UNVGY - East 72 Dynasty Trust Q4 2023 Quarterly Report

2024-01-11 05:18:00 ET

Summary

- East 72 Holdings is a unique Australian publicly listed investment company listed on the National Stock Exchange of Australia and is a leveraged investment company.

- Dynasty Trust benefited from diverse individual stock positions during the quarter.

- We have made assorted adjustments to the valuation to account for the substantial issuer bid in November in both ELF and UCL.

Performance and net asset value

| Quarterly return †: 5.67% |

| NET ASSET VALUE PER UNIT AT 31 DECEMBER 2023 †: $1.0695 |

† after all ongoing and performance fees. The high water mark on 31 December 2023 is $1.0723/unit

Global equity indices generally rose in the December quarter by 7-10%, with a strong rebound since the end of October, as a more positive - almost euphoric - narrative regarding the direction of US interest rates began to coalesce. This reversed the spike in US long bond rates seen in the prior quarter, continuing a high level of volatility in the price (and yield) of the planet's ultimate reserve long-duration asset. China-related markets continued to fall, and a number of European markets showed only modest gains. A rise in the Australian dollar against all major currencies over the quarter hampered returns - we estimate by 1.5% over the quarter - since we deliberately do not hedge the currency.

Dynasty Trust benefited from diverse individual stock positions during the quarter, with two new additions - Ocado plc ( OCDGF ) ( OCDDY ) (November) and Fairfax India Holdings ( FFXDF ) (December) - both contributing significantly, rising 31.6% and 13.3% above purchase price. As would be expected in such a euphoric environment, we had several other 20%+ gainers, notably Catapult Group ( CAZGF ) (+29%), Pershing Square Holdings ( PSHZF ) (+27.5%), Aviation PLC (+26.4%) and News Corp. ( NWS ) (+22.4%).

Dynasty Trusts' top twenty positions as of 31 December 2023 as a percentage of net asset value are:

| Catapult International |

| 4.11% |

| D'Ieteren Group ( SIETY ) |

| 2.92% |

| Compagnie de L'Odet ( FCODF ) |

| 4.11% |

| E-L Financial Corp ( ELFIF ) |

| 2.87% |

| Vivendi ( VIVEF ) |

| 3.65% |

| Softbank Group Corp. ( SFTBY ) |

| 2.86% |

| Société des Bains de Mer ( BMRMF ) |

| 3.37% |

| MFF Capital Investments |

| 2.79% |

| Ocado PLC |

| 3.30% |

| Aviation PLC |

| 2.76% |

| Fairfax India Holdings |

| 3.25% |

| Lion Selection Group |

| 2.59% |

| Bolloré ( BOIVF ) |

| 3.07% |

| Christian Dior ( CHDRF ) |

| 2.50% |

| Magellan Financial ( MGLLF ) |

| 2.97% |

| Senvest Capital ( SVCTF ) |

| 2.50% |

| Robertet SA ( RBTEF ) |

| 2.93% |

| Harworth Group PLC |

| 2.48% |

| Virtu Financial ( VIRT ) |

| 2.92% |

| TFF Group ( FRFTF ) |

| 2.43% |

At quarter end, we hold around a 4% cash weighting.

Over the quarter, we exited some smaller positions where we were unable to prove the investment thesis to a competitive level against other stocks in the portfolio and added new positions in Ocado PLC and Harworth Group PLC in November with more recent additions of Softbank Group Corporation and Helloworld Limited in December. Softbank, the parent company effectively controlled by Masayoshi Son is extremely complex and controversial with numerous off-balance sheet financing structures. We have followed the company for some years and believe the IPO - small though it is - of ARM Holdings, the UK manufacturer and designer - is a key plank in reducing risk and enabling the discount to NAV which is in the high 40% area - to be closed up.

Helloworld is an Australian travel facilitator in both retail and wholesale markets and is benefitting from vastly increased demand for outbound travel but should see more benefit from the slower-paced recovery of inbound visitation. The company is conservatively financed and effectively controlled by the Burnes family who are its largest shareholders and occupy key management roles. The shares trade at a significant discount to their local peers.

One year in (ninety-nine to go)

The equity market environment in 2023 was especially strange, with an enormous focus on the seven large US-based mega-cap technology companies, and their very positive influence on domestic US equity performance. In our view, the most bizarre aspect of this outcome was the treatment of these companies as homogenous, when their prospects and challenges are quite different. We suspect this divergence will play out much more over 2024.

Frustrations: stocks that have done less well than we hoped in 2023 - but we are happy holders

Bolloré. Investors have increasingly embraced the merits of Universal Music Group (+14.6% in € terms in 2023) as they have Spotify ([[SPOT]] + 138% in 2023, and recognised the two are integral to each other. UMG is the largest asset in the Bolloré galaxy (cash is next) - but the translation of the paper gains to the relevant Bolloré companies (ODET.PA, BOL.PA, VIV.PA) has been proportionally non-existent. ODET is trading below the levels of the first week of January 2023. We hope that as the proceeds from the sale of Bolloré European logistics are received and the future group pathway becomes clearer, these translations and other positive initiatives will be reflected in the stock price. We know value has been built - it's just not yet exhibited.

VW/Porsche Group ( VWAGY )/( POAHY ). Whilst other conventional vehicle companies' share prices performed well in 2023 - few better than Stellantis ( STLA ) which rose 64% over the year[1] - the VW complex struggled as earnings and revenues failed to match company projections at the end of 2022. Revenue growth was still a healthy 16% through September (cf STLA +10%) but the China impact has weighed heavily on the group, not just directly through the VW JV's but also through sharply lower Porsche (P911.DE) deliveries, which has sent the 75% owned subsidiary's shares down from a peak of €120 down to the effective IPO price of €80 by year-end 2023. VW sales in China were down 3% YTD through September 2023 in contrast to 23% gains in Europe; China is still 35% of VW Group sales units and the shares remain perceived by investors - frustratingly - as a "Chinabeta" play. VW shares returned 3.7% in 2023 including the generous €8.91 dividend. With Chinese and Hong Kong stock markets again weak - HK's Hang Seng index is down four years running - this is a particularly hefty weight against the world's view of US vehicle tech domination.

