RISR - Don't Hold Gold Through Inflation Buy These Instead

2023-11-21 03:26:55 ET

Summary

- Gold's relationship with inflation is weak, suggesting it may not be the best hedge against inflation.

- Investors should consider alternatives such as interest-only mortgages, newly issued MBS, managed futures, and commodities carry to benefit from rising rates and persistent inflation.

- Gold may not outperform these alternatives in capturing inflationary pressure.

Introduction

Shares of the SPDR Gold Shares ETF ( GLD ) represents physical gold bullion held under the Thames River in the Bank of London's vaults. This is the best way for investors to access liquidity in the physical gold market, through ETFs like this and others such as Sprott's ( PHYS ) or iShares' ( IAU ).

Gold has long been seen as an asset that can stand alone from commodities. It reacts differently than the rest of the commodities markets to changing market conditions. You can spot the difference most prominently during market crashes as a "flight to safety." You can also see gold's performance against several other asset classes in Figure 1, below.

Gold is also prized as an asset because of its ability to separate itself from the value of the dollar. This has given many investors the idea that gold can be a safe haven from not just crashes, but also changes in money supply that lead to inflation.

Gold & Inflation

Gold is not like other productive assets like equity where we can assume it will generate value on its own. Instead, holding gold is speculative. The price does not necessarily go up without the extrinsic value of gold (the investment premium above its value to producers) also rising.

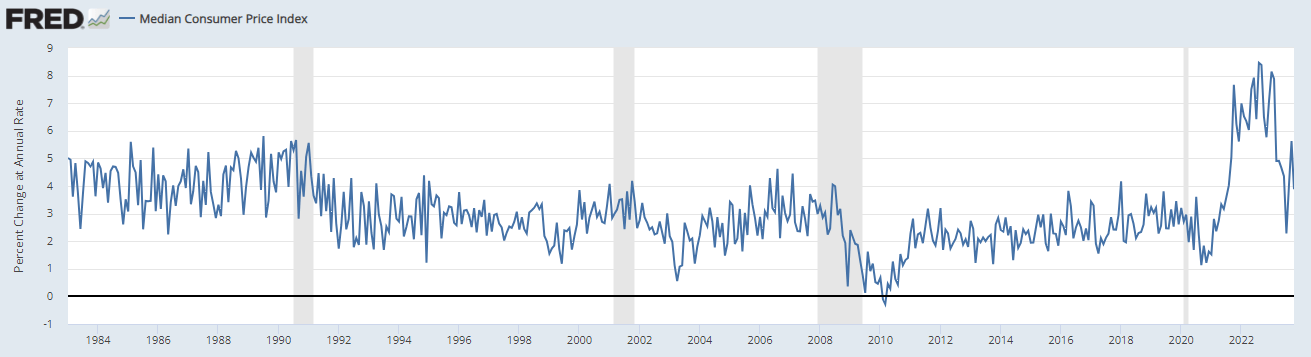

One of the drivers of the gold thesis is the US' current inflation problem, as gold has a reputation for benefiting when there is unexpectedly high inflation. It looks really dramatic when you use the median CPI.

{kind=link}

Figure 2 (FRED)

