WMG - East 72 Dynasty Trust - Bolloré SE: The Most Interesting Company In The World

2023-07-15 06:30:00 ET

Summary

- If there is a more interesting company on the planet than the French conglomerate Bolloré, we are yet to find it.

- The Bolloré story in the public sphere dates from 1985 with the IPO of Bolloré Technologies.

- On any reasoned analysis, Bolloré shares are extraordinarily cheap.

The following segment was excerpted from this fund letter.

Bolloré ( BOIVF ): à 201 ans, l'entreprise la plus intéressante du monde [2]

"Je remercie Dieu que Google Traduction ait été inventé" (I thank God that Google Translate was invented)

From the viewpoint of financial structure, rather than ((say)) technology innovation, if there is a more interesting company on the planet than the French conglomerate Bolloré, we are yet to find it.

In its current form, Bolloré is a 40+ year history and playbook of every investment banking skill ever taught: cheap acquisitions, expensive sales, spin-outs, squeeze-outs, arguments with regulators, corporate raids and greenmail; buybacks, share swaps, buying then selling, selling than buying, and growth from the ground up. Political connections and disconnections. A supposedly retired patriarch who has moved upstairs to the "passive" controlling entity in a separate building adjacent to the Bois de Boulogne. It's also a structure that is rarely seen and dissuades the lazy analyst; it's not a Brookfield with part subsidiaries and management fees, but an entanglement born of paranoia over control, a relationship with a special investment banker and an acquisition of a bumbling establishment bank which itself had compartmentalised everything into over 800 companies.

To do justice to Bolloré's full history would require an encyclopaedic-sized manuscript. No one has written it yet [3] since it requires not only the skill of writing, the genius of accounting and math, and a preparedness to irritate a significant media owner. You have to track back through public archives which are not always in good order from the relevant period; to be fair, given legendary French bureaucracy, some actually are! In contrast to the myriad takes on Berkshire Hathaway ( BRK.A , BRK.B ) - an enterprise built on enviable stock investment skills and business acquisitions, not least to provide insurance cash flow - Bolloré is the company enterprising investment banking students at business schools around the world should study.

Bolloré has been fuelled by a sense of history, strong organic growth, and smart acquisitions, partly funded by spectacular corporate raids in the 1980s and 1990s. It's a bit of an anti-establishment company - due to its Brittany roots - which has picked off (some of) the upper echelons of corporate France and itself become the establishment - a little like the planet's current richest individual, Bernard Arnault with whom there is a mild intertwining of interests [4] .

Moreover, when you play in the Bolloré family stadium, you play by their rules. Share prices in the Bolloré complex tend to move in "waves" reflecting a specific corporate action, but as a minority shareholder, if you don't do your homework, you seem to be fair game to be perfectly legally disadvantaged. As the latest documentation supplied by an independent expert for a Bolloré transaction [5] illustrates clearly, it is not intended to provide insight and analysis, merely the statutory requirement. As we discuss later, there is an easy way to not be disadvantaged.

Why a lengthy treatise?

So why write such a lengthy piece on the company dredging back through 40+ years of history? Firstly, we are lucky that in the fledgling history of the Dynasty Trust, the "restructure" of Bolloré is occurring as the 71year old patriarch, Vincent Bolloré applies the "finishing" touches to his life's work. Secondly, we already have positions in three of the group companies and - subject to risk management - could foresee investing in others. Thirdly, it's interesting - any finance student should become familiar with the elements of the story. We like to learn too.

But fourthly, in its 201st year, Bolloré is moving towards honing down its size, given the sale and now the pending sale of its two largest operating businesses, to leave a highly liquid but unwieldy corporate structure, ripe for capital management initiatives.

Fifthly, Bolloré is perhaps the ultimate example of the type of company in which we look to invest Dynasty Trust's funds. It is fabulously run by an effective family group, and has historically operated in intriguing industries but is complex and so gives an opportunity to the investor who works harder at unravelling the structure. There are double, triple, and quadruple discounts available, which when interrogated potentially offer major price upside. It's where a small investing team working diligently can potentially do the job.

Finally, and importantly, when companies like this which have traditionally traded at large discounts to NAV start to self-liquidate, it is inevitable that the discounts will close up - perhaps only slowly, but they will.

These initiatives are likely to see the puppeteer, Vincent Bolloré, from his position as "President directeur général" of Compagnie de L'Odet ( FCODF ), Bolloré's largest shareholder using not dissimilar skills to optimise the future corporate structure. Indeed, the recently closed Bolloré buyback offer is straight out of his 1990s playbook. The independent expert in the latest deal [6] thinks it's a great idea for you to sell your Bolloré shares back to the company (family-controlled) at a significant discount to what WE (and many other independent writers) think they are worth.

It's the epitome of what investing in these family-controlled companies is often (not always) about: forget the dialogue - just follow the money . Whether it's the top company, not a controlled subsidiary, or just doing what they do, not what an external party thinks. In the latest Bolloré deal, as we shall see, the smart money has not sold its Bolloré shares; it's actually BUYING ODET shares.

The Bolloré story in the public sphere dates from 1985 with the IPO of Bolloré Technologies. However, the current Bolloré Galaxy STILL contains 14 publicly listed entities that are either consolidated or equity accounted: 10 leftovers from Groupe Rivaud acquired in 1996 including four plantation companies [7] , then the four big ones: Bolloré, Compagnie de L'Odet, Vivendi ( VIVEF ), and UMG ( UMGNF ).

With the 100% owned assets - subject to the sale of logistics - being trimmed down to the battery, film, automated systems, and energy businesses, with the vast media holdings (excluding an 18% stake in UMG) now housed in Vivendi, this 14 company listed structure looks far too unwieldy. Could it be coming to a conclusion as the patriarch potentially looks to reduce the stake of minorities in the publicly listed entities?

To ascertain whether this is the case, how it may be achieved, what are the sensitivities, and what's in it for hanging around, it is worth spending some time tracing through the history of the company. It's complex and utterly fascinating for any student of finance.

So this lengthy treatise is divided into three parts:

- The history of the group from 1985 onwards: it is not meant as a complete document of every deal or company chronology. There are foci on some small, but what we view as significant deals - from a financial or behavioural viewpoint - with no mention of other large businesses. However, we believe that without visiting the past, the reader will have no clue as to why Bolloré looks like it does in 2023 and why some of the tactics it will utilise in the near future have evolved - everything old is new again in the "Bolloré Galaxy";

- How to deal with the treasury control loop whereby Bolloré and Odet effectively control themselves; and

- A focus on the four major remaining companies and an assessment of the valuation and pricing discounts available.

We conclude, working from the bottom up that:

Universal Music Group is an astounding business and is marginally undervalued (by ~25%) against cohorts of high-quality annuities; however, especially if there are changes in the Bolloré structure, it will become more important to Bolloré itself, and both it and Vivendi represent significantly discounted entries.

Vivendi has rightly been heavily discounted to the degree that on a sum-of-the-parts basis, the shares value the core Canal+ and Havas income streams at ~1x EV/EBITDA in 2023, assuming a net nil contribution from the other smaller businesses. But optimising Vivendi may require significant debt commitments. The "puppeteer" appears to exhibit a significant influence from the outside. We have a small position in Vivendi and could see a scenario where Bolloré will eventually bid (don't hold your breath, it will be well into 2024). Forget the recent share sales - there are many Bolloré precedents of selling then repurchasing (Havas, notably). But it has to be recognised that Vivendi shareholders have not been that well treated by Bolloré (or their predecessors) and the company is the most remote from the centre of the Bolloré Galaxy.

Bolloré itself (owned by E72DT) is ridiculously underpriced, partly as a result of the continued misunderstanding of the Treasury control loop, but also the lengthy appraisal process of selling Bolloré Logistics to CMA CGM which liquifies the group to the tune of a further €5bn. If it fails to complete, some of the analysis postulated will look foolish and the patriarch's legacy won't be easily completed. If it is consummated, we value Bolloré at ~€13/share before applying any kind of conglomerate discount. If the patriarch is willing to countenance a heavier GROSS debt load adjacent to his favoured exposure in the Galaxy (Compagnie de L'Odet) an acquisition of Vivendi once the logistics deal completes and the assorted conditions of Vivendi's 57% Lagardère purchase are met.

Compagnie de L'Odet (owned by E72DT) the group holding company, in our opinion, does not currently trade at a major discount to the market price of Bolloré. ODET is a 100-bagger since the 1992 backdoor listing into SEPA, is still the patriarch's favoured exposure, and hasn't been adulterated with other holdings to any extent. Of course, the discount to real value blows out dramatically as the more realistic view of the pricing of Bolloré shares is applied, and also trades at 60% below a sum of the parts valuation. We can calculate a value of ODET at ~€3750/share on a sum of the parts basis and haven't been blind to recent "aggressive" (by ODET standards) accumulation by its immediate parent, Sofibol.

Part I: The History

A. The bits above Bolloré: Cascading share structure

The Bolloré family business - specialising in thin papers, pharmaceuticals, rolling tobacco [8] , and capacitors was established in Brittany in 1822. Vincent Bolloré, the current "retired" patriarch [9] , saw the business sold, in distress, to Baron Edmond de Rothschild - his mentor - for whom he worked. In 1981, Bolloré reacquired the business, still struggling for a symbolic Ffr1 [10] with his brother, Michel Yves. In 1983, having cast around for funds to recapitalise the enterprise, the brothers through their company Financière V persuaded Sebastien Picciotto - now known for his family investment company Orfim - to invest Ffr10 million (€1.52m).

In November 1985, having stabilised the financial situation, developed new product lines, and boosted turnover from Frs200 million (€30m equivalent) at acquisition in 1981 to Frs600 million (€91 million equivalent) in 1985, a newly created company "Bolloré Technologies" containing the business was floated on the second market of Paris Bourse only four years after acquisition in November 1985. The new IPO was valued at FFrs500 million (€76 million).

Various other HNW families invested in the group up until September 1988 when the graphic above [11] depicts the structure of the business around the public company "Bolloré Technologies".

Aside from Picciotto, there are familiar well-connected names on the diagram, notably:

- Edmond de Rothschild, Vincent Bolloré's old employer;

- Lazard - home of the man who created the structure - Antoine Bernheim;

- French banks Credit Lyonnais and BNP plus smaller institutions Sofialpe and Arjil (Lagardère);

- Assurances Générales de France (AGF), the previously state-owned insurer, by then part of Allianz;

- IFINT SA is part of the Agnelli group predating the amalgamation into Exor; and

- Compagnie de Presbourg, part of the Lagardère stable (everything old is new again…).

However, how much better if you also effectively control the votes of the "minority" 50%? Originally, in the case of Bolloré (see graphic), this meant supportive high net worth individuals or institutions ensured the creation of the impregnable "Breton Pulleys" where aside from the "downward" cascade of 50% of 50%, the "minority" 50% is tied up as well by supportive shareholders of the appropriate pedigree.

