GRABW - DoorDash: Where Is The E-Commerce Delivery Industry Going In 2023

Summary

- DoorDash is a leading e-commerce delivery business, with over 50% market share.

- We believe market conditions in 2023 will harm delivery businesses due to a fall in discretionary income and continued inflationary conditions.

- The delivery industry is highly competitive. We expect opportunities such as Robot delivery but the medium-term looks difficult with margins tightening, due to restaurants and consumers demanding better pricing.

- DoorDash is the least loss-making of a loss-making bunch. The business is more profitable on every metric and more conservatively financed. The issue is profitability is not certain in the future.

- We see no catalyst for positive price action but many risks that could bring a bearish eye over the business. It is currently priced at 3x revenue, but we see fair value closer to 2x.

Company overview:

DoorDash, Inc (DASH) operates a logistics software platform that connects merchants, consumers, and drivers internationally, with the majority of its services being based in the US. DoorDash operates through an e-commerce Storefront, which allows merchants to offer consumers food for delivery. Further to this, DoorDash Drive is a logistics delivery platform and DoorDash marketplace provides merchants data and analytics for order processing.

DoorDash is one of many businesses which have sprung to prominence in recent years, as a natural innovation in convenience. The industry is highly competitive globally, with many large players. Given the nature of the industry, requiring driver footprint to increase usage, we have seen a degree of consolidation. The largest two deals were the acquisition of Just Eat in the UK for $8.3BN and Grubhub for $7.3BN.

The following chart illustrates the current state of play in the e-commerce delivery business, with incredible value destruction v. the S&P. The reason for this has been a difficulty many tech businesses face when transitioning from revenue acquisition to profitability.

Many are speaking of Tech as a great investment area in 2023, following the sharp decline in share price. We will look to assess the delivery market as a whole, with an overarching eye on the economy, before turning our focus to DoorDash's performance so far.

Macro-economic consideration:

We will begin this paper with an overview of current macro conditions, as this will provide context for the basis of our near-term performance expectations.

During COVID-19, many were locked away at home but found themselves with greater net cash. This is because any reduction in cash was compensated by the lack of "outdoor" spending. For this reason, we saw the use of delivery services increase quickly ( sales doubling ). It was truly the perfect industry for such unusual times. Following the end of lockdowns in most countries, demand continued to remain heightened.

Conditions began to reverse quite quickly in 2022 with slowing demand and growing inflation. The contributing factors to inflation include the Russian invasion of Ukraine and supply chain issues. During the year, interest rates increased in order to combat this and cool demand. In the US, there is some evidence to suggest this has worked, with successive quarters of inflation decline . Other nations, including the UK, have not been so lucky.

Going forward, it is likely that demand will continue to fall in 2023 as interest rates continue to increase, as a <5% inflation rate continues to be the target. This will almost certainly trigger a recession in many countries, with a cost-of-living crisis in full swing.

For many, spending on take-out food is discretionary and is fairly elastic in demand. For this reason, if economic conditions deteriorate further, it is likely that demand in the industry will fall. In addition to this, it will likely trigger greater competition, as market incumbents look to take market share when competitors are weakest.

Therefore, when looking at DoorDash, we must consider that on a like-for-like basis, demand will almost certainly slow further into 2023. What we will then be looking for is evidence of greater efficiency, which has the ability to minimise the impact of this.

E-commerce delivery industry:

Overview of the current industry and outlook:

The E-commerce delivery space has seen an astounding rise to prominence, with growth in all corners of the earths. The economics of the service are fairly simple. These businesses charge the restaurant a small fee for every transaction and for advertising if they desire. They charge consumers for delivery, as well as additional surge fees where applicable (e.g., minimum orders). In exchange, consumers can now eat at home and do not need to go to a location to pick up, ultimate meal convenience.

