BWLLF - Dorian LPG: Scrubber-Focused Fleet Loses Out On Narrowing Scrubber Spread

2023-09-13 05:28:44 ET

Summary

- Dorian LPG has had a fantastic year in a supply-constrained market, reaching strong freight rates.

- Its listing on the NYSE provides an availability and liquidity advantage over its main peers.

- However, there are indications that its share price is high, its availability advantage will disappear in early 2024, and its fleet profitability somewhat depends on the scrubber spread.

- While not necessarily a better choice than its peers, its ability to provide strong dividend yields looks set to continue in the current beneficial market.

Investment thesis

Dorian LPG ( LPG ) displays equally strong fundamentals as its two main peers, BW LPG (( OTCPK:BWLLF ) and Avance Gas (AVACF). It separates itself by being run by its founders - there have been almost no changes in the management team over the years, providing stability - and by being listed on the NYSE, a substantially more accessible and liquid exchange than the bourse its two peers are listed - the Oslo Stock Exchange. Its trading environment advantage will carry much less weight in early 2024 when its peer BW LPG completes its NYSE listing.

Its reliance on scrubbers makes it vulnerable to a narrowing scrubber spread but reduces complexity in managing the fleet. Like its peers, its ability to increase fleet size is constrained by new-build prices and long delivery times (yards can deliver new orders in 2027).

The market outlook has been strong for multiple quarters and still is. Supply constraints are likely to remain for some time still. These forces provide buoyancy for strong freight rates in the short to medium term.

Like SA Quant, I arrived at a hold rating for Dorian LPG. Its ability to pay substantial dividends remains, but its recent strong stock price development limits its upside potential.

This is the final article in a three-part series on VLGC pure plays Avance Gas , BW LPG , and Dorian LPG.

Company Overview

Dorian LPG, a VLGC pure play, was founded in 2013 and is managed by its founders. It started trading on the NYSE in May 2014.

It has 25 VLGCs in its fleet, of which four are chartered-in. The bulk of its fleet consists of scrubbers, along with four LPG dual fuel-capable vessels.

Fundamentals: Not Better, Not Worse Than Peers

Let's begin our review by considering trailing P/E and P/B ratios for Dorian LPG and its two main peers, BW LPG and Avance Gas.

Dorian is in the middle of the pack in terms of the P/E and the P/B ratios. Looking back three years, this sector's P/E ratio of about 5.6 is not exceptionally high.

However, Dorian and its peers have seen their P/B ratios reaching historical highs over the past six months. All three are trading at a premium to their book values. This does not necessarily mean that they are overvalued. Freight rates have been resilient this year, avoiding the usual seasonal dips. In addition, the Panama Canal delays have adversely affected LPG shipping, reducing the world fleet size. Finally, shipyards are sold out, indicating new deliveries only in 1H 2027. For two quarters running, these companies have been able to sell off old vessels at a premium to book value, indicating that the market value of their ships surpasses book value.

Let's consider the return on equity to get a check on the P/B ratio.

As we can see in the graph above, the return on equity is broadly similar for all three companies, especially during the past year - and increasing. This development validates the increased book values seen in the same period.

Turning our attention to the Debt to EBITDA ratio, we note the following:

Both Dorian and its peers have used the past year to deleverage and have reached a three-year low in terms of leverage. While Dorian and Avance employ almost the same leverage and have been for three years, BW LPG consistently runs a much lower leverage.

To conclude this section, let's consider the dividend yield.

Throughout 2022, Dorian LPG had payout ratios far exceeding its EPS, resulting in exceptionally high yields approaching 30%. Having reverted to the mean, Dorian has reached the same level as its peers, around 15%.

However, the graph above shows its peer, BW LPG, providing a yield of 20%. I suspect this has more to do with its recent dividend policy change. The board will consider "trading profit" instead of net profit when deciding on the dividend payout. I covered this change at length in a recent article on BW LPG. In the last quarter, trading profit was considerably higher than net profit, possibly skewing the dividend figure above. In other words, its dividend yield can be expected to be somewhat lower, probably approaching the level of its peers.

Valuation

{kind=link}

Share price development (Seeking Alpha)

Dorian is trading at its 52-week high, increasing 100% in the past year. Freight rates for VLGCs reached around $130,000/day in the week ending September 10, according to Fearnley's Fearnpulse . This is a robust level, and given the supply constraints outlined in the "market outlook" chapter below, I think rates will remain at these levels for some time. However, freight rates could not continue towards, say, $200,000/day, given the transient nature of the current supply constraints. Consequently, I believe Dorian LPG - like its peers - is close to its target price but could reach $30. One should instead consider its dividend outlook.

Company-specific factors

Fleet Composition: Different Propulsion Strategies

Dorian's fleet consists of 25 ships as of August 2023: 21 owned and four chartered-in vessels. Its last extensive new build program concluded in 2015, with 16 ships delivered during that year and one additional delivery in 2016.

Since then, it has contracted and taken delivery of one VLGC, the LPG dual fuel Captain Markos , of which delivery was announced on March 31, 2023. In addition, it has chartered three LPG dual fuel vessels during 2023.

The graph below shows its ship count by delivery year and ownership type. It also includes peers Avance Gas and BW LPG for comparison.

{kind=link}

Fleets by year of delivery (Fleet lists at each company's websites)

As in many areas of life and nature, the bell curve can also be overlaid here. The biggest part of their fleet was delivered around 2015 for all three companies.