Hence, in 1987 and 1988, Bolloré incorporated the private entities Sofibol, Financière V, and Omnium Bolloré (not shown on the graphic) with assistance from Picciotto and Bernheim clients.

From 1996 onwards, with the effective full acquisition of Group Rivaud (see below), the Breton Pulleys were completed as Bolloré's own capital - as majority-controlled subsidiaries of the holding company itself, gradually replaced the high net worth capital, some of whom swapped into the capital of Bolloré itself (Albatros Investments, later Bolloré Investissement at the time).

In 1989, as part of the acquisition of businesses in the transport industry - the foundations of the logistics business now being sold - Sofical, the transport acquisition vehicle acquired a majority interest in SEPA, a holding company quoted on the Marseille cash market, which was a holding company of Mattei Automobiles, a car rental outfit.

In 1992, Bolloré used SEPA as a shell company for RTO [12] Financière de L'Odet and provide liquidity to the institutional shareholders. With this being the closest holding company to the main operating companies ever since, and Vincent Bolloré's continued involvement, "L'Odet" has a real mystique about it.

In September 2006, Bolloré Investissement, the former Albatros (which by then was listed) acquired the minorities in Bolloré (formerly Bolloré Technologies) with the merged group now the current day Bolloré, controlled by Compagnie de L'Odet.

B. "Groupe Rivaud": the asset-rich Gaullist spiders-web

"Undoubtedly the Rivaud Group remains the most mysterious and the most padlocked of French finance. The most anonymous, too: in its formidable organisation chart, a real interlacing of companies, its generic name appears only twice" (L'Express "Rivaud: the miscalculations of M. le Comte" 24 October 1996) (translated)

It is difficult to (credibly) explain to a 21st-century investor the background to Rivaud, eventually "acquired" by Bolloré in 1996. Put on your colonial pith-hat and here goes. After a preliminary introduction, we assess Rivaud's importance to Bolloré in four areas:

- Money boxes;

- Funding growth of the global logistics business;

- Providing capital for highly lucrative corporate raids; and

- Aiding the closure of the Treasury control loop

The group was founded by four brothers - Olivier, Max, Maurice, and Rene Rivaud de Raffiniere - in the early part of the twentieth century building and funding rubber and palm oil plantations in the Far East and Africa. The plantations were developed as investors alongside a Belgian agronomist, Adrien Hallet, who it is rumoured met Olivier's father on a train.

Hallet establishes plantations in the Congo (under Belgian colonial rule at the time) in 1890. He moved to Malaysia in 1906 and further into Indochina as a result of the partnership with Rivaud, who acquired the original Socfin [13] in 1919. Hallet died in 1925 and his son Robert took over the running of the group and developed it further with Rivaud establishing other plantations and creating separate companies around Africa and Indochina. Upon Robert's death in 1947, his executor Phillipe Fabri took on the running of the group and was succeeded by his son Hubert Fabri - the same age as Vincent Bolloré - an important point as the Rivaud Group began to unravel in the late 1980s and 1990s. The Fabri's eventually (see below) became the largest shareholders in the "new" Socfin, created in 1973 by the merger of "old" Socfin and Financières des Colonies.

Very recently, at the end of May 2023, Bolloré & Fabri negotiated an agreement whereby the Bolloré holding in Socfin (listed on the Luxembourg Stock Exchange) attributed its voting rights to Fabri, giving him 95% of Socfin's voting rights and facilitating a squeeze-out action, in one minor clean up within the group.

Rivaud Group evolved around a bank - Banque Rivaud et Cie - which under Olivier Rivaud de Raffinière's son-in-law, Jean de Beaumont, developed significant connections with the RPR (Rassemblement pour la Republique - the Gaullist party). De Beaumont was a member of the International Olympic Committee for 20 years, and his son-in-law - Edouard de Ribes - chaired the bank from 1975 onwards.

The group had listed a number of tightly held companies effectively representing individual country plantation holdings, with two over-riding listed holding companies, Socfin (see below) and Plantations des Terres Rouges, and the unlisted Société Bourdelaise Africain (SBA). All up, Rivaud contained some 800 companies and 130 often inter-locked holding companies by the late 1980s.

The initial connection with Bolloré was between Count de Ribes and Michel Bolloré, Vincent's father. In 1989, as part of the financing of the "upper" part of Bolloré, the group's exchanged 30% shareholdings in SBA and Financière V.

Aside from the bank and planation interests, Rivaud was a treasure trove of other assets - properties, assorted shareholdings in French corporations (notably Genérale des Eaux, now (of course) known as Vivendi) replete with capital gains.

In 1990, the investment banks Duménil Leblé and Stern made a takeover offer for Socfin; not being able to succeed, despite accumulating nearly 40% of the capital, they sold the shares to Italian financiers Giancarlo Parretti and Florio Fiorini through their Swiss company, Sasea. The Italian financiers were looking to acquire the French Pathé cinema chain with the assistance of Rivaud which facilitated the acquisition of 37% of Plantations des Terre Rouges (PTR), one of the key "planation" holding companies. The Pathé acquisition was thwarted by the French Government on "cultural" grounds. Both Italians were eventually arrested on fraud charges relating to the takeover of MGM-UA. [14]

In September 1990, the Italians' shareholding in Socfin - controlled by the security holder, Credit Lyonnais - is sold together with the 37% holding in PTR and assorted smaller holdings in Rivaud's plantation companies for US$322 million (Ffr1.7 billion at the time) to Bolloré and Credit Lyonnais through a 60/40structure - Compagnie des Glenans (Glenans). In tandem, Bolloré increases his shareholding in SBA to 40% and this holding is installed into the Glenans structure.

It is a further six years before the ultimate payday comes to fruition. Rivaud is hit by a quadrella of disasters:

- Raids by 100 tax agents on the Rivaud HQ in August 1996, suggesting illegal capital transfers;

- Bankruptcy of the Rivaud-controlled Air Liberté in September 1996;

- Further allegations by the French tax office of tax evasion; and

- An investigation by French Banking Commission into the management of the Banque Rivaud itself.

On 17 September 1996, Vincent Bolloré became president of all the main Rivaud holding companies, despite the Comte de Ribes still owning 60% of SBA. He set about liquifying the bank but simplifying the structure by buying in large-scale minority holdings in the Rivaud structure such as a 32% stake in Compagnie du Cambodge held by Axa.

In March 1997, Bolloré acquired the Comte de Ribes holding in SBA but allowed the Ribes/de Beaumont to exercise the voting rights until de Beaumont's death in 2002. A year later, in March 2003, the structure was finally cleaned with Bolloré acquiring Credit Lyonnais 41% stake in Glenans, held by its 'bad bank" unit CDR.

C: Rivaud's importance to Bolloré I: Money boxes and squeeze outs [15]

The structure in early 1997 [16] is illustrated in the chart above; it still has importance and resonance 26 years on for three reasons:

- 6 of the eleven then-listed structures (including Plantations Nord-Sumatra listed in Belgium) still exist today trading on Euronext Paris, some with significant holdings in the "upper" part of the Bolloré control structure, notably Compagnie du Cambodge and Financière Moncey; only 5 (see below) have been fully acquired via "squeeze-outs";

- These companies were the beneficiaries of the asset sales within the Rivaud Group - ranging through the property, American screw manufacturers, and thousands of hectares of plantations - the cash from which was used in the five key highly profitable "raids" on Bouygues, Pathé, Lazard (Rue Imperiale), Vallourec and Aegis PLC (section D below).

- Parts of the cash in the consolidated Bolloré group is still held in these non-100 % controlled subsidies but placed on "treasury" with Bolloré - notably Cambodge with over €1 billion.

Since 1996, five of the Rivaud companies have been fully acquired by components of the Bolloré group as follows:

| date |

| Acquired |

| Acquiror |

| Price offered |

| Issued Shares |

| Market Capitaln (€mn) |

| Minority stake |

| Minority value (€mn) |

| August 2001 |

| Padang |

| PTR |

| €485 |

| 421,200 |

| 204.3 |

| 11.4% |

| 23.3 |

| August 2001 |

| Kali |

| Cambodge |

| €325 |

| 1,213,577 |

| 394.4 |

| 9.3% |

| 36.7 |

| Oct - Nov 2007 |

| NSI |

| Bolloré |

| €545 |

| 346,500 |

| 188.8 |

| 27.6% |

| 52.1 |

| Oct-Dec 2012 |

| SAFA |

| Cambodge |

| €80 |

| 577,200 |

| 46.2 |

| 12.1% |

| 5.6 |

| April - June 2013 |

| PTR |

| Bolloré |

| €2,000 |

| 1,135,275 |

| 2,270.2 |

| 2.8% |

| 63.6 |

If you wish to join a new "cult", now's your chance. Six of the old Rivaud companies are still listed in France (excluding the three "Socfin" plantation concerns listed on Luxembourg Stock Exchange). Given the interest in Vincent Bolloré, there are always theories that one or other of these companies are going to be privatised via a "squeeze-out", given Bolloré group holdings are over 90%. There are significant valuation discrepancies in some, but they are all hopelessly illiquid. If you want an entry ticket to the Bolloré cultists group, here's your chance. But I'm not doing any detailed homework for you:

| €million [17] |

| CBDG |

| ARTO |

| FMONC |

| FORE†† |

| MLCVG |

| MLTRA |

| price |

| €6500 |

| €4980 |

| €7850 |

| €600 |

| €6350 |

| €5200 |

| shares o/s |

| 559,735 |

| 226,200 |

| 182,871 |

| 141,333 |

| 62,850 |

| 9,150 |

| Equity cap |

| 3,638 |

| 1,126 |

| 1,436 |

| 85 |

| 399 |

| 48 |

| public owns |

| 0.77% |

| 4.2% |

| 3.7% |

| 2.2% |

| 3.7% |

| 6.0% |

| Public cap |

| 28 |

| 47 |

| 53 |

| 2 |

| 15 |

| 3 |

| Net assets† |

| 4,363 |

| 1,847 |

| 1,687 |

| 22 |

| 18 |

| 3.4 |

| NAV/share |

| €7794 |

| €6939 |

| €9225 |

| 153 |

| 287 |

| 376 |

| (% discount) |

| (17%) |

| (28%) |

| (15%) |

| 292% |

| 2112% |

| 1383% |

| † stated as per the 2022 annual report (no revaluation of holdings) †† converted at €1 = CFAfranc 656 |

D: Rivaud's importance to Bolloré II: one strategic holding helped build a €10bn empire

Bolloré's largest businesses for much of its listed existence have been logistics, ports, shipping, and general transport. However, they do not owe their establishment to Group Rivaud, except for one strategic shareholding which enabled Vincent Bolloré's strategic deal-making genius to exert itself - and nearly take the whole group into extremely difficult times in the early 1990s.