China. VW's largest shareholder Porsche Automobil Holding (PAH3.DE) was "double-China'd" through its ownership of VW and the direct 12.5% stake in P911. No surprise the shares fell ~10% over the year. We are happy that the Porsche/Piech families are on the right track with their overhaul of VW. The issues with Chinese growth not matching expectations, together with regulatory volatility also impacted our two Swiss holdings, CFR and Swatch ( SWGAY ) with the "mid-luxe" sector falling out of favour as the year progressed.

Opportunity cost. We owned Alphabet ( GOOG ) early on but sold the shares as we felt the valuation had run too far. Likewise, at the time we established the Dynasty Trust, we owned Meta Platforms ( META ) in other accounts, but those shares ran ahead and didn't retrace to where we felt comfortable entering. We underestimated Meta's cost reductions and revenue growth.

Preamble on compounding

The concept of "compounding" in equities - holding an investment for a lengthy period of time to enable the concept of compound interest/return from reinvested earnings to work its magic - is not complex. The selection of the investment is where the controversy starts. The best-known compounding company on earth - Berkshire Hathaway ( BRK.A ) ( BRK.B ) - has done so via multifarious means ranging from the adroit use of profitable insurance and reinsurance cash flow/float, selection and retention of high-quality publicly listed securities, purchase of strong businesses at attractive prices and retention of high levels of liquidity to avoid cyclical distress, promote strength and partnership capacity together with bouts of opportunism rarely seen elsewhere. No dividends.

Insurance - especially in life insurance, providing there is ongoing sales growth - once matured, and subject to conservative management, is amongst the best compounding businesses around. It offers potentially long periods where the company retains policyholder cash upon which returns can be obtained prior to eventual payment or hopefully, ultimate retention as the insured risk expires. Depending on the type of policies written - mortality rather than morbidity - the aging population is an even stronger benefit. For obvious reasons, life insurance companies tend to spawn asset management businesses, which should have a high return on capital affairs.

Compounding sits logically alongside the Dynasty Trust, since (especially) family-controlled companies tend to be long-term owners of their businesses, nurturing them, and expanding them carefully through acquisition, in turn allowing earnings and returns to compound over time. As the TFF Group[2] vision statement says "Time is on our side".

The company we discuss below is based in Toronto. Canada is an astonishing breeding ground for family-controlled enterprises of substance; moreover, it has a survey produced by the National Bank of Canada ( NTIOF ) which is produced regularly to track their performance[3]. The latest publication - December 2023 - is the fifth research report since the inaugural 2015 edition. The 43 companies contained therein account for 25% of the S&P/TSX (Canadian) wider equity market index and have a market value of C$ 700 billion at publication.

E72DT holds four Canadian stocks, all of which are family-controlled and in the finance sector; none are in the NBC Family Advantage survey as they have insufficient trading liquidity to qualify. All have exceptional long-term track records (though volatile in the case of Senvest Capital), and all trade at enormous discounts to NAV; Canadian General Investments - a closed-end fund established in 1930 - trades at a 38% discount to NAV, despite a portfolio where three of its four largest holdings are NVIDIA ( NVDA ), CP Kansas City Limited ( CP ), and Apple ( AAPL ).

The analysis which follows covers the two related companies E-L Financial Corporation (ELF.TO) and Economic Investment Trust ( ECVTF ) (EVT.TO). The story is ~100 years old, but investors' lack of willingness to interrogate life insurance accounts, in our view leaves ELF shares trading at close to a 50% discount to real worth. To understand how value in ELF has built over time, we have researched back through newspaper filings to the 1920s, compiled a seventeen-year compounding table of the predecessor company through the 1950s and 1960s (21.4%pa total return over that period), and benefitted from Canada's respectable preservation of corporate history.

E-L Financial Corporation: 100 YEARS of compounding available at half price [4]

If you bought ONE share of Empire Life Insurance - formed in Toronto in 1923 - upon its public float[5] in October 1951 at ~C$19.25, you would now have 44 shares[6] of E-L Financial Corporation worth $46,122 at 31 December 2023 and have collected dividends of $12,303 along the way[7]. That's an internal rate of return of 13.1% pa across over 72 years.

Despite this staggering performance, in our view, the shares are fundamentally undervalued and the controlling owners clearly know this, having changed a long-standing capital management strategy four years ago.

E-L Financial Corporation ((ELF)) is a Toronto-based life insurance holding and investment company controlled by the Jackman family, now in its third generation of stewardship. They are (effectively) beneficiaries of 100 years of compounding with the 2023 centenary of the "E-L" piece - Empire Life Insurance Company, based two and a half hours north-east of Toronto in Kingston, Ontario. In addition to owning 99.4% of Empire Life, E-L runs its own $4bn+ investment portfolio and controls 56% of the listed closed-end fund United Corporations Limited. These businesses are consolidated into the financial statements of ELF. Additionally, there are two associated companies Algoma Central (37% owned) and Economic Investment Trust[8] (25% owned); EVT's largest investment is E-L Financial Corporation.

ELF is remarkable - there are effectively fewer shares on the issue than was the case when the company was formulated in its present state in early 1970. The Jackman family has a reputation for parsimony[9] but the biggest advantage for shareholders is that their greatest area of thrift is arguably in the issuance of shares of their companies. This is a long-term observable trait across the three Jackman companies of interest which makes Warren Buffett seem almost profligate in equity issuance[10]. That the Jackmans have started to retire equity since 2020 magnifies this attribute .

What follows is not a family history of the Jackmans but touches on the key relevance to ELF. The first Jackman generation, led by Henry R. (Harry) Jackman became involved in the securities industry at Dominion Securities in the 1920s, alongside Charles P. Fell. Fell left in 1929 to "straighten out"[11] Empire Life. Over the next 30 years, Harry Jackman spent nine as a Canadian MP but acquired control of a number of closed-end funds, most notably the then publicly traded Dominion & Anglo Investment Corporation Limited [12], currently ELF's largest (41%) shareholder.