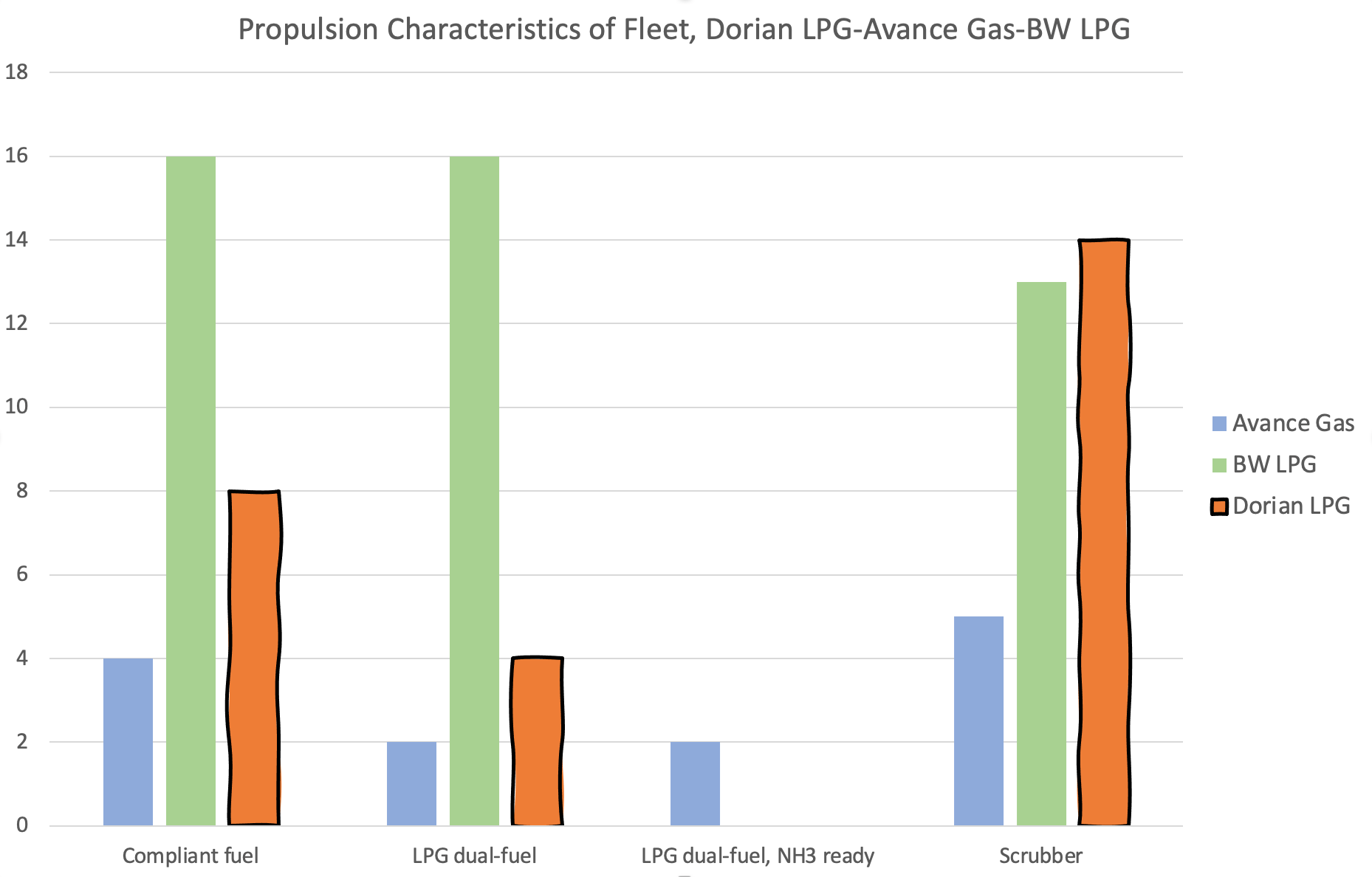

Let's look at the fleet from a different perspective: Propulsion. The graph below shows all three companies' fleets by propulsion characteristics:

{kind=link}

Propulsion Characteristics of Fleet (Each company's annual reports and websites)

To create the graph above, I have grouped all vessels into the following categories:

- Compliant fuel: Ships running on IMO 2020-compliant fuels (i.e. VLSFO)

- LPG dual fuel: Ships capable of running on both LPG and conventional fuels like HFO and MGO

- LPG dual fuel, NH3 ready: Like above, but ready to be converted to using ammonia as fuel

- Scrubber: Ships fitted with scrubbers, allowing them to run on cheaper HSFO and still comply with IMO 2020 regulations.

Reviewing the graph, a couple of distinguishing features of each company become evident:

- Dorian has invested in retrofitting scrubbers in its fleet. The fact that it has time chartered three LPG dual fuel vessels during 2023 and received one new build could give off an impression of Dorian being "late to the LPG dual fuel party." In its latest earnings call , however, management argued why it feels charter-in is the better option: ".. the chartered in ships give us market exposure, optionality on length and the potential upside of the purchase options while not requiring a large upfront investment."

- BW LPG's primary focus is on owning LPG dual fuel ships. As far as I know, it has no less than 16 in its fleet, making it the largest single owner of LPG dual-fuel ships.

- Avance Gas aims for the newest possible fleet, incorporating "alternative" fuels like ammonia. It currently owns two ammonia-ready LPG dual fuel ships, and has an additional four ammonia-ready ships (although they are medium gas carriers, not VLGCs) on order.

Is one strategy better than the other?

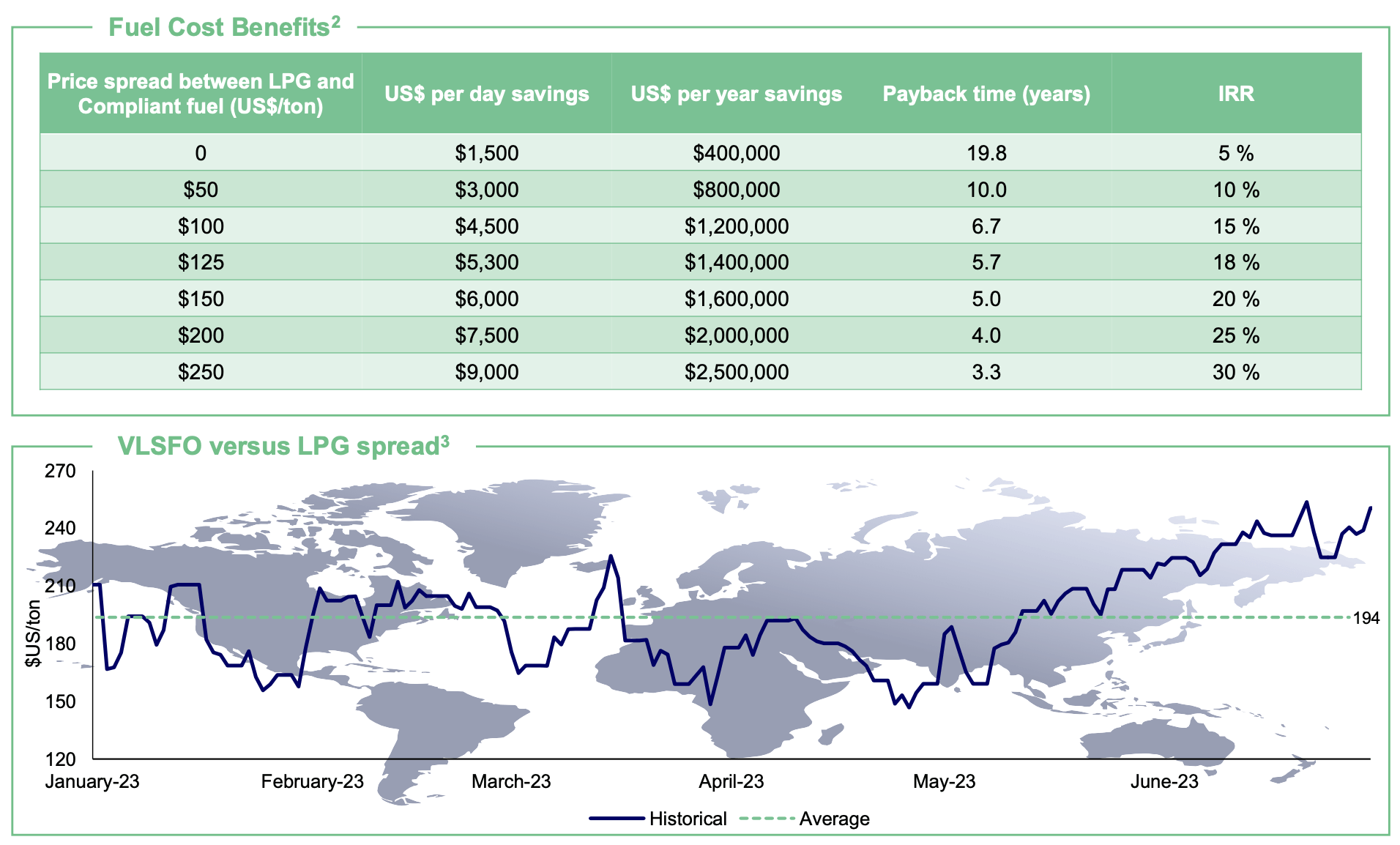

Having mainly scrubbers or LPG dual fuel ships is about which end of the VLSFO-LPG spread you end up. BW LPG offered the following helpful graph in its latest earnings report:

{kind=link}

VLSFO vs LPG spread, 2023 (BW LPG Q2 2023 earnings report)

An average spread of about $200 per ton saves the company $2 million annually. In other words, it's been a great year regarding fuel savings for LPG-powered vessels.

Winning using ammonia-ready ships is contingent on ammonia becoming an important ship fuel. According to Bureau Veritas , there are no ammonia-powered ships in service today. Towards the end of 2023, however, there might be an ammonia-powered tug .