The building of Bolloré Logistics Africa - sold in 2022 to MSC Group for €5.1 billion (plus €600m loan repayments) and Bolloré Logistics - being sold under a put option for €5bn to CMA CGM and due to settle in H1 CY2024 (subject to competition authority clearances) is a 38-year story. This story of building >€10 billion worth of business value in logistics and tobacco - throws up clues into Bolloré's future in four areas:

- A willingness to sell and buy (or vice versa) the same asset in quick succession (Coralma);

- Extreme patience in maintaining sub-optimal corporate structures (hello VivendiLagardère!);

- Not overpaying ever again; and

- Sensitivity to legal actions on squeeze-out transactions.

(1) Tobacco

Shortly after Bolloré Technologies IPO in 1985, the company acquired 70% control of Sofical, a company with a significant tobacco business in Africa. It supplemented Bolloré's cigarette paper interests through three brands - the acquired JOB and Zig-Zag together with the long-standing company-owned brand OCB.[18]

Bolloré established a new tobacco holding company, Tabaccor to expand the business; it did so by forming a new JV on a 60/40 basis - Coralma International - with SEITA[19], the French Government-owned domestic tobacco monopoly (Gitanes, Galoises).

Nearly two years later, Bolloré attracted another high net worth global investor with Rothmans International (Dunhill, Players, Rothmans) controlled by the South African Rupert family (see Compagnie Financière Richemont today) acquiring 4% of Albatros Investissment, the controller of Bolloré Technologies.

Bolloré's gradual exit from tobacco started with the sale of the three cigarette paper brands to Republic Technologies in July 1999, including the family brand OCB.

A few months after the merger of SEITA with the Spanish Tabacalera [20] to create Altadis, Bolloré acquired the SEITA 40% stake in Coralma for €63 million in July 2000, valuing 100% of Tobaccor at €126 million. In return, Bolloré sold a 5% stake in the listed SEITA for €127 million. Better still, and creating more mystique about whether Bolloré is really buyers or sellers, Bolloré sold the entire Tobaccor business (in two tranches) to Imperial Tobacco for €387 million, an actual profit of well over €200 million.

By all accounts, Altadis wasn't too fussed. It eliminated the French stock exchange listing, and eight years later, Altadis sold itself to Imperial Tobacco for €16.2 billion.

(2) Logistics

Whilst logistics has produced enormous value add to Bolloré across Europe and the African continent, its most cyclical area - shipping - also brought difficulties which at one stage in the early 1990s put the group under a degree of strain. The African ports business also produced difficulties in respect of allegations levelled against the patriarch himself, since settled.

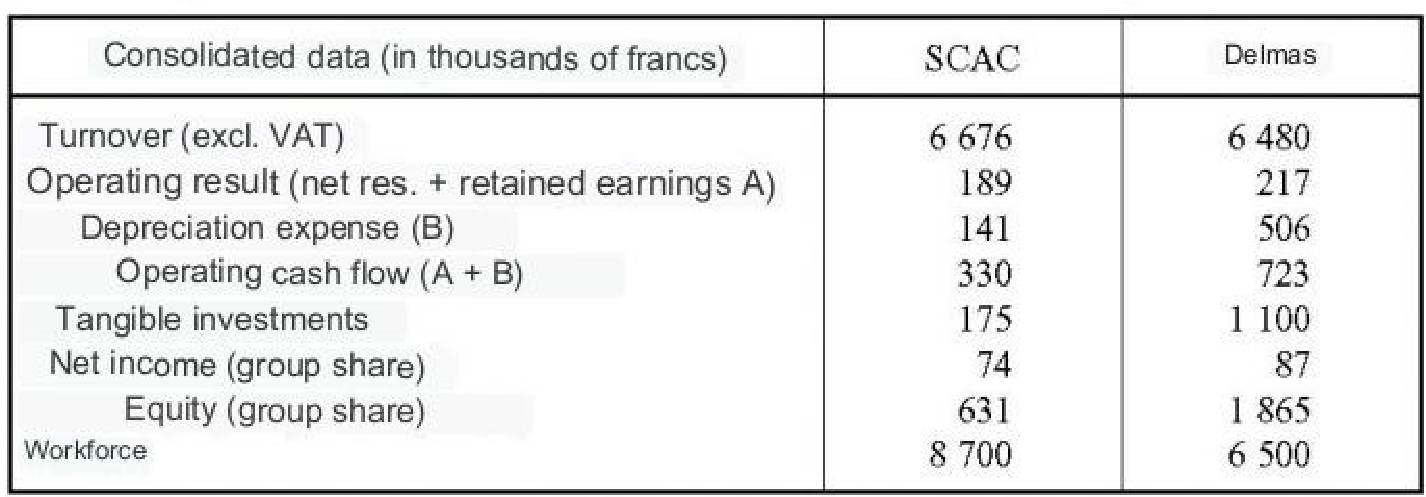

The transport interests were initiated in June 1986 via Sofical acquiring a 37% interest in SCAC [21] from Suez Group for Ffr159m (€24.2m) plus 14% a year later for Ffrs60m, together valuing SCAC at Ffrs430 (€66m) giving Bolloré a start in shipping and handling. The expansion by acquisition continued in mid-1988 with the purchase of a stake in Rhin-Rhône, a petroleum transporter from a shareholder group with an offer to move to 51%. The 39.5% shareholder, Elf Aquitaine, launched a counter offer which with successive bids and counter bids forced Bolloré to spend Ffrs615 million (€94m) for 76% of Rhin Rhône valuing the business at €123 million.

The early 1990s saw this transport acquisition strategy cause significant headaches for Bolloré through overextension, competitive pressures, and regulatory difficulties. In April 1989, a significant hidden asset in the Rivaud Group came to the fore. Bolloré's then immediate parent, Albatros Investissement acquires 30% of Société Bordelaise Africaine (see prior section); within SBA is a 4.6% stake in Société Navale et Commerce Delmas Vieljeux (SNCDV). But with Sofical also holding 2.1% and allegiances from other supporters, Bolloré is able to count on 18% support of SNCDV - a Ffrs4.3 billion (€650 million) company. In early 1991, with shareholder stalemates and the business not performing, Tristan Vieljeux sells his stake partly (10%) to Bolloré - giving them 31% - and 7% to others to give "them" control - at a significant premium to prevailing stock prices.

La Journal de la Marine marchande 5 July 1991

{kind=link}

Bolloré wants to set about merging SCAC and Delmas-Vieljeux (see above data for 1990 and divide by 6.55 for Euros) who have been aggressively competing in freight forwarding, shipping, and Africa, plus replicating infrastructure investment. However, a spoke is placed in the wheel with the (then) regulator CBV (Council of Stock Exchanges; Conseil des Bourses des Valeurs) alleging Bolloré is part of a concert party designed to circumvent the takeover rules by staying below one-third of the capital.

After appeals, CBV wins out and requires Bolloré to bid for the remainder of the two relevant companies, CFDV and Navale Delmas, at excessive prices. Moreover, the Delmas group also has Ffrs3 billion of debt embedded within the structure.

Bolloré acts quickly to merge SCAC into Delmas to create a group (SDV) with a 1991 turnover of over Ffrs14.5 billion (€2.2 billion) but only a 3% margin and weighed down at the parent (Bolloré Technologies) with over Ffrs7.5 billion (€1.15 billion) of debt in a cyclical industry. The result for Bolloré (Technologies) itself is a nightmare - losses of over Ffrs1 billion between 1992 and 1993.

With cost reductions and global economic improvement, the business begins to improve and Bolloré's debt is reduced by the Rivaud acquisition and asset sales. The next step in the logistic path is to work with the South African ship owner Safren and Belgian Compagnie Maritime Belge (CMB) to resuscitate SAGA, a major French loss-making cargo handler, via a joint venture company, BCR. By the end of 1997, Bolloré buys out the two co-venturers and bid for the minorities in the publicly traded SAGA. This gives Bolloré ownership of the two largest cargo-handling businesses in France and Africa.

From that point onwards, the growth in the logistics businesses in Europe and France is organically based. In Africa, Bolloré aggressively pursued port concessions in competition with Moller Maersk, growing to 15 port terminals, mainly but not exclusively in Francophone Africa. The entire group was branded Bolloré Logistics in 2016.

In April 2022, Bolloré announced the sale of its Bolloré Africa Logistics business, which was turning over €2.3 billion and handling (amongst other items) ~5 million TEU [22] containers each year to MSC Group [23] for €5.1 billion in equity and repayment of €600m in loans.

In May 2023, CMA CGM - a privately owned French company, mainly by the Saadé family based in Marseilles - agreed to acquire the remaining mainly European-based logistics business from Bolloré for €5 billion subject to competition clearances. This a mere drop in the ocean for the company which turns over US$74 billion a year and in 2022 made US$33bn EBITDA and nearly US$25 billion net profit.

E: Rivaud's importance to Bolloré III: Funding five key corporate raids: 1998 - 2012

The Rivaud companies were key to financing Bolloré's raid on major French corporates commencing in 1998 via the establishment in early that year of "Financière du Loch" ( Loch ), an unlisted company owned 32.5% by Bolloré directly, 55.5% by Compagnie du Cambodge ( Cambodge ) and 11.9% by Société Industrielle et Financière de l'Artois ( Artois ). Hence, the spoils of these raids were shared with the small minorities who held Cambodge and Artois.

Loch was 100% absorbed into the parent Bolloré in October 2012 after an agreement to divest the shares in the fifth of these major [24] raids - Aegis PLC.

The five major corporate raids, described in more detail, which netted estimated profits of over €2.5 billion (~158% return) are illustrated in the following table [25] :

| Company |

| Dates |

| stake |

| Entry cost (€mn) |

| Divestment (€mn) |

| Profit (€mn) |

| Bouygues |

| 1998 |

| 10% |

| 348 |

| 575 |

| 227 |

| Pathe |

| 1998/9 |

| 19.6% |

| 321 |

| 443 |

| 122 |

| Rue Imperiale/Lazard |

| 1999/2000 |

| 31% |

| 305 |

| 595 |

| 290 |

| Vallourec |

| 2002-2009 |

| 25% |

| 207 |

| 1,678 |

| 1,471 |

| Aegis |

| 2005-12 |

| 26.4% |

| 450 |

| 915 |

| 465 |

| TOTAL |

| 1,631 |

| 4,206 |

| 2,575 |

Bouygues

In December 1997, Bolloré (through Loch) quietly built up a 10% stake in the family-controlled construction-based conglomerate Bouygues, run by the Bouygues brothers Martin and Olivier. The company's attraction was its TV interests - notable TF1 - and an aim of having the fledgling mobile telecoms business sold off.

Strangely, the brothers and Bolloré entered a pact to effectively pool their holdings in a "concert party" type arrangement. Over the course of 1998, tensions continued to build between the groups, and the brothers were keen to have the pact concluded. Bolloré demurred until November 1998 when he agreed to its dissolution and promptly sold (by then) a 12.6% stake in the company to Francois Pinault's[26] private Artemis investment company. Most estimates calculate that Bolloré paid Ffr700/share (€106.90)for the 3.259m Bouygues shares, selling them at Ffr1160 (€176.84) for a profit of around €228 million over the course of a year.

