DTM - DT Midstream Goes Natural (Gas)

2023-10-22 06:53:14 ET

Summary

- DT Midstream is a recently spun-off midstream company with operations in areas known for high dry gas production.

- The company is well-positioned to benefit from increasing export capacity in North America.

- The relatively low yield and need for cash to fund capital projects suggest potential for future growth that exceeds typical midstream expectations.

- Finances appear to be conservative.

- The short public history and relatively expensive valuation are risk factors.

DT Midstream ( DTM ) is unusual in that the operations are located in areas known for a lot of dry gas production. The company is also a recent spinoff. Now, it happens that North America has a lot of export capacity under construction. Therefore, this midstream company is in a position to benefit from that increasing export ability because upstream demand for more capacity should grow as North American Prices join the world market.

Short Public History

DTM Midstream has a relatively low yield for a midstream company.

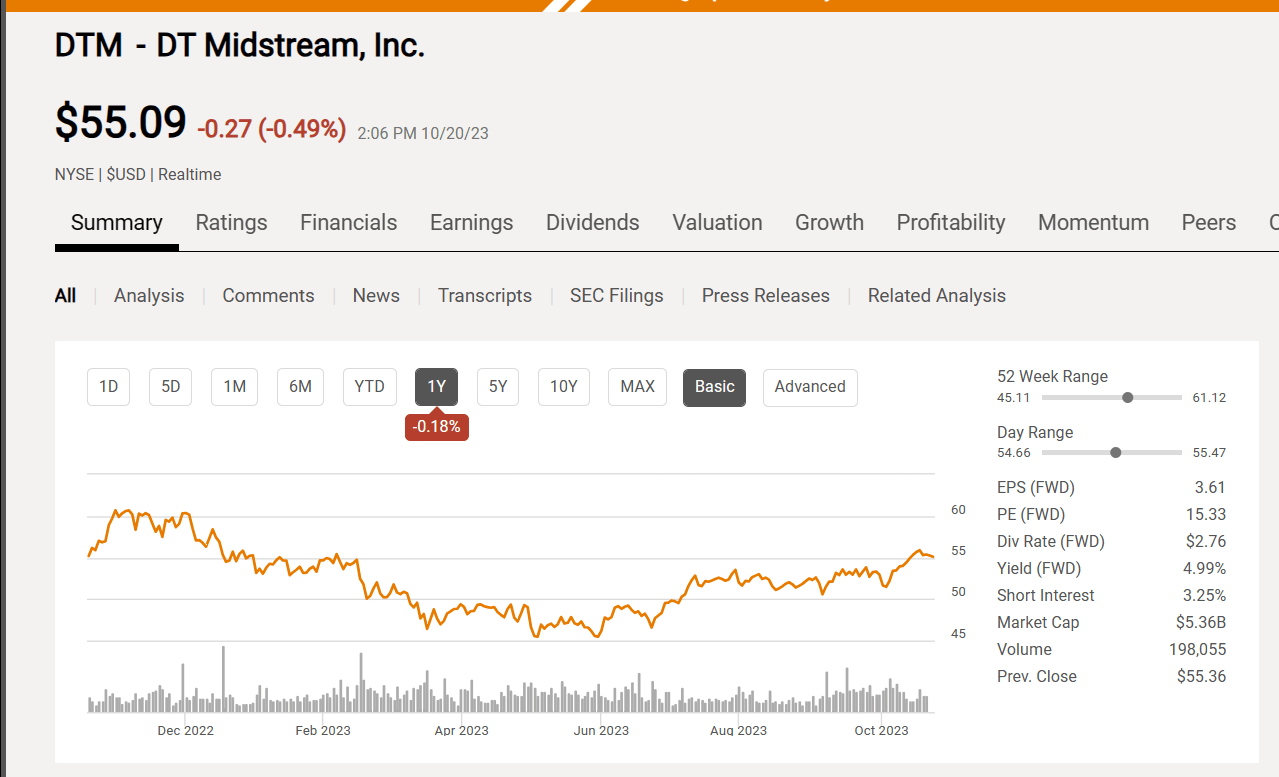

DT Midstream Common Stock Price History And Key Valuation Measures (Seeking Alpha Website October 20, 2023)

{kind=link}

Normally, I would like a five-year history as a public company as a way to reduce investment risk. There is also the relatively, low yield when a lot of more established midstream companies have higher yields. Any change in the market perception of this company could prove to begin a major valuation readjustment.