An article at IEEE Spectrum sums up the status quo:

Shipowners and industry analysts say they expect ammonia to play a pivotal role in decarbonizing cargo ships. But there's a crucial caveat: No vessels of any size today are equipped to use the fuel. Even if they were, the supply of renewable, or “green," ammonia produced using carbon-neutral methods is virtually nonexistent. Most ammonia is the product of a highly carbon-intensive process and is primarily used to make fertilizers and chemicals.

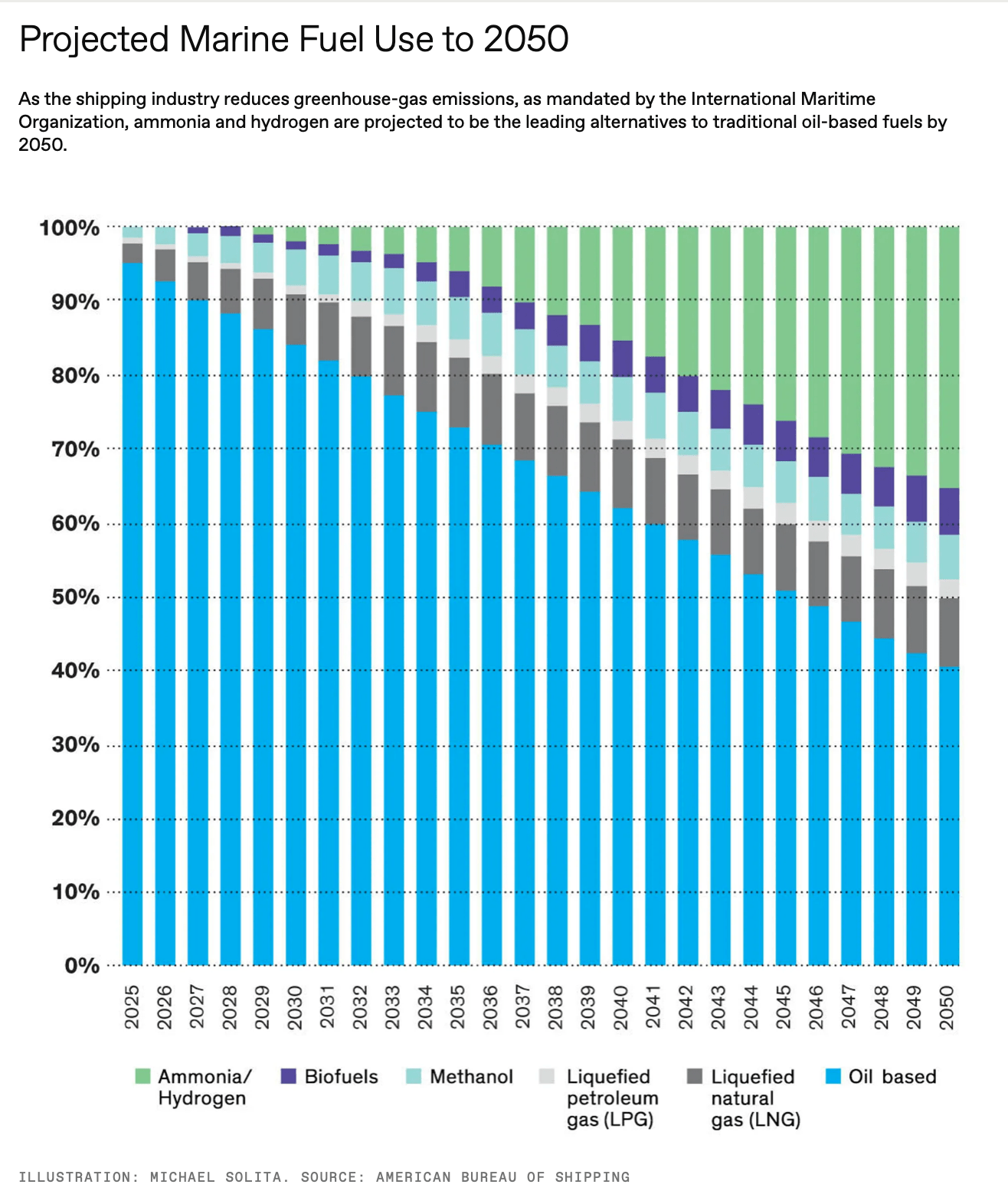

The same article explains that ammonia is just one of several alternative propulsion methods and fuels being developed currently. Using American Bureau of Shipping projects, the following graph was created by the authors of the IEEE article mentioned above:

{kind=link}

Projected ammonia use in oceangoing vessels, 2025-2030 (IEEE Spectrum article referenced in the paragraph above)

According to this projection, oil-based fuels will become a minority in 2046. Ammonia, on the other hand, will remain almost nonexistent until 2030 and gradually increase to about 35% of the fuel mix by 2050.

Whatever the case in 2050, it's clear that ammonia as a ship fuel is still in its very early phases.

But - burning ammonia as a fuel is not the only reason for acquiring these vessels. Carrying ammonia as cargo is perhaps more critical. Mr. Oystein Kalleklev, CEO of Avance Gas, spent a significant portion of its latest earnings call talking about its fleet renewal program and ammonia and summed up its strategy as follows:

... the big capital allocation strategy we have been pursuing now is to selling older ships and replacing them with new MGCs which are future proof in terms of efficiency and also given that they can transport ammonia as well as LPG.