Pathe

In December 1998, Bolloré (via Loch) acquired 10.5% of Pathe, which at that stage had production and distribution interests in France and Germany plus two other key assets: 12.7% of the fledgling BSkyB in the UK and 20% of canal satellite, the leading French Pay-tv operator. The idea was to force a sale of the minority assets, in the structure controlled by the Seydoux family. Bolloré moved rapidly to 19.6% of Pathe by the end of 1998 at a cost of ~€321m [27] .

They didn't stay long! By the end of January 1999, Canal+ and Vivendi had bought out the then 19.6% stake for €443 million leaving the group with a €122 million or 38% profit in a month.

Rue Imperiale de Lyon/Lazard

On 17 June 1999, via Loch, after the successful realisation of raids on Bouygues and Pathe, Bolloré acquired 11.5% of Rue Imperiale de Lyon, one of the intermediate holding companies controlling the investment bank, Lazard. Half of the stake came from funds manager Ivory & Sime. Rue Imperiale was controlled by the scions of Lazard, notably Michel David-Weill. By the end of June 1999, the stake had been raised to 20.7% but with an acknowledgement by Bolloré NOT to seek control of Rue Imperiale - in other words, cap its holding at 33%.

Over the course of 2000, Bolloré took the Rue Imperiale stake up to 31%- see chart [28] to the left (substitute Bolloré for Credit Agricole). Bolloré's clear strategy - following other modus operandi amongst complex French family-controlled companies - see chart [29] above (substitute Bolloré for Credit Agricole).-to attempt to force the controlling families to collapse the complex structure holding Lazard.

In that respect, Bolloré had a company in the shape of UBS Warburg whose proprietary trading desk in the Bahamas was placing pressure further down the chain in the next set of holding companies (see chart). The two actions effectively coalesced. On 13 November 2000, Eurafrance made a takeover offer for Azeo, to form Eurazeo which still operates today as a private equity owner under Lazard's control.

On 24 November 2000, Bolloré (Loch) sold its 31% stake in Rue Imperiale - acquired for €305 million - to Credit Agricole for €595 million, with Vincent Bolloré and Michel David-Weill having met on the morning of the Eurafrance-Azeo offers to negotiate the transaction. The profit to Bolloré over the course of a year: €290 million.

Vallourec

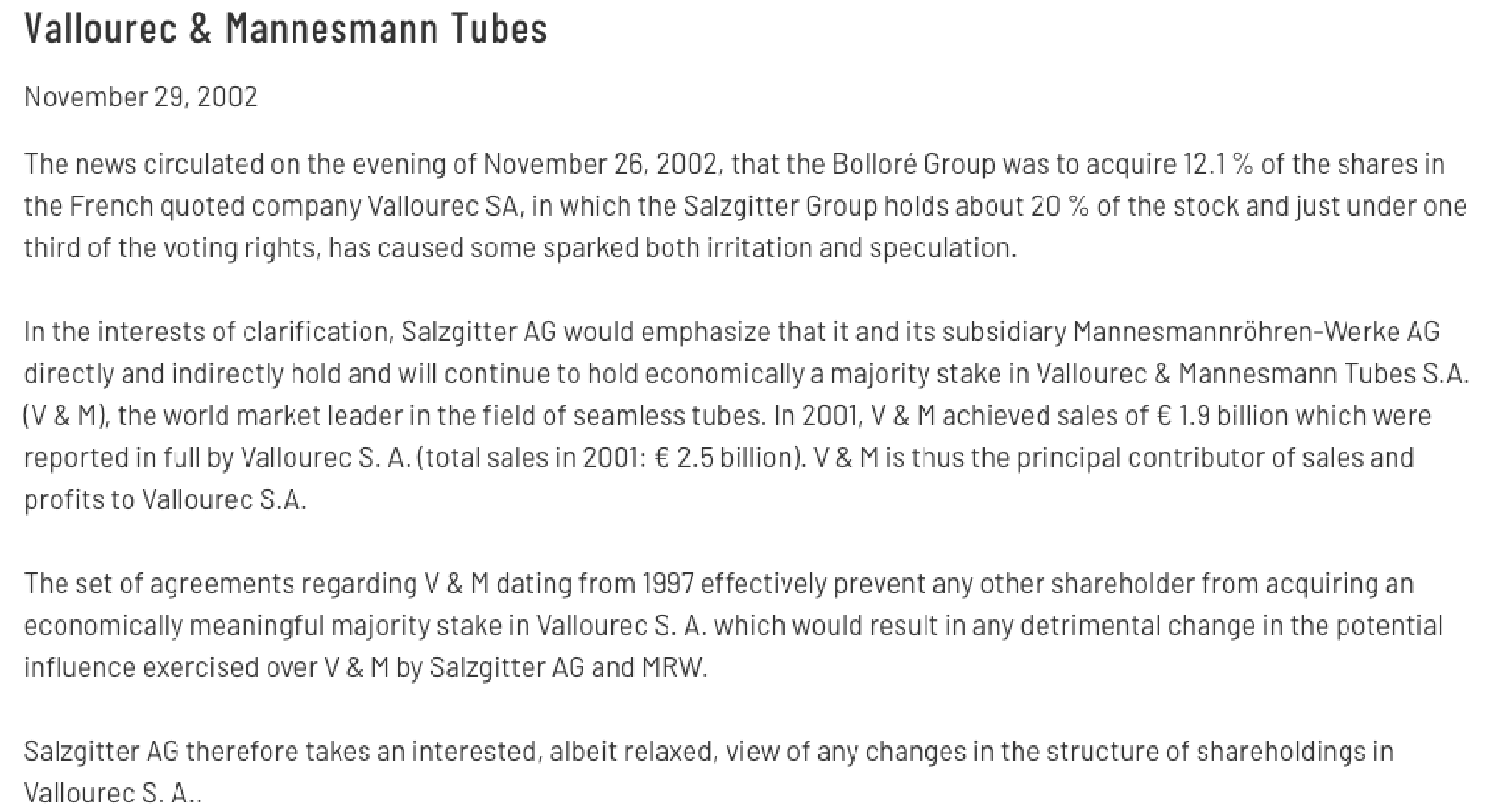

Whilst the transactions on Lazard are the most intriguing given the investment banking background, Bolloré's investment in the less alluring world of steel tubes was far more profitable. On 26 November 2002, Bolloré (mainly via Loch) acquired 12% of the steel tube group, Vallourec, at around half net asset backing, sparking one of the most honest press releases you will ever see from the largest Vallourec holder, Salzgitter AG - a sharp contrast to today's "spin":

{kind=link}

Moving through 14% at the end of January 2003 and up to 18% by June 2003, Bolloré continued to buy Vallourec through 2003 and became the largest shareholder with a peak stake of 25% by June 2004. Vallourec then moved to enact the desired Bolloré strategy, to buy out its German partner from V&M Tubes to close the gap between share price and real value, as well as develop its drill pipe strategy.

Salzgitter's "relaxed" nature regarding Vallourec was truly warranted: aside from realising €545 million in June 2005 on the sale of their JV interest, they also recorded profits of over €900 million on the sale of their shares in August 2006.

We estimate Bolloré's average entry price to Vallourec, adjusting for the 5-1 stock split in 2005, to be ~€14.30/share within the Loch/NSI structures; Vallourec shares peaked at €232 in mid-2006. The transparent outcome can be seen in the Cambodge accounts for each relevant period between 20052009 (ignoring the later 2011 exercise).

Over five calendar years, Loch/NSI realised €1,678 in proceeds from the sale of Vallourec, of which €1,471 million was capital gains - over a 700% return on the investment. The Vallourec play remains Bollorés most successful straight equity market transaction.

Aegis

In August 2005, Bolloré (through Loch) acquired a 6% stake in the UK-based ad agency Aegis Group PLC spending £68m to purchase ~63mn shares at £1.09. The stake was rapidly more than doubled to 13.3% by October 2005. Bolloré continued to build its stake which peaked at just under 30% in 2007.

Aegis opposed Bolloré's desire to have two board seats given that at the time Vincent Bolloré was Chair of Havas -a direct competitor to Aegis; equity investors clearly believed Bolloré would try to merge the two companies, although, despite some discussions, this never came to fruition. The antagonistic nature of the relationship cost Aegis its Managing Director at the time, Robert Lerwill, who departed in November 2008, with the share price of Aegis less than half (£0.50) of Bolloré's initial acquisition price over three years prior.

Aegis shares recovered strongly in line with growing profitability and a re-rating in the sector and were trading around £1.62 in July 2012, with the Bolloré stake still over 26%. The Japanese advertising giant Dentsu then arrived on the scene with an agreed bid at a 48% premium to the prior day's price, with an immediate acquisition of 15% of Bolloré's stake. All up, Bolloré sold ~310m shares into the Dentsu takeover in three tranches at £2.40, to realise €915m in proceeds and a profit of €465mn - having at one stage being down over 50% on its investment.

As noted above, Loch was absorbed into Bolloré via a share issue to Compagnie du Cambodge after the Aegis exercise, enabling the cash to be recycled up to the parent company.

PART II: The Treasury Control Loop

F: Rivaud's importance to Bolloré IV: The Treasury control loop

In Section A (page 5) we highlighted the 1988 ownership chart of "Bolloré" with the various banks and HNW families supporting the fledgling company at various different cascades of ownership. Perhaps Rivaud's greatest benefit to Bolloré has been to supplant these "third parties" with money from the Bolloré Galaxy to own shares in each of the companies forming the cascade above Compagnie de L'Odet, Bolloré's real controller with 69% of the shares after the recent buyback.

The Treasury control loop - Breton Pullies - continues to confuse analysts to this day who struggle to deal with it. It's actually a fairly standard cross-shareholding structure that has been used at various times - notably the 1960s-1980s - for two purposes:

- Gear up returns by borrowing against the "full equity" including the cross-shareholding [30] ; and

- Provide protection against unwanted takeover [31]

The first real analysis of the Bolloré control loop was made by "Muddy Waters" the hedge fund research outfit run by Carson Block, in February 2015. In the 26-page report [32] , Muddy Waters goes the whole hog and admirably does stock eliminations right down to the smaller Rivaud group companies. That may be overkill, but the principles used are applicable.

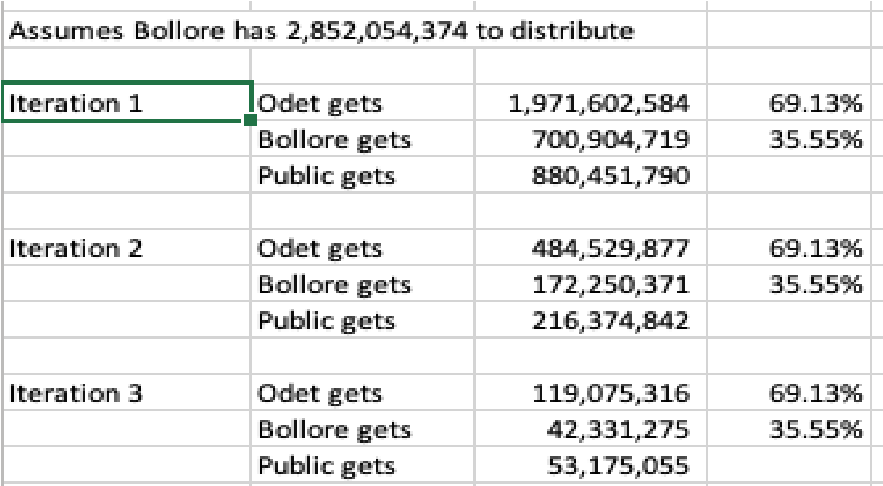

Our more basic analysis of the control loop suggests that instead of Bolloré having 2,852 million issued shares, with investments in itself to maintain control, we can reduce that number of shares down by ~58% to around 1,184 million. How?