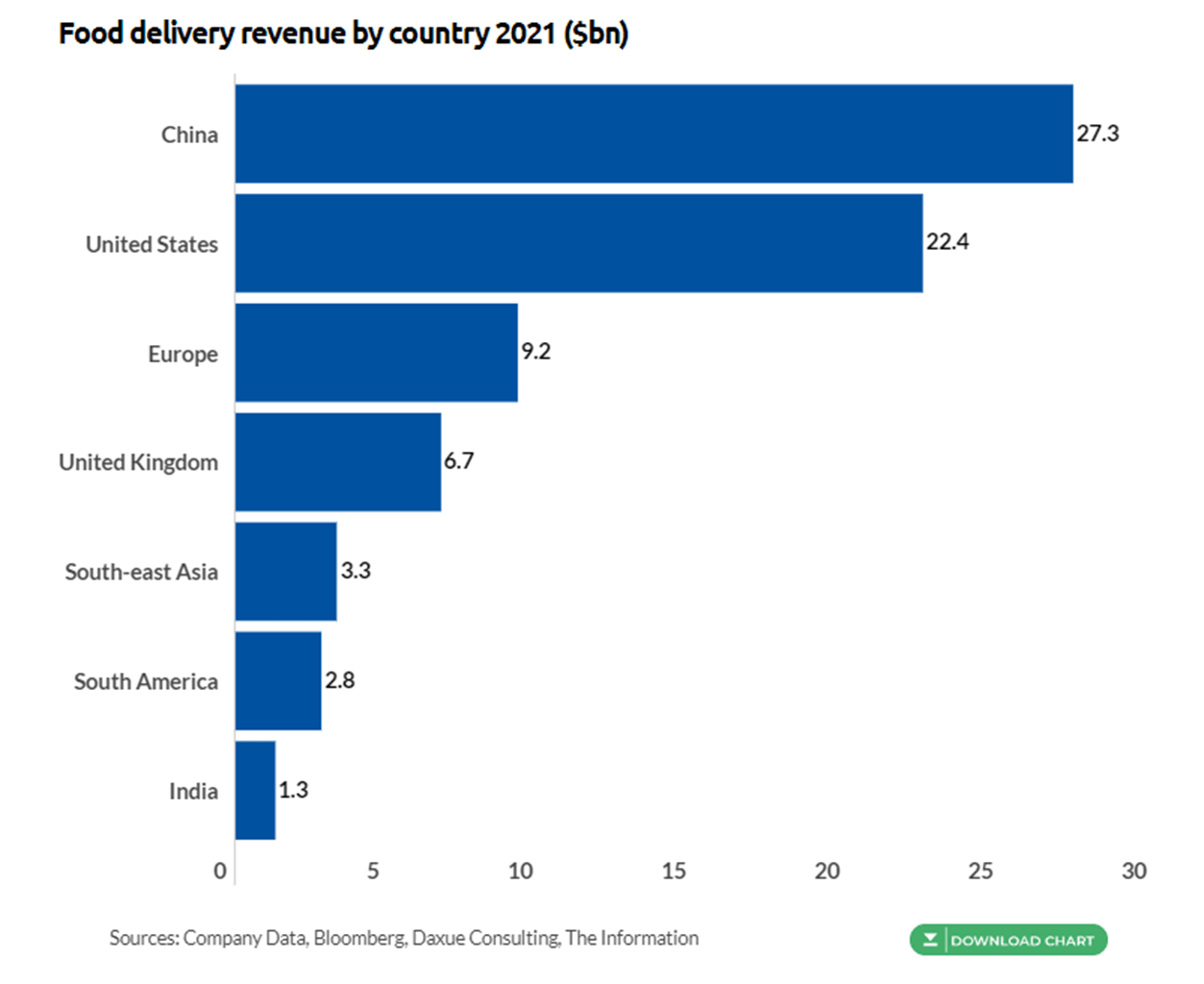

When we look at the revenue split by region, we see a diverse list.

Food delivery revenue by region - 2021 (BusinessofApps)

{kind=link}

This reflects the universal demand for this service, which is genuinely adding value to consumers.