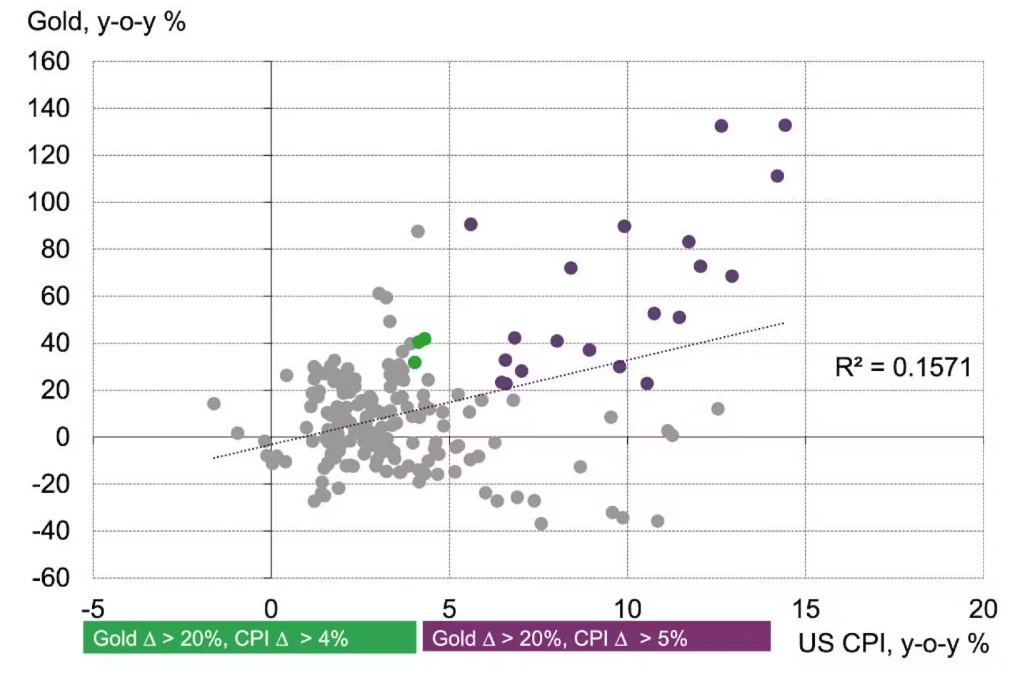

However, this isn't necessarily new, but there has been a fair bit of empirical work done on gold's poor relationship with CPI.

{kind=link}

Figure 3 (Reuters)

The figure above shows quarters of both high inflation and gold appreciation, and the correlation is positive but very weak at 0.16.

Gold's returns during periods of high inflation are not consistent, either. The purple dots in Figure 3 are all from 1973 to 1980.

{kind=link}

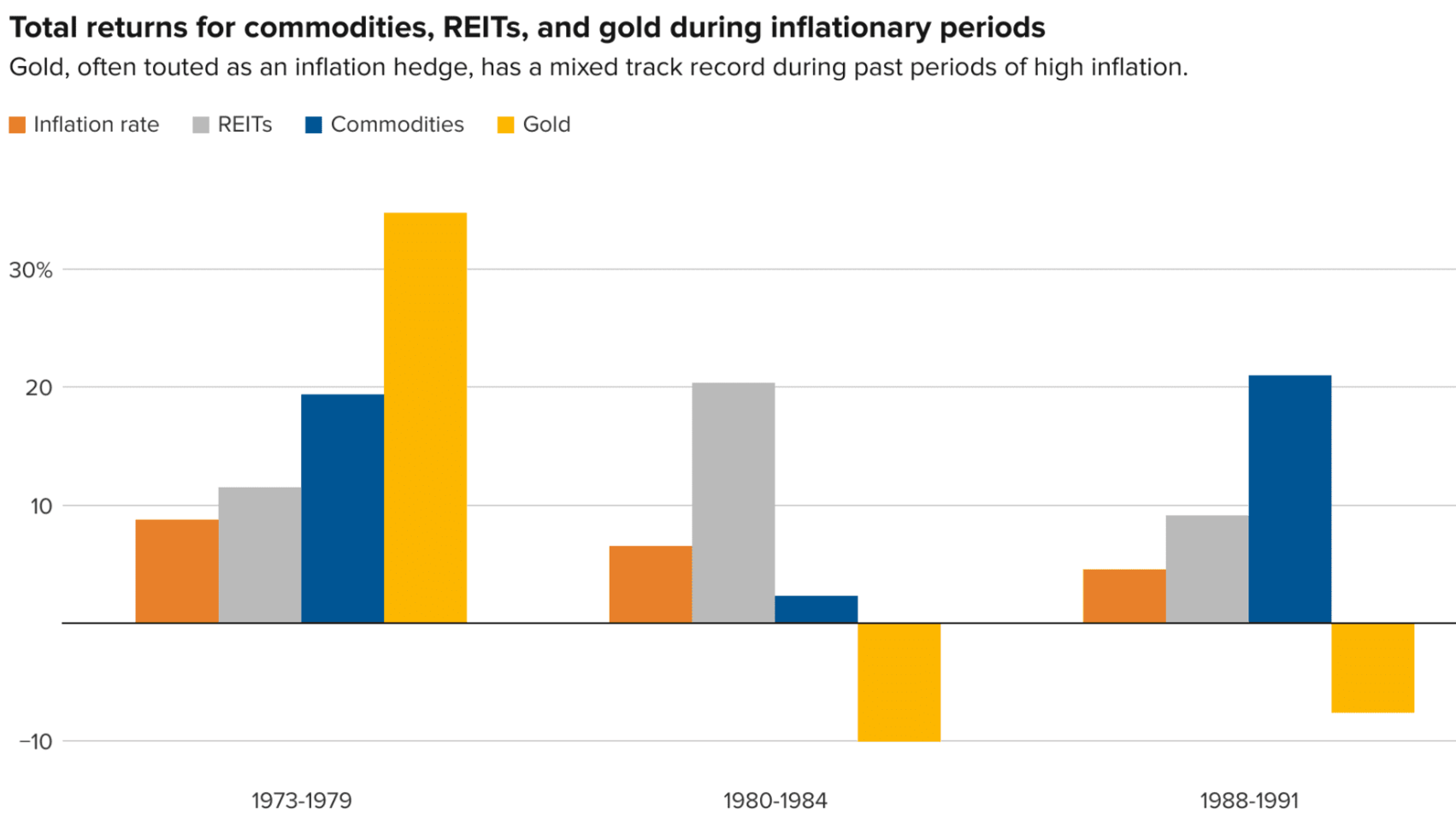

Figure 4 (Morningstar)

