JGH - DSL: NAV Destruction Points To Struggles With The Distribution

2023-11-14 16:32:06 ET

Summary

- The DoubleLine Income Solutions Fund offers a competitive yield of 11.54% compared to other similar funds.

- The DSL closed-end fund's performance has been underwhelming, with a 5.22% decline in share price since the last article on it was published.

- The fund's high exposure to foreign markets provides diversification, but also makes it difficult to predict its future performance.

- The fund's distribution does not appear to be sustainable, as the net asset value has been declining for two years.

- The fund is trading at a premium valuation, which does not appear to be justified considering the risks to the distribution.

The DoubleLine Income Solutions Fund ( DSL ) is a fixed-income closed-end fund that investors can employ as a source of income. The fund performs reasonably well in this function, as its 11.54% yield is comparable to other funds that invest in similar assets:

| Fund |

| Current Yield |

| DoubleLine Income Solutions Fund |

| 11.54% |

| First Trust/abrdn Global Opportunity Income Fund ( FAM ) |

| 12.68% |

| Nuveen Global High Income Fund ( JGH ) |

| 11.07% |

| Western Asset Global Corporate Defined Opportunity Fund ( GDO ) |

| 10.61% |

| BrandywineGLOBAL - Global Income Opportunities Fund ( BWG ) |

| 12.88% |

There may be a few readers who point out that the DoubleLine Income Solutions Fund does not have the highest yield that is available among its peers. That is certainly true, but as we have seen in various previous articles, those funds that have incredibly high yields also tend to come with higher amounts of leverage or more aggressive valuations that expose investors in them to a greater level of risk. Many investors who are interested in purchasing an income-producing asset are retirees or other individuals who do not want to take on excessive levels of risk. As such, this fund's apparent more balanced approach may be attractive.

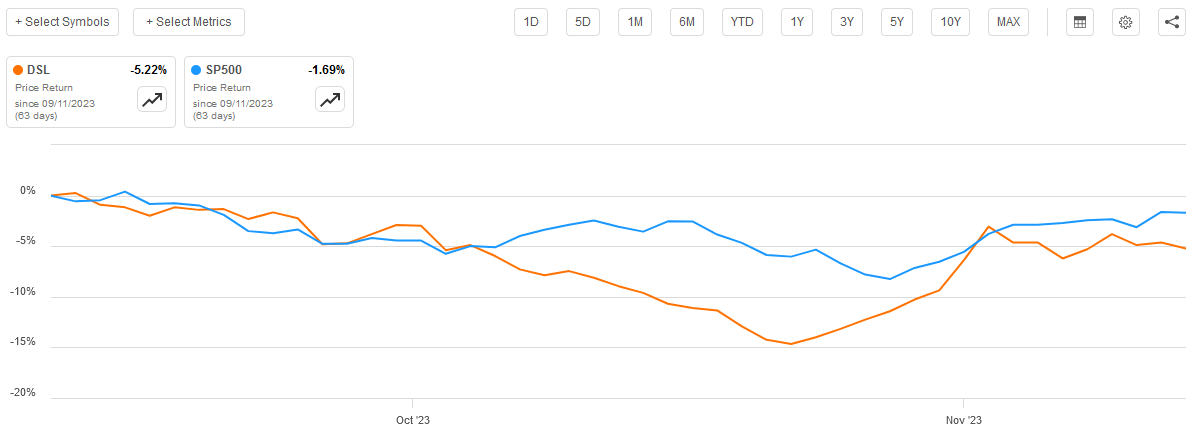

As regular readers may recall, we last discussed the DoubleLine Income Solutions Fund in the middle of September. At the time, my only real complaint about it was that the fund was trading at a fairly large premium compared to its intrinsic value. The fund's performance since that time has not been particularly good though, as its shares are down 5.22% since the date that the previous article was published. This is considerably worse than the S&P 500 Index ( SP500 ), which has only fallen by 1.69% since that date:

{kind=link}

As I have pointed out in the past though, it is best to evaluate closed-end funds in terms of total return, not simply price return. This is because these entities pay out nearly all of their investment profits in the form of distributions. This tends to give them very high yields, and in some cases, these yields can be sufficient to offset declines in the share price. Exchange-traded funds that track indices do not do this because they do not tend to realize capital gains. Unfortunately, in this case, the DoubleLine Income Solutions Fund still underperforms the S&P 500 Index, as investors who purchased shares of the fund at the time that my previous article was published have lost 3.40% of their investment compared to a 1.69% loss had they purchased the S&P 500 Index.