Method 1 (see table of first three iterations) is to take Bolloré's 2,852 million shares (post recent buyback) of which 69.13% are directly held by Odet, of which Bolloré's subsidiaries own 35.6% and "distribute" them via iterations; so in the first iteration, Odet are entitled to 69.13% of 2,852 million, but 700.9 million of those (35.55%) really belong to Bolloré.

{kind=link}

Then we move to a second iteration that Odet is entitled to 69.13% of the 700.9 million shares from the first iteration that "belong" to Bolloré. This gives Odet 484.5 million shares but 35.55% of those (172.3 million) really belong to Bolloré. In each case, the public is entitled to the residual number of shares. We continue the iteration twelve times until the numbers become miniscule and arrive at the conclusion that the public owns 1,167 million shares or 40.9% of Bolloré after eliminating Bolloré's subsidiaries' investment in Odet.

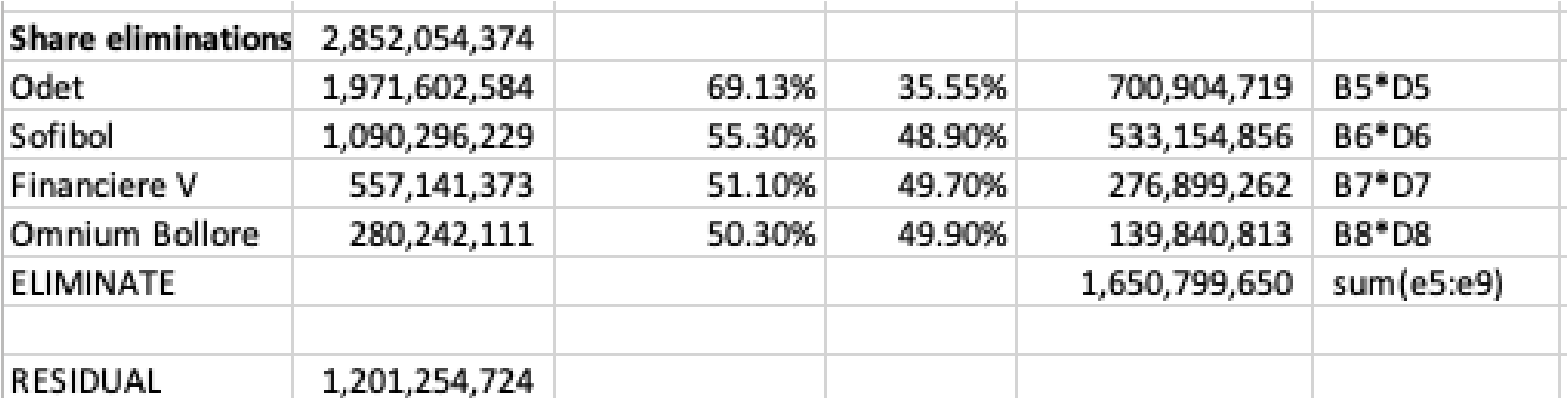

Method 2 is simpler and applies the same logic to eliminating the control loop looking upwards at Sofibol, Financière V, and Omnium Bolloré and eliminates each company's theoretical entitlement to Bolloré based on Bolloré's ownership of it.

{kind=link}

Method 2 yields the public retaining 1,201 million Bolloré shares. We average the two in our calculations to come up with 1,184 million shares on issue excluding the assets of the Treasury control loop.

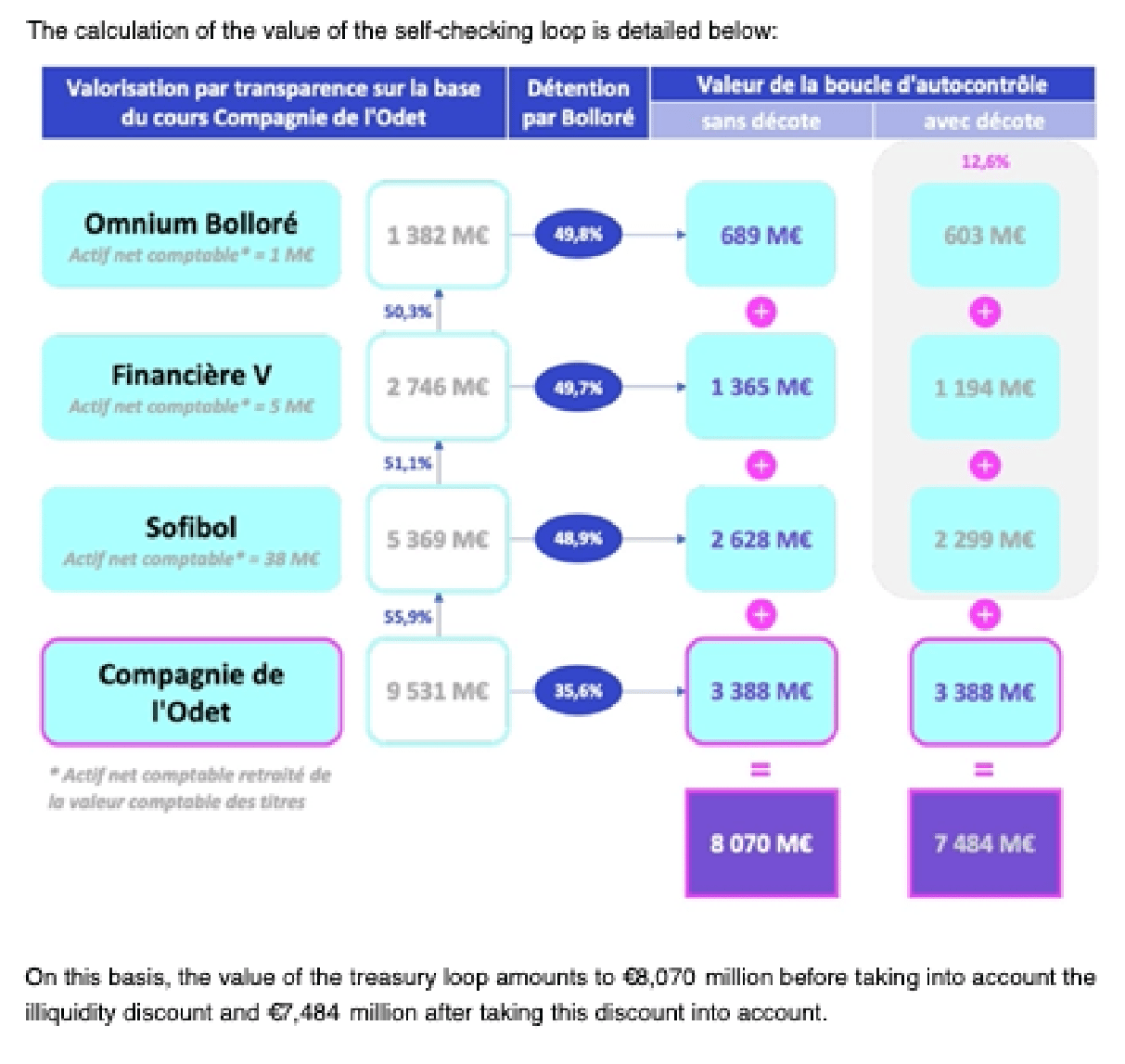

Neither of these methods is strictly correct because they fail to account for the minority holdings in the Rivaud companies such as Compagnie du Cambodge or Financière Moncey which own Bollore's ODET shares. However, in our view they are far more preferable to the method used by A2EF, the independent expert for the buyback of Bolloré shares [33] who used the share price of Compagnie de L'Odet based on a 20day VWAP, to value the companies upwards of it, and then apply a 12.2% discount. Since we regard Compagnie de L'Odet as fundamentally undervalued, using its share price would drag down the value of the treasury loop dramatically.

A2EF's valuation of the Treasury loop is shown below.

If we look at the A2EF valuation, of €8070m (without discount), when applied to the number of Bolloré shares in the Treasury loop - say a midpoint of 1,664 million prior to the buyback - it equates to €4.85 per Bolloré share. Way, way below any reasoned value for the company.

{kind=link}

PART III: The Four Key Companies In Bolloré Today

G: Universal Music Group

Vivendi acquired UMG in June 2000 (completed January 2001) from Seagram, the Canadian conglomerate controlled by the Bronfmann family for an EV of US$41.4 billion in scrip ($34.4bn and assumed debt $7bn); Seagram had acquired 80% in 1995 as part of the acquisition of MCA from Matsushita Electric and added Polygram for $10.6 billion in 1998. Vivendi's timing was atrocious being the peak of the US music industry before physical delivery of music in vinyl, cassettes, and CDs started to decline.

The US industry didn't bottom out until 2014 with revenue of US$7bn - down 50% from the 1999 peak. Recorded music catalogues (and to a lesser degree music publishing) began to gain traction as high-quality assets as a result of the growth of streaming services (Spotify ( SPOT ), Apple ( AAPL ), etc.) from 2007 onwards; moreover, the industry moved to an effective oligopoly with UMG, Warner Music, and Sony.

Vivendi acquired the residual 20% of UMG from Matsushita in 2006 for $1.15 billion, then BMG in June 2007, and EMI for US$1.9 billion completed in 2012 after assorted anti-competitive divestments.

UMG owns over 3 million recordings and 16 "record labels" including EMI, Virgin, Island, Motown, Polydor, Decca, and EMI, together with over 4 million publishing titles. Whilst there are over 60 million recordings available worldwide, the "market" is very much a pyramid. UMG Q1 FY23 results presentation noted that of 9 million content uploads, 8.3 million have less than 1,000 monthly listeners and only 2% are professional artists. Hence, the key is engagement and marketing. In that respect big is better.

They don't come much bigger than Taylor Swift, Drake, The Weekend, and BTS. 4 of the top 5 artists on Spotify in 2022 [34] ; a full list of UMG's roster including Ariana Grande, Coldplay, Justin Bieber, Lady Gaga, The Wiggles and U2 is available on Wikipedia [35] .

The economics of the industry are very strong for the biggest players but still contain elements of risk with a fixed cost structure in operation. Despite the complex accounting (see later), the core top-line economics are remarkably simple and consistent. From over €11 billion of total revenue, of which 80% comes from recorded music products - UMG generates a gross margin of 44-47% of revenue but has a fixed cost base of ~€2.85bn (FY23E) to service. Revenue for the product is dominated by streaming where on average over 50% of streaming service revenue from the Spotifys of the world goes back to UMG for their catalogue. UMG also generates revenue from royalties paid by radio, public performance, film, and TV usage. Its cost base is the royalty paid back to the artist under the relevant agreement, together with marketing and administration.