In 1956, Harry joined the Empire Life board, becoming Chair in 1957, acquiring a substantial interest from Fell in 1959. In the meantime, Harry's son Henry N.R. ((HAL)) Jackman had commenced an investment career which saw him take an increasing interest in Empire Life[13].

Empire Life

Empire Life Insurance Co was formed in February 1923, and in August 1929, having built assets to $699k effectively acquired Commonwealth Life and Accident Insurance (assets $621k) to enlarge the company. Fell became President of Empire in March 1933, a position he held until February 1967. Empire acquired Mutual Relief in 1935.

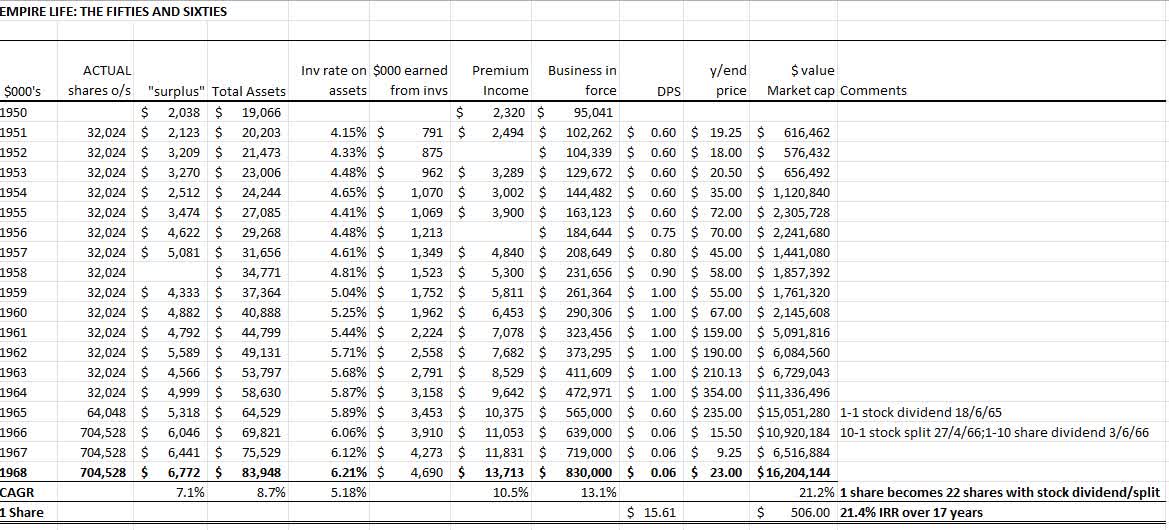

Empire Life shares, in partly paid form, were unlisted but tradeable via brokers until 15 October 1951, when its reorganised 32,024 shares of par value $10 were listed on the Toronto Stock Exchange, with early trades at $19. The table overleaf shows how the company rode an astonishing wave of growth in life insurance post-war, which took Canadian life insurance premiums to over 3% of GDP.

Empire's premium income grew at over 10% per annum for 17 years, constantly adding to a pool of assets on which an average 5.2% pa was earned (the assets were mainly bonds). With a conservative approach to dividends, and no new share issuance other than stock dividends and stock splits, this resulted in a significant compounding of per share value by 21%pa over the 17-year period.

Henry Jackman's significant shareholding was joined by his son, the current patriarch Hal Jackman, by the late 1960s, by which time they had jointly acquired 47% of Empire's shares. The means of acquiring these shares was via control/influence over a number of (then) listed closed-end funds[14], most of which have subsequently been de-listed.

In November 1968, Empire became the first Canadian life company to break the shackles of regulation, which prohibited any Ontario-based life company from owning more than 20%[15] of the shares of another corporation. The strategy used was the same as in the US at that time and more latterly used in Australia by Macquarie Group (late 2007) and ANZ Banking Group (early 2023) - the use of an over-arching holding company structure whereby the regulated entity became a subsidiary.

In November 1968, Empire offered its shareholders 4 new shares of E-L Corporation plus a single warrant to purchase ELF at $12 in exchange for every 2 Empire shares. With the Jackmans in control, the offer rapidly gleaned acceptance and by January 1969 Empire was a 90%+ subsidiary of ELF. So Empire Life's 706,034 shares in late 1968 became, after full warrant exercise, 1.765m ELF shares.

The move was made because the Jackmans had a strategy: in January 1969, acquired agreed control of Dominion of Canada General Insurance (Dominion) with a scrip offer by ELF of 3 convertible preference shares, 7 common shares, and a $12 warrant per Dominion share. Effectively 10-1 on Dominion 202,000 common shares.

On conversion of the preference shares (and warrants from both Empire and Dominion transactions), these would be the last new securities of any note issued by E-L Financial to this day. With recent capital management initiatives, ELF now has effectively fewer shares on the issue than in 1971[16].

So with minimal share issuance between 1923 - 1951, for Empire Life, no share issuance between the public listing in 1951 to the ELF transaction in late 1968/early 1969, and the two warrant issues plus script bid for Dominion, the exercise in 1968/69 is, we believe, the only new equity ELF and its predecessor has issued in a century.

Given that the equity issued to buy Dominion was worth $25 million at the time, Dominion was stripped of its life company (estimated 20% of value), and the general insurer sold to Travellers for $1.08 billion in November 2013, maybe they should do it more often...

{kind=link}

ELF further developed the insurance business in 1986 by acquiring Montreal Life from Guardian Royal Exchange, in an innovative arrangement that involved issuing no holding company securities, but allotting GRE 19% of a subsidiary company holding the enlarged life business. The empire was subsequently supplemented with books of business from other life insurers and with two small acquisitions.

ELF bought out GRE in December 2015 at approximately book value (19% for $199.9 million) thereby increasing the effective ownership of the enlarged Empire back up to 99.3%. Empire has been able to finance itself with a series of preference share issues, which were listed on TSX until 2021, although the only residual series ($100mn) remaining is entirely held by ELF. In 2021, Empire issued the first limited recourse notes by a Canadian insurer and has continued to use subordinated debentures.