This underperformance relative to the S&P 500 Index may turn off some investors. However, as I have pointed out in a few recent articles, the past several weeks have seen many closed-end funds see their shares sell off far more than is justified by the performances of their portfolios, which has now caused them to offer very attractive valuations to any new investors who are looking to increase their positions. As such, we should have a closer look at this fund to see if this is the case here and whether or not this fund may present an opportunity for investment.

About The Fund

According to the fund's webpage , the DoubleLine Income Solutions Fund has the primary objective of providing its investors with a very high level of current income. This makes a lot of sense when we consider the fund's general strategy. The website explains this strategy:

The Fund will seek to achieve its investment objectives by investing in a portfolio of investments selected for their potential to provide high current income, growth of capital, or both. The Fund may invest in debt securities and other income-producing investments anywhere in the world, including emerging markets.

This description specifically implies that the fund will mostly invest in debt securities, although it does leave things open-ended to a certain degree as some common stocks can be considered "income-producing" investments. However, for the most part, the DoubleLine Income Solutions Fund should be considered a bond fund, as currently 103.27% of the fund's net assets are invested in debt securities:

CEF Connect

There may be some readers who point out that the fund's bond allocation is in excess of 100%. This is certainly true, but it is not really unexpected. One of the defining characteristics of closed-end funds that invest in bonds or other debt securities is that they typically employ a significant amount of leverage to allow them to control more assets than they would otherwise be able to be based on their net assets. This increases the fund's effective yield. After all, compare the 11.54% current yield of this fund to just about any bond index and you will quickly see the impact of leverage. When we consider the incredibly low yields that most bonds have possessed over the past two decades, we can very quickly see why leverage is necessary for any bond fund to be able to deliver a level of income that is acceptable to most income-seeking investors. Unfortunately, the use of leverage also brings risks with it, which we will discuss later in this article.

The fund's focus on the provision of current income makes a lot of sense for a bond fund. As I explained in my previous article on this fund:

As such, it is not especially surprising that the fund's objective would center around current income. This is because bonds and other fixed-income securities provide the overwhelming majority of their investment return through direct payments made to investors, with only a limited potential for capital gains. That makes sense since bonds have no direct link with the growth and prosperity of the issuing company. After all, a company will not increase the amount of money that it pays to its bondholders simply because its income improved.

As I have pointed out numerous times before, bonds have no net capital gains over their lifetimes. When a bond is issued, the investor purchases it at face value. The same investor receives the face value back when the bond is redeemed. Thus, there is no net capital gains potential despite most bond funds claiming that they are endeavoring to earn capital gains for their shareholders.

With that said, there is some potential to earn some capital gains off of bonds by exploiting changes in their prices that are caused by interest rate changes. The DoubleLine Income Solutions Fund only has a 24.00% annual turnover, so it is certainly not engaging in a substantial amount of bond trading, but it is still doing some.