The standard starting point - as it always has been - is to look for talent and back them with an upfront payment in exchange for ownership of the first "few" albums. Clearly if the artist bombs, then the upfront will not be covered by sales and there will be an effective cash loss.

In exchange for the up-front payment, UMG retains ownership of the recorded music product, but not necessarily publishing rights, potentially retained by the writers. For example, in February 2022, UMG acquired Sting's publishing rights (for a rumoured $300 million) but already held the former school teacher's entire recorded music catalogue.

The new world of social media, data, and online streaming has radically altered the odds in favour of the very largest recorded industry giants. The UMGs of the world get a chance to see artists on social media before they are signed, and have everything loaded their way in terms of being able to financially promote the artist. In turn, for a budding star, why come to a smaller label when the marketing clout of UMG is behind you?

Management have a massive emphasis on keeping the artist happy; in any event, today stars receive proportionally more of the revenue than their 80's predecessors since manufacturing costs are far, far lower. However, one thing the 80's stars have in their favour is the longevity of their music. Some 60% of revenue for UMG comes from catalogue more than three years old. That's one facet of why UMG is such a great business. The other is the sheer market share - around 32% of the planet's recorded music (and 21% of publishing rights) - being the biggest of the three oligopoly players - UMG, Warner Music ( WMG ), and Sony ( SONY ). That's in a market that covers every age group; don't forget today's 80year olds were in their early 20s when the Beatles broke through. Today's 70-year-olds are Led Zeppelin fanatics. (The Beatles are a UMG property; Led Zep are a Warner Music asset).

So what are the issues? UMG and its competitors are increasingly buying up expensive publishing rights of the 1970s-1980s stars and even the actual recorded music catalogues where they have been retained or bought back in earlier years. Some are complex covering only certain countries.

Sony acquired Bruce Springsteen's publishing and recorded music catalogue in late 2021 for US$500 million, and private equity is increasingly looking to invest in these non-correlating assets, pushing up prices. This increasingly pressures UMG to find new talent.

Additionally, the threat of AI has been a dampening effect on investors; AI has the capacity to rapidly "process" UMG's catalogue, and effectively remix selected tracks creating a new piece of product. UMG, led by its industry veteran MD Sir Lucien Grange, is ruthless regarding the pursuit of copyright at this early stage against these "faux" imposters. Investors perhaps don't share his optimism to be able to successfully do so.

The biggest investor issues in respect of UMG, in our opinion, revolve around the appropriate valuation of the shares.

Bolloré and Vivendi recognised that the implied valuation of UMG was not being reflected in the Vivendi shares price from 2019 onwards when Tencent acquired a 10% stake for a valuation of €30 billion; the Chinese company followed up with an agreed further 10% investment at the same valuation in December 2020, with an undertaking to list UMG by end 2022.

In July 2021, after negotiations involving using a Pershing Square Holdings SPAC as a listing vehicle, Bill Ackman's Pershing Square Holdings ( OTCPK:PSHZF - Dynasty Trust is long) acquired a 10% stake at an enterprise value of €35 billion [36] ; based on the net debt of just over €2bn at the time, this implied an equity value of just under €33 billion or €18.18 per share.

In September 2021, UMG was split off from Vivendi with a distribution in-specie of 60% of Vivendi's 70% stake in the business on the basis of 1 UMG share for every Vivendi share; as the largest Vivendi shareholder, this gave Bolloré a direct stake of 18% in UMG. As a guide to the undervaluation of Vivendi at the time, in August 2021, VIV.PA shares were trading around €27; the first-day trade of UMG gave that share a price of just over €25 (38% above Ackman's subscription) with the Vivendi stub in the mid-€10s.

The UMG spin-off has been a disappointment from an equity market perspective with the shares currently just above €20, despite ongoing strong revenue and profit growth. Based on our estimates, revenue will have compounded at 13.6% pa from 2018 (€6bn) to 2023E (€11.4bn) and "adjusted EBITDA" by just under 20%pa from €979m in 2018 to an estimated €2.4bn in the current year.

The company's emphasis on "adjusted EBITDA", as with others, is irritating. Aside from excluding share-based payments, it doesn't really capture the reinvestment in the catalogue, successful or otherwise. We have a bigger focus on our own adjusted cash flow: gross cash flow less investment in catalogue less investment in other intangibles less rent and capex. Whilst not capturing share-based payments it really gives an indication of what the business is spitting out before tax and financing structure. On a period-to-period basis, it can be very volatile. If the rumoured acquisition of the Queen catalogue for $1 billion is to be believed, it would reduce annual adjusted cash flow to less than €500 million.

We believe based on published figures that over time adjusted cash flow should equate to around 14% of revenue across the group. Using a four-stage net present value model (12%pa down to long-term growth of 7%) a discount rate of 10% and the tax rate of 23%, we derive an enterprise value of €50.7bn for UMG.

Deducting the group's €1.8 billion of debt suggests on those NPV metrics each of the 1,814 million shares to be worth around €27, or the equivalent of ~21x EV/adjusted EBITDA. That type of multiple can be seen elsewhere in the very highest quality annuity businesses (infrastructure, luxury) and the shares traded very close to that price after the IPO.

At the current €20.35 per share, we regard UMG shares as being a little under-priced given their attraction in the prevailing environment - it's rare to stop your cheapest form of entertainment in a tough economic environment.

H: Vivendi

Vivendi has morphed from an "old world" water company - Generale des Eaux - formed to sell water to Lyon, then Paris…to an "old world" media company not dissimilar to others around the globe. In common with the others - Discovery, News Corp, and the like - it lends itself to a sum-of-the-parts analysis given its investment holdings and fully consolidated income streams. Like those, it appears cheap on any break-up analysis and is held separately in E72 Dynasty Trust.

It can, controversially, however, be looked upon as a Bolloré dustbin, prone to advantageous dealing in favour of the parent. This thesis is likely to be examined in some detail over the course of the next twelve months as the partial acquisition of Lagardère is fully consummated and opportunities within subscription TV in the chosen areas of Africa and Asia present themselves. Vivendi's net debt could be ratcheted up, potentially impacting its equity value - a brilliant scenario for Bolloré! We examine this thesis at the end of the Vivendi section.

From initial diversifications in 1976 into transport, Vivendi became the founding shareholder of a number of successful French companies, notably Veolia (waste management) and Vinci (autoroutes). In 1983, it helped to form Canal+, France's first pay-tv company (which it still owns) In 1997, the company changed its name from GdE to Vivendi and expanded into the burgeoning telecoms and paytv area outside France.

As with many media concerns of notable size, Vivendi has over the past twenty years engaged in a myriad of asset acquisitions, sales, and asset swaps with others in the area in an attempt to gain strategic superiority. This mainly involved acquisition, then sales of mobile telephone assets in France and Brazil. It also owns 19% of Telecom Italia in what has been a long-running and highly unprofitable saga. In 2007, Vivendi merged its game publishing business with Activision, to form Activision Blizzard, now subject to a long-running takeover offer from Microsoft. Not that Vivendi will benefit, having sold a 51% stake in 2013 at US$13.60 a share and then most of the residue at $20.50 in 2014 [37] . Vivendi has effectively replaced Activision with GameLoft fully acquired in 2016.

Bolloré's entrée to Vivendi began in 2012 with the acquisition of 2.7% of the capital, supplemented by €279m of shares issued by Vivendi to Bolloré for the acquisition of Direct 8 and DirectStar by Vivendi's Canal+ unit. Bolloré rapidly built this 4.4% holding to over 5%. Vincent Bolloré became President of the Supervisory Board in June 2014, adding further to the holding in March 2015 moving to over 8%, and then 12% a month later.

Vivendi effectively came under full control of Bolloré from October 2016 when the latter announced a complex stock-loan deal which when consummated would give it over 20% of the capital of the media group but would trigger the double voting rights entrenched in French corporate law. From that time, there has been a succession of deals and swaps which have cemented the Vivendi of today. The three most important have been:

- Spin off of Universal Music Group - dealt with separately above;

- Acquisition of Havas; and

- Acquisition of 57% of Lagardère, the publishing and retail business.

Havas: buy, sell, buy, then stuff

If there is one corporate manoeuvre that encompasses virtually every trick in the Bolloré toy box, it is the acquisition of Havas over a period of thirteen years: aggressive initial purchases, extreme patience, buybacks, sale, repurchase, and eventual resale to Vivendi.

Bolloré's purchases of Havas began in July 2004 when the conglomerate acquired 4.5% of what was then the World's #6 advertising agency at a price of €3.90/share; with Bolloré in the middle of the Aegis "campaign", there was frenetic speculation as to tie-ups between the two orchestrated by Vincent Bolloré. Bolloré continued an aggressive pattern of share purchases and by October 2004 had passed through 20% culminating in a holding of 22.4% by December 2004, at which time the shares were placed into a special purpose vehicle Bolloré Medias Investissement with support from Société Generale.

Bolloré ensured board control by removal of the CEO in 2005 and the company retained the Havas stake and built slowly up to 32.8% until March 2012. The share price ostensibly did nothing in this period, with Havas shares only 4% above the level of Bolloré's initial purchases at that time. On 26 March 2012, Havas announced a buy back to acquire 12% of its own shares at a price of €4.90 against €4.05 prior to the announcement. With Bolloré declining to participate, their stake increase to 37% at the conclusion of the exercise.

In October 2014, Bolloré opted to bid for the residue of Havas using Bolloré scrip on a 9-5 basis, valuing Havas 413.4 million shares at €6.82 per share; based on this price and net debt of €380 million (excluding tax credits), Havas was priced at an EV/EBITDA (average 2014/15) of 9.9x - around a 2point premium to the tightly priced cohort of Publicis, WPP, Omnicom and IPG at the time [38] .

Bolloré concluded the offer in early 2015 with an 82.5% stake in Havas. So is the next step? SELL 22.5% (93.9m shares) of Havas on 26 March 2015 at €6.40 per share to reduce its stake to 60%.

Just over two years on, in early June 2017, Vivendi acquired the 59.2% stake in Havas from Bolloré at €9.25/share and made a public offer at the same price to move to 100%, concluded in late 2017. Vivendi's cost of acquisition was an equity value of €3,925 million partly offset with ~€571 million of net cash acquired within Vivendi for an enterprise value of €3,354 million.

