LVMHF - Double Entendre

2023-12-08 07:26:24 ET

Summary

- The article discusses the recent rally in various asset classes, including US high-yield and US investment-grade bonds.

- It highlights the significant performance of US investment-grade bonds, particularly at the long end of the yield curve.

- The article also mentions the potential impact of the Bank of Japan's monetary policy on global asset allocation and carry trades.

Man's most valuable trait is a judicious sense of what not to believe." - Euripides

Looking with interest the unfolding "everything rally", in effect an early Santa Claus rally, which we anticipated while watching Bitcoin as a proxy liquidity indicator when it came to selecting our title analogy given our fondness for multiple referencing we decided to go for "Double entendre".

A "Double entendre" is a figure of speech that is devised to have a double meaning, of which one is typically obvious whereas the other often conveys a message that could be perceived as suggestive or even offensive in some instances. "Double entendre" generally relies on multiple meanings of words or different interpretations of the same primary meaning. The phrase has not been used in French for centuries and would be ungrammatical in modern French. No exact equivalent exists in French we must confide. Our signature style of using title analogies can indeed be akin to "Double entendre" but definitely not doublespeak, which deliberately obscures, disguises, distorts, or reveres the meaning of words. We use "Double entendre" while politicians and central bankers use "doublespeak". Doublespeak is the language used to deceive usually through concealment or misrepresentation of truth. We often joked that we were immune to these "Jedi tricks".

In this conversation, we want to look at the epic rally we saw during the month of November and what it entails as we move toward 2024 from an asset allocation perspective.

Santa Claus rally came early

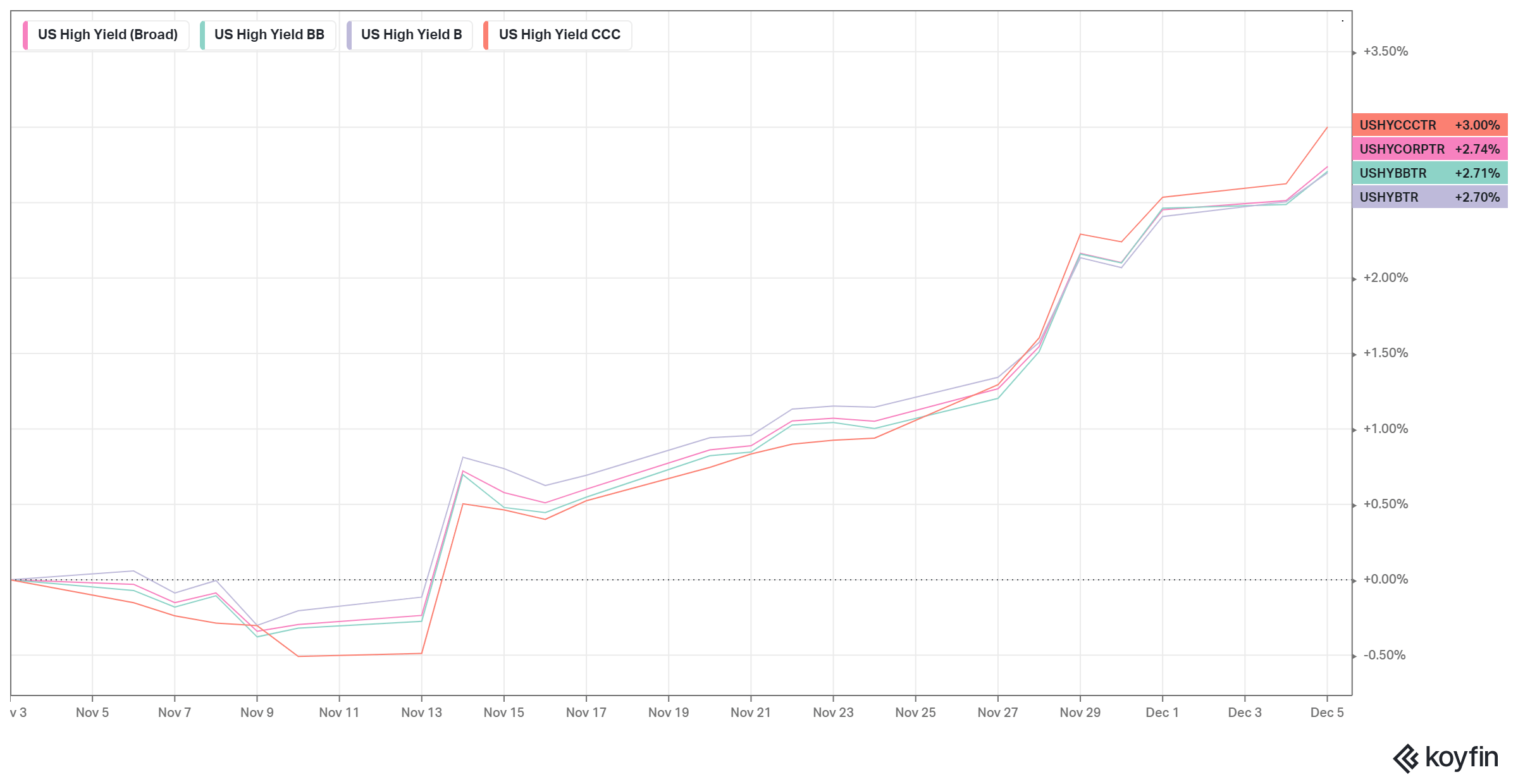

Thanks to the continuation of the fall in US yields, we have seen a significant bounce in the "high beta" space like in the US high yield (1-month chart) with CCCs leading the race:

{kind=link}

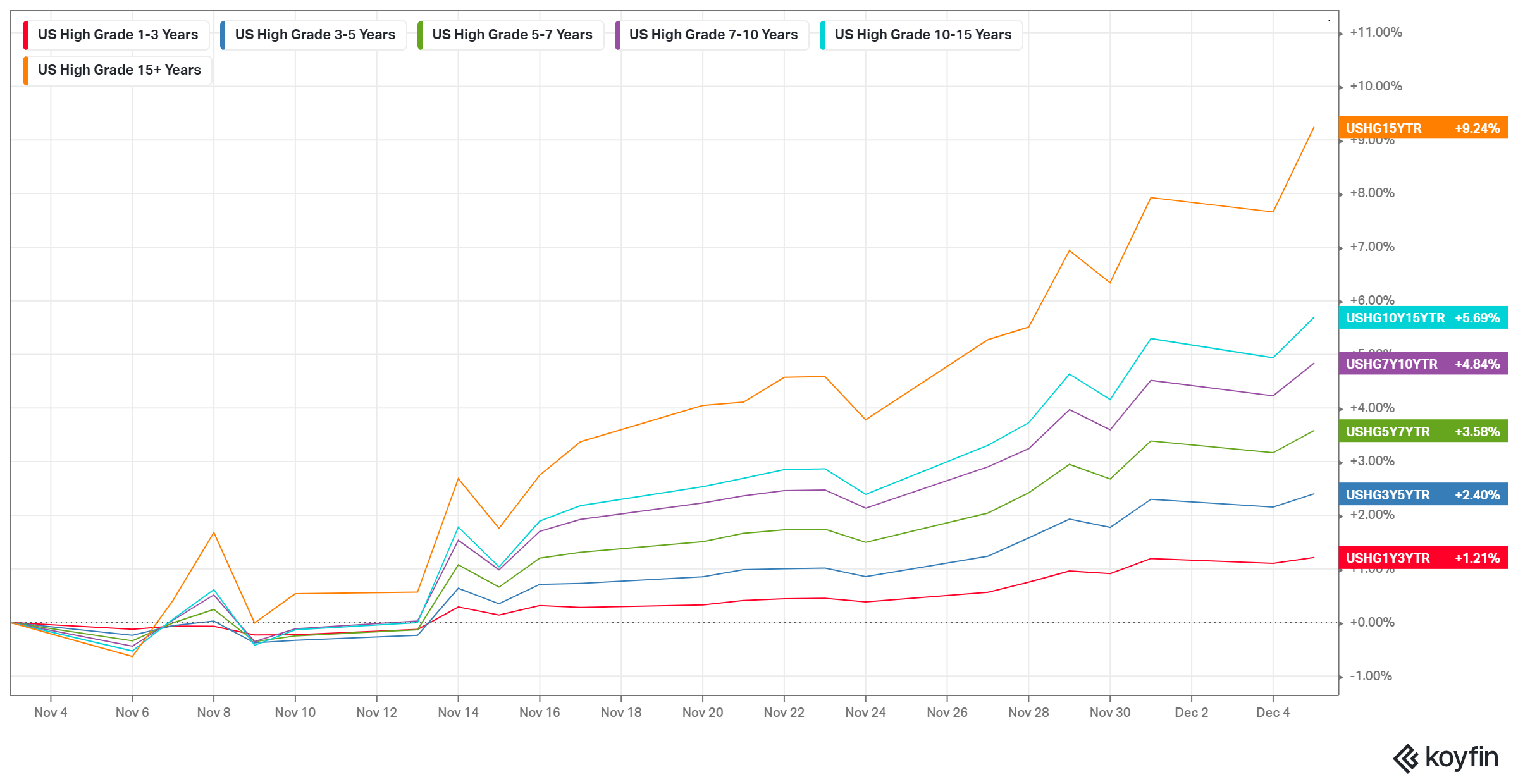

The most spectacular move during the course of November was at the long end of the US investment grade. The performance has been spectacular, to say the least and particularly the long end, no real surprise there given the fall in yields in the long end of the US Yield curve (1 month):