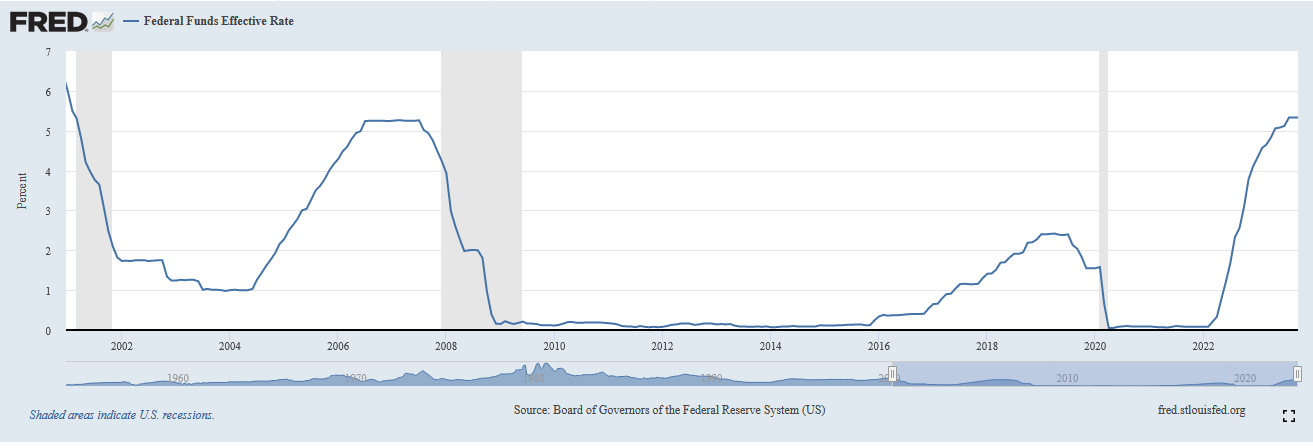

Unfortunately for this fund, it has become much more difficult to obtain trading profits from bonds than it used to be. This is mostly because the Federal Reserve has been raising interest rates over the past two years in an effort to control the very high rate of inflation that is dominating the economy. We can see this quite clearly by looking at the federal funds rate, which is the rate at which the nation's commercial banks lend money to each other on an overnight basis. As we can see here, the effective federal funds rate is currently sitting at 5.33%, which is the highest level that has been seen since February 2001:

{kind=link}

The effective federal funds rate was 0.08% as recently as February 2022, so it has clearly increased at a very rapid pace. This is the reason why bond funds have delivered massive losses to their investors, as this surge in rates has caused bond prices to decline.

However, it is important to note that the federal funds rate only affects American bonds, although it will have some impact on the price of foreign bonds that are denominated in U.S. dollars. This is very important in evaluating the DoubleLine Income Solutions Fund because it invests in bonds that are not issued by American entities (although it does have some American bond exposure). Unfortunately, neither the fund's website nor its fact sheet provides a country-by-country breakdown of the fund's assets. CEF Connect states that 49.04% of the fund's assets are invested in American fixed-income securities and the remainder of its assets are invested in something else:

CEF Connect

This chart shows 49.04% of the fund's assets invested in American fixed-income securities along with 0.60% of its assets invested in American equities. That means that fully 50.36% of the fund's assets are invested in foreign securities. This is a very high allocation to foreign markets for any global closed-end fund. After all, the United States accounts for 70.23% of the iShares MSCI World ETF ( URTH ) and 51.56% of the Bloomberg Global Aggregate Float-Adjusted and Scaled Index ( BNDW ). These weightings far exceed the United States' actual contribution to global economic output, which is a bit less than 25%. As American assets account for such a high percentage of the global indices though, most funds will have outsized exposure to this country. The fact that this fund is somewhat more reasonable with its country allocations is very nice to see, especially for American investors who tend to be overexposed to their home country.

The fact that this fund has very high exposure to foreign markets means that we cannot necessarily use the Federal Reserve's policy as a guiding factor in our analysis of this fund's forward performance. In fact, it is difficult to use the monetary policies of any individual nation to evaluate where the fund's share price or net asset value is likely to go over the coming years. This is because no individual country represents a large enough position in the portfolio to dominate over the others. The United States is by far the biggest right now though, and it is big enough to have a large influence on the fund's overall performance. However, if enough other countries adopted a loose monetary policy rather than a tight one then they could cause the fund's net asset value to go up even if the Federal Reserve is trying to hold American interest rates up.

The fund has also had much less exposure to the United States in the past, so we know that it could adjust its allocation to favor other countries if opportunities abroad begin to look more appealing. For example, the last time that we discussed this fund, the DoubleLine Income Solutions Fund only had a 41.75% weighting to the American fixed-income market and a 0.54% weighting to the American equity market. Thus, the fund has substantially increased its exposure to the United States over the past two or three months. This appears to simply be opportunistic positioning as the fund's management likely expects that American assets will outperform in the near future. However, the fact that it can reduce its American exposure means that we are not being held hostage to the Federal Reserve with this fund, as we would be with most other bond funds. That is something that should appeal to just about any American investor since most Americans who participate in the markets have gotten crushed by central bank policy since the start of 2022.

