of the issuers or counterparties it is invested in are subject to an actual or perceived deterioration in their credit quality.

I know this is the legalize, and that every ETF has something like this. Well, at least they have something that describes the ETF's strategy and risks. Most don't read like this. Because most ETFs don't resort to holding 15% of their assets as a surrogate for writing call options on a portfolio of stocks. JEPI likely does this because they have outgrown the traditional, liquid options market. That means they must resort to ELNs, a set of private contracts with counterparties.

ELNs: not my favorite flavor when it comes to pursuing this investment style

I cover plenty of ETFs that own private swap or options contracts. But they are very upfront about who the counterparties are. I went beyond the standard holdings list, right to the source (JEPI's own website), and I still did not get much detail. My bottom-line: if the ETF makes due diligence this cumbersome, it gets knocked down a couple of pegs on my rating scale.

And, while maybe this is much ado about nothing, I invested through 2008, when counterparty risk and opaque contractual instruments used as surrogates for "real" securities like stocks and options were at the epicenter of the crisis that nearly brought the financial system down.

My conclusion on JEPI: another example of Wall Street creating a fine product in concept, but then it got so popular, almost cult-like, that it has to let the proverbial wolf in the door, in the form of replacing good old covered call options with, well, I don't exactly know what.

So, that was my recent journey to embrace covered call writing ETFs, or at least one of them for now. I see potential for this investment style in a stock market starving for direction, any direction! But for my first foray into it, DJIA was my tool of choice, not JEPI. I also have my eyes on ways to combine covered call ETFs with other ETFs that create an even more alpha-seeking portfolio. But that's another story for another time, as it develops. For now, DJIA is in my portfolio, and I rate it a Buy. I'll consider it JEPI's "frenemy," a combination of its friend (peer) and its enemy (competition).

For further details see:

DJIA: JEPI Has A Frenemy, And It Highlights JEPI's Risks