COLD - Don't Fall Prey To The Dark Side Of AI Buy These REITs Instead

2023-12-18 07:00:00 ET

Summary

- Artificial intelligence has gained excessive coverage and attention in the financial market news since November 2022.

- There are concerns about the potential job losses and ethical implications of AI as well as the possibility of AI being used inappropriately.

- In this article, I'm providing readers with a few of my highest conviction REITs.

If you follow financial market news - and I assume you do since you're here - you may have seen a story or two this year about artificial intelligence, or AI.

And by a story or two, we all know I mean excessive coverage. Ever since November 2022, when ChatGPT leaped into public focus, the race has been on. Everyone and their mother's chiropractor's best friend's neighbor seems to want in on the action.

Every company that can has talked up its AI efforts.

Every investor has put at least some money into the game, fueling the "Magnificent Seven's" astronomic share gains this year.

Every news outlet is covering it in hopes of generating more clicks.

Even AI's detractors have to admit there's real potential here. They just disagree with how long it will take to reach it and/or whether "it" is ultimately for good or evil.

In full disclosure, I'm involved in an AI real estate startup, which I have a lot of hope for. Even so, I believe there are legitimate questions and concerns about this emerging technology that need to be discussed.

For instance, how many people will lose their jobs because of AI? And what will the economic effect of that be?

What are the ethical implications of human morality being removed from our technological interactions like this?

Is this the start of an apocalyptic sci-fi existence?

Do we really know what we're getting into?

Let the Artificial Intelligence Trials and Errors Begin

Already, there's been a few epic failures from AI usage.

Take recently eliminated Sports Illustrated CEO Ross Levinsohn. Yahoo News reported earlier this week how:

"A spokesperson for The Arena Group ( AREN ), which publishes Sports Illustrated… declined to specify why Levinsohn had been fired, saying the decision was made to 'improve the operational efficiency and revenue of the company.' However, Levinsohn's termination comes weeks after an investigation by tech website Futurism alleged that Sports Illustrated had published articles from authors generated by artificial intelligence."

According to Arena Group's "initial investigation," this was inaccurate. The product reviews in question were "from an external, third-party company, AdVon Commerce" which uses "both counter-plagiarism and counter-AI software on all content."

However, it learned that some AdVon writers in some articles used pseudo names, which is apparently unacceptable.

So, Arena removed the content, initiated an investigation, and ended the partnership.

A little odd, right?

Moreover, Levinsohn wasn't the only executive fired. So were COO Andrew Kraft, media president Rob Barrett, and corporate counsel Julie Fenster.

If the Yahoo News comments are any indication, most people still believe inappropriate AI usage was involved. To quote "Young Gun":

"It's the old adage: 'If you ain't cheating, then you ain't trying.' Their mistake wasn't just the cutting of corners to save money - it was getting caught doing it."

And "Mike" added:

"There is nothing good coming out of AI. Has no one seen any of the Terminator movies? How about the book Demon Seed by Dean Koontz? How long will it take even the smallest computer to decide humans are not needed?"

The first comment, incidentally, had 17 likes and one thumbs down at last check. And the second had a full dozen approvals with not a single dissenter.

The Professional, Proactive Thing to Do

Ars Technica publicized another example on Wednesday: " Michael Cohen's lawyer cited three fake cases in possible AI-fueled screwup ."

It appears that:

A lawyer representing Donald Trump's former attorney Michael Cohen filed a court brief that cited three cases that do not exist, according to a federal judge. The incident is similar to a recent one in which lawyers submitted fake citations originally provided by ChatGPT, but it hasn't yet been confirmed whether Cohen's lawyer also used an AI tool."

That other case, incidentally, happened back in June. And the AP says a federal judge fined responsible parties $5,000 in response.

Who knows if Cohen's team will face the same. But it seems safe to say U.S. District Judge Jesse Furman isn't impressed with the lawyers' case so far.

These incidents are a big problem across so many industries. That's why, according to The Wall Street Journal , SEC head Gary Gensler remains pretty skeptical about AI.

"The SEC's examinations division has sent requests for information on AI-related topics to several investment advisers, part of a process known as a sweep. The agency wants details on topics including AI-related marketing documents, algorithmic models used to manage client portfolios, third-party providers and compliance training, according to one such letter obtained by Vigilant Compliance, a regulatory compliance consulting firm."

This is far from a criminal investigation, but it does indicate significant concern.

Again, I fully understand those worries. AI should be a useful tool, not a substitution for good old-fashioned human reasoning.