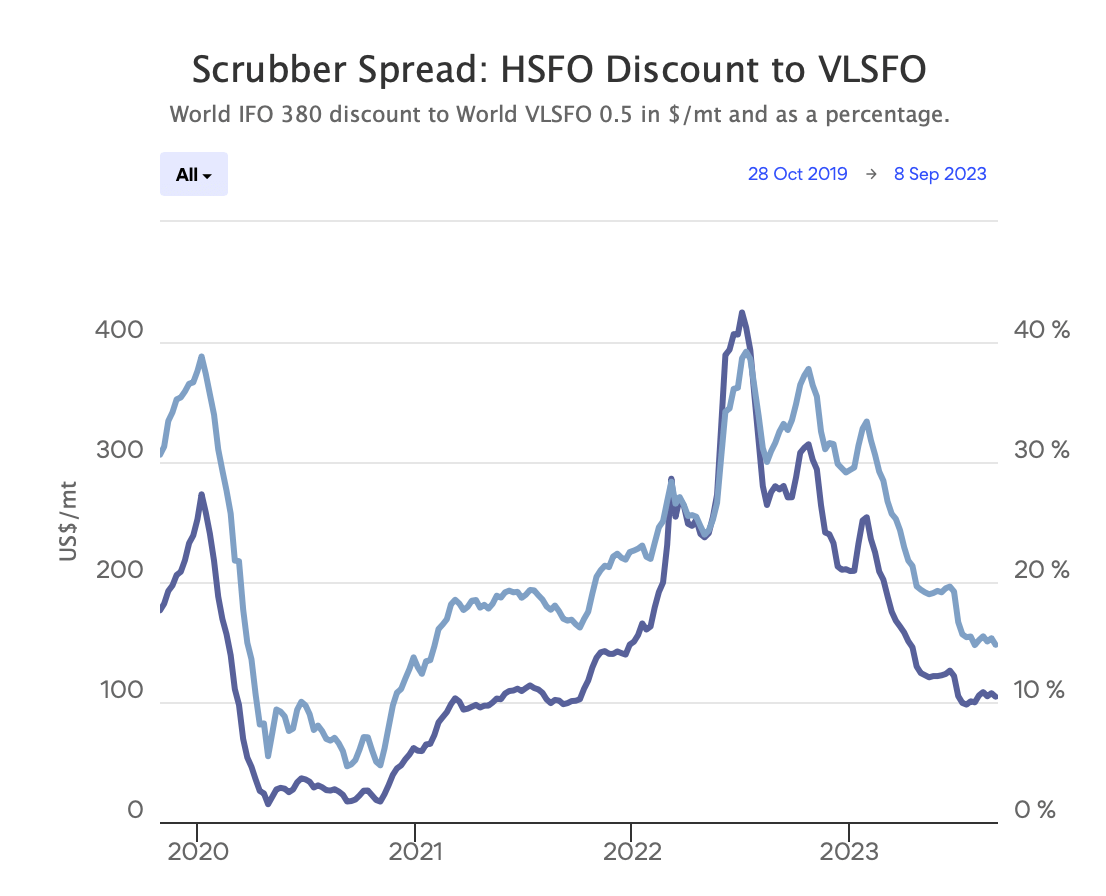

Returning to Dorian LPG's scrubber-oriented fleet, let's consider the scrubber spread. The darker line shows the $/mt amount, while the lighter blue line shows the percentage spread:

{kind=link}

Scrubber spread, 2020-2023 (Bunkerindex.com)

A lower spread means that Dorian saves relatively less on its scrubber-fitted vessels. An article in Ship and Bunker commented,

Scrubber industry representatives have previously talked of the $100/mt spread level of a rough indicator of where installing the systems start to look profitable.

Fleet diversity: Dorian LPG Relatively Less Diverse

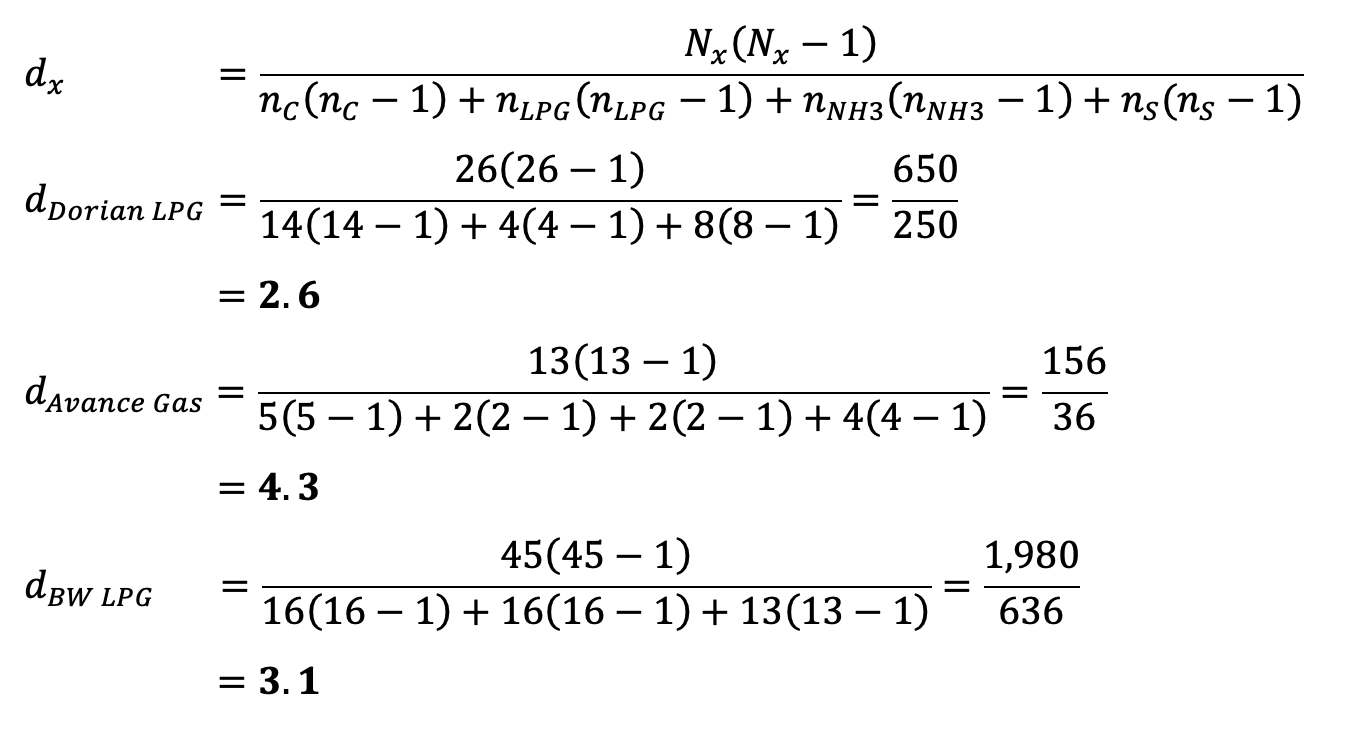

Since there is no straightforward answer to a question like, "What's the most profitable propulsion method over time?" let's consider another metric by which we can judge fleet strategies: fleet diversity.

While there are several diversity indexes, let's keep it simple and use an index of measure as laid out here .

The resulting calculations are shown below. The first calculation shows the formula, and the next is the index calculation for each company's fleet.

{kind=link}

Fleet diversity index (Author's calculations)

(Nx = fleet size of the company, nC = count of compliant fuel ships, nLPG = count of LPG dual fuel ships, nNH3 = count of ammonia ready ships, nS = count of scrubber ships)

Dorian LPG has the lowest fleet diversity index among the three peers.

These numbers make sense if one looks at the graph above. Dorian's fleet is tilted toward scrubbers, while Avance's and BW LPG's are more evenly split between propulsion technologies.

Plans for fleet renewal: No plans

In its latest earnings call, Dorian LPG CEO John Hadjipateras had this to say regarding capital allocation in his prepared remarks:

Regarding fleet renewal, 25 ships with a useful life of approximately 25 years implies replacing one ship per year. We capitalized on a good set of market dynamics to build one ship and to charter in three more on initial seven year terms with options. These fleet renewal deals were economically attractive. As the chartered in ships give us market exposure, optionality on length and the potential upside of the purchase options while not requiring a large upfront investment. We price optionality in our investment decisions as we continue to evaluate fleet renewal and other opportunities.

A caller later asked about capital allocation, to which Mr. Hadjipateras replied:

I think that what you heard is more or less everything we have to say at the moment.

Newly appointed BW LPG CEO Kristian Sorensen was direct and to the point when asked about capital allocation in its latest earnings call:

We still believe (..) the prices are too elevated like I mentioned. So there are no talks about newbuildings at the moment.

On the other hand, Avance Gas spent much of its latest earnings call talking about its fleet renewal program. It is bull on ammonia as cargo and believes it can secure attractive deals on MGCs. Furthermore, it has sold nearly all its older ships (15+ years old), with one remaining in its fleet. The following quote from the earnings call is instructive:

Then we have contracted four MGCs with a combined CapEx of $246 million, we do find this very attractive. [indiscernible] value for these ships are already about $5 million higher than the price we have contacted them for. So if we assume 70% loan-to-value, it might seem a bit high compared to what we have of loan-to-value today, but reflecting the fact that a lot of these ships typically have longer-term charters, which you can bank on and get a higher leverage on the ships.

That means our financing capacity of $186 million and the equity release or the cash release from Iris and Venus would be $60 million. So we will be able to finance the equity portion of these two ship -- of these four ships with the sale of two older ships. And that means one plus one is four new ships sold. So two 15-year ships can then easily become four newer ships. And if we fail on doing that, we also have a very substantial cash balance of $192 million, which we can utilize to finance the ships as well.

