DTM - DTE Energy: Delivering To Shareholders

2023-12-21 23:32:45 ET

Summary

- DTE Energy Company's shares have been rebounding as risk-free rates have receded, though the shares still remain fairly attractive to consider a long-term investment.

- The company has updated its earnings outlook for 2023 and 2024, with a slight decrease in guidance for 2023, but they are anticipating growth to return for 2024.

- DTE has increased its dividend by 7.1%, delivering to shareholders thanks to the consistent earnings that the company is able to produce as a utility.

Written by Nick Ackerman

DTE Energy Company ( DTE ) is a multi-utility company with operations throughout Michigan. While it is a multi-utility company that offers both electricity and natural gas services, electricity is the largest segment of its business.

Shares of this otherwise mostly boring utility company have performed rather weakly since our last update . However, the utility space overall performed rather poorly during this time due to significantly higher rates as the Fed aggressively raised its benchmark rates.

DTE Performance Since Prior Update (Seeking Alpha)

So, while the S&P 500 was up significantly during this time, overall utilities were down around 10% in this period, using the Utilities Select Sector SPDR ( XLU ) as the benchmark. That puts DTE's results in line with the sector in terms of performance. Overall, it isn't too disappointing, considering I've owned this name personally for years, and it's doing exactly what I would expect: continuing to pay increasing dividends. Capital appreciation over the longer term with a utility company would otherwise be a bonus. Given that they generally are steady earnings over the long term, it often leads to gradual appreciation over the years.

That being said, higher interest rate environments are one thing that can really disrupt this area of the market. As risk-free Treasury Rates backed off more recently, that has helped ease up the pressure on the space. It makes it a tempting place to put capital to work, especially if one is expecting a softer economy next year. Utilities tend to deliver in good times and bad times. Even during this higher rate environment, earnings have been more or less steady even if the share price doesn't reflect this.

Utilities are mostly viewed as income-oriented investments, so when risk-free rates offer more compelling yields with no risk, investor dollars will move to those instruments. Additionally, operating utilities tend to take a lot of CAPEX to maintain the infrastructure, and they tend to utilize more debt than other sectors. This was partly because it was so cheap for so long and partly because their normally steady operations make them reliable for repaying debt.

Besides the economic and interest rate environment change since our last update, the company more recently updated its earnings outlook for the remainder of 2023 and gave some guidance for 2024. With this most recent update, the company also announced its dividend hike right on schedule.

Business Update

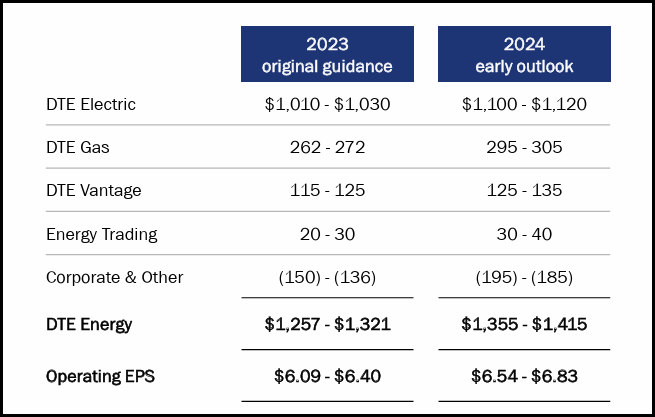

When the company announced its latest updates, it trimmed its outlook for 2023 operating EPS but did up its guidance for 2024 and maintained its operating EPS growth at 6 to 8% through 2028.