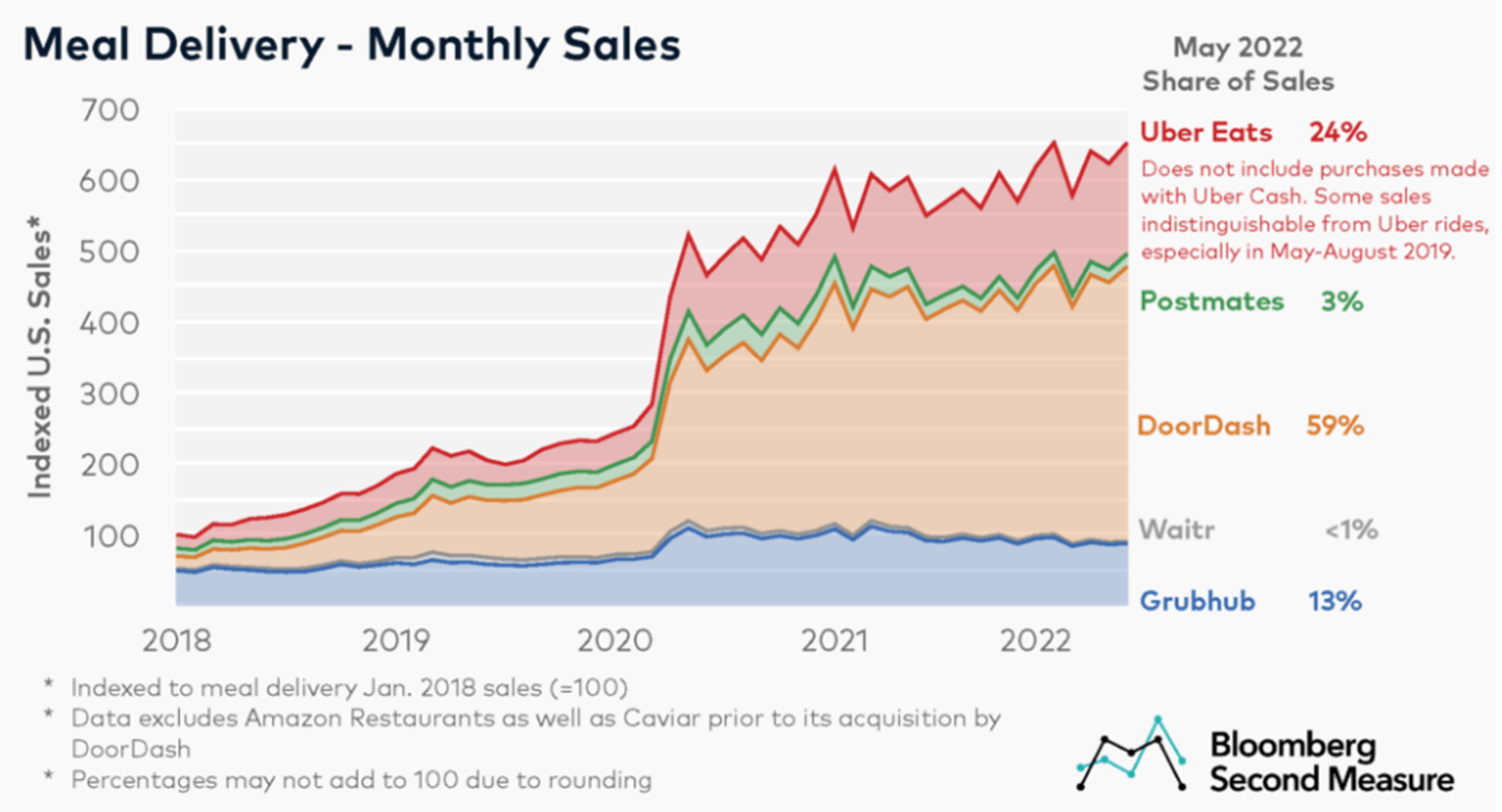

DoorDash primarily operates in the US market, within which they are market-leader, with around 59% market share.

Meal delivery market share - US (Bloomberg)

{kind=link}

DoorDash was not the first in the market but was able to grow quickly due to a superior strategy . They would focus on suburbs and restaurant selection v. cities and speed. They were able to identify that people did not care too much about speed if it came in a reasonable time and they knew that expanding in the city would be the most difficult. They understood it would be smarter to wait till the brand was established before moving into cities.

The US market is highly competitive, similar to other countries, with competition stemming from selection and price.