Avance Gas can find a market for its older VLGCs and use the proceeds to partly finance its "beautiful" four MGCs deal, which it thinks is a safe bet due to its cash position and the fact that "these ships typically have longer-term charters."

In summary, both Dorian LPG and BW LPG are reluctant to expand their fleets, while Avance Gas is expanding its product offering by adding MGCs to its VLGC fleet.

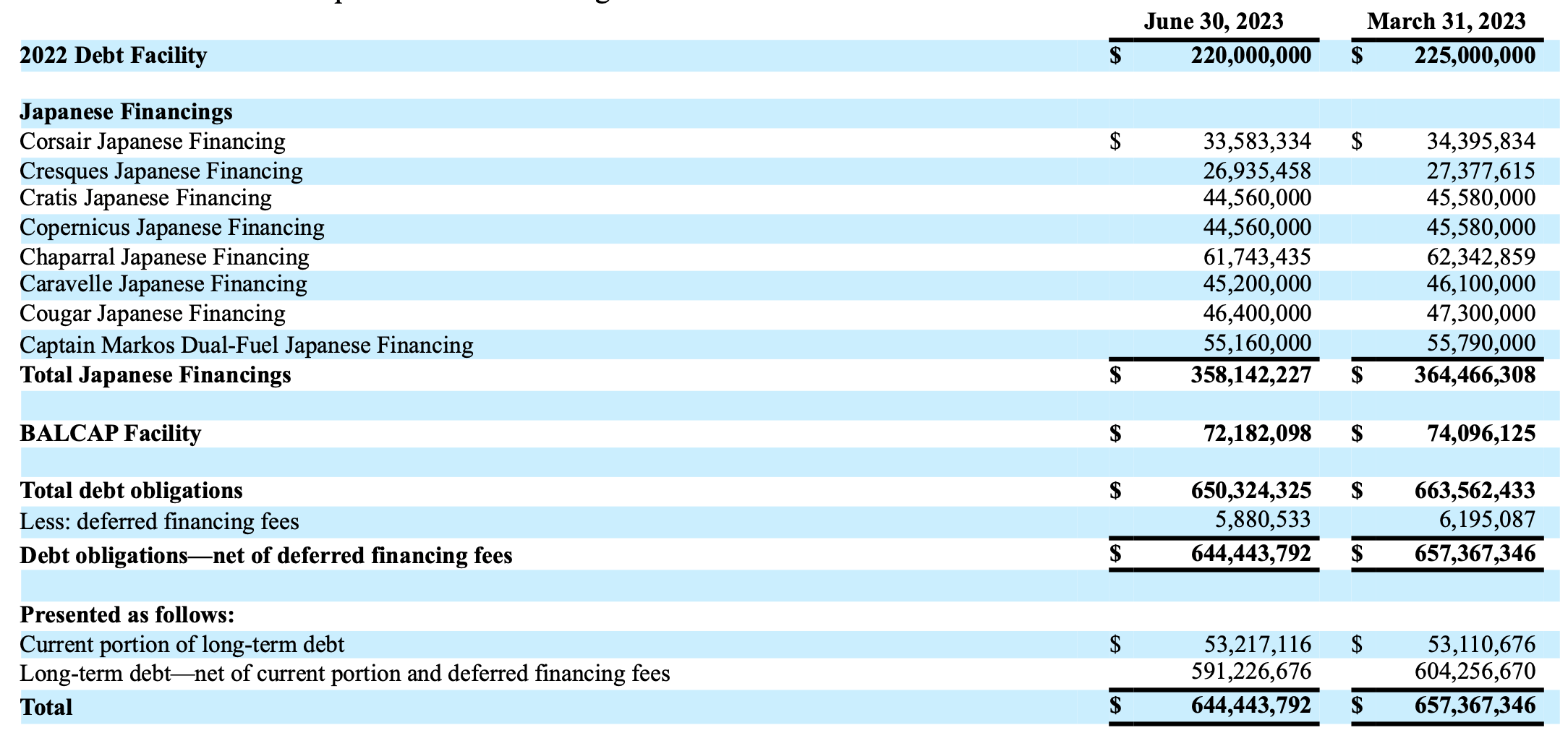

Long-Term Debt Profile: No Balloon Payments Before 2027

As of June 30, 2023, Dorian LPG had $644 million in long-term debt, with $53 million maturing within one year. An overview of its debt obligations is shown below:

{kind=link}

Long-term debt as of June 30, 2023 (Dorian's Q1 2024 quarterly report, p. 10)

Dorian's long-term debt consists of three primary sources:

- The 2022 Debt Facility, which refinanced a 2015 debt facility, is about one-third of the outstanding debt,

- The Japanese Financings, which are tied to individual vessels and are about half of its debt,

- The BALCAP Facility, which refinanced loans secured by two of Dorian's VLGCs, is about one-tenth of its debt.

Its "Japanese" and "BALCAP" debt obligations include monthly "mortgage-style" principal payments, with balloon payments at its last term.

Entering fiscal year 2023 (April 1, 2022 - March 31, 2023), Dorian had $72 million of its long-term debt due within 12 months. For the next three years, the current portion of its debt will decrease to about $53 million:

{kind=link}

Minimum principal repayments, 2024-2028 (10-K year ending 2023, p. F-25)

The increase in 2027 obligations is explained by the BALCAP facility maturing, with a balloon payment of about $44 million.