What might Empire Life be worth? How IFRS17 changes the environment

Empire's business has not changed radically in some years. The company has three key areas:

- Wealth management, comprising segregated funds of some $8.5billion and annuities of $850million;

- Group Solutions; and

- Individual insurance, the longest-standing component of the company.

The wealth management business is a management fee-driven division with management fees derived for the investment management of the segregated assets - effectively investments with some form of death benefit guarantee or guaranteed minimum withdrawal benefit (akin to an endowment policy); insurance contracts make up 95% of the segregated fund business. This business has significant equity market exposure with >70% of assets in preferred and common stocks at the end of September 2023. Hence, the business is directly sensitive to equity market levels with respect to fees but also with respect to product sales which fall away in times of equity market dislocation.

Group Solutions focuses on small to medium-sized companies offering benefits such as dental, assorted medical, accidental death, and more niche products in travel assistance. The market for these products is consistently competitive and the expected profit on inforce business of $25-$30million per annum has been eroded in the past two years by adverse claims experience, including internal issues related to staffing. Hence, despite pulling in over $450m of premium income, the division is barely profitable with an expense-to-premium ratio of over 25%.

Individual insurance - term life and universal life - has expected profits per annum of ~$50 million; however, recent results have been volatile due to changing interest rates (positive when rates rise as discounted liabilities fall) but also changes in claims and especially lapse rates, a fundamental issue for insurers worldwide. However, the business continues to generate slow but steady premium growth on a current level of $450m per annum and under normal conditions is highly profitable given the substantial investment backing to policies.

IFRS17

IFRS 17 is the International Financial Reporting Standard relating to insurance, which has radically changed the reporting environment fall all insurers. Within the life area, it places a more onerous demand on actuarial reporting but has an excellent trade-off in giving a relatively solid and assessable performance component.

What follows below is HIGHLY simplified and does not get into the actuarial mechanics of different approaches to measurement of the variables. Imagine a simple term life insurance policy - one that only operates for a specific term (say 20 years) and pays out in the event of the death of the policyholder. In pricing the product, the insurer builds on assumptions regarding the probability of death (mortality), interest rates, and investment returns over the period, together with a profit margin. These calculations are more complex, and the policy is far more expensive if it is a permanent (or whole of life) insurance policy where a savings component is involved together with providing insurance until death.

The new accounting concept is CSM - contractual service margin - which is crudely the profit expected to be released over time from insurance policies written; the value is NOT held on the balance sheet. If the insurer writes no new business, then the margin released in each accounting period - which is solely from the insurance component - will simply reduce the value of CSM[17]. Amendments to CSM are generally carried "below the line" by insurers in their profit and loss accounts. Moreover, the addition to CSM from writing new insurance business does NOT go through the profit and loss account but is an effective off-balance sheet actuarial item.

Life insurers now carry pages of assumptions and assumption changes in their reporting relating to their exposures including CSM. But critically, the ability to grow CSM through writing profitable new business will lead to a building of future profit growth for the insurer. We believe this is best summed up by two slides released by Prudential PLC in July 2023 at its IFRS17 briefing[18]:

{kind=link}

Comparisons between companies will reflect the different nature of their business composition, as well as changes in assumptions over a period. With most companies, there is only a seven-quarter period from end-

December 2021 to glean an idea of the development of CSM.

As the second Prudential slide shows, there can be significant movement in the value of CSM even in individual periods by changes in "economic assumptions" which move with amendments to real-world discount rates.

Analysis of the comparative pricing of life companies is moving away from metrics such as price to embedded value to more earnings-based metrics but also looking at "adjusted price to book value" ratios, where CSM is added to a measure of book value (tangible or otherwise) to provide a basic comparative assessment of companies.

Over time, price/adjusted book value will reflect expected growth rates and returns on capital, as it historically has done in the banking and insurance sector. However, it will take a few years yet to see the analysis fully evolve, especially as its first full year has coincided with absurd volatility in US ten-year bond rates, which has translated to other global risk-free metrics.

Lining up Empire with the cohort

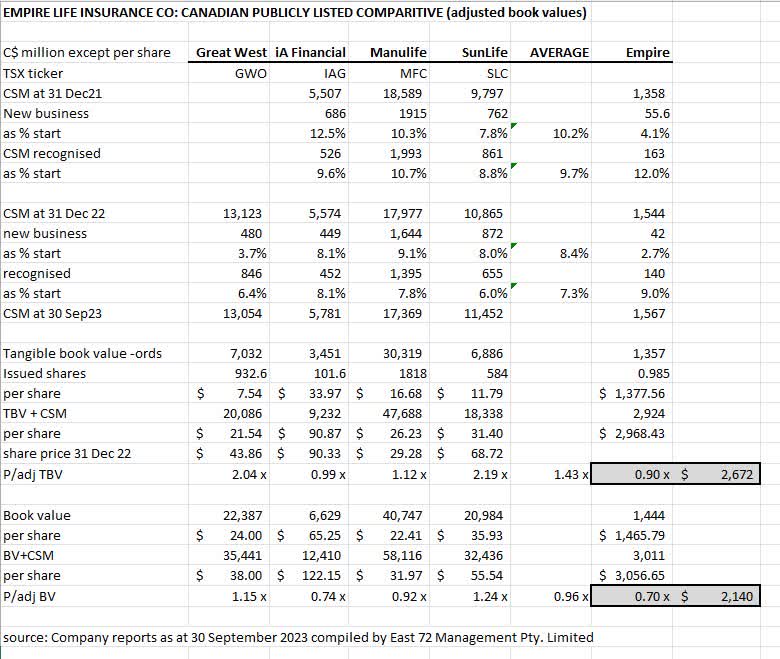

Empire is the 9th largest life-based company in Canada measured by assets, but only eleventh by premiums[19]. Aside from the four publicly listed cohorts below, Empire is smaller in premiums than four significant mutuals (Desjardins, Beneva, Wawanesa, and Equitable Life) together with two bank-owned units (RBC Insurance and BMO Life).