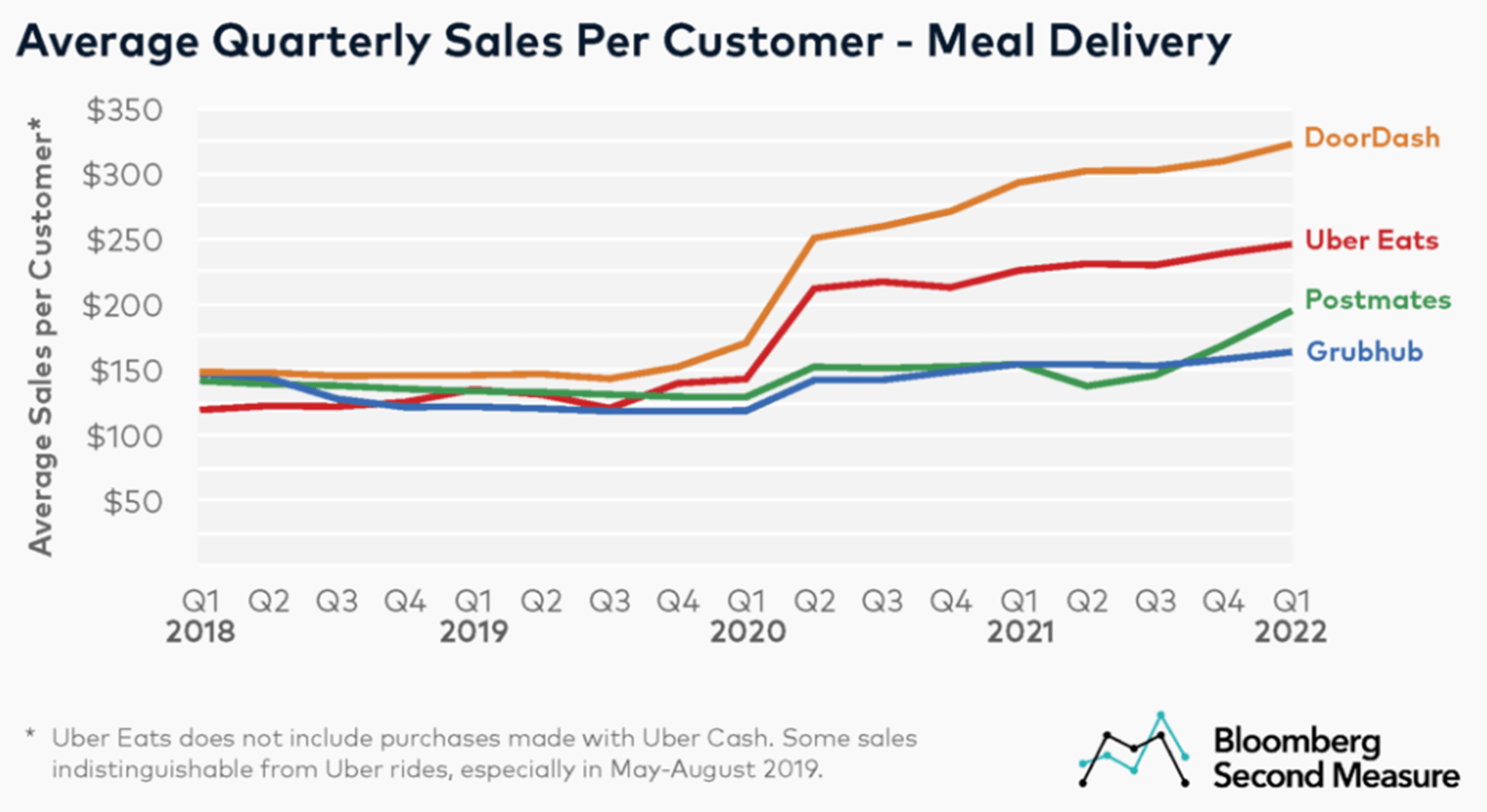

This selection point is important as consumers are willing to spend more if they are getting exactly what they want. One would expect that the average sales by customer is relatively uniform in the market but it's not, DoorDash massively outperforms. This suggests that their offering has consumers coming back for more far more regularly.

Avg. quarterly sales per customer (Bloomberg)

{kind=link}

Going forward, Grandview Research believe the market can growth at a CAGR of 18.7%. They believe the driving force of this will be further digitalization in society, as well as development in the services offered beyond just restaurant food.

When conducting research into the market, we observe the following themes.

Partnerships:

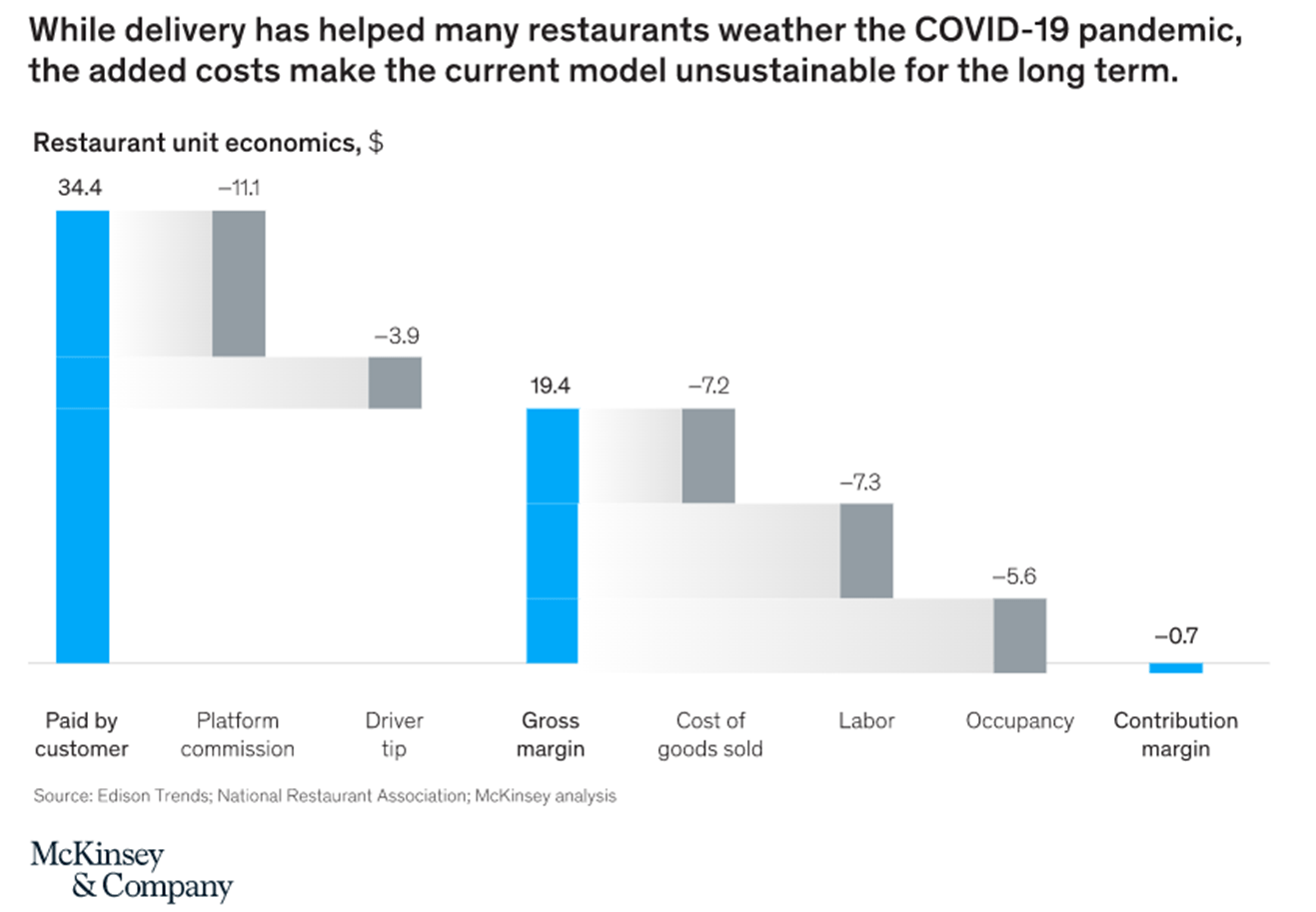

Developing relationships with restaurants is vital in this industry and is something which DoorDash has focused on from early. According to an article written by Janine Perri, both Chipotle and Cheesecake Factory have publicly credited DoorDash for increasing their sales, with 11% of Chipotle's sales coming from DoorDash. This is an example of a positive relationship, but some restaurants are unhappy with the current pricing model. Deliveries are eating into their margins and potentially cannibalizing their in-person sales, which are higher margins. As McKinsey illustrate, the current pricing model is unsustainable.

Restaurant unit economics (McKinsey)

{kind=link}

For this reason, we could see restaurants leverage the competition in the delivery space to negotiate better platform commissions. Regardless, it is likely that we have seen the top of what delivery companies can charge restaurants as commission.

Price justification:

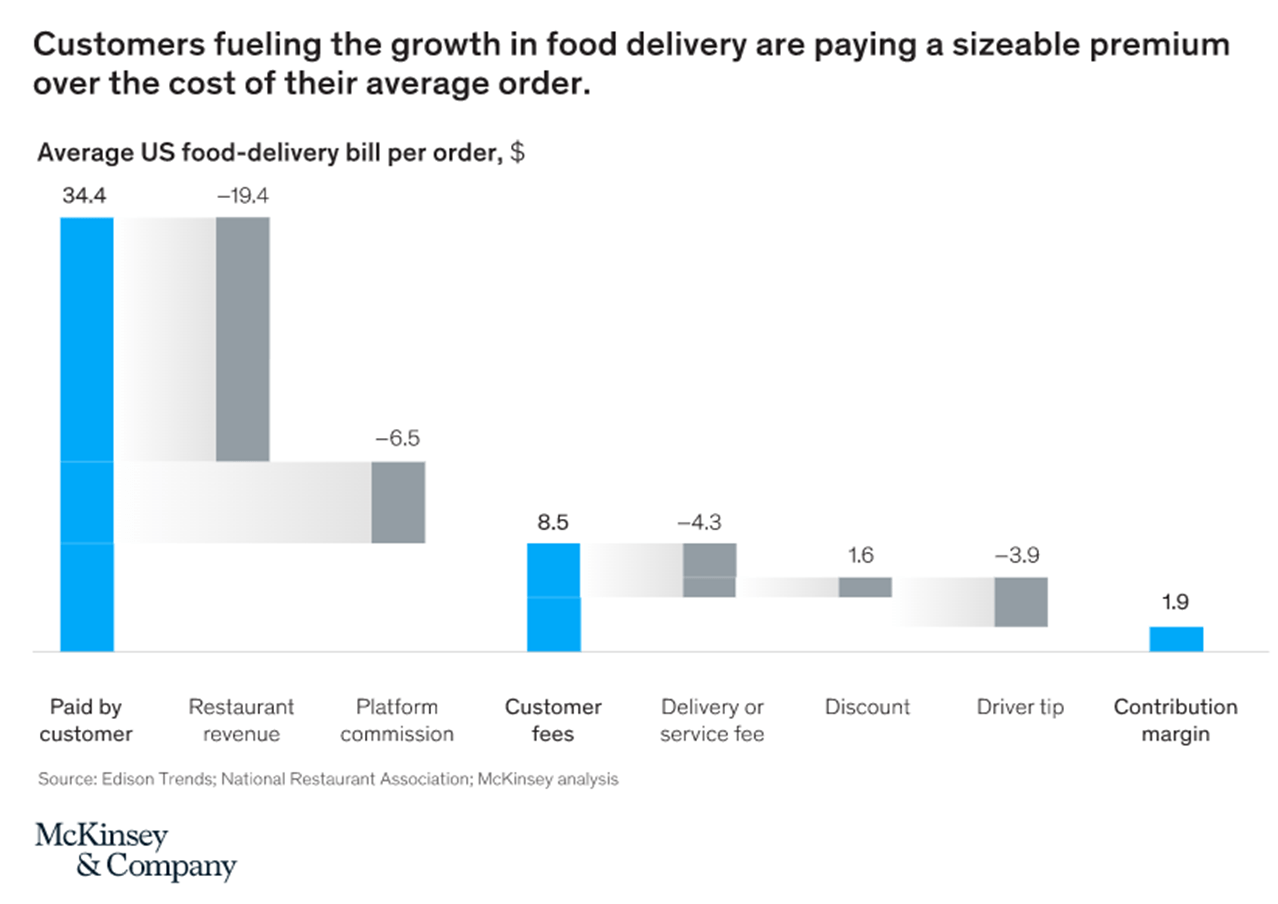

Consumers are currently paying a sizeable premium compared to restaurant prices for the convenience of this service. initially and during COVID-19 this was not an issue, but we are seeing slowing demand and consumers seeking cheaper prices. As the following diagram from McKinsey shows, consumers are paying far more than the actual price of the good, in order to fund the delivery businesses growth strategy.

Consumer premium economics (McKinsey)

{kind=link}

As the market begins to mature, consumers will demand that prices fall in order to retain their business. Delivery businesses can either seek to be more efficient, which looks unlikely given the diagram above, or improve the service they provide.

Range of services:

As mentioned above, the pricing model is unattractive, which is deterring some customers and could mean issues in the future with margins. In order to combat this, some businesses are developing further complimentary services to bundle alongside it. As an example, GRAB offer taxi and grocery services also, acting as a superapp.

Offering multiple types of services (beyond deliveries) is not something DoorDash currently offers but could become a necessity in the future, especially if subscription models which bundle services become the normal. Currently, we see this as an opportunity more than a threat, given the "superapp" concept's infancy in the US.

Subscription models:

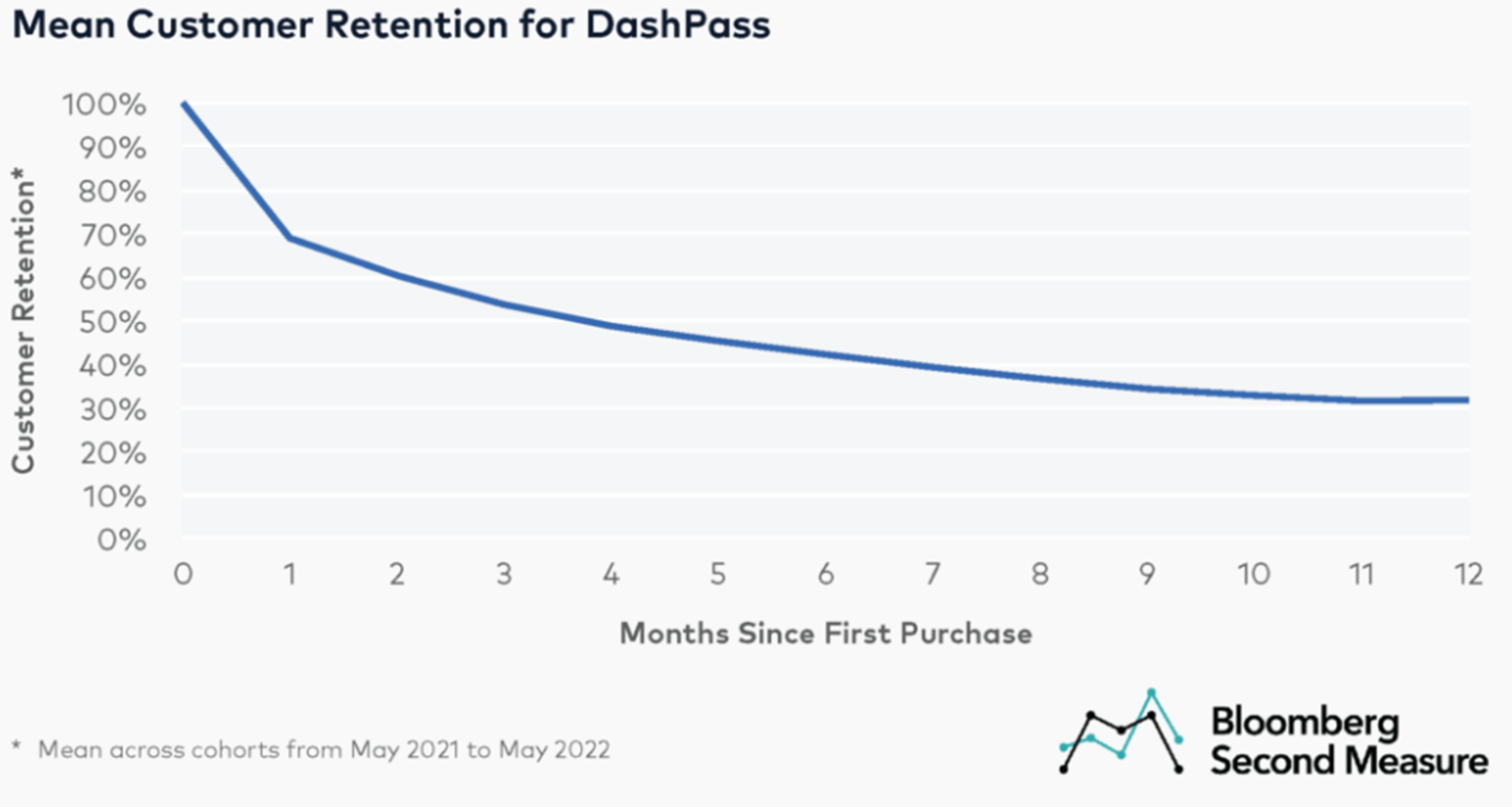

One of the major issues in the market is that consumers do not care which app they use, as long as it gives them what they want. For this reason, businesses are focusing in varying amounts on delivery, range of services and selection. With much consolidation seen in recent years in order to combat weaknesses. In order to create some stickiness, businesses have created subscriptions, providing customers with such things as free delivery in exchange for a monthly payment. This is a smart and natural development as it exchanges one fee (delivery for example) in order to generate greater orders and create stickiness. Consumers are saving money on delivery so are likely to order more, DoorDash make up the lost delivery in greater take from restaurants plus the subscription amount.

DoorDash's retention has been moderate, with 30% of customers staying for at least 12 months. Given that these subscriptions usually come with sign-on bonuses, seeing a large initial drop-off is expected.

DoorDash customer retention (Bloomberg)

{kind=link}

Route to profitability:

The final theme is one which wraps up what we have discussed so far succinctly. One would think that these factors have led to highly profitable delivery companies, but it has not. Every single major player is loss making on the bottom-line, with no profits in sight.

Based on our points made above, gross profit margins will likely contract in the medium-term, as restaurant commissions are reduced and / or prices charged to consumers falls. Given that we are in an inflationary environment, both factors are less likely to occur now.

Profitability will likely come from innovation and the other two points mentioned above. The use of robots could allow for human-less delivery, thus significantly reducing marginal costs. Further, the bundling of similar services into a subscription model could entice recurring monthly revenue, should the package justify the price. Again, this will trade a small revenue source in exchange for the recurring income and volume.

Having said all this, is profitability around the corner? No. We cannot see how any of these factors will improve margins to the level required within the next three years. That said, the market does show opportunities for growth, alongside evidence that maturity is soon to come.

Financials:

DASH - Financials (Tikr Terminal)

DoorDash's financials look very good for a growing business. Revenue has grown at a CAGR of 114%, with growth between LTM Nov22 and FY21 still at a respectable 24%.