So, the market clearly recognizes some of the future prospects of this midstream company. Clearly, management recognizes the possibility of a lot of capital projects because the dividend payout is a relatively low amount of earnings.

Dividends paid were listed at $67 million. This is a relatively small fractio n of the $125 million calculated for Free Cash Flow. The six-month calculation would be more conservative. Like the low yield, this also points to a need for cash to fund capital projects. Management is telling potential investors that this company has a lot of potential growth projects on its plate.

This is not going to be the typical midstream investment where dividends or distributions make up most of the investment income.

Debt

Similarly, as a spinoff, this division has a major (some would prefer significant rather than major) customer, and that customer for a long time was DT Energy ( DTE ). Now this was an atypical setup for me in that most major customers I follow are upstream companies. Here, it is a utility.

But that means the midstream operations service the basin rather than what was the parent company, even though sales were likely to head to the parent company utilities. Therefore, there is still one main customer. It is on the sales side. That could change now that DT midstream is independent.

The debt levels are typical for a midstream company that was until recently controlled by a parent company. Midstream companies with a parent company like this recent spinoff often have some of the lowest debt levels in the industry. That often makes them much safer investments from a financial viewpoint.

Similarly, the midstream business is often seen as the utility business of the oil and gas industry. It makes sense why a utility business would build a midstream business that (itself) is seen as a relatively steady part of the oil and gas industry.