There are four major life insurance-based companies publicly listed in Canada. All have specific angles with significant non-Canadian operations: Manulife generates less than a quarter of core earnings from Canada with businesses in Asia and the USA being equivalent in size[20]; Sun Life owns a significant global asset management business (MFS) and in combination, the US and Asian insurance and related businesses are producing as much income as Canada[21]; Great-West (owner of Canada Life) has just divested its Putnam Investments asset management business but massively expanded its US business in 2022 with the US$3.5billion acquisition of Empower, the retirement services business of Prudential Financial ( PRU ) (not Prudential PLC).

The nearest real comparative in the publicly listed sphere for Empire is iA Financial ( IAG:CA ) ( IAFNF ) (IAG.TO) a C$9.2bn market capitalisation business, which has a US operation but is still dominated by its Canadian business with similarities to Empire.

Not surprisingly, in keeping with the ethos of ELF, Empire stands out as an asset-rich, modest-growth company against the giants of the industry. However, it has been consistently profitable and an attractive dividend payer to ELF since the 1968 reorganisation. As a guide, since 2010, Empire has paid out $550 million in dividends to ELF, including $75 million in the 2023 period through to the end of October. Most notably, when ELF commenced its equity retirement program in March 2020, the first tranche was funded by Empire's declaration of a $113/share dividend in late February 2020 - yielding $111 million in one fell swoop to ELF.

On 30 September 2023, Empire had a net worth of $1.74 billion (including $100million preferred stock all held by ELF) and capital notes; removing the preferred, capital notes and $87million of intangibles gives Empire's tangible book value on 30 September 2023 of $1,357million ($1,377 per Empire share of which there are only 985,076 being 99.4% owned by ELF).

Adding the disclosed contractual service margin on a pre-tax basis of $1,567 million[22] to this would give an adjusted book value of $2,924 million. Allowing for goodwill would boost this to just over $3 billion.

We have tabulated a comparison of the four largest publicly listed entities with Empire below:

There is a clear premium pricing afforded to the two enterprises with asset management arms of the brand which cannot be translated onto Empire, especially when seen against its modest new sales additions to Contractual Service Margin, which has been maintained by changed economic assumptions.

In our opinion, using metrics at a discount to the lowest publicly listed cohort ((IAG)) would price Empire at between $2,140 - $2,672 per share or $2,108 - $2,632 million. This is somewhat greater than prior estimates we have used of ~1.88 billion for the common equity of Empire and supports a higher valuation of ELF.

{kind=link}

We average the two methodologies and use a gross value of $2,350 million for Empire in our "market value" tabulations below.

United Corporations Limited

United Corporations Limited ( UCPLF ) ((UCL)) is a C$2 billion closed-end fund established in 1933 from the remnants of Consolidated Investment Corporation, which defaulted on its loan commitments. The full history of UCL, with every year's equity base, adjusted NTA, and stock dividend is laid out in each year's annual report. The entire stock portfolio is disclosed each quarter. We deconsolidate UCL in valuing ELF.

UCL is a global investor with three external managers - Comgest Asset Management (Dublin) with - $550mn, Causeway Capital Management (Los Angeles) with $500 million, and Neuberger Berman Canada with ~$1 billion having being allotted an approximate quarter tranche of assets from the displaced manager, Harding Loevner. UCL has a 9.4% shareholding in Algoma Central (ALC.TO), a 27.8% direct associate of ELF but which accounts for only ~2.6% of UCL's assets.

ELF's involvement with UCL began in May 1972 when they acquired a 13% block of shares at around a 17% discount to NAV ($17 versus NAV of $20.39). ELF built the stake up over 40% by 1976 as the share price of UCL fell in line with equity market distress at the time. ELF's stake remained at just over 40% for some thirty years, before it was built to 46% in 2008 and finally consolidated with over 50% in the final quarter of 2012. A Jackman-related company, UnitedConnected Holdings, owns a further 2.744 million shares.

UCL has historically traded at a significant discount to NAV - currently around 37%[23] - despite recent share buybacks in tandem with those announced for the parent, weekly NAV announcements, and a full portfolio disclosure. This reflects:

- the extraordinary portfolio diversification with 730 stocks as of 30 September 2023 (excluding ALC.TO) across USA (356) Europe (160), UK (44), Japan (93), Emerging Markets (49), and Australia (28); effectively UNC is a lowish cost (0.6%pa before stock lending income) global exposure;

- the fact that after the recent off-market buy back[24], ELF controls 56.6% of the capital and the Jackman-related company a further 24.4%, leaving a free-float of only 19% (2.141m shares) or ~$260m of equity capital

Equity retirement

In tandem with ELF and EVT, UCL has made six equity retirement initiatives since March 2020 - similarly four "normal course issuer bids" (on-market buybacks) and two "substantial issuer bids" (off-market tenders) retiring 7.6% of 2020 capital at a 39% discount to current NTA.

| date |

| nature |

| concluded |

| shares |

| Av. price |

| Spend ($000s) |

| March 2020 |

| NCIB (buyback) |

| March 2021 |

| 95,700 |

| 81.92 |

| 7,840 |

| March 2021 |

| NCIB (buyback) |

| March 2022 |

| 14,600 |

| 107.56 |

| 1,570 |

| March 2022 |

| NCIB (buyback) |

| March 2023 |

| 24,400 |

| 92.91 |

| 2,267 |

| Sept 2022 |

| SIB (tender) |

| Sept 2022 |

| 454,545 |

| 110.00 |

| 50,000 |

| March 2023 |

| NCIB (buyback) |

| March 2024 |

| <580,102 |

| n/a |

| n/a |

| Dec 2023 |

| SIB (tender) |

| 338,983 |

| 118 |

| 40,000 |

| TOTAL |

| 928,228 |

| $109.54 |

| 101,677 |

Valuing ELF on a sum-of-the-parts basis

ELF is a relatively simple deconsolidation of Empire Life and UCL, then valuing these entities separately; we add in other investments at market value, even though there are significant discounts involved in the closed-end fund companies.