Which is why I pledge to make the most of my resources.

I can't say I'll never utilize artificial intelligence. But I'll always go "above and beyond" by doing my own research and coming to my conclusions.

I hope you see that in every recommendation I make, including the ones below.

You Can't Cure Cancer on the Couch

Alexandria Real Estate ( ARE ) is a life science REIT that owns campuses in "innovation cluster locations" such as Greater Boston, the San Francisco Bay Area, New York City, San Diego, Seattle, Maryland, and Research Triangle.

The S&P 500 REIT has over 800 tenants with an asset base 75.1 million SF which includes 41.5 million RSF of operating properties and 5.6 million RSF of Class A/A+ properties undergoing construction, 8.9 million RSF of near-term and intermediate-term development and redevelopment projects, and 19.1 million SF of future development projects.

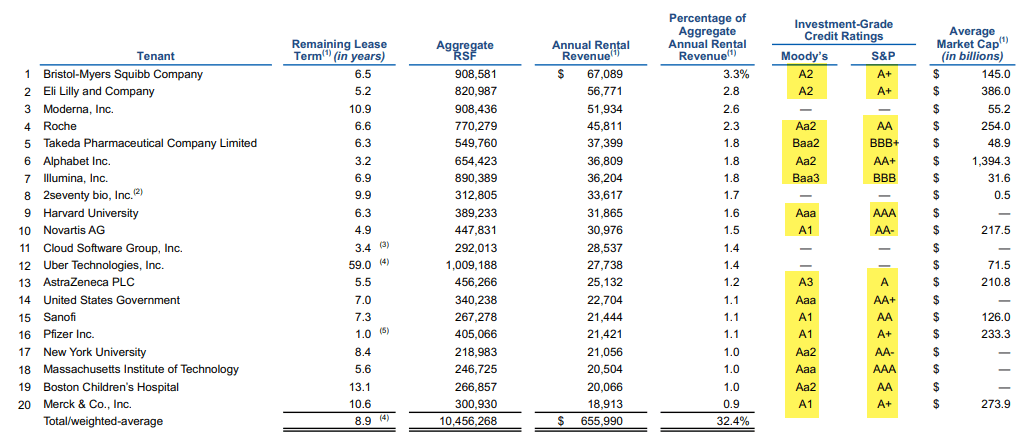

As seen below, 91% of ARE's top 20 tenants' annual rental revenue is generated from investment-grade or publicly traded large-cap tenants:

{kind=link}

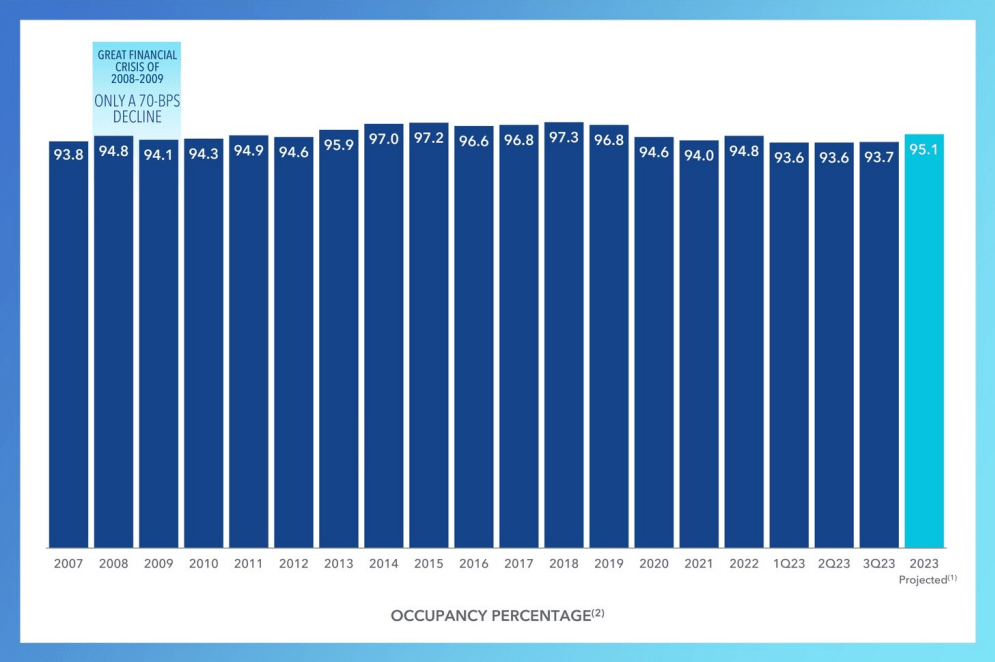

As of Q3-23 the occupancy percentage of ARE's operating properties was 93.7% and the 10-year average occupancy percentage was 96%.