Leverage

As mentioned earlier in this article, the DoubleLine Income Solutions Fund employs leverage as a method of boosting the effective yield of its portfolio. I explained how this works in my previous article on this fund:

In short, the fund borrows money and then uses that borrowed money to purchase bonds or other income-producing assets. As long as the purchased assets have a higher yield than the interest rate that the fund needs to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, that will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not using too much leverage since that would expose us to too much risk. I do not generally like to see a fund's leverage exceed a third as a percentage of assets for this reason.

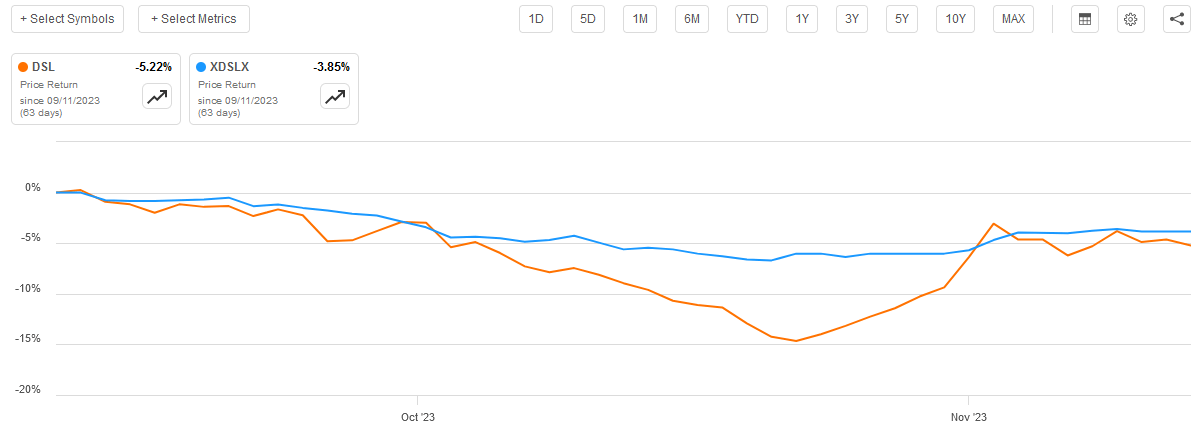

As of the time of writing, the DoubleLine Income Solutions Fund has levered assets comprising 24.54% of its portfolio. This is a slight increase over the 23.87% leverage ratio that the fund had the last time that we discussed it. The increase here is disappointing, particularly in today's high interest-rate world. However, it is very understandable that the fund's leverage would increase considering how its portfolio has performed since the last time that we discussed it. As we can see here, the fund's net asset value declined by 3.85% since the date that the prior article was published:

{kind=link}

This means that the fund's leverage will increase unless the fund actively pays it down. After all, the amount of money that the fund owes does not decrease just because the value of the assets in its portfolio went down.

The fund's leverage still remains well below that of most fixed-income closed-end funds, however. It is also below the one-third maximum that I would normally like to see. As such, we probably do not need to worry about its leverage too much, but we definitely want to keep an eye on it to ensure that it does not keep going up.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the DoubleLine Income Solutions Fund is to provide its shareholders with a very high level of current income. In order to achieve this objective, the fund invests in a portfolio that consists primarily of debt securities issued by entities all over the world. Bonds and other debt securities provide the majority of their investment returns in the form of direct payments to their investors, which the fund collects on behalf of its shareholders. The fact that this fund is able to invest in foreign assets, particularly emerging markets, helps a lot here because emerging markets tend to have substantially higher interest rates than most developed nations. As such, the presence of these securities in the fund's portfolio provides it with a higher level of income than it could obtain simply by investing in developed market bonds. The fund then applies a layer of leverage to allow it to purchase more bonds than its net assets would otherwise allow. The fund collects all of the money that it receives from these bonds and pays it out to its shareholders, net of the fund's own expenses. It might be expected that this would result in the fund's shares having a very high yield.