ELF itself excluding UCL or other related investments has a diverse common and preferred stock portfolio of just under $4.2billion on 30 September 2023; given strong equity markets in Q4 CY2023 (S&P 500 +11%, S&P/TSX Composite +7.2%) it is not unreasonable to believe this portfolio could have returned 6%+ in the quarter giving it a value at end December 2023 of over $4.4billion.

We have made assorted adjustments to the valuation to account for the substantial issuer bid in November in both ELF and UCL (we discuss Economic Investment Trust ((EVT)) separately). We do NOT make adjustments for the circular shareholding that EVT holds in ELF, which would increase the value per share further.

Our two sets of valuations coalesce to a degree; valuing everything at NTA brings down the value of Empire whilst carrying UCL at some $300 million (~ $87/share) above its public market price. The reduction in the value of UCL and EVT to account for the public market discount is offset by the increased value - even allowing for an increased assumed tax impost - for Empire Life. Our tabulations as of 31 December 2023, allowing for recent share buybacks and some investment gain in the parent in Q4 2023 are given below:

Hence, at the prevailing price of $1048 at the end of December 2023, we view ELF as trading at a 47% discount to a reasoned current value of the company, with an increased chance of the value emerging over time.

Why? Think back to the preliminary comments of ELF having fewer shares on issue NOW than in 1971. Since early 2020, ELF has thrown away its long-standing policy of not buying back shares and has completed six equity retirements (one is ongoing) as follows:

| date |

| nature |

| concluded |

| shares |

| Av. price |

| Spend () |

| March 2020 |

| NCIB (buyback) |

| March 2021 |

| 200,970 |

| 599 |

| 120 |

| Nov 2020 |

| SIB (tender) |

| Dec 2020 |

| 109,863 |

| 750 |

| 82 |

| March 2021 |

| NCIB (buyback) |

| March 2022 |

| 9,800 |

| 916 |

| 9 |

| March 2022 |

| NCIB (buyback) |

| March 2023 |

| 35,060 |

| 866 |

| 30 |

| Aug 2022 |

| SIB (tender) |

| Sept 2022 |

| 103,626 |

| 965 |

| 100 |

| March 2023 |

| NCIB (buyback) |

| March 2024 |

| <177,854 |

| n/a |

| n/a |

| Nov 2023 |

| SIB (tender) |

| Dec 2023 |

| 90,668 |

| 1050 |

| 95 |

| TOTAL |

| 549,987 |

| $792.75 |

| 436 |

The six completed equity retirements have seen ELF acquire 13.5% of the capital outstanding before the announcement, at a discount of 40% to the 31 March 2020 quarter's NAV (the recent low point) or at a 56% discount to the last disclosed equity value per share of $1,792 at 30 September 2023. The equity retirement is at a 60% discount to our mid-point valuation of $1979 per share .

We can't think of too many other capital management initiatives adding so much value - if only more shares could be acquired.

A double discount way to play ELF: Economic Investment Trust

Economic Investment Trust ((EVT)) has a real history: it was the first closed-end investment trust formed in Canada in 1927 and proudly, at the rear of each annual report across three pages displays its track record since inception along with stock dividends and splits made along the way. Hal Jackman joined the board in July 1966 and E-L Financial moved above a 20% shareholding in 2009 and began equity accounting EVT, gradually building to the current shareholding of 25%.

EVT - market capitalisation of $735 million on 31 December 2023 - is a strange conveyance with a roughly 50/50 (actually 47/53) of ungeared investment assets (as of 30 September 2023) between two "strategic" holdings in the ELF galaxy (ELF itself and Algoma) plus stockholding of Bank of Nova Scotia ( BNS ) (BNS.TO) arising from the merger of three trust companies controlled by the Jackmans and sold to BNS in 1997 for $1.25 billion and a portfolio of global stocks managed by Neuberger Berman.

The Neuberger stock portfolio is heavily diversified with 213 holdings (6 Canada, 103 USA, 28 Europe, 39 Emerging markets, 17 Japan, 12 UK, and 7 Australian resources stocks). EVT has also had an equity retirement strategy over recent years in keeping with that of ELF and UNC, with disappointing results, having only acquired 3.3% of the shares outstanding in March 2020 despite five completed initiatives:

| date |

| nature |

| concluded |

| shares |

| Av. price |

| Spend () |

| March 2020 |

| NCIB (buyback) |

| March 2021 |

| 27,600 |

| $86.94 |

| 2.4 |

| March 2021 |

| NCIB (buyback) |

| March 2022 |

| 2,200 |

| $118.78 |

| 0.3 |

| March 2022 |

| NCIB (buyback) |

| March 2023 |

| 17,900 |

| $119.46 |

| 2.1 |

| Aug 2022 |

| SIB (tender) |

| Sept 2022 |

| 113,007 |

| $140 |

| 14.4 |

| March 2023 |

| NCIB (buyback) |

| March 2024 |

| <273,231 |

| n/a |

| n/a |

| Nov 2023 |

| SIB (tender) |

| Dec 2023 |

| 36,231 |

| $138 |

| 5.0 |

| TOTAL |

| 186,938 |

| $129.45 |

| 24.2 |

The reason for the "disappointment' is twofold:

- the same taxation issues that beset SIBs in Canada - the latest SIB had a deemed dividend of $136/share which meant for any overseas holder, the effective price received would only be $117.60 after deduction of withholding tax of 15% on all but $2 of the consideration; and

- the share register is extraordinarily tight with Hal Jackman being associated with 4,670,029 shares[25] or 86% of the outstanding stock.

We can "slice and ice" EVT in various ways, but, assuming a 6% gain in the global portfolio since 30 September 2023, the 31 December 2023 NAV of just above $202 can be dissected as follows:

| Holding |

| # of shares |

| Price/comment |

| C$000s value |

| Algoma Central |

| 2.843 |

| $14.95 |

| 42,509 |

| Bank of Nova Scotia |

| 0.900 |

| $64.50 |

| 58,019 |

| Global portfolio |

| Including Canadian "passive" |

| 591,194 |

| Other net assets |

| 16,739 |

| Liabilities (tax) |

| Will have increased but low rate |

| (77,815) |

| Net assets excluding E-L Financial |

| 630,646 |

| PER EVT SHARE |

| 5,425,197 |

| $116.24 |

At EVT's share price of $135.50, at the end of December (market capitalisation $735million) investors were effectively paying $104.5million, before imputing any discounts into the ex-ELF portfolio, for an equivalent of ~477,582 ELF shares, an effective entry under $219/share.