ARE's occupancy is projected to be 95.1% at the end of 2023 (this implies 140 bps increase).

{kind=link}

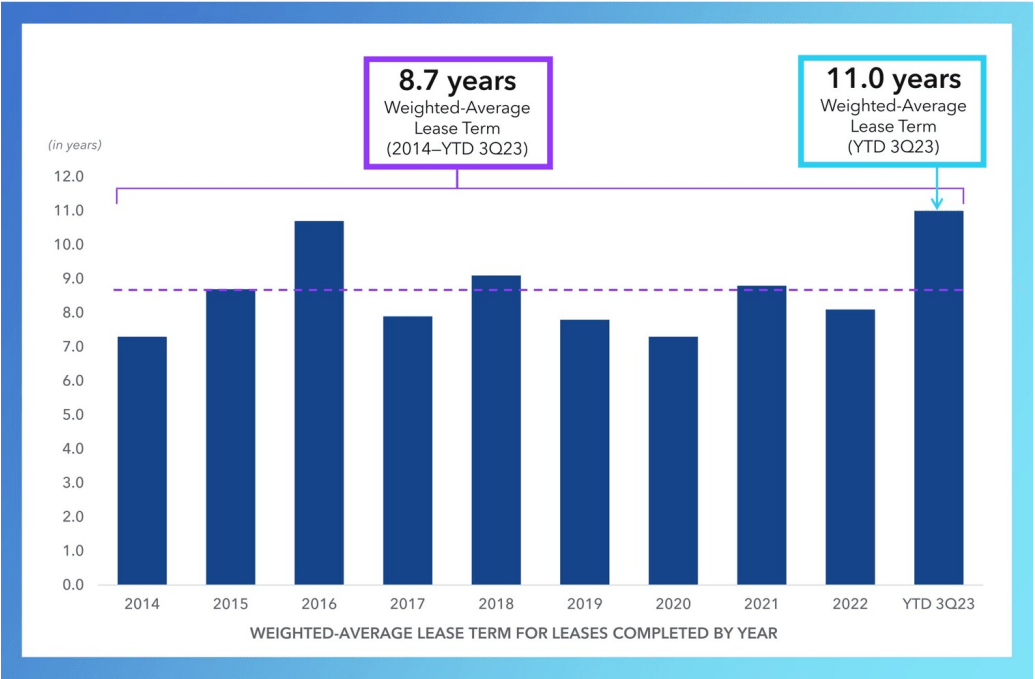

In addition to a diversified and stable income stream, ARE also enjoys long-duration leases - the weighted average lease term is ~11 years which significantly exceeds the weighted average lease term since 2014 of 8.7 years.

{kind=link}

ARE's balance sheet is in excellent shape with $5.9 billion of liquidity (as of Q3-23) with no debt maturities until 2025. 99% of ARE's debt is fixed rate with an average interest rate of 3.7%.

The company enjoys solid investment grade ratings (BBB+ and Baa1) from S&P and Moody's. Through Q3-23 ARE had $875 million of dispositions completed and another $699 under LOI to close in Q4-23.