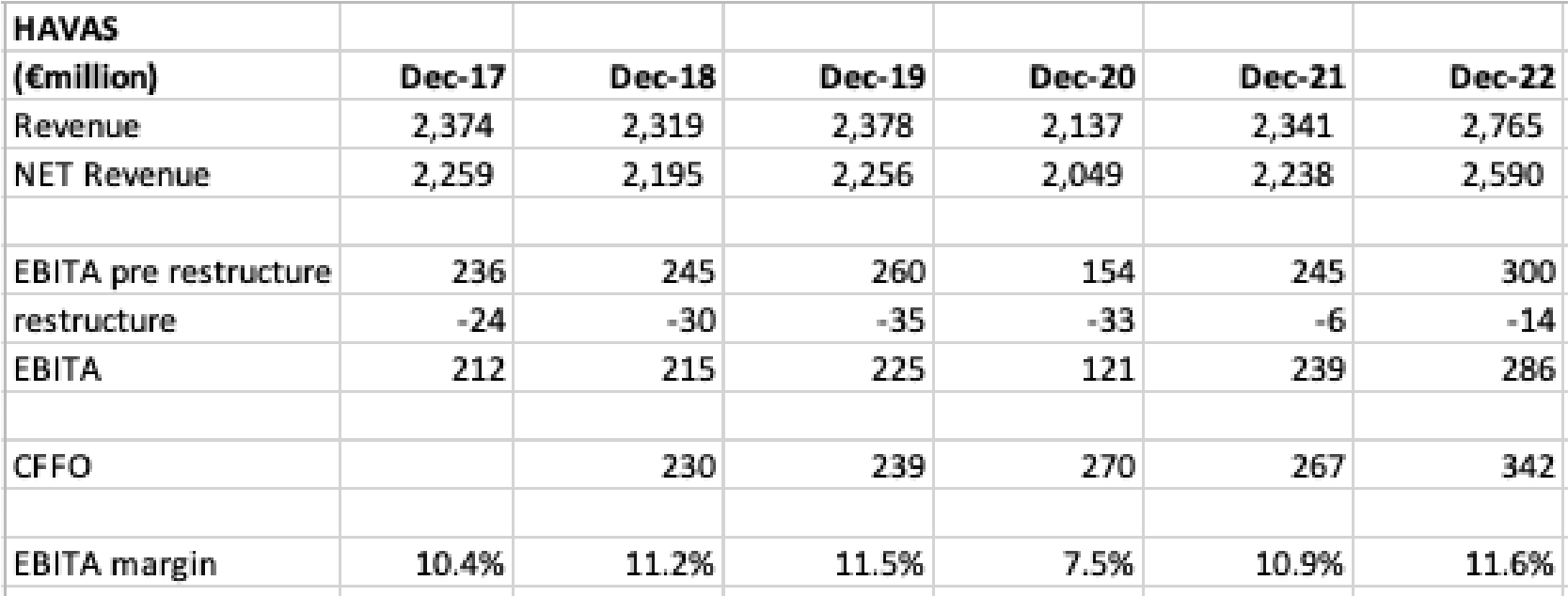

Given the interruption of COVID, it is only in the past year (2022) that Havas has in any way lived up to the price. Five years on, revenue has grown at a pedestrian <3% CAGR, and EBITA (before restructuring costs - which have totalled €142 million over six years - will be just over €300 million on most projections in FY23 - effectively Vivendi paid a 14.5x equivalent P/E for earnings six years out.

That's actually ABOVE current year P/Es for the cohort group - Interpublic ( IPG ), Omnicom ( OMC ) and Publicis ( OTCQX:PUBGY ) which trade at an unweighted average P/E of 12.4x CY23 and 11.7x CY24 earnings. On this basis, Havas would be worth around €2.9 billion on an equity basis, some 30% below what was paid in 2017.

{kind=link}

Canal +

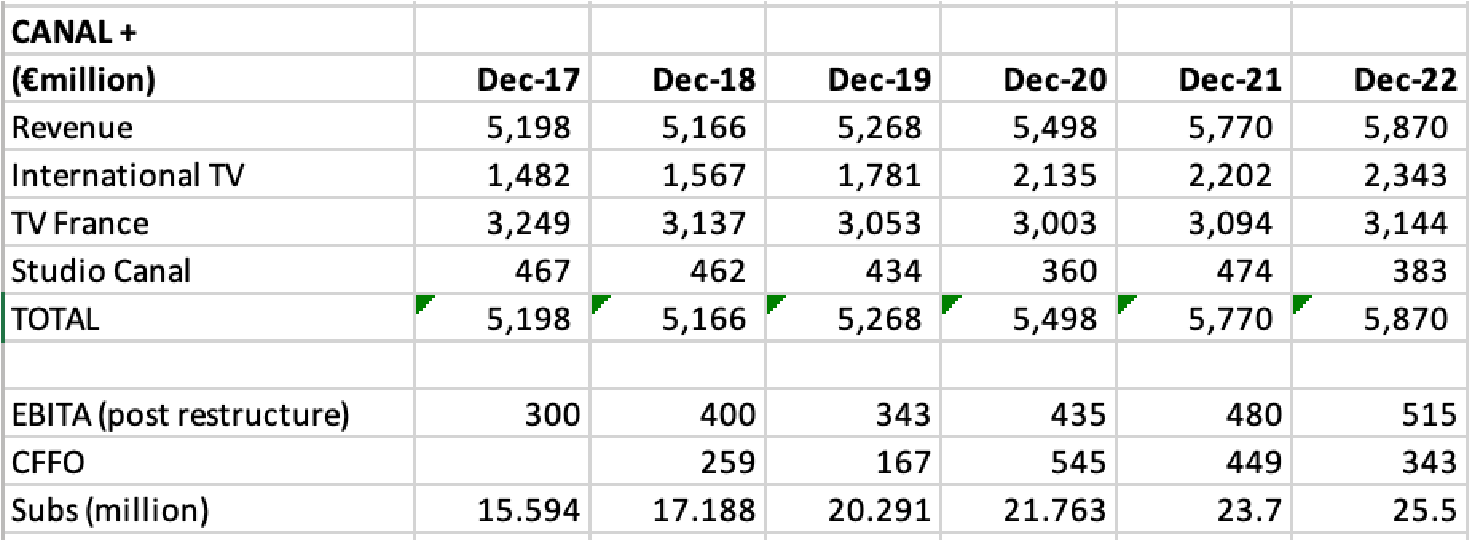

In contrast to Havas, Canal+ has been a more respectable grower via the expansion of its international footprint. International revenues have increased by 9.6% pa over the past five years, in contrast to the French "mainland" TV where revenue fell to €3 billion in COVID and is now once again starting to pick up. In 2017 as Vivendi was acquiring Havas, the domestic TV business had 8.6 million subscribers; it has grown that by ~900k. However, as with other businesses within Bolloré, Africa has been a real success story with subscribers more than doubling from 3.5 million to 7.6 million between 2017 and 2022. Other overseas - notably Asia - is up from 1.3 million to 2 million over the five years, with the overall subscriber base up just less than 10 million to 25.5 million at the end of December 2022.

{kind=link}

Given the strong growth in Africa, and other global market trends in the area, revenue per subscriber has continued to fall progressively over the period which makes the acquisition of new subscribers an imperative. There is an increasing sense that Canal+ is prepared to grow through acquisition and partnership.

The nearly 32% holding in the SA-listed MultiChoice ( OTCPK:MCHOY ) is a case in point. MCG has 23.5 million subscribers split between SA (9.5m) and the Rest of Africa (14.2 million); the SA portion has an average monthly subscription of ~US$11.65 with the prime attraction being the ubiquitous "Super Sport" [39] ; the non-SA subscribers pay around US$7.05 a month. MCG was spun out by NASPERS in 2019 and has been subject to the Bolloré-squeeze virtually ever since. The business has been beset by issues such as electricity outages in SA and rampant inflation in many of the countries in which the service operates, resulting in significant currency headwinds against the global cost of (especially) sports products.

A full acquisition of the majority stake would require around €1.6 billion (assuming a price of ZAR107 and a current exchange rate of €1=ZAR20.3); there would be no net debt assumption but a potential working capital shortfall suggesting the need for a €1.75 billion commitment.

More recently, on 20 June 2023, Canal+ forked out US$200m (€185 million for 26% in Viu, an HK-based streaming firm, backed by PCCW, as part of a US$300m investment; beyond that, Canal+ can move to a 51% stake. Viu has 66 million total monthly active users with 12 million paid subscribers.

Hence, it appears Canal+ has a creeping strategy of being the key player - multilingually - in a number of emerging Asian and African markets from its current beachhead. But how far will the Bolloré controllers stretch Vivendi's operations and investments?

Vivendi is valued as trash

We believe Vivendi's core earnings base from media, agency advertising, and games (less corporate costs) is valued at 1x EV/EBITA when the assorted investments and cash are stripped away; this is not dissimilar to companies such as News Corp where analysts perceive the core business to be slow growing and pressured by the mega-tech US companies.

We derive this low pricing of Vivendi's core earnings streams as follows:

| Shares owned (million) |

| Price |

| Value € millions |

| Vivendi equity |

| 1041.7 |

| €8.41 |

| 8,761 |

| Net debt [40] |

| Cash €2,298 |

| Debt €3,394 |

| 1,096 |

| ENTERPRISE VALUE |

| 9,857 |

| Universal Music (10.2%) |

| 181.8 |

| €20.35 |

| 3,700 |

| Lagardère (57.5%) |

| 81.4 |

| €21.45 |

| 1,746 |

| MultiChoice (31.6%) |

| 140.1 |

| ZAR95.49(€4.65) |

| 652 |

| EQUITY ACCOUNTED AT MARKET VALUE |

| 6,098 |

| Telecom Italia (17.04%) |

| 3,640.1 |

| €0.258 |

| 939 |

| FL Entertainment (19.76%) |

| 81.33 |

| €9.05 |

| 736 |

| Media For Europe "A" (24.2%) |

| 281.0 |

| €0.511 |

| 143 |

| Media For Europe "B" |

| 281.0 |

| €0.702 |

| 197 |

| Telefonica (1%) |

| 57.7 |

| €3.72 |

| 215 |

| Prisa SA (9.5%) |

| 67.3 |

| €0.38 |

| 26 |

| Viu (unlisted - cost 26.1%) |

| 185 |

| Undisclosed/units |

| 36 |

| INVESTMENTS |

| 2,477 |

| TOTAL "LISTED" |

| 8,575 |

| Editis held for sale (net assets) |

| 605 |

| INVESTMENTS + EDITIS |

| 9,180 |

| IMPLIED VALUE CONSOLIDATED EARNINGS |

| 677 |

| EBITA CY2023E |

| 683 |

| ADJUSTED EV/EBITA |

| 0.99x |

Why is Vivendi valued as trash?

Much of the reasoning behind the non-existent rating of Vivendi is based on the Lagardère transaction. Lagardère (MMB.PA) is a €3.4 billion equity value (at the last Vivendi offer price) focused around two key verticals:

- Publishing via numerous brands, notably Hachette, with leading positions in France, UK, #4 in the USA, and the third largest trade publisher globally generating revenue of €2.75 billion and EBITA of €302mn in 2022; and

- Travel retail, via the well-known "Relay" airport stores but numerous other niche localised brands. Travel retail was decimated by COVID but is rebounding strongly and generated €3.9 billion in revenue and €136mn of EBITA in 2022. These figures will increase strongly in 2023 given the 44% revenue gain in Q12023 over Q12022, aided by entry to new markets.