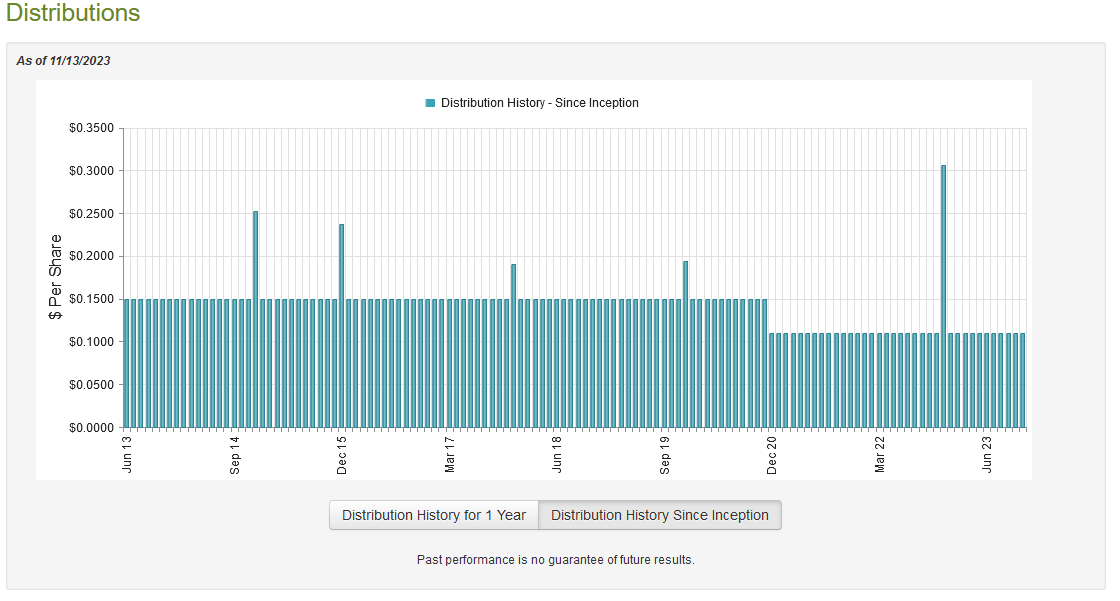

This is certainly the case, as the DoubleLine Income Solutions Fund currently pays a monthly distribution of $0.11 per share ($1.32 per share annually), which gives it an 11.54% yield at the current price. As we saw in the introduction, this yield is competitive with other closed-end funds that invest in the global bond market. It is also a substantially higher yield than that provided by pretty much any American market index. Unfortunately, this fund has always been consistent with respect to its distribution, but it has generally done better than other debt funds:

{kind=link}

The big thing that we see here is that the fund cut its distribution back in December 2020. Otherwise, it has been very stable over time. That is surprising, as this is a task that very few bond funds have been able to accomplish considering how sensitive the securities that they hold are to interest rates. The fact that this one is a global fund does help a bit, but all major nations have increased their interest rates over the past two years so we would expect that the fund must have taken some losses. This is, in fact, the case as the DoubleLine Income Solutions Fund's net asset value is down 35.83% over the past two years:

{kind=link}

The fact that it has not cut its distribution is quite confusing when we consider this. We should have a look at the fund's finances in order to determine how sustainable its current payout is likely to be.

Unfortunately, we do not have an especially recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the six-month period that ended on March 31, 2023. As such, it will include no information about the fund's performance over the past seven months. That is very disappointing, as quite a lot has happened over that period, including a change in the market's attitude towards rates. The first half of this year was characterized by an incredible amount of optimism that the Federal Reserve would backtrack with respect to its monetary policy and cut interest rates. While this fund does not invest solely in the United States, this still could have given it the potential to earn some profits as investors were bidding up the prices of American bonds. This all changed in mid-July though, and since that time investors appear to have resigned themselves to the likelihood that high interest rates will be with us for a very long time. This latter period will not be reflected in the fund's most recent financial report, which is disappointing as its net asset value has declined since July and that may have put some pressure on its ability to maintain its distribution.

During the six-month period, the DoubleLine Income Solutions Fund received $76,349,106 in interest and $1,094,798 in dividends from the assets in its portfolio. This gives the fund a total investment income of $77,443,904 over the period. The fund paid its expenses out of this amount, which left it with $57,906,823 available for the investors. That was, unfortunately, not nearly enough to cover the $87,363,079 that the fund paid out in distributions over the same period. At first glance, this is almost certainly going to be concerning because the fund is unable to cover its distribution solely using the income that it collects from the bonds in its portfolio. We normally like fixed-income funds to be able to cover their distributions solely out of net investment income.