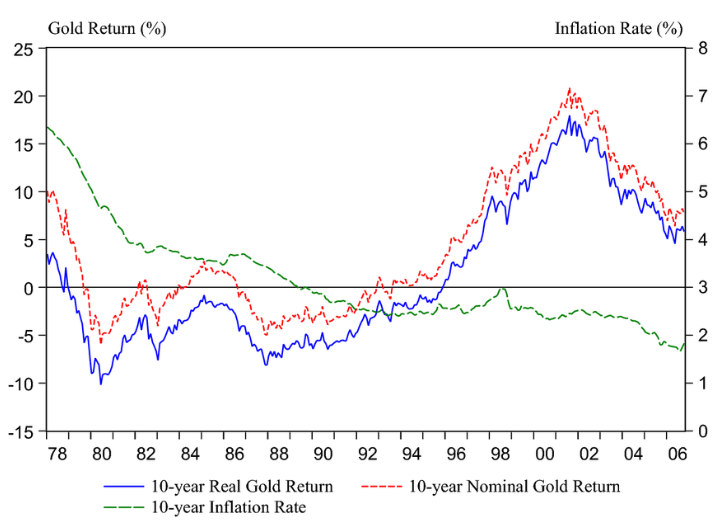

Even zooming out to larger periods of inflation, such as Figure 4, doesn't help much. When TIPS were introduced and inflation-protected bonds became more liquid, inflation expectations were easier to gauge and manage; through the 90s, they stabilized.

{kind=link}

Figure 5 (FRED)

Gold's real return has only been positive since that change, which was good for gold investors as a whole.

With a low inflation rate, fiat money fully off the gold standard, and a consistent level of inflation that was easier to anticipate due to TIPS, holding gold since the 90s has had a very positive absolute return.

{kind=link}

Figure 6 (Empirical Economics)

I don't believe that inflation is starting to decelerate . The short-term narrative that drives gold prices out of fear is exactly that: short term. As inflation carries on, we shouldn't expect gold to outperform other alternatives designed to capture inflationary pressure.

Alternatives to Capture Inflationary Pressure

Investors today choosing to diversify assets for an equities portfolio may have overlooked bonds in the past due to prevalent low interest rates. Since this last inflationary episode has begun, rates have climbed and bonds now offer significantly more upside than they have in the last ten years.

Rates rise when inflation is high, so we can expect rates to stay at this level or around it so long as inflation remains persistent. To take advantage of this, investors are better off buying a productive asset like debt that will take advantage of the relatively high rates.

The FolioBeyond Alternative Income and Interest Rate Hedge ETF ( RISR ) invests in interest-only mortgage-backed securities (MBS IOs), carries a negative duration and has a current 30-day SEC yield of 7.61%.

The Simplify MBS ETF ( MTBA ) is incredibly new and invests in newly issued MBS, which provides higher coupons than the current MBS index, which is full of older mortgages purchased as low as 2.75%. We should expect to see a yield much closer to 7-8% once this fund is fully up and running. The man behind the strategy has been writing about this for a while now and has written fantastic articles breaking down the strategy. Check out Harley Bassman on his blog, Convexity Maven.

The KFA Mount Lucas Index Strategy ETF ( KMLM ) is a fund that offers exposure to an actively managed futures strategy, providing full exposure to trend-following and tactical allocation of commodities, currencies, and fixed income markets. The fund is allowed some leverage since it uses futures. This allows for the manager to overweight high conviction positions without underweighting others.

Alternatively to KMLM, another incredible managed futures fund without leverage is the iMGP DBi Managed Futures Strategy ETF ( DBMF ). This fund takes positions across commodities, equity indices, and currencies. This strategy, as well as KMLM, is designed to allow for both long and short positions, which should offer positive absolute returns if done well.

Our last contender is the iShares Commodity Curve Strategy ETF ( CCRV ), which takes the traditional commodities fund approach and applies an overlay that prioritizes positively yielding positions along the term structure (futures curve) of each of the ten commodities contracts it holds, weighted by liquidity and degree of backwardation (favorable positioning on the curve).

How have these alternatives dealing with rates and commodities stack up to plain old gold?

I am missing data for MTBA since that fund is so new. For now, we will have to wait on that one.

Conclusion

Gold's relationship with inflation is weak, but common investing narratives sell gold as a way to beat inflation. There are better alternatives for investors to consider, taking advantage of the high rates that inflation brings.

To this end, I have recommended several alternatives including interest-only mortgages, newly issued MBS, managed futures, and commodities carry. These strategies are better positioned to benefit from rising rates and persistent inflation than gold ((GLD)).

For further details see:

Don't Hold Gold Through Inflation, Buy These Instead