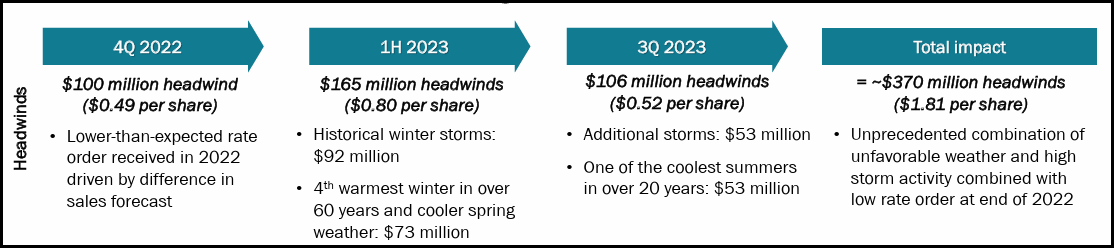

Cutting their 2023 guidance to $5.65-5.85 was actually announced in early November. They missed their Q3 results and took down their guidance for the remainder of the year. They noted "unprecedented operating earnings headwinds." This was, of course, as it usually is for this sector, primarily related to weather. They laid out in the first half of 2023 that it was historical winter storms, the 4th warmest winter, and a cooler spring. For Q3, they just summed it up as "additional storms."

{kind=link}

However, with this, they noted how they overcame and offset a significant portion of these operating EPS headwinds so it wasn't more damaging for the year. That primarily included $1.29 per share savings of "one-time O&M actions" and "created opportunities throughout the portfolio."

With $3.76 in adjusted EPS in the bank through the first nine months of the year, the company would need to deliver $1.99 for the final quarter of the year.

Heading into 2024, they are anticipating operating EPS of $6.54 to $6.83. They highlight that this would imply around a 7% growth outlook at the midpoint from the original 2023 guidance. However, from the reduced guidance midpoint, it would actually suggest growth of over 16% year-over-year.

{kind=link}

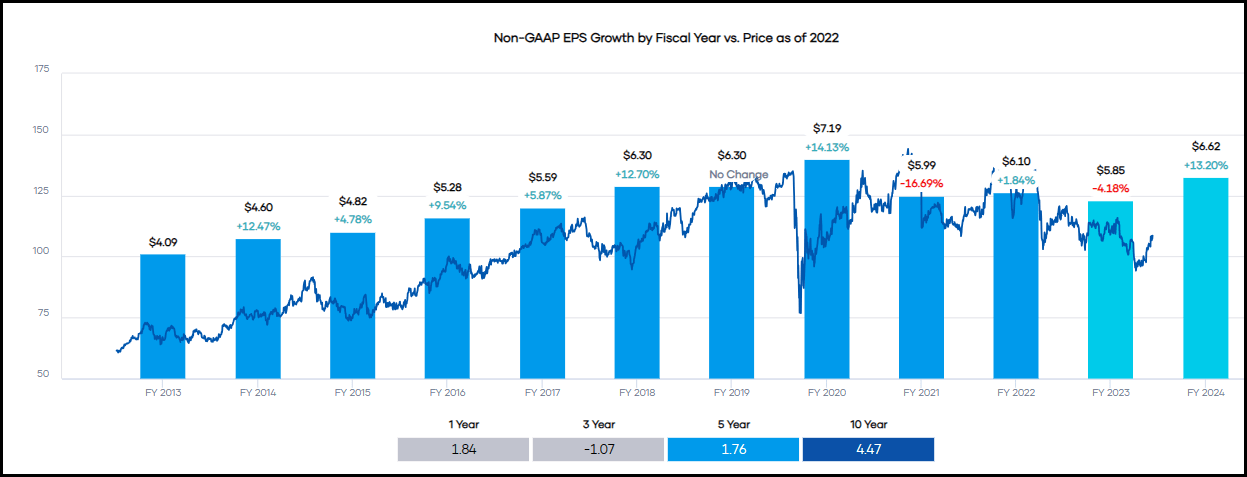

Analysts are looking for similar next year in terms of earnings with adjusted EPS coming in at $6.62. This is just below the midpoint of $6.69 on this early outlook. The company has missed earnings expectations in 5 out of the last 16 quarters, with the latest Q3 results being one of the largest downside surprises. However, like most companies, they still often exceed expectations.

{kind=link}

Part of driving earnings is the regulated rate increases that they are able to put into place regularly. Although the Michigan Public Service Commission approved what was only around 60% of the increase requested , this was information known prior to the company providing this earnings outlook. So that shouldn't be a big disruption in their outlook for earnings next year.

In addition to these rate increase requests, additional demand and population growth can also help provide additional connections and growth through more consumers. Michigan's population has been trending higher , albeit one of the slowest growths of the states that are growing but still slowly but surely.