ELF trades at around a 33% discount to disclose NAV. Adding in a more appropriate valuation of ELF of $1979/share would make EVT worth $300/share, for a discount of 55% before any tax adjustments .

The table above shows why we didn't adjust for the 11% EVT shareholding in ELF in calculating our NAVs since it would add value to ELF that's not realistically available, as we explain below. (ELF E72DT has a small holding in EVT not only because of the discount and sheer rarity value but also because of its potential role in the "end game".)

The final thesis - what might be the end game?

The end game might reasonably be construed to "own the last ELF or EVT share not owned by a Jackman". That's not as trite as it sounds.

The third-generation Jackman - Duncan - is now the Chair of ELF. The free float of ELF is gradually dwindling with Hal Jackman - now aged 91 and quietly leaving the board at the 2023 AGM - being "related" to 2,945,765 shares[26], either directly through a trust structure established in 1969 with his father or other companies in which he has an interest. The majority of these shares are held in the two old closed-end funds (Dominion and Anglo Investment Corp. and Canadian & Foreign Securities) together with Ecando Investments and Dondale Investments. However, 11.2% of ELF is held in the publicly listed Economic Investment Trust.

That leaves only 515,959 shares or 14.9% of ELF in 'independent" hands or $550 million worth of shares - but arguably over $1 billion of value.

In our view, the key to any end game is that it would be most unlikely to see a takeover offer by one group company for another . Whilst there would appear immutable logic for ELF to bid for EVT, the shareholders of EVT would not want their tax position to be disturbed[27] and such a bid would likely fall foul of Canada's tax-free share rollover legislation[28], since the two parties would not be dealing at arms length given the 85% and 86% "influence" held by Hal Jackman prior to such a potential transaction.

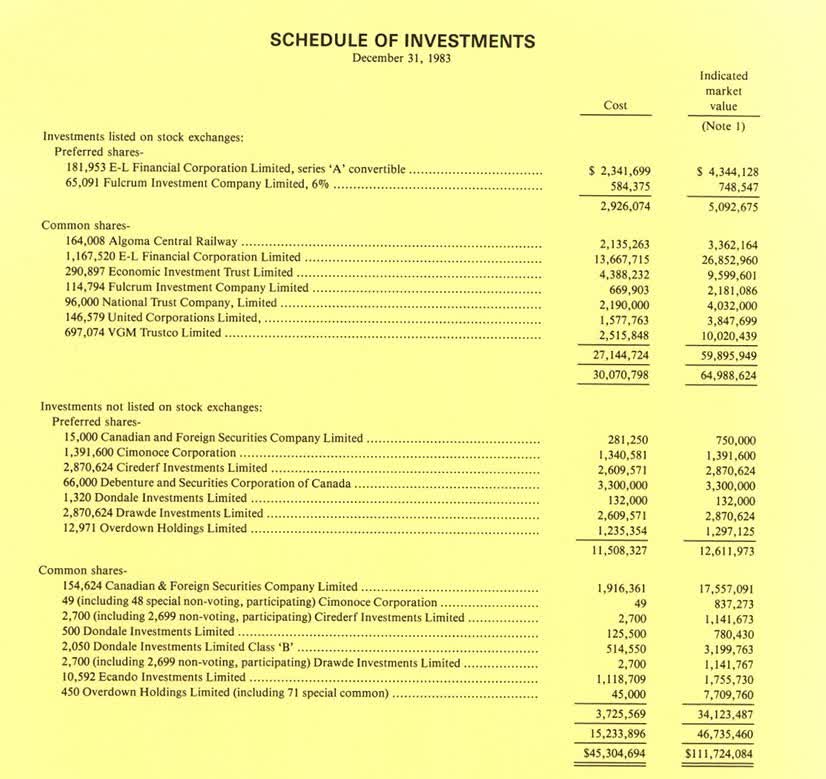

The degree of stability that the family would not wish to be disturbed can be seen in the snapshot below, from the 1983 Dominion and Anglo Investment Corp annual report, the latest that I can source, being the last year of the D&A preference shares being quoted on TSX:

{kind=link}

The shareholding list shows the investments in the trust companies later sold to BNS in 1997 and only 110,000 less shares in ELF than the entity currently holds. The holding of EVT has built considerably. It's a classic list of all of the known Jackman companies - probably why they aren't keen for updated versions to be on public display.

So the end game, should the Jackman's wish to privatise the bulk of the ELF group, realistically has to be equity retirement on an ongoing basis with a final "swoop".

Whilst the substantial issuer bids (tenders) have amassed ~100,000 ELF shares on their three occasions, there are potential tax issues for acceptors, which are chronic for overseas holders. In the latest SIB, amounts above around $45 become taxable as dividends, with significant withholding tax deductible. The best way forward for most investors would be a more aggressive on-market buyback and an agreed on-market offer by the company.

Based on recent experience, if the SIBs were done annually, it might only be 3-4 years before an infinitesimal number of shares remained outstanding, not related to the Jackmans, which could be mopped up with an NCIB, which is done as a maximum of 5% of outstanding shares.

Hence, we believe that with a low free float and enormous discounts to NAV, the opportunity cost of waiting in ELF is very modest.

Why would the Jackmans even want to privatise the group? There is significant trapped value in the form of hefty discounts to the value of liquid, globally traded securities that could be sold extremely quickly, which would accrue in some manner to the family, not necessarily at great expense to external shareholders. There are obvious administrative savings from taking ELF and EVT private, though Empire would continue to lodge public accounts. Removing EVT and ELF from public markets would enhance the privacy the family appears to crave[29]. This is another family-controlled public company that NEVER does presentations to shareholders, albeit the quarterly disclosure is exemplary.