{kind=link}

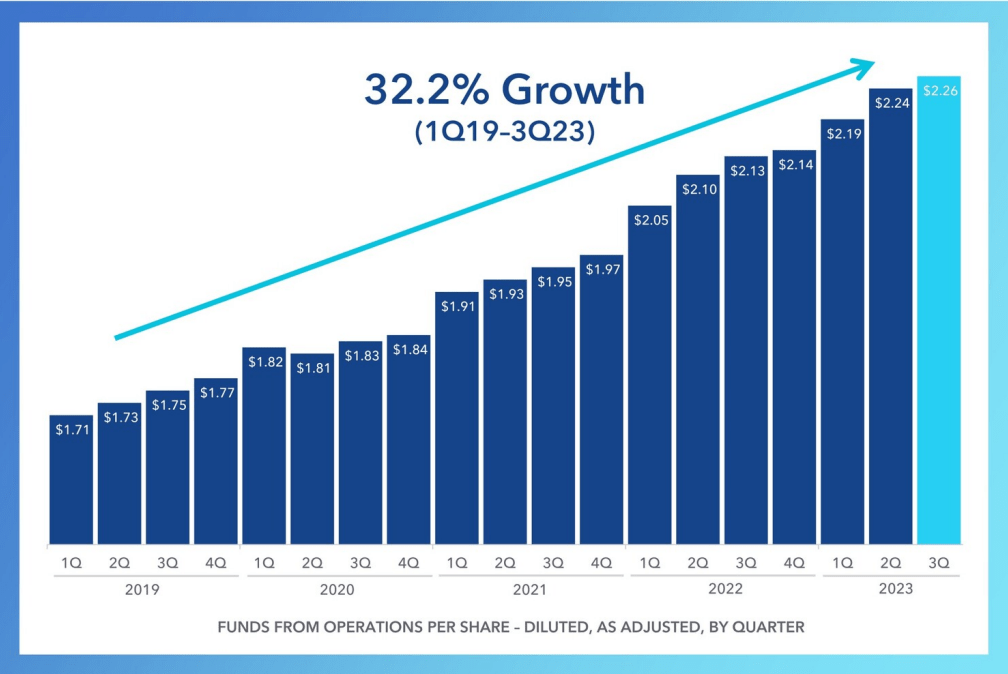

ARE has generated steady earnings growth (as shown below): FFO per share has averaged 7.5% annually over the last decade.

In Q3-23 FFO was $2.26 per share, up 6.1% from Q2-22 and the company said it was on track to deliver FFO per share growth of 6.7% in YE 2023 (midpoint of guidance).

{kind=link}

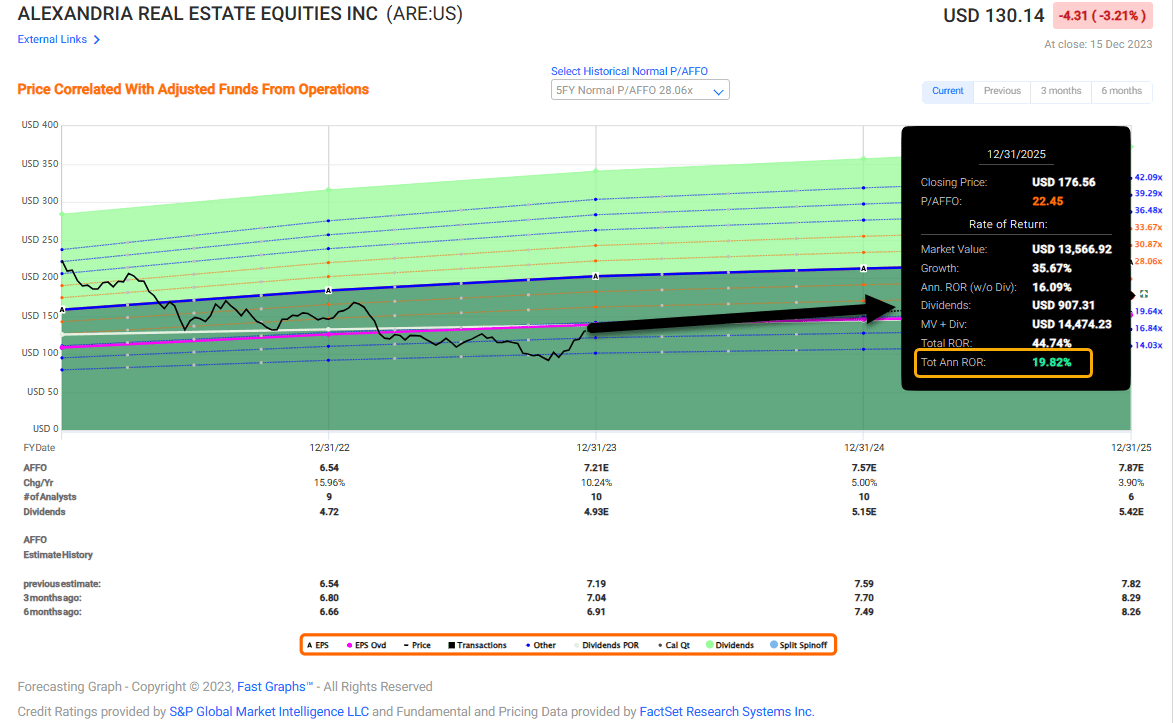

Although I'm +12% with my stake in ARE, I'm still buying. Shares today trade at $130.14 with a P/AFFO multiple of 18.1x, well below historic levels (normal is 12.6x). The dividend yield is 3.9% with a modest payout ratio of just 68%.