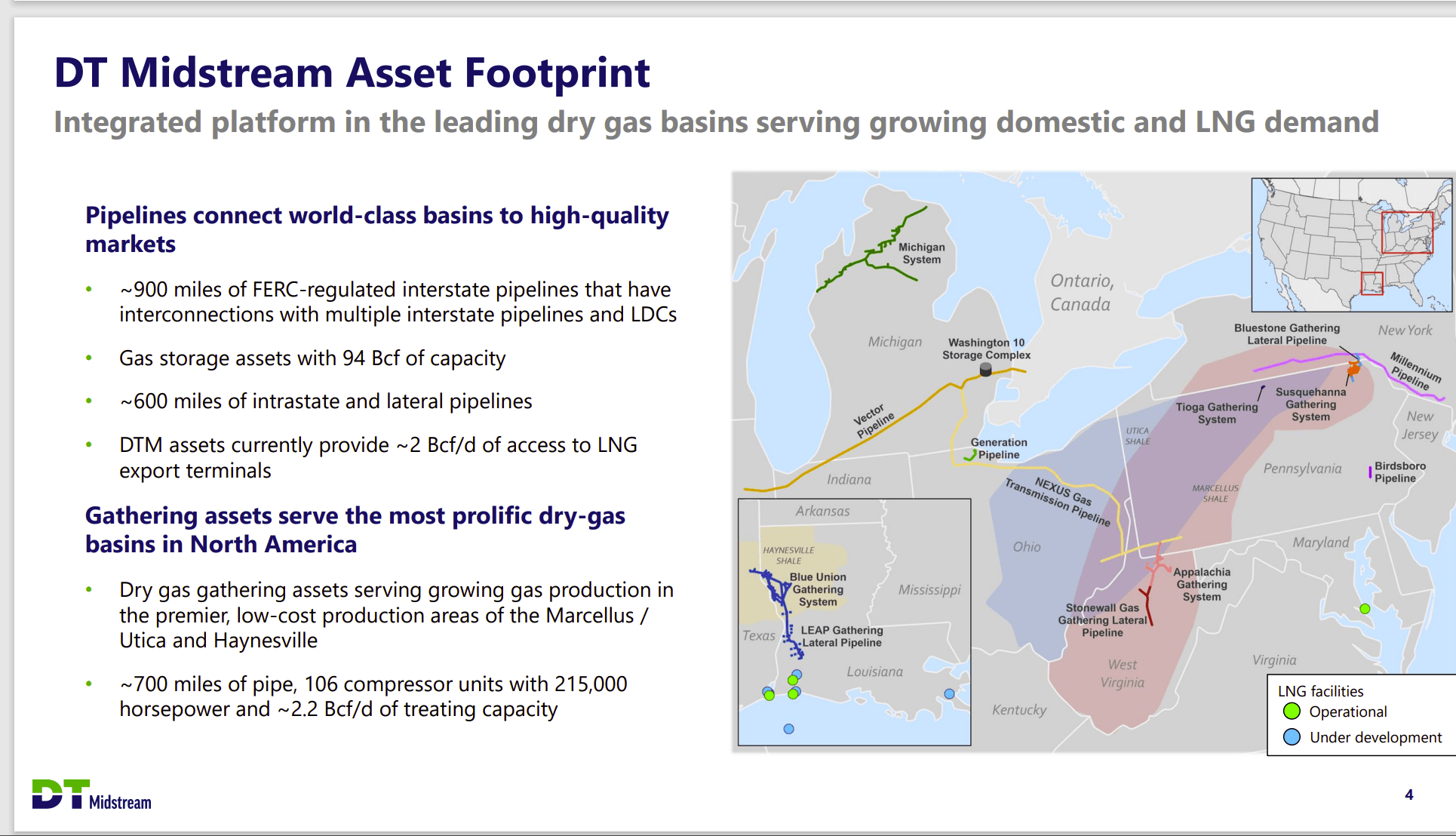

Map Of Operations

This midstream company hooks up to other pipelines that enable the natural gas to go to other markets that may provide better pricing.

DT Midstream Areas Of Operation (DT Midstream Presentation At Wolfe Research Utilities, Midstream & Clean Energy Conference September 29, 2023)

{kind=link}

With the connections to other pipelines noted, this company likely going to be a beneficiary of the growth of natural gas production due to the stronger pricing as export capacity climbs.

Minimum take-or-pay commitments should help during times of pricing weakness. The Haynesville, in particular, has been noted in the past to be a swing production area. Therefore, production in this basin will be more sensitive to the upstream business cycle than is the case in other basins.

The Permian, in particular, bases the production decisions on oil (usually) and so natural gas production will continue regardless of the natural gas pricing conditions. That is not going to be the case when the upstream companies are located in dry gas production areas. Therefore, this midstream company may have a different business cycle pattern than is the case for many companies I follow that are primarily located in oil-focused production areas (and then provide natural gas services for the accompanying natural gas production).

The Marcellus does have a dry gas production area. But that basin also has rich gas production, where the added value of liquids production could permit production to continue to rise because the liquids provide need profitability during times of weak natural gas pricing.