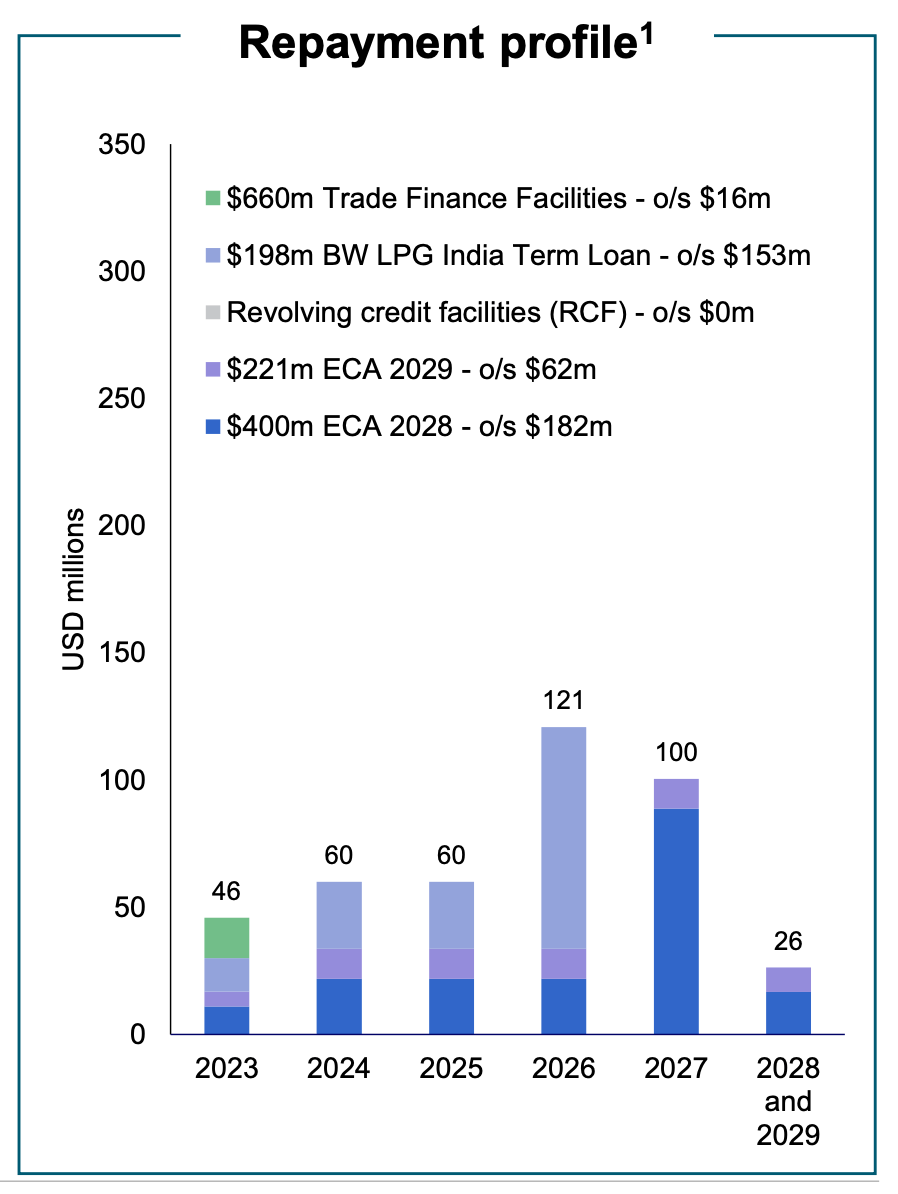

How does this repayment profile compare to peers BW LPG and Avance Gas?

BW LPG offered this illustration in its latest earnings presentation :

{kind=link}

BW LPG repayment profile, 2023-2029 (Q2 earnings presentation, p. 15)

A large portion of the BW India term loan matures in 2026, while a large part of the 2028 ECA matures in 2027.

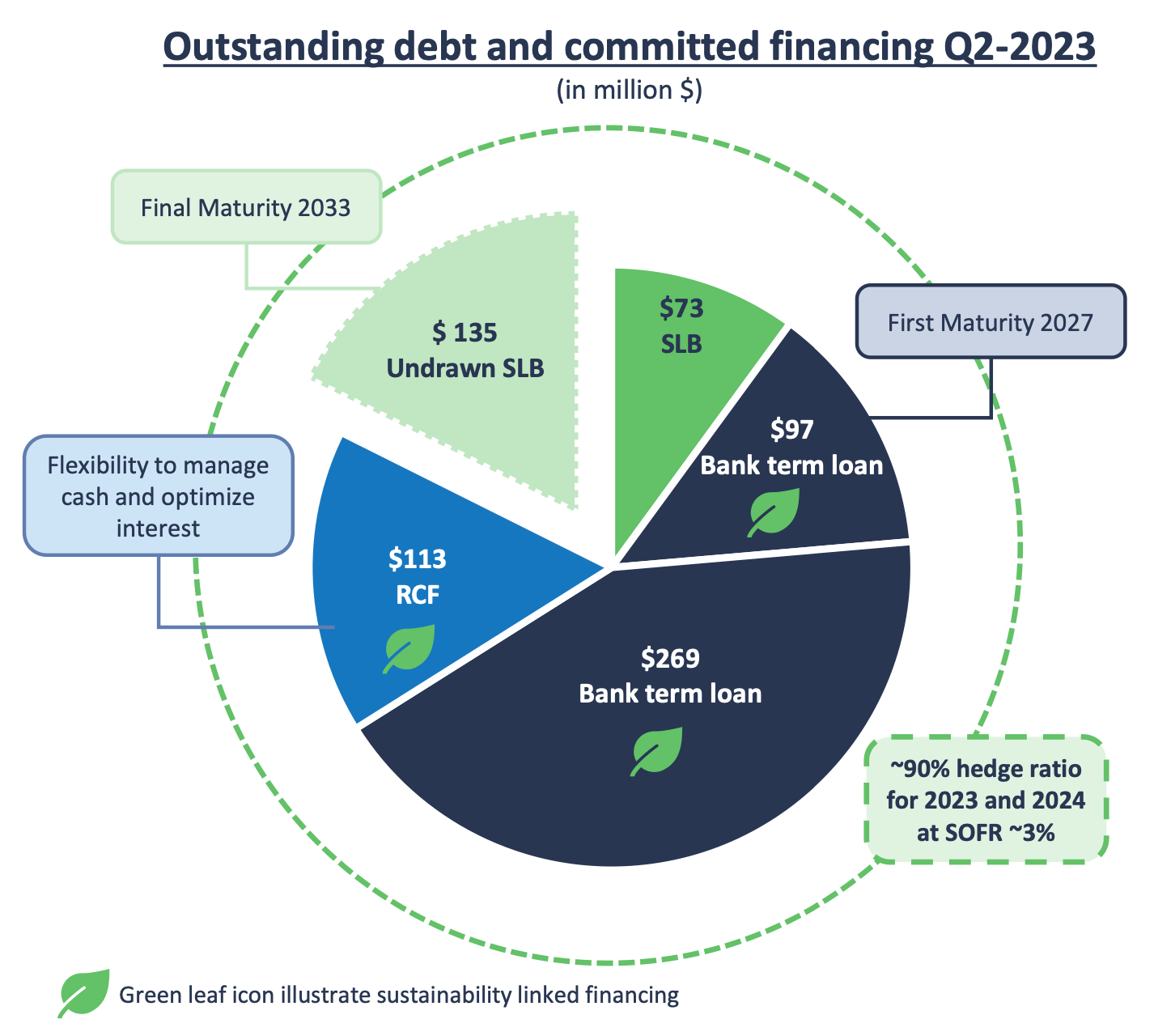

Finally, its peer Avance Gas presents its debt obligations in the following manner in its latest earnings presentation :

{kind=link}

Avance Gas debt obligations and repayment profile (Q2 earnings presentation, p. 14)

This illustration shows that Avance's next significant maturity is the $97 million portion of its bank term loan, maturing in 2027. Furthermore, Avance Gas reported a current long-term debt of $43 million at the end of Q2, 2023.

As a side note, the light-hearted use of graphics on slides 5 and 6 in the Q2 presentation might be seen as amusing or unprofessional, depending on one's outlook. I think it is pretty funny and reflects a company with a different style than its peers. You can take a look at my previous Avance Gas article for more about its energetic CEO.

In summary, the long-term debt obligations of all three peers are broadly similar, with all three having significant maturities coming in 2026 and 2027.

Senior Management Team: Managed by its Founders

Today's management team is also its founders, for the most part. Five of the six senior directors listed on its website have been with the company since its inception in 2013. Its team has been in the same roles, except Alex Hadjipateras, the son of President and CEO John C. Hadjipateras, who joined the company in 2013 as Secretary. In 2022, he was promoted to Senior Executive Vice President at Dorian LPG ((USA)) LLC and Managing Director at Dorian LPG Management Corp. (Athens).

The sixth, chief commercial officer Tim Hansen, has been with the company since 2014.

In other words, Dorian's management shows impressive resilience and stability. Stability and predictability at the senior management level benefit the organization, giving it room to work on reaching its objectives rather than time and again adjusting to the direction a new management team or CEO would introduce.

However, as one dissenting voice claims, "Long CEO Tenure Can Hurt Performance." This Harvard Business Review article states that a "long CEO tenure" means more than 4.8 years. The reasoning goes,

Early on, when new executives are getting up to speed, they seek information in diverse ways, turning to both external and internal company sources. This deepens their relationships with customers and employees alike.

But as CEOs accumulate knowledge and become entrenched, they rely more on their internal networks for information, growing less attuned to market conditions. And, because they have more invested in the firm, they favor avoiding losses over pursuing gains. Their attachment to the status quo makes them less responsive to vacillating consumer preferences.