Analysts forecast growth (based on AFFO) of 5% in 2024 and 4% in 2025. That's a little less than historical growth (of around 7% per year) but the shares remain cheap and iREIT® forecasts shares could return another 20%.

{kind=link}

I'm Warming up to COLD

Americold ( COLD ) is an industrial REIT focused on temperature-controlled warehouses in North America, Europe, Asia-Pacific, and South America.

The company owns and operates 243 properties (195 owned, 43 leased, and 5 managed) with total capacity of 1.5 bn cubic feet (45.7 mm square feet). The average size of a COLD facility is 188k square feet.

COLD has an enterprise value of $10.8 billion with a $7.7 billion market cap. COLD's revenue breakdown is as follows:

- Warehouse 89%

- Transportation 10%

- Third-Party Managed: 1%

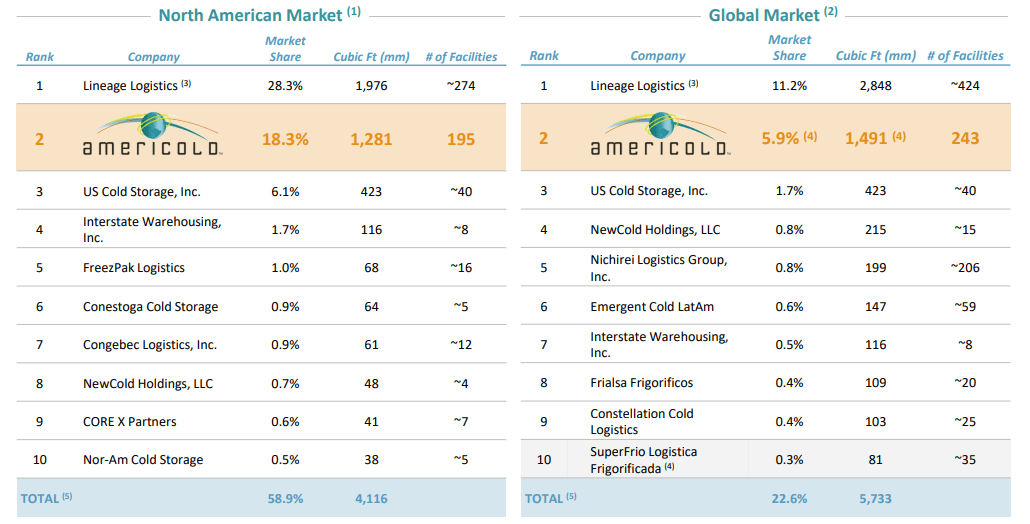

COLD owns mission-critical infrastructure assets that generate rent and storage income. As seen below the company is a global market leader with tremendous economies of scale advantages as seen below:

{kind=link}

In Q3-23 COLD's same-store economic occupancy increased to 84% (345 bps increase over last year) and +80 bps from Q2-23. Also, COLD generated 50.4% of rent and storage revenue from fixed commitment storage contracts (187 bps higher than Q2-23) and maintained a low churn of just 3.2%.

COLD's diversification helps reduce revenue volatility associated with seasonality and changing commodity trends. As seen below, ~79% of revenue comes from food manufacturers and ~19% from retailers.

COLD IR

COLD has long-standing relationships with top 25 customers which positions the REIT to grow market share organically and through acquisitions. Of the top 25 customers:

- Have been with Americold for an average of ~36 years

- 15 customers are investment grade

- 100% utilize multiple facilities

- 100% utilize technology integration

- 92% utilize value-add services

- 96% utilize committed contracts or leases

- 72% are in fully dedicated sites

- 60% utilize transportation and consolidation services

COLD IR

Recently COLD completed or is in the process of stabilizing $472 million of development projects in

- Auckland, NZ

- Lurgan, Ireland

- Calgary, Canada

- Dunkirk, NY

- Dublin, Ireland

- Barcelona, Spain

- Lancaster, PA

- Gateway, GA

- Russellville, AR

- Spearwood, Australia

These projects are estimated to generate $53 million in NOI.

COLD has two projects under construction (in Plainville, CT and Allentown, PA) at a total cost of approximately $260 million. The current development pipeline is approximately $1 billion, and the company has 730 acres of excess developable land.

At the end of Q3-23 COLD had total debt outstanding of $3.2 billion with total liquidity of $824 million consisting of cash and revolver availability. The net debt to pro forma core EBITDA was approximately 5.7x.