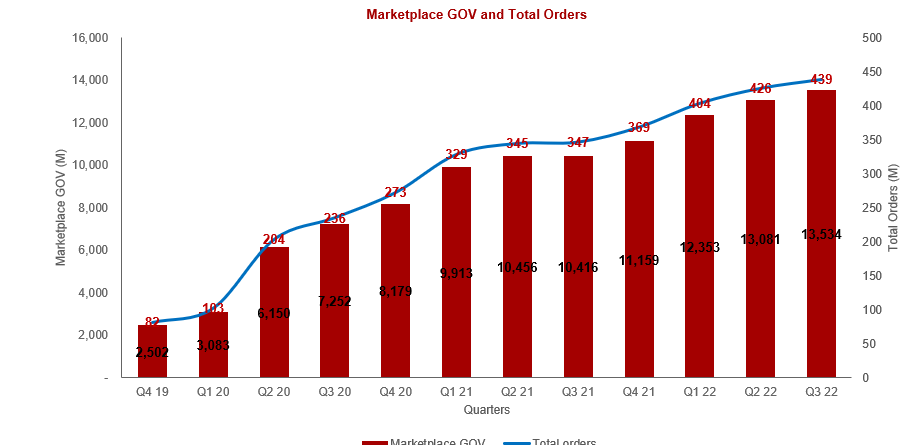

When looking deeper into sales generation, we observe a slowing of both Marketplace GOV and Total orders. The last quarter's growth was only 3%, which could mean Q1 or Q2 23 turns negative, which could act as a negative catalyst. We saw something similar with Netflix ( NFLX ) whose stock fell considerable when investors saw growth grind to a halt. With our expectation of slowing growth in 2023, we believe it is likely DoorDash will trade flat on the top-line annually but should avoid negative growth.

Marketplace GOV and orders (Q3 investor pack)

{kind=link}

Impressively, S&A costs are accretive having only grown 87% in the period relative to revenue, cementing Management's impressive razer focused strategy. Further, this is supported by record levels of subscriptions in Q3. Margins have improved across the historical period but look to be flatlining somewhat, suggesting they may have peaked. EBITDA margin remains negative due to stock-based compensation ($740M in the LTM period, c.$20BN market cap) but on an adjusted basis is positive and edging slowly upwards.

The company is also financed very conservatively, with little debt and FCF / CFO positivity, despite the negative accounting net income. Investors should not be concerned about solvency.

DoorDash's financials are reflective of the industry analysis we have conducting, showing what looks to be a quality growth business. The problem remains that profitability looks difficult to achieve and we may already be seeing signs that margins are tightening.

Peer analysis and valuation:

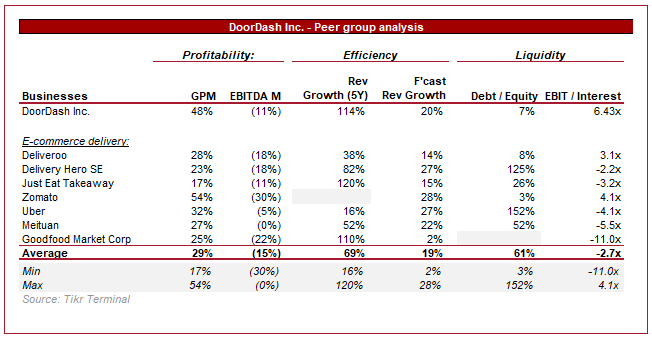

Peer group analysis (Tikr Terminal)

{kind=link}

When looking at DoorDash's peers, we observe the general industry characteristics. All businesses lack profitability but are growing quickly.

DoorDash looks further developed than its peers, boasting above average growth and margins. With consolidation and a movement to maturity in the coming years, it is likely some of these businesses will never see profitability, with DoorDash being one of the more likely ones. Being the market leader in the US supports the evidence that this is due to the quality of their offering, as opposed to an aggressive loss-funded growth. With the conservative funding noted previously, DoorDash is in a good position to gain market share through maintain marketing spending, while competitors may need to scale back as the cost of financing grows.

Our view is that DoorDash looks the most likely, alongside Meituan and Uber, to reach profitability first. They are the key market leaders globally and should attract a premium valuation.

Peer Group Valuation (Tikr Terminal)

When comparing DoorDash to its peers, the business looks to be trading at an average level. Even if we consider the average between Uber and Meituan, the revenue multiple is 3x.

The problem is that the whole industry is overvalued, especially going into 2023. Our slightly harsh view is that any business that we believe cannot achieve profitability should be valued at <1x revenue. If profitability is uncertain but possible, 1-3x is reasonable. In this case, the jury is out. Given our belief that margins will contract, and the market will weaken in 2023, we are closer to the 1x level than 3x. For this reason, we consider DoorDash overvalued.

Conclusion:

DoorDash is a marker leading e-commerce delivery business which has performed extremely well. The business has a strong Management team who have been able to sustainably grow the business, taking market share from competitors with greater resources. We are impressed by its FCF positivity and unit economics, which are best placed in the industry to transition to profitability.

However, we do believe the market will struggle in 2023, as economic conditions weaken, and consumers find themselves with less discretionary income. Further, we think the industry is moving towards maturity, with margins compressing due to both restaurants and consumers demanding better pricing.

For this reason, it is difficult to see what could initiate positive price action in 2023, with much that could easily cause bearish sentiment. This currently feels like a high-risk low reward play.

We have thus rated this stock a sell.

For further details see:

DoorDash: Where Is The E-Commerce Delivery Industry Going In 2023