YYY - Don't Expect Too Much From YYY

2023-07-17 15:41:29 ET

Summary

- Amplify High Income ETF has a current dividend yield of 12% but has underperformed market indices since its inception, with a share price down -42%.

- The fund holds 45 CEFs in its portfolio, selected based on dividend yield, discount to NAV and liquidity, but this approach can result in picking "yield traps" and underperforming CEFs.

- The fund's long-term performance shows an annual compounded growth rate of 3.12%, and its total annual return is only a quarter of its annual dividend.

Amplify High Income ETF ( YYY ) is a high yielding income play that has a current dividend yield of 12%. The fund has been around for a decade, and its performance has been underwhelming to say the least. I don't expect a reason for this fund to start outperforming anytime soon.

Since its inception, YYY's share price is down -42% but its total return (including reinvestment of dividends) is up 103%. The fund has vastly underperformed market indices in both metrics, as S&P 500's share price appreciation came at 238% and its total return came at 317% during the same period.

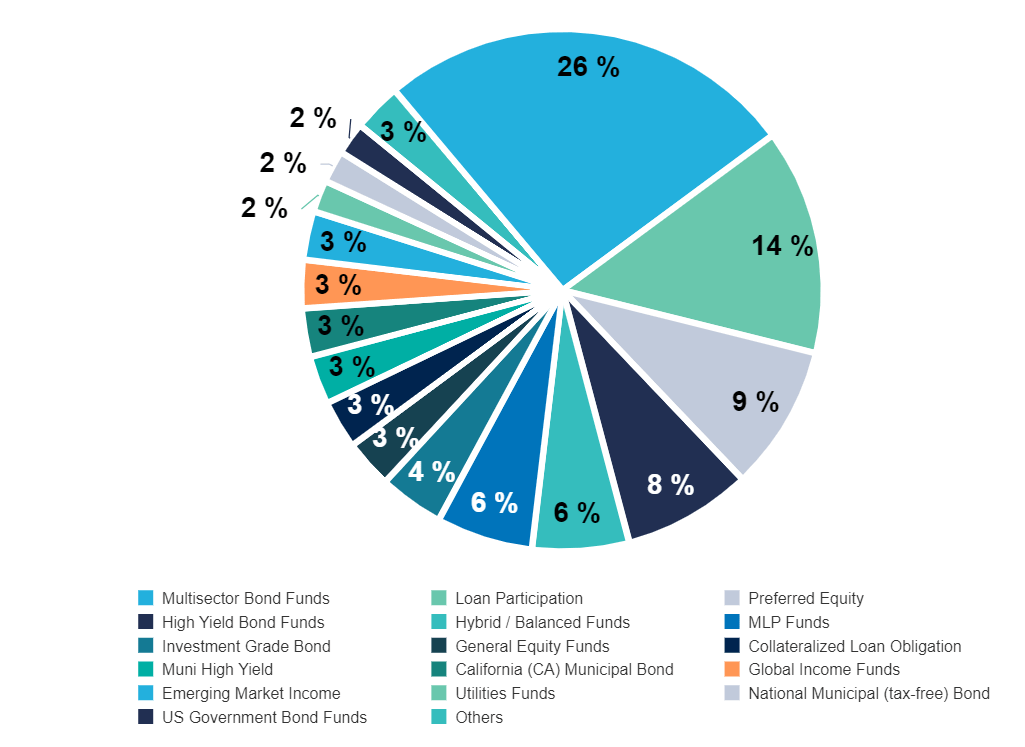

The fund holds a total of 45 CEFs in its portfolio. It's not exactly actively managed, and its holdings rarely change. Currently, 26% of the fund's holdings are in multi-sector bond funds, 14% in loan participation funds, 9% in preferred equity funds and 8% in high yield bond funds.