COLD has investment grade ratings from Fitch (BBB), Morningstar (BBB), and Moody (Baa3). As seen below, there are no material debt maturities until 2026.

COLD IR

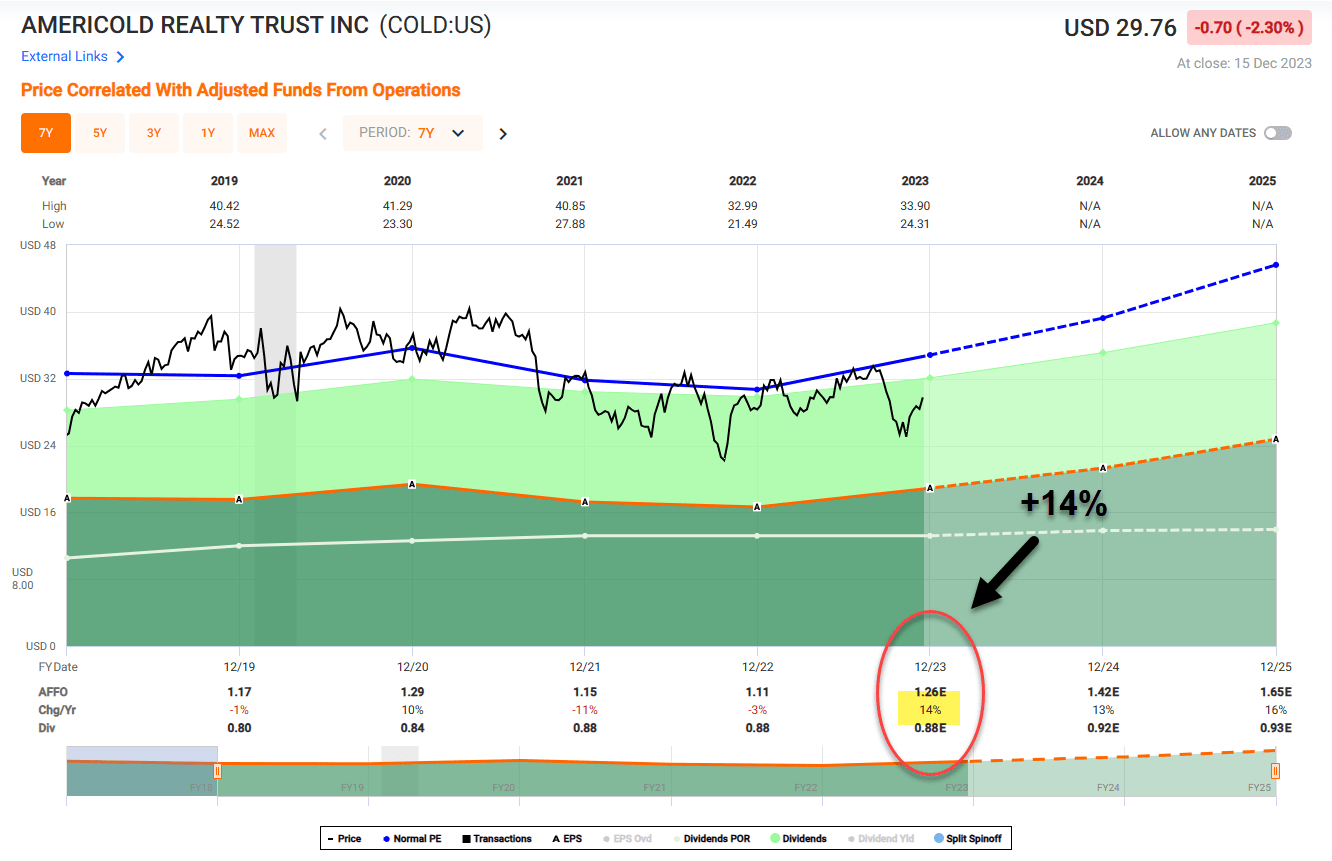

In Q3-23 COLD delivered AFFO per share of $0.32, an increase of over 10% versus Q3-22. This performance was driven by the global warehouse business which generated NOI growth of 5.3% (vs Q3-22).

Also in Q3-23 COLD tightened its full year 2023 AFFO per share guidance to a new range of $1.24 to $1.30, an increase of $0.02 at the midpoint. As viewed below, $1.26 (midpoint) represents year-over-year AFFO per share growth of 14%.