Lagardère has other activities including digital publishing and a small live entertainment business which generated €280 million in 2022 revenue at breakeven before restructuring costs. However, investors ponder whether this is just another "family" driven transaction to remove activist Amber Capital from the Lagardère register in return for past support of Bolloré by the Lagardère family in the 1980s - Jean-Luc Lagardère, the father of the current Chair, Arnaud.

We perceive nine reasons why Vivendi equity is valued so cheaply:

a. The equity market does not believe some of the investments to be fungible;

b. No indication of the sale price of the to-be-divested Editis to Daniel Kretinsky has been given (this sale has not been adjusted into our net debt estimates);

c. Vivendi may make numerous commitments to optimise cash flow which would see the current estimated net debt rise from €1.096 billion to close on €4.3 billion with the additional outlays for 60 million Lagardère (MMB.PA) shares at €24.10 plus the absorption of Lagardère's $1.7 billion of net debt;

d. On our estimates, Vivendi's core business trades at <1x EV/EBITA; based on the acquisition price for 100% of Lagardère, that business, which should generate ~€500 million of recurring EBITA in 2023 as travel continues to pick up, would be acquired for ~€5.2bn enterprise value or EV/EBITA of 10.2x - highly dilutive, unless done with Bollore cash.

e. Gaining full access to Lagardère wouldn't be easy; of the minority 43% holding, 12% is owned by Qatar Holding, 8% by Financière Agache (Bernard Arnault family office), 11% by Arnaud Lagardère associated entities, and 12% elsewhere - no fools or pressing needs for money amongst that group!

f. If Vivendi were to chase MultiChoice Group instead - and it has recently been creeping - it would be required to purchase a further 303 million shares at ( SAY ) €5.25 equivalent, requiring a further €1.6 billion-plus additional working capital, taking net debt (pre Editis) up to ~€2.8 billion+;

g. Bolloré appears to be "directing traffic" at arms-length to itself to create a slow-growing media business, whose cohort is presently valued very lowly in global markets - Discovery, News Corp. et al;

h. In the very short term Bolloré recently disclosed the sale of 18.6 million Vivendi shares reducing its stake to 27.9% which appeared to spook speculators postulating that a Bolloré bid for Vivendi was imminent; and

i. Further, in the short term, Vivendi recently fell out of the CAC-40 French core equity market index

Does that ring Bolloré's bell as they potentially seek to replace earnings from the logistics divestments, despite their recent share sale?

I: Bolloré

If you accept our methodology of removing the Treasury loop (section F) above, valuing Bolloré is surprisingly easy, with a little help from the independent expert [41] opinion and investment bank [42] assisting on the recent buyback.

We can take a mixture of the independent expert valuation (before the application of their methods to deal with the Treasury control loop and conglomerate discount) [43] and the Nataxis explanation [44] allied to adjustments for the actual buyback achieved (99.1 million shares) and recent small sale of Vivendi shares to come up with the following tabulation:

| €million |

| Comments |

| Bolloré Logistics |

| 5,000 |

| Per option deal with CMA CGM |

| Bolloré Energy |

| 448 |

| Per A2EF |

| Storage, systems, and films |

| 704 |

| Per A2EF & Nataxis |

| Agricultural assets |

| 82 |

| Per A2EF |

| Other listed investments |

| 246 |

| Per Nataxis |

| UMG shares |

| 6,634 |

| 326 million at €20.35 |

| Vivendi Shares |

| 2,405 |

| 286 million at €8.41 |

| Holding company costs |

| (1,213) |

| Per Nataxis |

| Cash |

| 1,831 |

| A2EF less buyback (€570m) plus VIV sale (€177m) |

| Provisions and minorities |

| (571) |

| A2EF |

| TOTAL EXCLUDING TREASURY CONTROL LOOP |

| 15,566 |

| Issued shares after elimination |

| 1,184 |

| See section F above |

| VALUATION BEFORE DISCOUNT |

| €13.15 |

| per share |

On any reasoned analysis, Bolloré shares are extraordinarily cheap, with the current share price and market capitalisation virtually backed by the shareholding in UMG, let alone €6.2bn of net cash IF the logistics transaction is consummated. It is clear that equity analysts struggle with the Treasury control loop implications, even years after Muddy Waters showed how to deal with it.

Perhaps the central question in Bolloré aficionado's minds is the potential for Bolloré to acquire one or more groups in the Bolloré Galaxy. Most obviously, Vivendi. But before we examine that possibility, we need to look at the head company, where the puppeteer resides: ODET.

J: Compagnie de L'Odet

Compagnie de L'Odet (ODET.PA) (as Financière de L'Odet) was utilised as the most proximate holding company to the publicly listed components of Bolloré in 1985 with outside capital from three shareholders, including the Lagardère family. In 1992, SEPA, an entity listed on the Marseilles cash market was utilised as a back-door listing entity for Financière de L'Odet. After the reconstruction of SEPA - which was 90% owned by ODET - to absorb ODET, the new entity ended up with an investment portfolio primarily comprised of 10.732m shares of Albatros Investissement with a value of Ffrs 110 each.

There were no new shares issued to entities other than the immediate "old ODET" shareholders, leaving the new ODET (nee SEPA) after a 10-1 bonus issue with 5,831,991 shares on issue at FFrs100 (€15.24). Hence, if you held one of the lucky 14,729 shares (€244k) of ODET at inception, you now have yourself a hundred bagger over just less than 31 years.

Because of the structure of the Bolloré Galaxy, somewhat bizarrely, despite the 100-bag, ODET is still cheap.

ODET is the main equity owner of Bolloré, with 69.1% of the shares after the recent buyback. In turn, Bolloré owns 35.6% of ODET; the main owner of ODET is the company one step up the cascade, Sofibol, which has recently been acquiring small amounts of shares to add to its 55.3%. Adding in Bolloré's cross-holding of 35.6% and other small "galaxy" holdings, the public owns a mere 7.4% (488k shares) of ODET.

ODET's asset base -before any Treasury loop adjustments - is simple:

| €million |

| Comments |

| Bolloré shares |

| 11,284 |

| 1971.6 million at €5.71 |

| Vivendi shares |

| 50 |

| 6 million at €8.41 |

| Debt (per 31 December 2022) |

| (495) |

| Per deconsolidation of Bolloré |

| Dividend paid |

| (24) |

| TOTAL NET ASSETS |

| 10,815 |

| Issued shares |

| 6.586 |

| Excluding elimination |

| VALUATION BEFORE DISCOUNT |

| €1,642 |

| per share |

If we work through the cross-shareholding elimination, ODET's share count comes down to 5.628 million but its Bolloré shareholding is partly eliminated as well:

| €million |

| Comments |

| Bolloré shares |

| 9,620 |

| 1684.7 million at €5.71 |

| Vivendi shares |

| 50 |

| 6 million at €8.41 |

| Debt (per 31 December 2022) |

| (495) |

| Per deconsolidation of Bolloré |

| Dividend paid |

| (24) |

| TOTAL NET ASSETS |

| 9,151 |

| Issued shares |

| 5.628 |

| Including elimination |

| VALUATION BEFORE DISCOUNT |

| €1,626 |

| per share |

Hence, at the current market price of Bolloré, ODET at €1554 is only trading at a marginal 4% discount to the parent company. However, if we start to impute our re-valued Bolloré, the discount widens appreciably:

| €million |

| Comments |

| Bolloré shares |

| 22,145 |

| 1684.7 million at €13.15 valuation |

| Vivendi shares |

| 50 |

| 6 million at €8.41 |

| Debt (per 31 December 2022) |

| (495) |

| Per deconsolidation of Bolloré |

| Dividend paid |

| (24) |

| TOTAL NET ASSETS |

| 21,676 |

| Issued shares |

| 5.628 |

| Including elimination |

| VALUATION BEFORE DISCOUNT |

| €3,851 |

| per share |

Hence, as with Bolloré, the discount is up around the 60% mark to see through value.

K: How might the future play out?

Bolloré-Vivendi merger

Assuming the completion of the logistics deal, Bolloré Galaxy will have far too much cash - over €6.3 billion net in Bolloré alone. At some stage, we would assume the cash will be put to use. But there are lessons from the source of the cash - the two logistics businesses - where Bolloré encountered the most acute difficulties in its public company life.

Vivendi has plenty of potential commitments, which is arguably why it did not enter the bidding for the Paramount book publisher Simon & Shuster, whose US$2.2 billion deal with Penguin Random House was blocked for anti-competitive reasons in 2022.

A Bolloré-Vivendi merger makes a lot of sense; if Vivendi pursued a full takeover of Lagardère, it would have an estimated €4.3 billion of net debt; to acquire the Vivendi "minorities" would require Bolloré to spend €7.4bn in cash (at €10/share) - €1bn+ over its net cash. Our estimates suggest a merged Bolloré-Vivendi-Lagardère would hold ~€5.7 billion of net debt. A merged Bollore-Vivendi was only about €2.1 billion. A pursuit of MultiChoice Group: debt of ~€3.8bn if Vivendi merged with Bollore.

Does any of these amounts sound too high? They need to be set against the merged entity having:

- 28% of Universal Music Group is currently priced at over €10.3 billion;

- Vivendi's other investments + Editis less MCG currently priced at over €3 billion; and

- Bolloré's other assets and businesses valued at €1.5bn

ODET-squeeze out [45] ?

If there is one comment and subsequent activity that has stirred Bolloré aficionados in the past few weeks it was the apparent comments by Vincent Bolloré at the ODET AGM (14 June 2023) about the ODET share price being too low and that "he would do something about it". Since then, Sofibol the next company up the cascade owning over 57% of ODET has been buying more aggressively than seen in some time.

It is noteworthy that Bolloré does not DIRECTLY own the shares in ODET - they are mainly owned by Compagnie du Cambodge (19%), Société Industrielle et Financière de L'Artois (5.6%), and Financière Moncey (4.9%). As is the case with the squeeze-out of Socfin, where Bolloré is giving their voting rights to Hubert Fabri to facilitate the squeeze-out, we ponder if it is in the throes of happening here.

The problem with a squeeze-out - legal action by the highly committed and intelligent minorities who are very aware of the significant upside in ODET. A squeeze out at €2,500 - still a large discount to our valuation - would require about €1.2 billion. But remember from the Delmas-Vieljeux deal, Bolloré is reluctant to get into a dispute with outside experts and market regulators, especially "at the end of the game"

Are the odds against both deals happening? Less than you think we suspect. However, it really depends on a fit-septuagenarian moving from enormous cash (assuming logistics completes) to a potentially respectable debt load, albeit against exceptional assets but closer to his "heart".

Even Murdoch doesn't do that anymore. But he's 20 years older. Whatever the outcome, heavily discounted stock prices and a quasi-Henry Singleton/Teledyne [46] scenario with billions of spare euros makes for a series of appealing investment opportunities.