TTE - DTH: Valuation Return And Distribution Metrics Are Unattractive

2023-06-26 11:37:57 ET

Summary

- WisdomTree International High Dividend Fund holds over 500 high-yield stocks from developed countries.

- 63% of assets is in 5 countries and 40% is in 2 sectors.

- Valuation is unattractive relative to one of its main competitors.

- The fund has lost over 40% in share price since 2008.

- Moreover, distribution growth couldn’t keep pace with inflation.

This article series aims at evaluating ETFs (exchange-traded funds) regarding past performance and portfolio metrics. Reviews with updated data are posted when necessary.

DTH strategy and portfolio

WisdomTree International High Dividend Fund ( DTH ) started investing operations on 06/16/2006 and tracks the WisdomTree International High Dividend Index. It has 538 holdings, a distribution yield of 5.7% and a total expense ratio of 0.58%. It pays quarterly distributions.

As described by WisdomTree , to be eligible in the index companies must:

- pay regular cash dividends,

- be incorporated in Japan, 15 European countries, Australia, Israel, Hong Kong or Singapore,

- have a market capitalization of at least $200 million and an average daily dollar volume of at least $200,000.

The top 5% ranked by dividend yield and the bottom half of a risk ranking based on momentum and quality metrics are excluded. Then, companies ranking in the top 30% by highest dividend yield are selected for inclusion. They are excluded when they fall out of the top 35% by dividend yield. Their weights are adjusted based on dividends. The index is reconstituted once a year.

Components are mostly large and mega-cap companies (about 75% of asset value). Australia and the U.K. are the heaviest countries in the portfolio, almost tie (15.2% and 15.1%, respectively). They are followed by Japan (12.2%), France (10.4%) and Germany (10.1%). Other countries weigh less than 8% individually and 37% in aggregate. The next chart includes all countries with a weight over 1%, which represent 96% of the portfolio.

DTH country allocation (chart: author with WisdomTree data.)

The fund is heavy in financials (24.9% of assets), and to a lesser extent in materials (15.1%). Other sectors are below 10%. Technology is almost ignored.

DTH sectors ( chart: author with WisdomTree data.)

I will use as a benchmark one of the fund’s largest competitors among non-hedged ex-US dividend funds: iShares International Select Dividend ETF ( IDV ). IDV expense ratio is a bit lower (0.49%) and it has a much higher trading volume (770k vs. 50k shares/day on average). DTH is significantly more expensive regarding the usual valuation ratios, as reported in the next table.

| DTH |

| IDV |

| P/E TTM |

| 7.73 |

| 5.24 |

| Price/book |

| 1.08 |

| 0.82 |

| Price/sales |

| 0.81 |

| 0.72 |

| Price/cash flow |

| 4.8 |

| 4.1 |

Data: Fidelity

The top 10 holdings, listed in the next table, represent 24.3% of asset value. Exposure to BHP Group is over 5%. Risks related to other companies are moderate. IDV also holds BHP Group, but other top holdings are different. Concentration is similar: about 5% in the top name and 28% in the top 10.

For convenience, U.S. tickers are listed below, whereas the fund holds stocks in primary exchanges.

| US Ticker |

| Name |

| Primary Ticker |

| Weight |

| EPS growth %TTM |

| P/E TTM |

| P/E fwd |

| Yield% |

| BHP Group Ltd. |

| BHP AU |

| 5.67% |

| 19.47 |

| 7.55 |

| 10.37 |

| 8.94 |

| Novartis AG |

| NOVN SW |

| 3.83% |

| -69.76 |

| 30.79 |

| 14.87 |

| 3.47 |

| TotalEnergies SE |

| TTE FP |

| 2.86% |

| 24.93 |

| 6.73 |

| 5.48 |

| 5.22 |

| HSBC Holdings plc |

| HSBA LN |

| 2.36% |

| 97.86 |

| 6.78 |

| 6.23 |

| 5.49 |

| Rio Tinto |

| RIO LN |

| 2.30% |

| -40.58 |

| 8.17 |

| 8.70 |

| 7.75 |

| Mercedes-Benz Group AG |

| MBG GR |

| 1.86% |

| -39.30 |

| 5.39 |

| N/A |

| 7.33 |

| Sanofi |

| SAN FP |

| 1.39% |

| 18.88 |

| 15.28 |

| 11.84 |

| 3.56 |

| British American Tobacco |

| BATS LN |

| 1.37% |

| -13.14 |

| 9.35 |

| 6.91 |

| 8.16 |

| Bayerische Motoren Werke AG |

| BMW GR |

| 1.33% |

| -47.58 |

| 6.56 |

| 6.58 |

| 7.81 |

| BP p.l.c. |

| BP/ LN |

| 1.31% |

| 257.44 |

| 4.10 |

| 5.85 |

| 4.35 |

Fundamental data: Portfolio123

Past performance

The next chart compares total returns of DTH and IDV since 1/1/2008. DTH has lagged its competitor by about 16% in 15 years. The difference in annualized return is less impressive: less than one percentage point.

DTH vs. IDV since 1/1/2008 (Seeking Alpha)

{kind=link}

However, DTH has outperformed in the last 12 months:

DTH vs. IDV, trailing 12 months ( Seeking Alpha)

{kind=link}

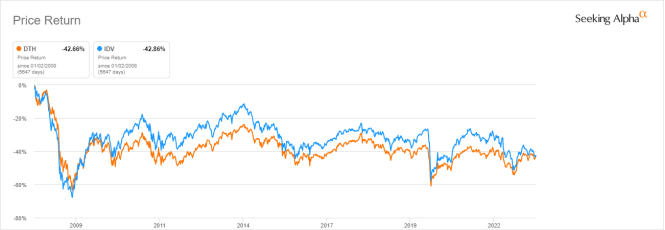

Both funds have suffered a decay in share price of almost 43% since 2008:

DTH vs. IDV, share price return (Seeking Alpha)

{kind=link}

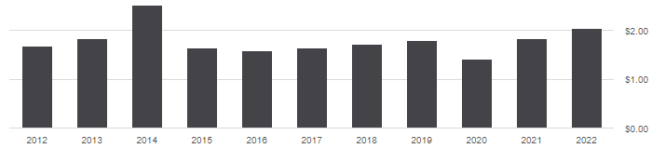

The annual sum of distribution has increased from $1.69 to $2.04 per share between 2012 and 2022. This dividend growth of 20.7% is below the cumulative inflation in the same time: about 29%, based on CPI. Our benchmark IDV has not done much better: 22.1%.

DTH distribution history (Seeking Alpha)

{kind=link}

Takeaway

WisdomTree International High Dividend Fund holds over 500 high-yield stocks from developed countries. About 63% of asset value is in five markets (U.K., Australia, Japan, France, Germany) and 40% is in two sectors (financials and materials). Valuation ratios are unattractive compared to its larger competitor iShares International Select Dividend ETF. DTH has suffered a share price decay over 40% since 2008 and distributions couldn’t keep pace with inflation since 2012. However, our benchmark IDV has not performed significantly better. This issue is not specific to these two funds: many high-yield ETFs have suffered significant capital decay over the years.

For further details see:

DTH: Valuation, Return And Distribution Metrics Are Unattractive