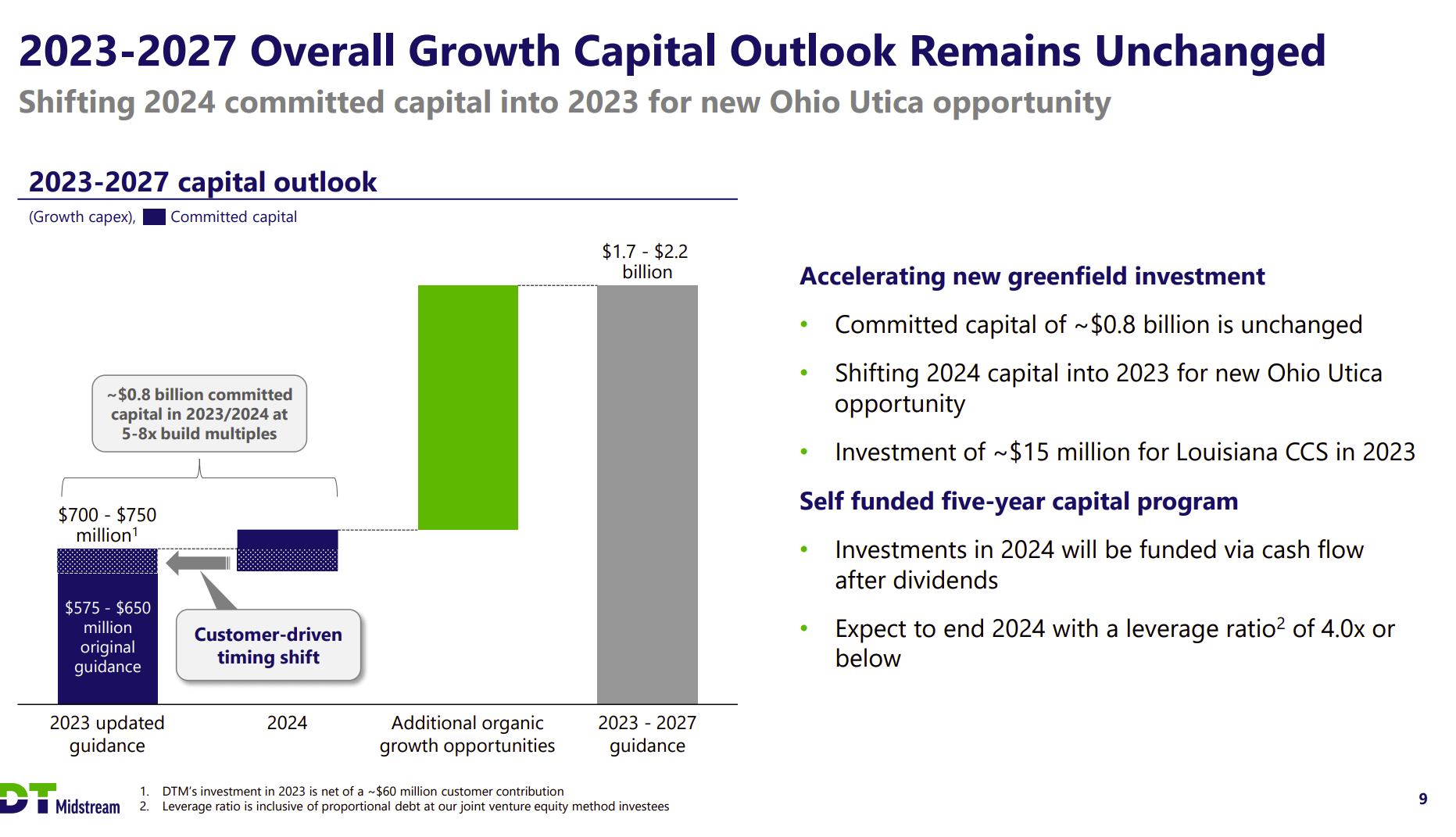

Capital Projects

This relatively small midstream company has a healthy backlog of growth projects. What is unknown is the profit effects of these projects because the profitability often varies by project.

DT Midstream Capital Project Guidance (DT Midstream Presentation At Wolfe Research Utilities, Midstream, & Clean Energy Conference September 29, 2023)

{kind=link}

This company may well be an acquisition candidate for its exposure to a part of the country that a lot of midstream companies just do not have exposure to (or not enough compared to what they may need).

The projected leverage shown above is definitely on the conservative side. As this company grows away from DT Energy, now that it is independent, that leverage may be a key driver in raising the debt rating more in the future. That could lower future interest expense and make more growth projects appealing.

Key Ideas

DT Midstream is a corporation that provides midstream services to two relatively under-covered basins. Both of these basins could experience considerable production growth in the future.

The company has fairly conservative finances for the midstream industry. Therefore, management has the ability to grow at whatever rate they choose.

The dividend yield is below average, and the stock is on the expensive side. So, an inability to meet future market expectations could result in a negative revaluation. However, it does appear that growth prospects are far more likely and will at least meet market expectations.

For me, management is the most important consideration of any investment decision. This management has just experienced a major organization change in the form of a spin-off. Whether this management can be as successful as it was as a part of DT Energy remains to be seen. The lack of history as a standalone company has to be a risk factor.

This company would likely be considered a buy or strong buy consideration for those willing to take on the additional risk as noted above. For most, a more established midstream company would prove to be a safer investment choice. There are a lot of cheaper midstream companies that have a higher distribution than is the case here. Therefore, one has to justify superior growth prospects from the given backlog with an already elevated market valuation. The finances are conservative, and management experience appears to be adequate. That makes this investment probably unsuited to typical investors and new investors.

For further details see:

DT Midstream Goes Natural (Gas)