With that said, there are other methods that the fund can employ to obtain the money that it needs to cover the distribution. For example, it might be able to take advantage of swings in bond prices that come with interest rates and earn some profits by trading bonds. The fund actually had mixed results at this task during the period. The DoubleLine Income Solutions Fund reported net realized losses of $125,488,623 over the period but it managed to offset these with $137,688,303 net unrealized gains. That was not nearly enough to cover the distribution though, and the fund's net assets declined by $13,970,093 over the period after accounting for all inflows and outflows. This is concerning, to say the least.

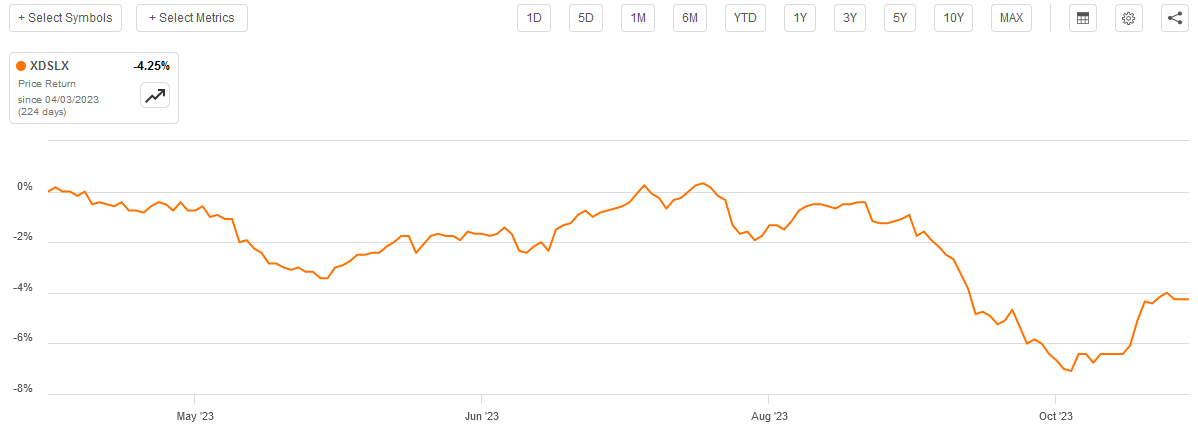

The fund's decline in net assets comes on the heels of a $637,188,554 net asset decline in the full-year period that preceded these results. Thus, the fund's net assets have declined for eighteen straight months. It seems likely that the fund has continued to see losses since the period covered by this report. As we can see here, the fund's net asset value has fallen by 4.25% since April 1, 2023:

{kind=link}

As such, it appears almost certain that the fund has failed to cover its distribution over the past eight months. It is very difficult to see how it can possibly sustain this level of capital destruction going forward. The fund will almost certainly have to cut its distribution in the very near future.

Valuation

As of November 13, 2023 (the most recent date for which data is available as of the time of writing), the DoubleLine Income Solutions Fund has a net asset value of $11.48 per share but the shares currently trade for $11.84 each. This gives the fund's shares a 3.14% premium on net asset value at the current price. That is a lot worse than the 2.50% discount that the shares have had on average over the past month. It also seems like a lot to pay for a fund that may be forced to cut the distribution in the very near future.

It is probably best to avoid this fund for now, especially at a premium price. It may be possible to justify purchasing it if you can get it at a substantial discount, but that seems pretty unlikely considering that the best price that this fund has had over the past year was a 7.79% discount.

Conclusion

In conclusion, I want to recommend the DoubleLine Income Solutions Fund, as it does have some very nice features. In particular, the high degree of global exposure is very nice as it allows American investors to obtain the international exposure that most portfolios lack. The fund's globally diverse portfolio should reduce the impact of any single nation's monetary policy on the fund as a whole.

However, it is very hard to see how DoubleLine Income Solutions Fund can possibly maintain its distribution considering the level of net asset value destruction that is going on here. When we combine this with a premium valuation, it makes no sense to purchase right now.

For further details see:

DSL: NAV Destruction Points To Struggles With The Distribution