{kind=link}

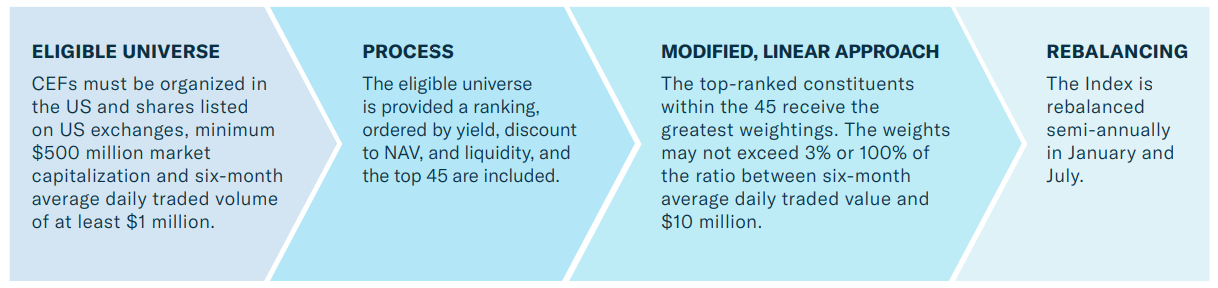

Even though the fund is not actively managed, it uses a screening criteria approach where its components are selected based on a number of pre-defined criteria. The fund's number of holdings are always set at 45 and no single position can exceed 3% of its total weight. The fund starts its selection by creating a list of all CEFs that trade in the US with a market cap of at least $500 million and daily average volume of $1 million for liquidity purposes. Then it ranks them by dividend yield, discount to NAV and liquidity to pick the top 45. Weightings within the fund are based on ranking of each component based on the screening criteria mentioned above. For example, CEFs with a higher dividend yield or bigger discount to their NAV are given a bigger weight. The fund's components and weights are updated twice a year.

{kind=link}

There is a problem with this approach, though. While selecting CEFs based on yield and NAV discount sounds like a great approach, it can result in picking "yield traps" and those CEFs that are bleeding out value. I can understand investing into CEFs based on NAV discount during market-wide panics and market crashes like March 2020 where almost every CEF was selling for a deep discount, but most other times, you have to pay attention to why a CEF is trading at a discount. There are many times, CEFs trade at deep discounts for a good reason, and they will likely continue trading at a deep discount until they fix their problems. If a CEF is constantly losing money, making bad bets, overly leveraged and designed poorly, it makes sense for that CEF to trade at a discount. Similarly, investors will often reward good CEFs with good management with a premium pricing against their NAV.

This fund not only uses dividend yield and NAV discount as the biggest criteria for stock selection, but also as the biggest criteria to determine the weight of each selection. In theory, they could give the most weight to the worst CEFs that trade at a deep discount and high yield because they are in deep trouble, and the least weight to CEFs that are well managed but trade at a premium price with lower dividends.

This strategy will also result in fund management trimming their highest performers and reducing the weight of those performers while adding to their worst performers and increasing their weight over time, so the problem doesn't end with initial stock decisions either. It continues on even after initial decisions have been made because the strategy rewards underperformers and punishes outperformers.

When we look at the fund's long term performance, its annual compounded growth rate comes at 3.12%. Compare this to the fund's dividend yield of 12%, and you find that the fund's total annual return is only 1/4th of its annual dividend. In other words, 3/4th of the fund's dividend payout will go to cover the value decay you might experience if you choose to reinvest your dividends. As a rule of thumb, if a high yielding fund's total annual return is less than 50% of its dividend yield, it's best to stay away. Ideally, a fund's total return level should be the same or even slightly above its dividend yield, but it should be at least half of the yield in a worst case scenario. Otherwise, you know that your dividend payments will barely cover the decay in your principal.

{kind=link}

In the last decade, we've seen YYY cut its distributions several times. Currently, the fund pays about 12 cents per share per month, but it was paying 20 cents not long ago and almost 30 cents a decade ago. This type of dividend performance is very typical with funds that see NAV decay over time because they have less and less assets to generate income with. Sometimes they try to remedy this by paying dividends out of ROC (return of capital) and other times they will use leverage to keep their dividends stable, but those rarely work in the long run. So far I haven't seen YYY employ leverage, but that would only result in faster NAV decay in the long run unless the fund's strategy was fixed. Also keep in mind that even though YYY doesn't use leverage, many of the CEFs held by YYY definitely do, so this is another thing to keep in mind.

Don't get me wrong, I don't hate all of YYY's holdings. There are actually some holdings of YYY I personally like and even hold in my portfolio, such as Pimco's PDI ( PDI ) and PTY ( PTY ). I also happen to like Liberty All-Star Equity ( USA ) considering its long track record of strong performance both in total return and dividend growth fronts. Neither am I opposing buying CEFs at NAV discounts. There have been many cases were buying high quality CEFs at deep NAV discounts resulted in strong returns, such as back in 2020. If a fund has a track record of strong performance over many years, and it trades at a discount, I'd absolutely buy it, but I wouldn't pick NAV discount or yield as my sole criteria when picking whether to buy or how much weight to allocate to a particular CEF.

I expect YYY's underperformance to continue for the foreseeable future as long as its strategy of picking funds based mostly, or only on, yield and NAV discount continues.

For further details see:

Don't Expect Too Much From YYY