While I find this perspective interesting, I don't see evidence supporting an argument to replace management. Dorian has succeeded in providing shareholder returns relative to its peers:

This is also true in many other companies, of course. I don't accept the notion that the "magic tenure length" is 4.8 years at face value.

Market Outlook Remains Strong

Dorian LPG's peers Avance Gas and BW LPG spent several slides arguing that the market outlook is positive in their earnings presentations. Dorian LPG does not similarly publish quarterly slide decks. Instead, it offers an informative rather than argumentative news bulletin , calmly stating that

The continuously tight VLGC supply/demand balance, the strong arbs and logistical constraints, including delays at the Panama Canal, have kept the freight rates consistently above the 5-year highs for the period.

Let's unpack this statement. It refers to three drivers for the consistently high rates the market has seen in 2023: world fleet imbalances, east-west arbitrage, and the Panama Canal delays.

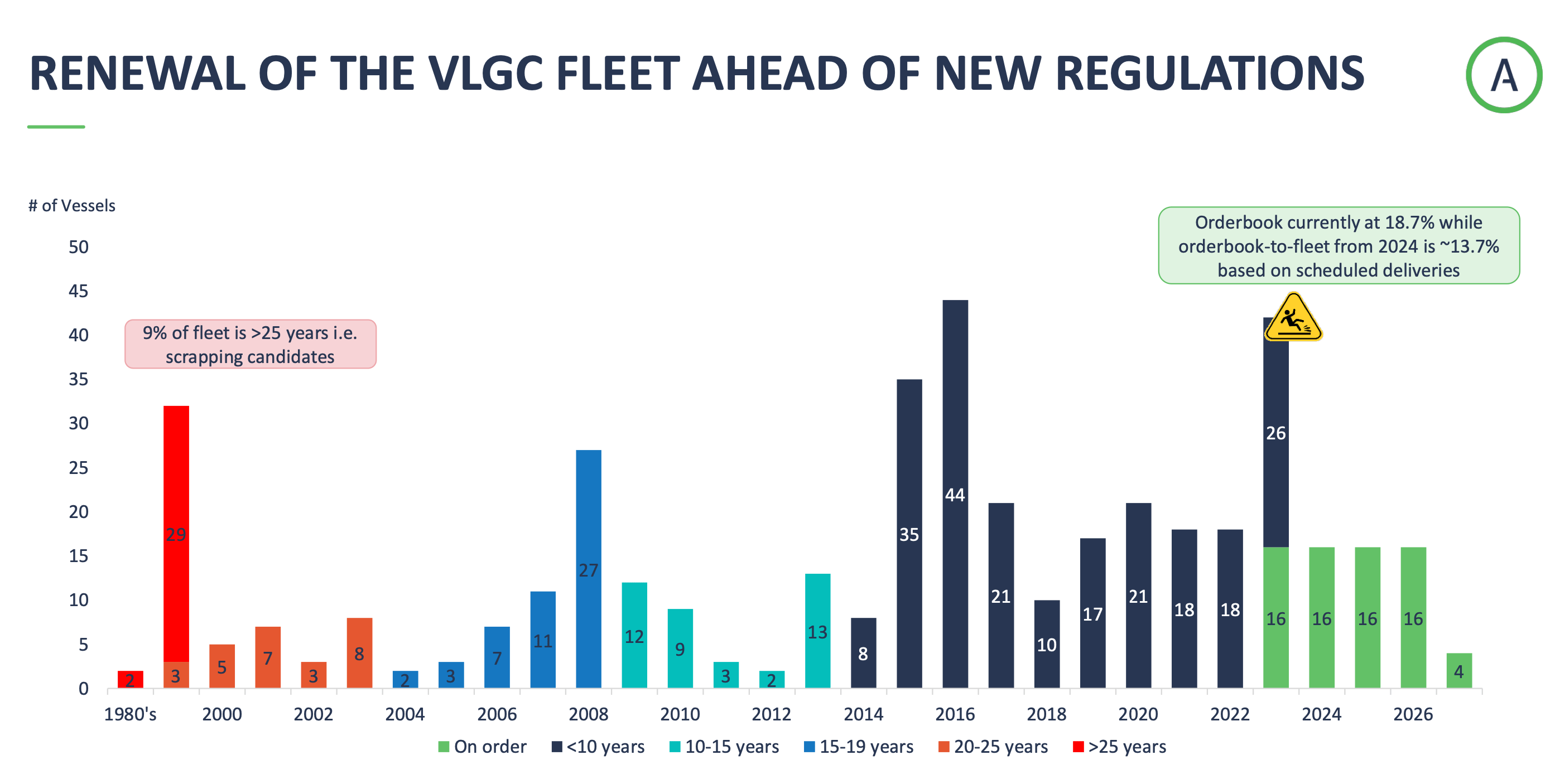

World fleet imbalance: Demand exceeds supply

Both BW LPG and Avance Gas point out this in their latest presentations. Avance offers this illustration:

{kind=link}

World fleet by age, order book (Avance Gas Q2 2023 presentation)

Orderbook-to-fleet is now about 19%, down from about 20-25% in the last quarter. Additionally, BW LPG states that shipyards indicate that they are sold out until 2027. Add to that the current high prices in the market mentioned above in the "plans for fleet renewal" chapter, and the sum of these effects is that expanding the world VLGC fleet seems unlikely at this point in time. Assuming demand does not change significantly, this bodes well for freight rates shortly.

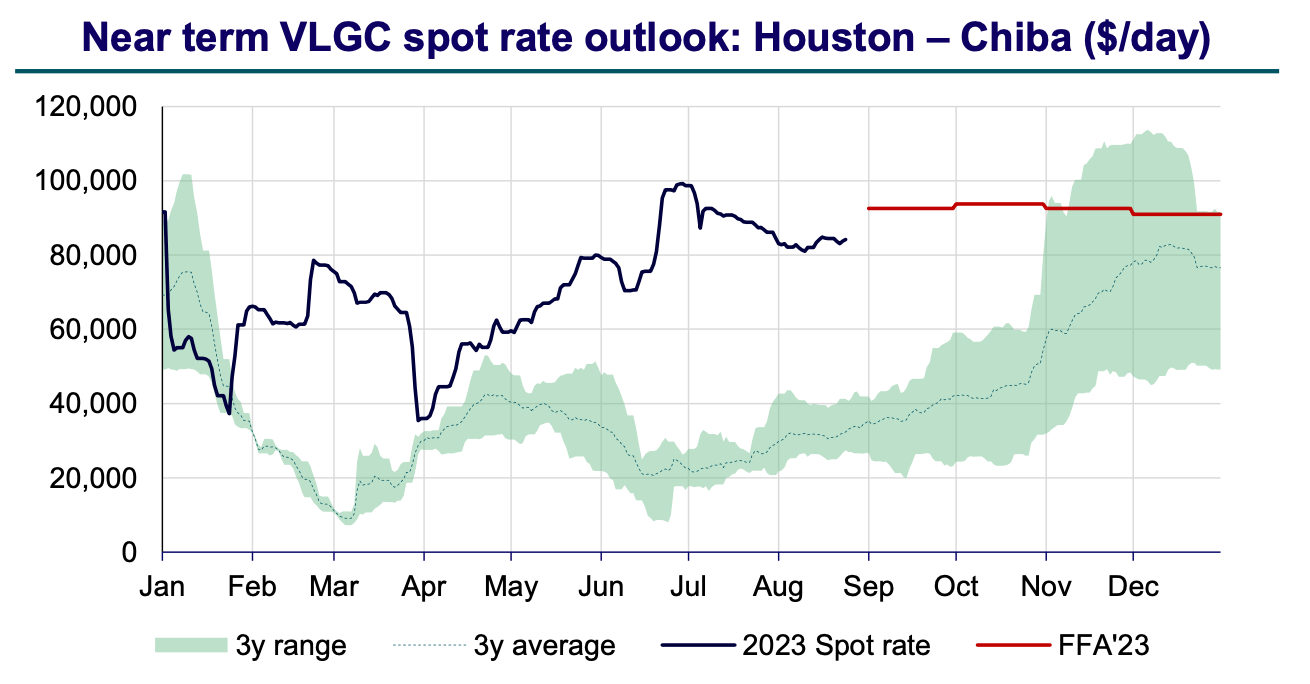

East-West Arbitrage

LPG is cheaper in the U.S., which produces large quantities, and rather more expensive in Asia, which consumes large amounts. This is an attractive dynamic for VLGC shippers. Avance Gas offers this illustration in its latest earnings presentation:

{kind=link}

East-West Arbitrage, Freight FFA (Avance Gas Q2 2023 presentation)

The forward curve indicates that this attractive arbitrage will continue well into 2024. With a forward product arbitrage over $150, there's much support for freight rates above $100/metric ton. According to Fearnley's Fearnpulse , VLGC rates once again exceeded $100,000/day in September.

Peer BW LPG reviews the forward freight agreement curve in its quarterly reports. Please look at the following manipulated image, showing BW LPG's near-term spot rate outlook. The graphs from the last three quarters are laid on top of each other:

{kind=link}

FFA curve, Q4 2022-Q2 2023 (BW LPG quarterly presentations, Q4 22 - Q2 23)

The red line, showing the FFA curve, has shifted upward each quarter. In other words, the forward market has consistently underestimated the supply/demand balance.

For reference, here's how the graph looks like in BW LPG's latest presentation:

{kind=link}

Forward freight agreement curve (BW LPG Q2 2023 presentation, p. 6)

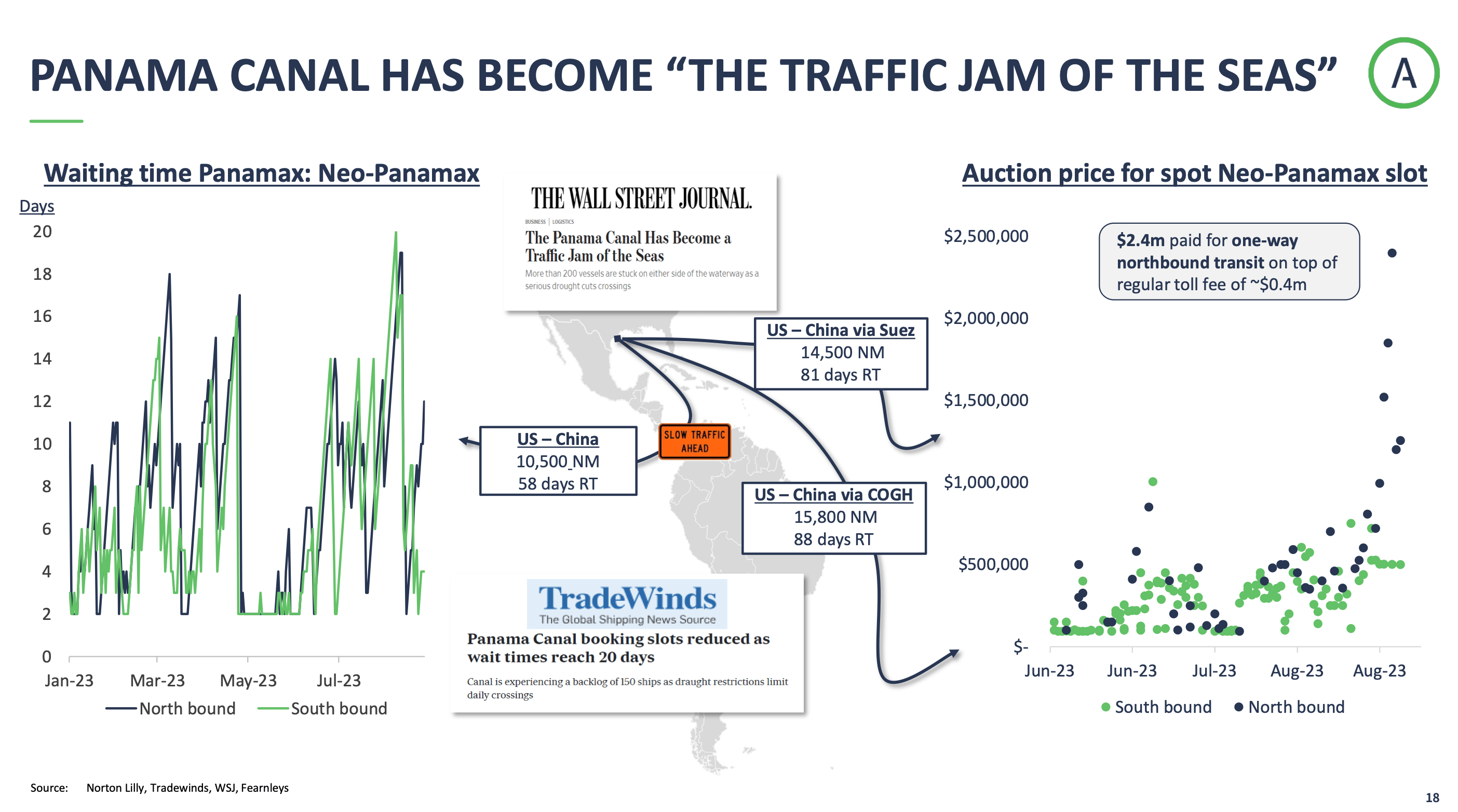

Logistical constraints: The Panama Canal

In its latest presentation, Avance Gas offered a great slide explaining the Panama Canal calamity. Though a somewhat packed decline, it is still the best one-pager explaining what's going on I have seen yet:

{kind=link}

Panama Canal delays (Avance Gas Q2 2023 presentation, p. 18)

Notice the unusually high auction prices for neo-Panamax slots gained during August. Shippers choosing to go the long route through Suez or around the Cape of Good Hope face a 40-50% longer voyage (return trip). The unpredictable, longer waiting times pose another problem: Meeting "laycan," the time the ship must be available for loading to start a new fixture. This unpredictability is driven by the nature of the LPG freight market: long-time charters are rare, and the spot market is significant. Preference is given to the Canal to vessels like container and cruise ships, which may book their passages a year in advance and carry more valuable cargo. This means, of course, that other ships - like gas carriers - have to wait.

These issues drive ton-mile demand (longer voyages) and reduce available tonnage by effectively keeping it out of the market, as ships are "trapped" in the canal.

Dorian LPG has employed mitigating tactics by ensuring that the three dual fuel vessels it has chartered during 2023 can use the old Panamax size.

Conclusion

This in-depth review has reviewed fundamental indicators, company-specific factors, and the current market outlook.

In terms of fundamentals, Dorian LPG is broadly similar to its peers.

It separates itself from its peers by having an extraordinarily stable management team, with almost no changes since its inception in 2013. However, as we've seen, that may also be a hindrance. An indicator for measuring fleet propulsion diversity was proposed and underlined that Dorian's reliance on scrubbers makes it more uniform but vulnerable to a narrowing scrubber spread.

The market outlook has been strong for multiple quarters and still is. Supply constraints are likely to remain for some time still. These forces provide buoyancy for strong freight rates in the short to medium term.

For further details see:

Dorian LPG: Scrubber-Focused Fleet Loses Out On Narrowing Scrubber Spread