{kind=link}

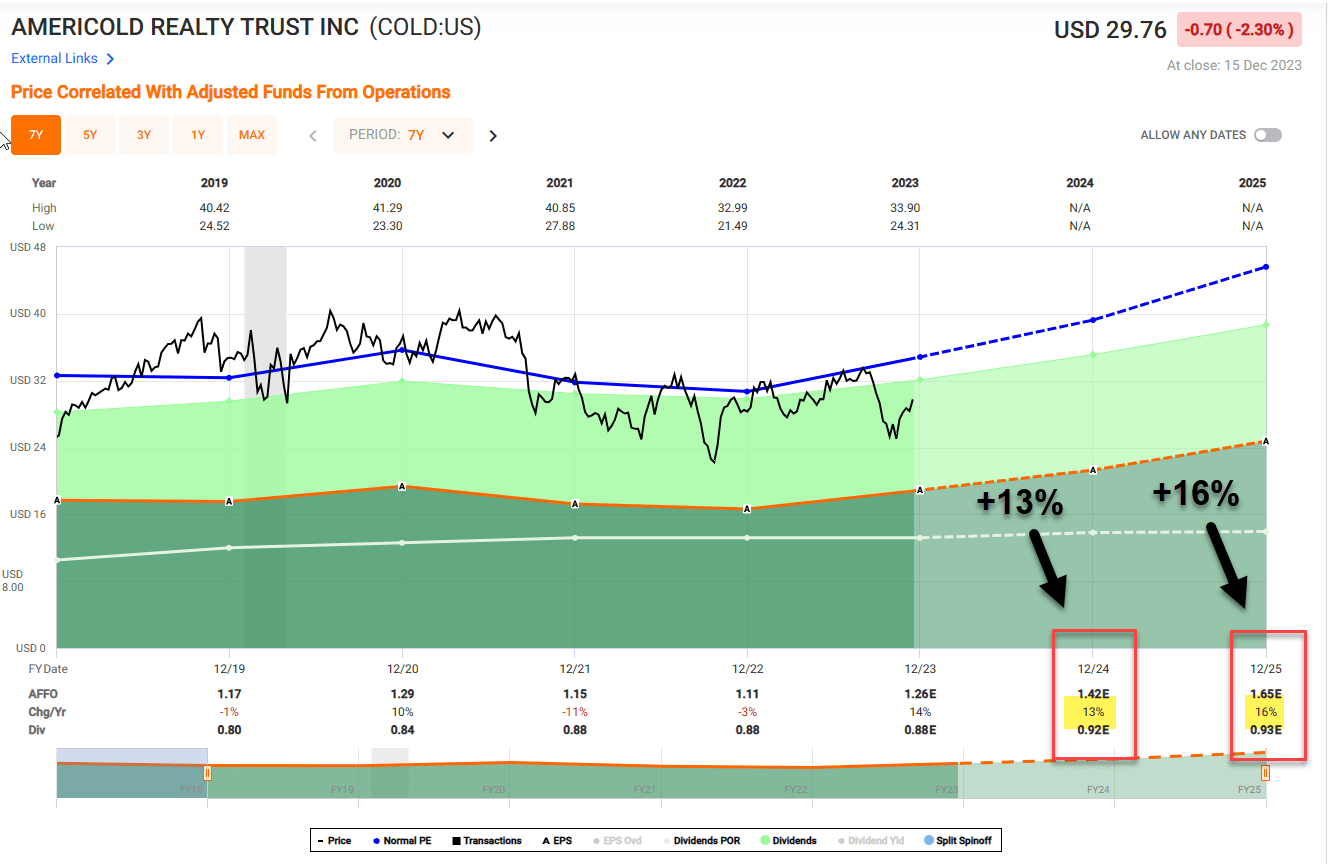

Analysts forecast AFFO per share of 13% in 2024 and 16% in 2025:

{kind=link}

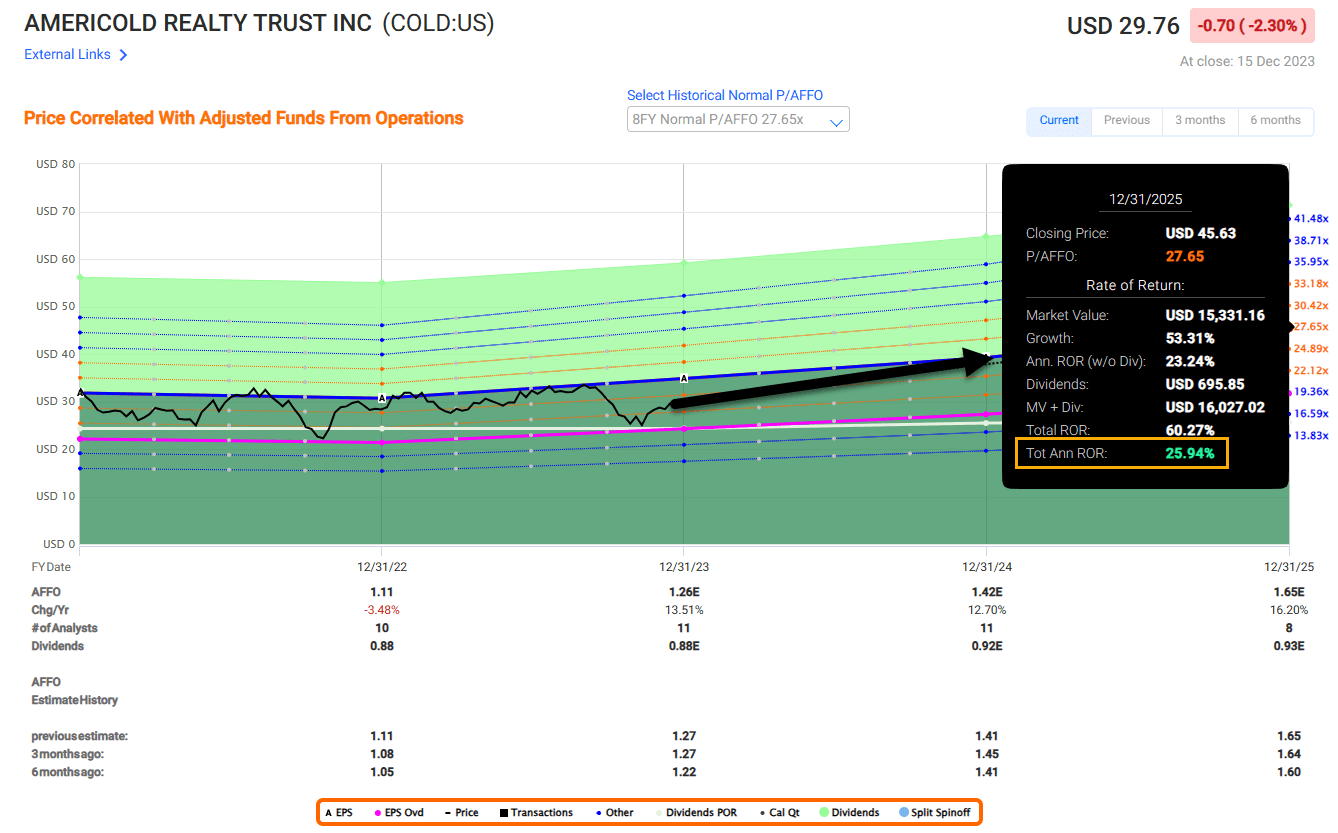

As I've pointed out to members at iREIT® on Alpha, I've been buying up shares in COLD (basis: $28.75) and I'm continuing to buy more.

Shares are now trading at $29.76 with a P/AFFI multiple of 23.7x (normal is 27.7x). The dividend yield is around 3.0% with a payout ratio of ~70%.

COLD is now around 1.5% of my portfolio (REITs and non-REITs) and I'm targeting exposure to max out at 4% by the end of this year.

{kind=link}

In Closing

I've been extremely happy with my investment in Digital Realty ( DLR ): I have over 5% exposure (REITs and non-REIT holdings) and shares have returned around 37%.

Similar to the two names that I just mentioned (ARE and COLD), DLR also has "mission-critical" properties.

Of course, Digital Realty's "mission critical" properties are also "mission critical" to artificial intelligence.

According to Forbes , " generative AI data center server infrastructure plus operating costs will exceed $76 billion by 2028 " and this cost " excludes the cost of the data center building structure but includes labor, power, cooling, ancillary hardware, and 3-year amortized server costs ".

Forbes

In other words, data centers are mission critical!

In short, all three of these REITs have "moats" that differentiate their business models and should provide continued pricing power because of their relevant scale advantages.

I consider DLR "soundly" valued today, however, ARE and COLD are unique REITs that I'm adding to my intelligent REIT portfolio . As I said earlier:

AI should be a useful tool, not a substitution for good old-fashioned human reasoning."

Happy REIT Investing!

For further details see:

Don't Fall Prey To The Dark Side Of AI, Buy These REITs Instead