{kind=link}

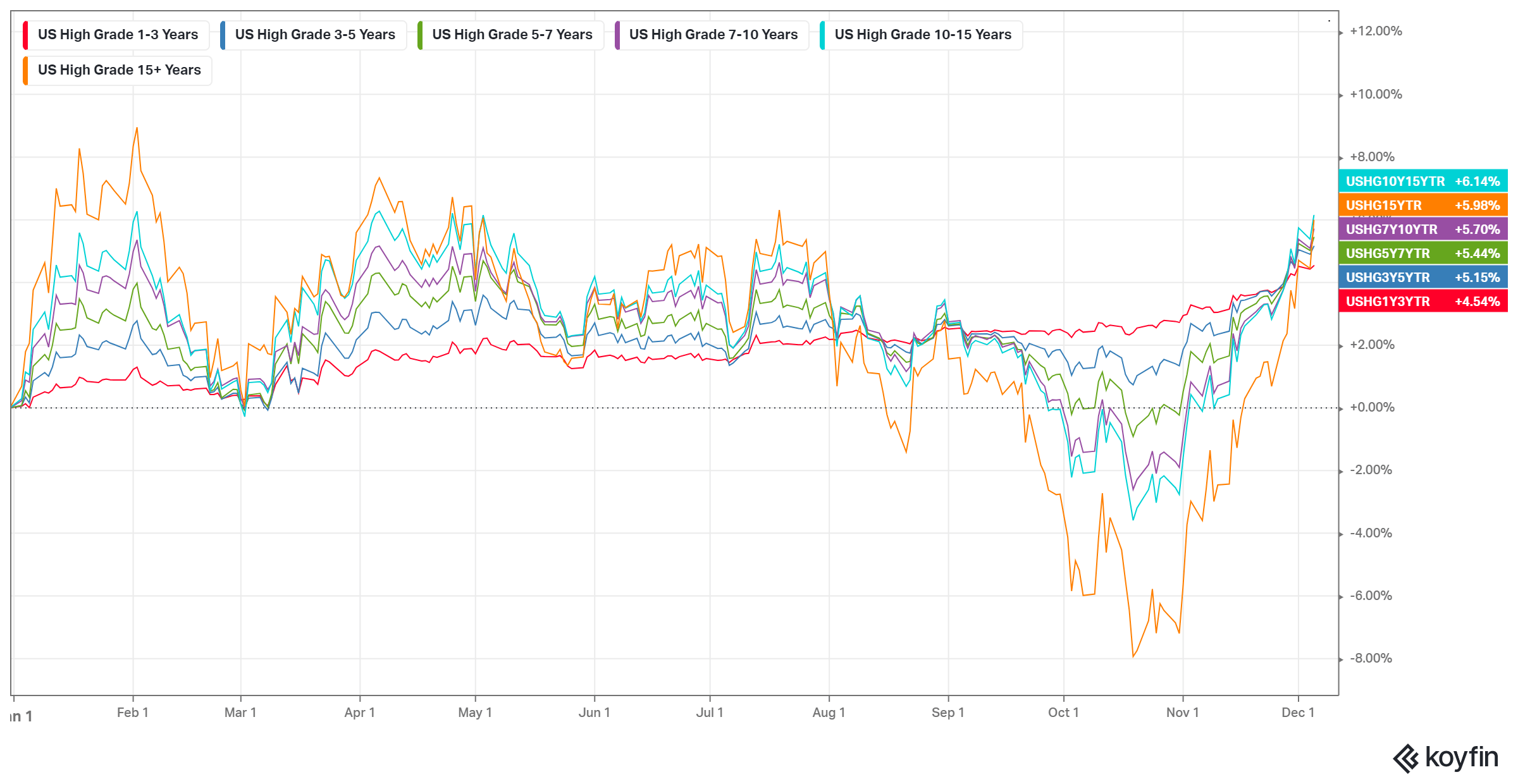

In relation to US investment grade, the volatility has been significant as displayed in the below YTD chart:

{kind=link}

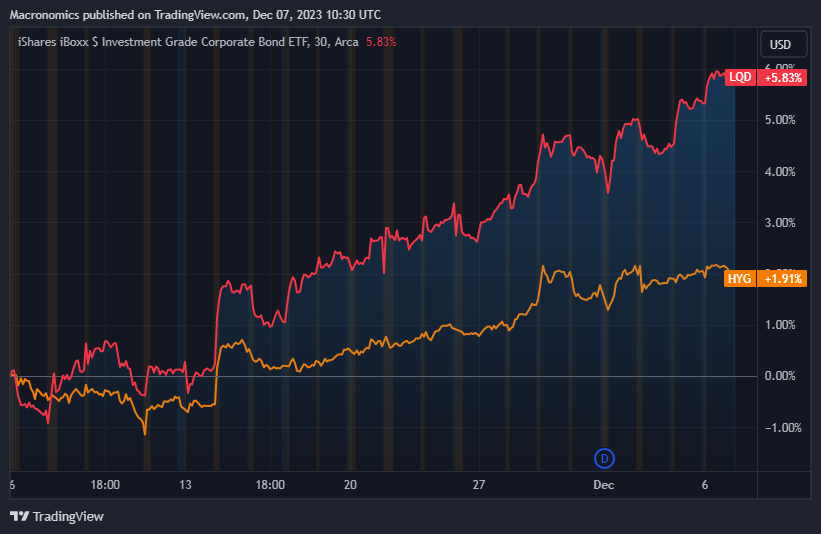

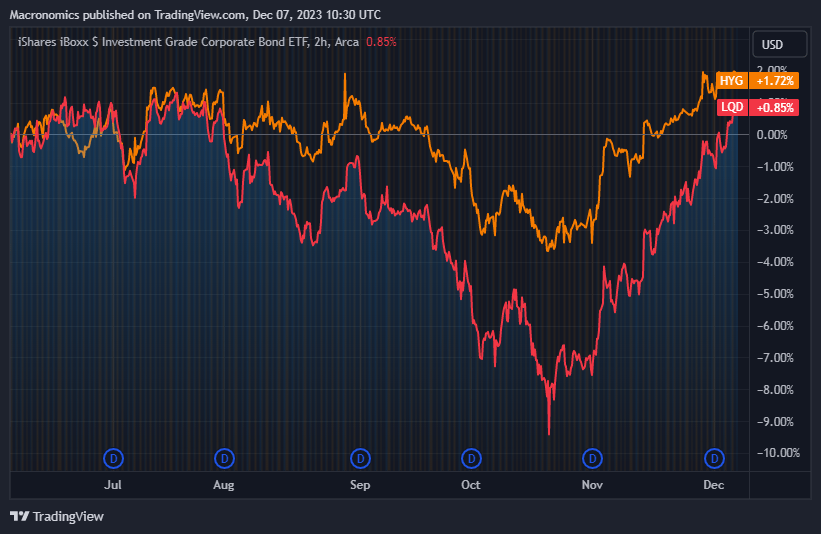

In one month, the performance of US investment-grade ETF (LQD) versus US high-yield ETF (HYG):

{kind=link}

Bond volatility in the long end has created huge volatility and as such, US investment-grade performance relative to US high yield has been plagued by "convexity" as shown in the below 6-month chart:

{kind=link}

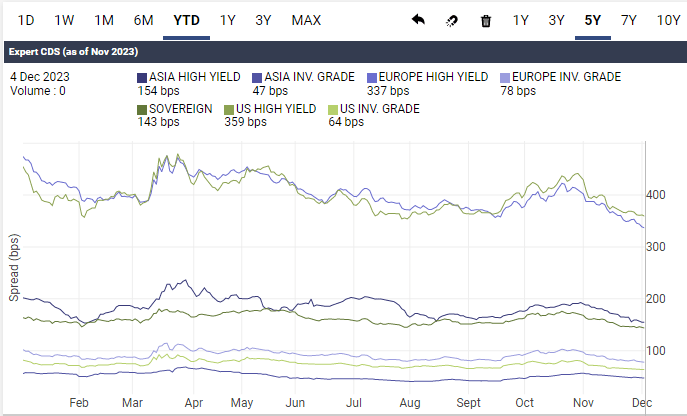

Credit risk-wise, 5-year CDS spreads have significantly receded (YTD chart). Since our last conversation, US high-yield CDS gauge is tighter by around 80 bps (359 bps now vs. 443 bps). European high yield, as well, is improving:

{kind=link}

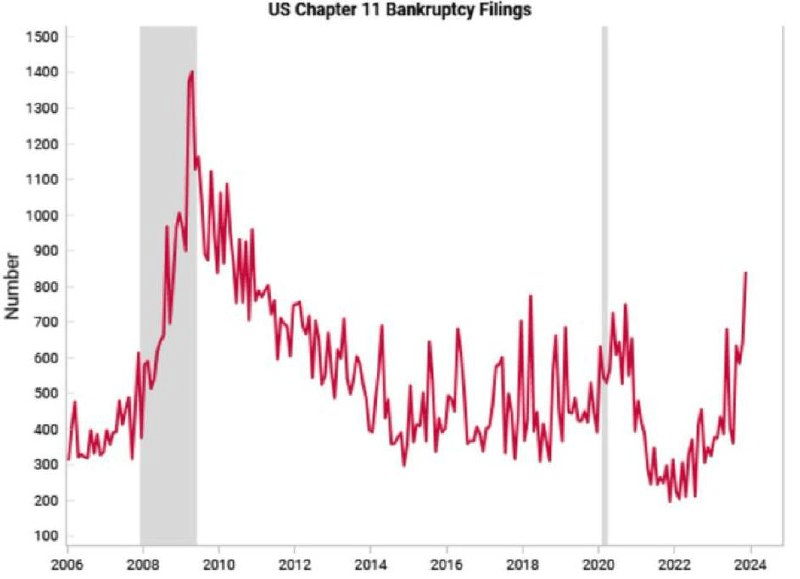

But, if indeed there are signs of the US economy weakening, then we think that credit spreads are, therefore, too tight in US high yield and we would think that 2024 should see an outperformance of US investment grade relative to US high yield and default rates should start in that instance to creep higher. US Chapter 11 Bankruptcy filings are rising according to Variant Perception:

{kind=link}

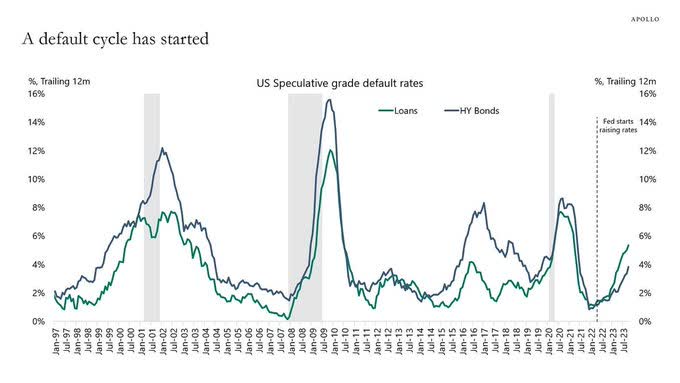

Since the Fed started raising rates in March 2022, default rates have gone from 1% to 5%+. US high yield and leveraged loans will continue to see rising default rates as the Fed holds rates higher for longer in that context:

{kind=link}

We think US high yield will widen in 2024 more relative to US investment grade following yet another stellar performance in 2023. But, bond volatility could make a significant return still and "convexity" exposed investment grade could be impacted as well given the current US fiscal deficit trajectory and issuance.

According to Bank of America, in the US investment-grade space, November's 5.6% total return was the strongest in 38 years. The 30-yr UST delivered a sweet 10% gain.

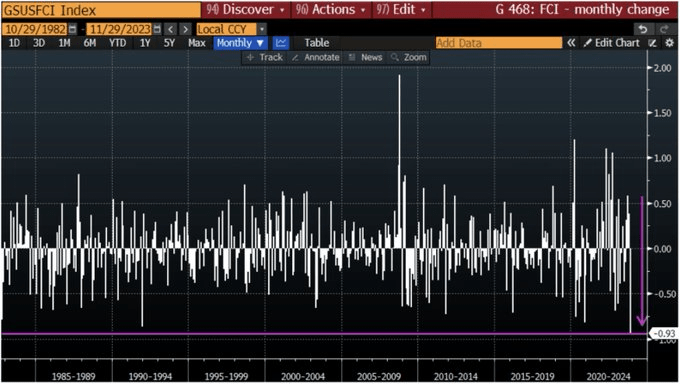

November saw the largest easing in US financial conditions of any single month in the past forty years hence the early Santa Claus rally:

{kind=link}

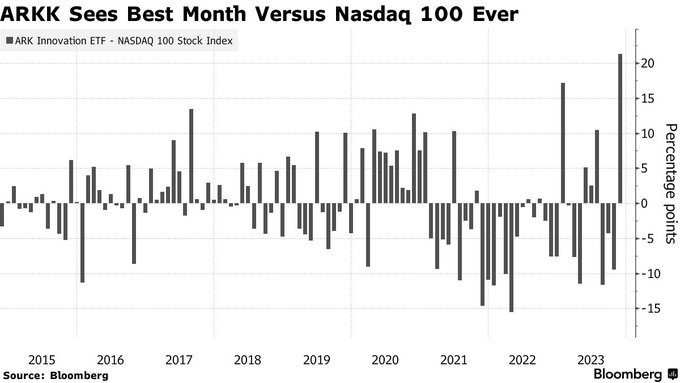

As well, [[ARKK]] aka the beta play, saw its best month versus the Nasdaq 100 ever:

{kind=link}

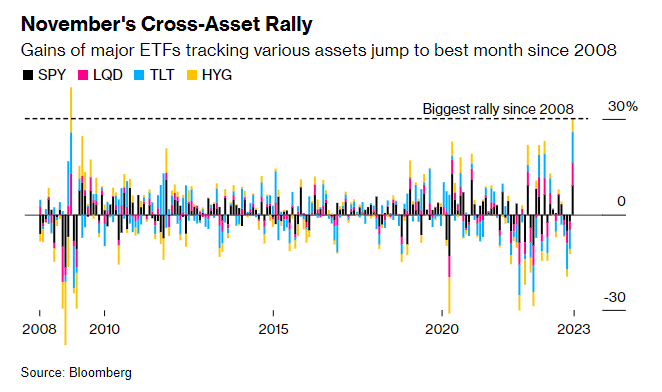

Overall, the month of November has been a month for the record books:

{kind=link}

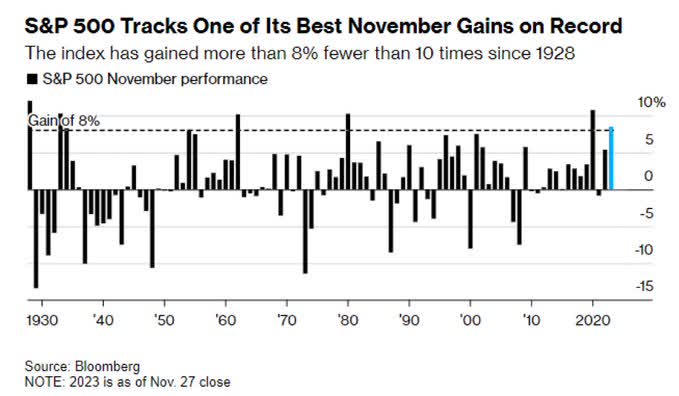

The S&P 500 finished November with a gain of 8.9%, the second-best November since 1980:

{kind=link}

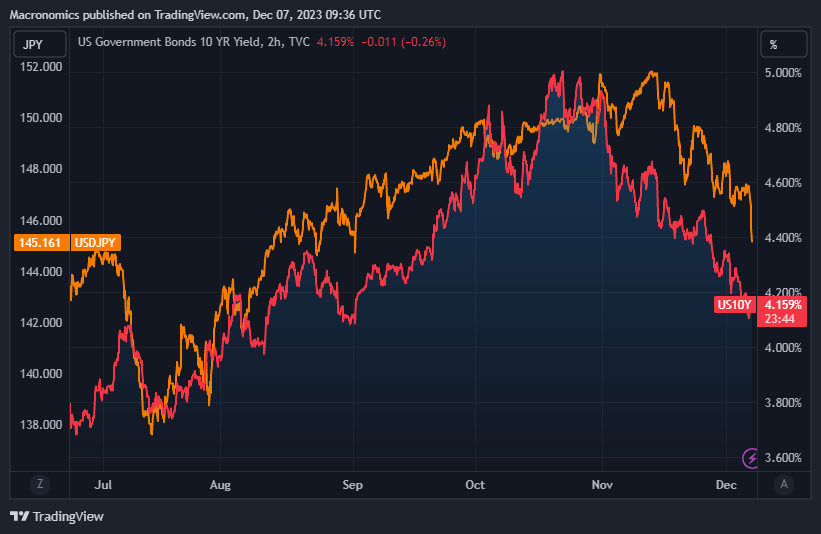

As you know by now, we have been tracking the Japanese yen depreciation in synch with the rise in US Treasury 10-year yields (6-month chart):

USTs 10 year yield vs USD/JPY 6 months (Macronomics - TradingView)

{kind=link}

As such, we indicated that a strengthening of the Japanese yen was on the cards. We believe that we will see further strengthening of the Japanese currency in 2024. The big elephant in the global markets room as we keep repeating ourselves and there is no "double entendre" there is the Bank of Japan monetary policy. The Bank of Japan racked up the most unrealized losses on its bond holdings on record in the latest six-month period to the tune of $71.2 billion. This illustrates the growing challenge facing Governor Kazuo Ueda if he moves toward normalizing policy after years of "easy policy". With inflation cooling to the slowest pace in over a year, it supports the current cautious stance of the Bank of Japan:

{kind=link}

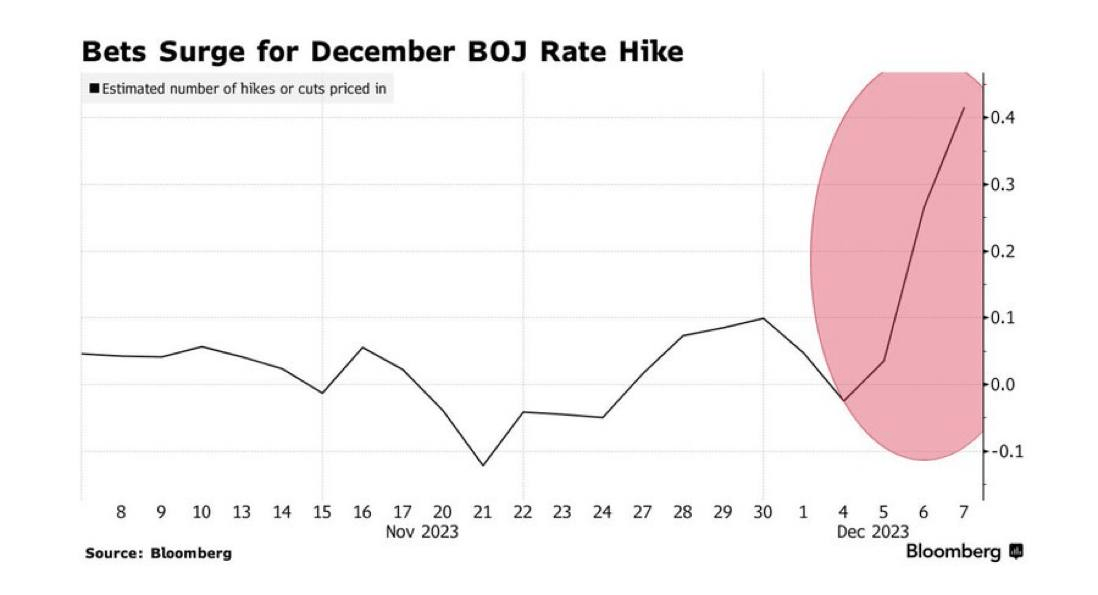

The Bank of Japan is currently discussing the end of Zero Interest Rate Policy (ZIRP); as such, there is a significant strengthening of the Japanese yen as we type this musing:

{kind=link}

We, therefore, think it is paramount to watch whether the Bank of Japan is going to end or not its ZIRP policy in the near term as it will have significant implications in terms of global asset allocation and carry trades. Is the Bank of Japan going to "break" global markets in general and fixed income in particular?

What's for 2024?

When looking at 2024, we do think China is already seeing supportive measures to the economy being set up as reported by China Daily:

Some provinces and municipalities in China are stepping up policy support for the consumption sector, with many giving out vouchers to boost sales of automobiles and home appliances."

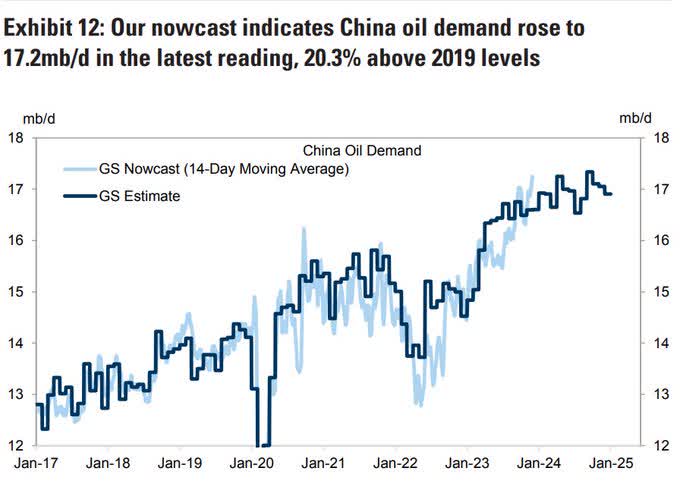

Also, China Dalian Iron Ore futures have surged 65% since May 2023, regardless of the Lehman narrative relating to Chinese real estate woes. Bear in mind that in just 5 years, China increased its oil consumption from 13 million barrels per day to 17 million barrels per day as per the below Goldman Sachs chart (H/T Michael A. Arouet):

China oil demand ( Michael A. Arouet - Goldman Sachs - X/Twitter)

{kind=link}

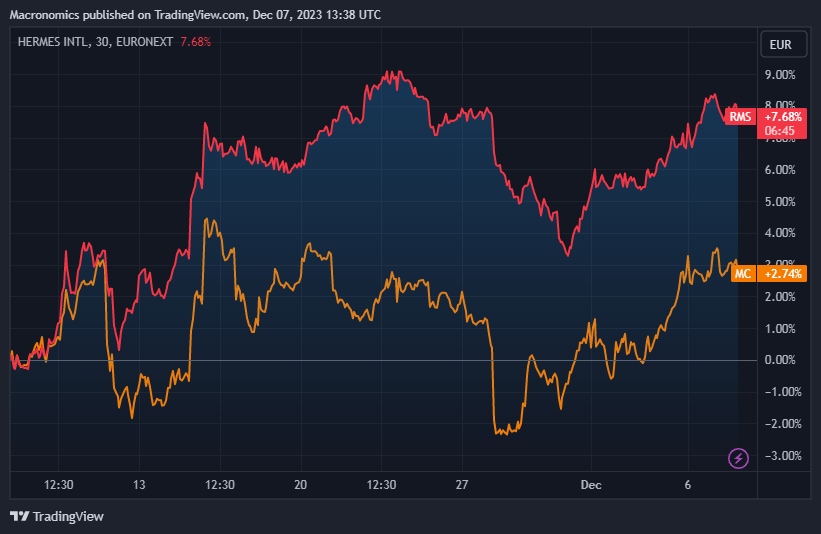

In various musings, we highlighted our fondness for the luxury sector driven by Asian demand in general and Chinese demand in particular. As such, we continue to favor Hermès (HESAY) over LVMH (LVMHF) for 2024, the year of the Dragon.

Hermès vs. LVMH - one month chart:

{kind=link}

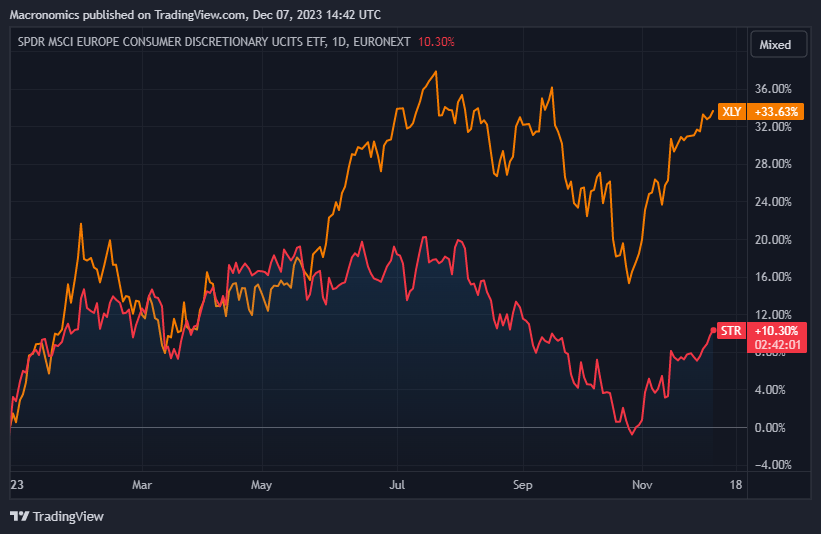

On an interesting note, ETF consumer discretionary between US and Europe are completely distorted by "Tech" given the US ETF comprises 23.82% of Amazon (AMZN), Tesla (TSLA) represents a weight of 17.77% whereas ETF STR the European version is strongly geared towards "Luxury" with LVMH weighting 19.58%, Richemont (CFRHF) 6.18%, Hermès International 6.12%. Textiles Apparels & Luxury Goods represent 42.25% of the European Consumer Discretionary ETF STR whereas the US ETF [[XLY]] is made up of 24.40% of Broadline Retail and 23.55% of Hotels, Restaurants, and Leisure. No wonder there is a huge performance gap YTD:

{kind=link}

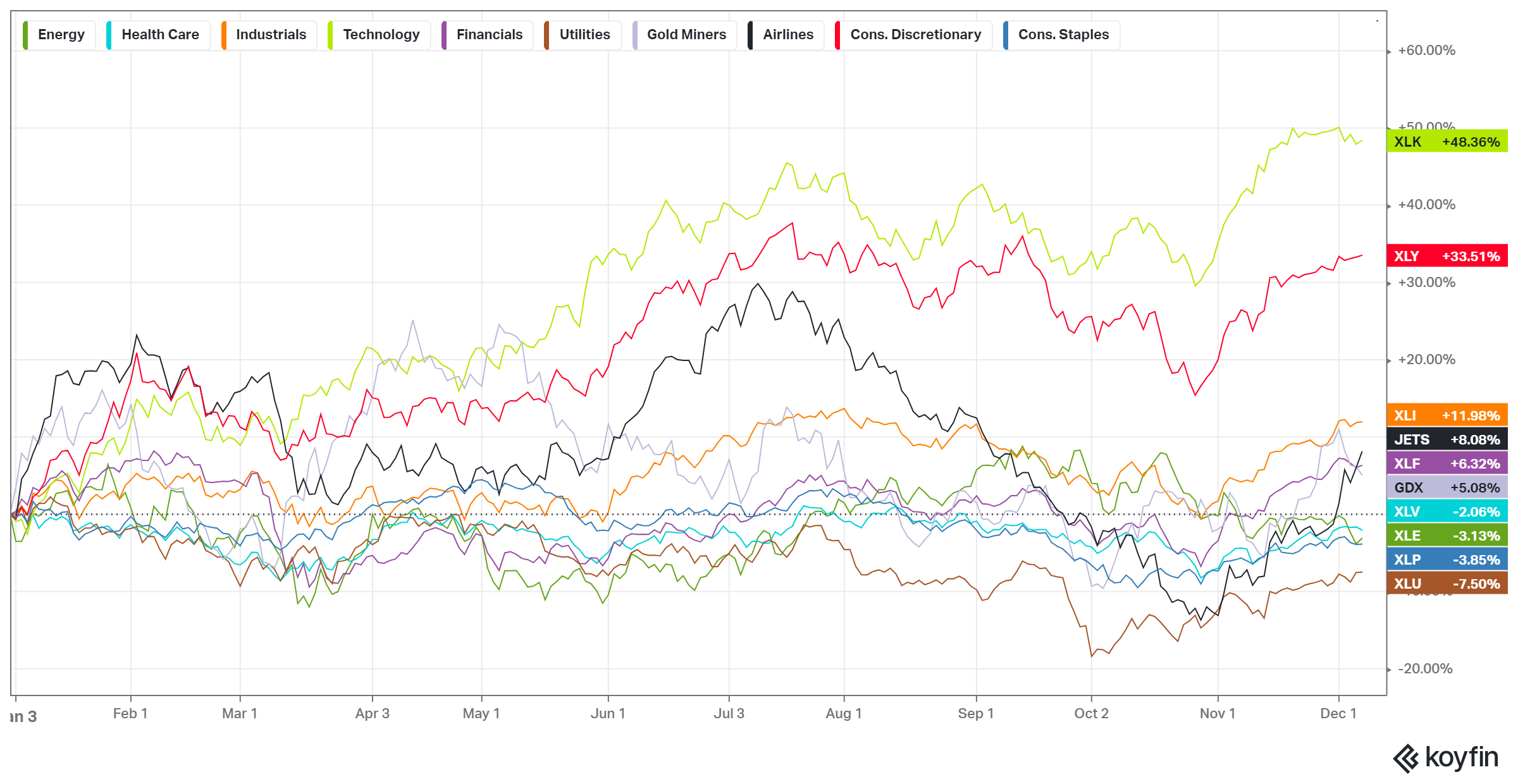

As such, US sector-wise, no wonder US ETF XLY (consumer discretionary) is slightly trailing US [[XLK]] (Tech) YTD:

{kind=link}

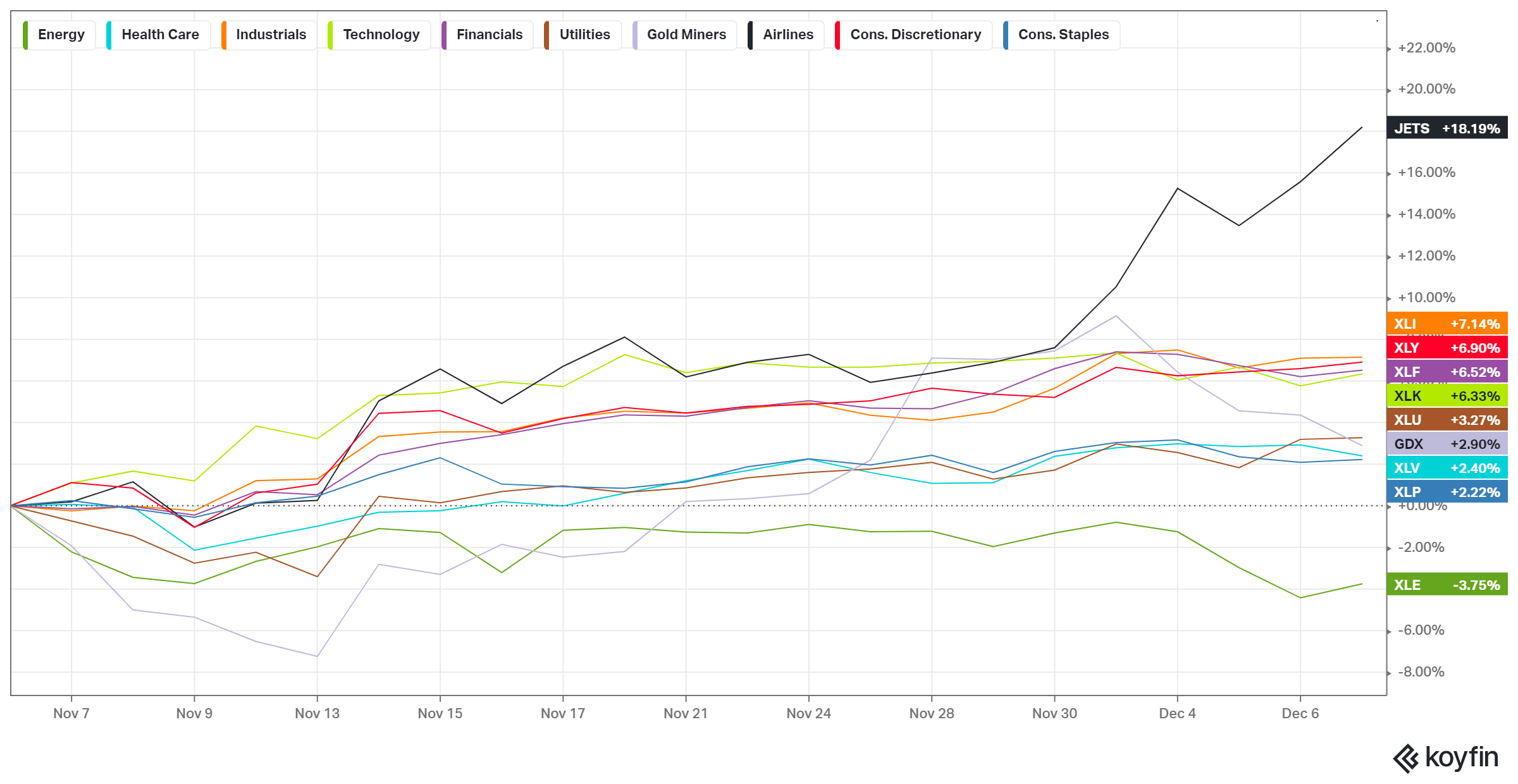

On a one-month horizon, ETF [[JETS]] has been flying above the rest thanks to 2.9 million US airline travelers on November 26, the busiest day for air travel in history:

{kind=link}

On the Tech side, we already confided we kind of like the Chinese battered Tech sector and as such, we have been adding exposure to Alibaba (BABA).

On the Alibaba story, we recommend you follow the take on "valuation" from our business partner Geoffrey Fouvry from GraphFinancials.

Here are a couple of points made by Geoffrey on what we think is a compelling "contrarian" take on the subject of Alibaba:

A lot of investors today have started their career in an environment where credit conditions were loose or extra-loose, they have not seen 2002-2003 or 2009-2011 for many quarters. They have just seen a brief 2020 blip where the name of the game was to "Buy! Buy! Buy!" fast as the money was flowing. Post 2014 what has mattered is not the protection on the downside but the momentum that continuous money printing has favored. To the point where "margin of safety" has disappeared from the Lexicon of investors. In a tight monetary environment (China) you look at the downside FIRST, SECOND and THIRD. You don't get too excited about projections but by the value.

Alibaba has grown its sales and earnings significantly, but that's not what is getting us excited. What is exciting is the nature of the business of AliPay with massive margins and revenues per employee at 1.2 million USD (yes not YUAN but with YUAN salaries), it has expanded by 500 million users since 2020. Granted the Fintech part at Ant Group is probably suffering a bit post ebullience but not the payment business.

The real excitement is the margin of safety/asymmetry. To make money you need not lose it first, because it's mutually exclusive hence the focus on the margin of safety in valuation and a hard-to-replicate business. Try to replicate a 1.5 billion people payment network. Play the augmented web presentation here link ."

By now, you know we like to buy what is "cheap" such as our recommendation to buy [[BTU]] and [[ARLP]] aka coal plays in December 2020. We also have to confide that we have been riding the Uranium play via [[URNM]] and via Kazatomprom stock. For us, Uranium is a long-term play.

In continuation of our previous conversation relating to the gold spread between New York and Shanghai, we continue to see a lot of central banks adding the "barbaric relic" to their reserves, a sign of the ongoing transformation of the monetary system in a growing multipolar world:

Central banks gold purchase (Bank of America - X/Twitter)

Falling real yields and deceleration of US economic growth in true Gibson paradox fashion should continue to support gold prices in 2024:

{kind=link}

As Ray Dalio put it recently:

Watch the value of your money (e.g. dollars) in relation to the prices of other currencies, gold, and goods and services to understand what is really going on with the value of your money and what it buys. If you don't do that, you might fall under the illusion that the things measured in that money (e.g., stocks and bonds) are going up, when the truth is the value of your money is going down."

The money illusion posits that people have a tendency to view their wealth and income in nominal dollar terms, rather than recognize their real value, adjusted for inflation. Irving Fisher reminded us about this concept in his must-read 1928 book before it was popularized by John Maynard Keynes but we ramble again.

For further details see:

Double Entendre