Investment Update

Coming with the updated guidance was also an increase in CAPEX investments. They boosted their total expected investment plans to $23.7 billion from $21.6 billion. This was for both electric and gas combined from 2024 through 2028, with electric spending to come in at $20 billion of the forecast.

Again, similar to any other utility company that operates in 2023, much of that spending is going toward renewable projects. The company still powers a significant part of its energy from coal, but it is now less than half, with the anticipation that it'll be completely removed by 2033. Additionally, in 2029, they are anticipating that the renewable sleeve will be the largest source of their generation mix, just edging out natural gas.

DTE Generation Mix Forecast (DTE Energy)

Despite not being a state quite known for its sunshine and wind sources, I can confirm, as a Michigan resident, that we do have both of these. Wind off the Great Lakes could be one particularly interesting prospect that was in development, perhaps aptly named "Icebreaker ." That said, the project has been put on hold due to "rising costs and other challenges" that have "dimmed its chances of success."

Dividend Update

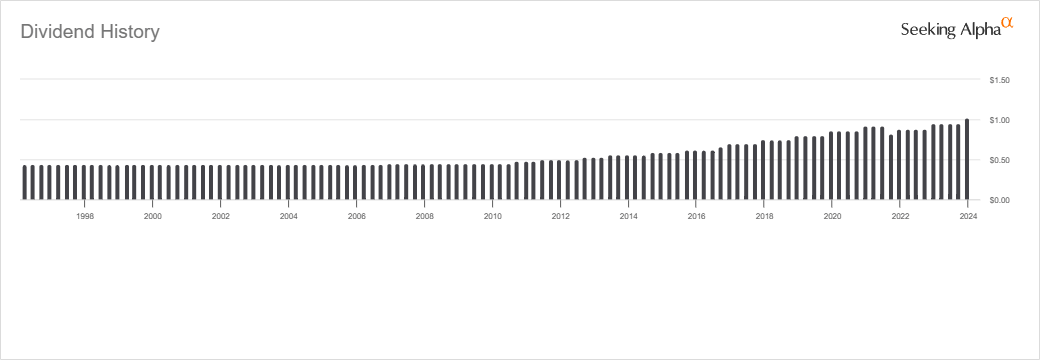

The company also increased its dividend upon announcing the new business outlook. This bumped it up from $0.95 per quarter to $1.02, good for a 7.1% increase. This was only a slight decrease from last year's bump, which was good for a 7.63% raise. Given the soft earnings for this year, it is still a very welcomed increase.

When adjusted for their spin-off of DT Midstream ( DTM ) in 2021, this sets it up to have growing dividends for 14 years since starting the increases in 2010. Prior to this, the company had held its payout steady for many years. They've also noted that they have paid dividends for over 100 consecutive years.

{kind=link}

The EPS payout ratio comes out to around 61% based on their next year's midpoint guidance.

While the company produces plenty of cash from operations, all of that cash and more was spent on CAPEX for 2023. Meaning that would push free cash flow negative for 2023.

DTE Cash Flow (DTE Energy)

Therefore, this results in the issuance of more debt and/or shares. They are targeting between $0 and $100 million in equity issuances through 2026, so they would be relying more on debt for operations and dividends.

DTE 2023 Capital Investments and Dividends (DTE Energy)

That's why lower rates would be particularly welcomed, and rate cuts into next year could help the company out. For what it's worth, this is an investment-grade-rated company with an otherwise strong balance sheet with consistent earnings and growth. As a company grows, so too can its debt load.

DTE Credit Rating (DTE Energy)

Conclusion

Overall, DTE has delivered rather solid results for investors looking to grow their income over the years. As a utility company, it's a fairly boring operation, and that is sometimes the exact type of business exposure we want in a portion of our investment portfolios. Utilities can be great for defensive positioning in one's portfolio due to the boring and steady nature of earnings, even during economic downturns.

The company's shares have come off the latest lows when risk-free rates receded; however, it still remains fairly attractive relative to its historical valuation range. Should rates continue to sink lower, that could potentially be a tailwind that could keep pushing the momentum of the share price upward.

For further details see:

DTE Energy: Delivering To Shareholders