In many ways, ELF is the archetypal closely held family-controlled entity: if you invest, you really DO have to go along with the family, at their pace. The good news is that from 2020 onwards, the equity retirement strategy of a group who have been parsimonious with equity issuance in the first place is stepping up the pace - just a little.

Pershing Square Holdings: Staring into the abyss was no bad thing.

Pershing Square Capital Management ((PSCM)), the investment management company established by William A. Ackman in 2003, has always had a significant profile, arising from its methodology and the highly confident nature of its founder. In the nine years between 2004-2012, PSCM compiled a net return of 20.4% per annum. Believing - quite rightly - that the concentrated style of investment undertaken by the firm would benefit from permanent, rather than semi-openended capital, Pershing Square Holdings ((PSH)) was launched at the end of 2012 and IPO'd in October 2014 at a price of $25 per share.

PSH is especially interesting having compiled a strong stretch of performance since staring into the abyss in 2016-17, but still trading at above a 30% discount to NAV, despite a strong management shareholding, consistent share buy-back program, and detailed presentations.

E72DT has a small shareholding in PSH in the belief that the discount can be further narrowed and NAV grow as a result of catch-ups in two of PSH's "lagging" investments, potential for the vehicle to be "onshored", as well as the over-riding motivation of management company profits and personal stock holdings. We acknowledge some of the easy money has been made but believe the next 2-3 years may provide a changed structure which will serve to close up the discount to NAV as well as growing asset backing.

As has been the case with many managers who have not previously run closed-end, publicly listed vehicles, the additional public and regulatory attention seemed to play with Ackman's psyche. From 2015-2018, PSH racked up four successive down years losing a cumulative 34.4% of NAV, against an S&P500 index return (not benchmark) of +32% over the same period.

So what happened? In many ways, Ackman hadn't lost his expertise but had started to believe his own publicity and became extraordinarily distracted from the core business. In December 2012, at the Sohn Conference Foundation, Ackman presented for three hours on the multi-level sales business Herbalife (HLF), where Pershing Square had initiated a significant short position. This was followed by an unsavoury, unscheduled live debate on CNBC[30] between Ackman and Carl Icahn, calling in and disclosing a long position.

Ackman also willingly participated in a documentary "Betting on Zero"[31] effectively documenting evidence against HLF. Over time, whilst Ackman may have been fundamentally correct about some aspects of HLF, Pershing Square misjudged HLF's willingness to repurchase its own shares with debt - funded by a strong cash flow (at the time) - together with the fact that other hedge funds smelled blood with Ackman caught in a short squeeze as the share capital contracted and free float diminished aided by Icahn and others.

The beginning of the end of the HLF short trade is plain to see in PSH Q3 2017 quarterly report[32] and the five-year escapade, which was imported into PSH, finally concludes at the end of February 2018.

In 2015, the all-consuming significant investment in Valeant Pharmaceutical [33] was made; Ackman's (and CEO Mike Pearson) attempts to fight back against the claims of Valeant acquiring other companies and therapeutics to then cease the R&D spend and ratchet up prices of lesser-known drugs were increasingly discredited.

The final nail in the Valeant coffin was the agreed revelation[34] that Valeant had engaged in improper revenue recognition via a subsidised mail-order pharmacy, Philidor. For an investment professional known for enormously detailed presentations on investee companies[35], this was embarrassing indeed. Even worse, the whole messy saga was laid out in a Netflix documentary, "Drug Short"[36] where short-sellers who successfully bet against Valeant illustrated the type of skills expected of a credentialled player (and insider) such as Ackman, making him appear especially foolish and captured by management. Ackman exited Valeant with a $3 billion loss in March 2017.

The combination of poor returns and adverse publicity took its toll on PSCM. In October 2014, PSCM held assets under management of US$18 billion of which US$6.3bn (~35%) was PSH[37]; by the end of 2017, firm assets were down to US$9.3billion and PSH $4.24bn (~46%).[38]

In January 2018, Ackman took decisive action in an attempt to prevent the whole show from falling into the abyss, with significant cost reductions and a refocus of his own role to concentrate on research and ideas. This was swiftly followed in March 2018 by a $300 million tender (9.5% of shares being 22.3 million at a price of $13.47/share) to buy back PSH shares after an attempt by Ackman personally to do so was rebuffed by regulators. However, shareholders voted to remove the 4.99% shareholder restriction cap on PSH in Q1 2018, and Ackman plus other members of the investment management team embarked on a significant buying spree. Between May & October 2018, Ackman acquired 23.7m shares at an average price of $15.01 to bring his holding to 39.9m shares or 18%; the entire team held 20% of PSH stock.

As with other (a carefully chosen adjective because there are not many) fund management turnarounds, the upturn did not commence immediately with PSH returning -0.7% in 2018 largely as a result of poor equity conditions. However, the realignment of management objectives with those of the PSH entity has been significantly rewarded in the past five years with NAV/share climbing from $17.30 at the end of 2018 to the end of 2023 figure of $65.04.[39]

However, in three of the five years, performance has been aided by well-structured macroeconomic bets, notably:

- 36.6% addition from credit default swaps being triggered due to COVID in CY2020;

- 7.7% accretion from interest rate swaptions in CY2021;

- 14.3% accretion from interest rate swaptions in CY2022; and

- Likely significant gains from interest rate positions in CY2023.

Hence, only the stunning 58.1% return in CY2019 was fully comprised of the outturn from stock picking.

The current portfolio is dominated by only eight positions (Alphabet is held in both Class "A" and Class "C") forms together with the two small positions in Fannie Mae ( FNMA ) and Freddie Mac ( FMCC ); Universal Music Group ( UMGNF ) (UMG.AS) is held directly and as part of a special purpose vehicle and is the largest component of the ~$14billion portfolio valued at ~$3billion.

PSH only publishes the exact portfolio twice per annum and there are significant derivative positions on occasion which can add to or detract from performance. We follow the portfolio from PSCM's 13-F filings with the SEC given that PSH accounts for some 87% of the domestic US holdings. There will be an update to shareholders on 8 February 2024 and the 2023 Annual Report will be available at the end of March 2024.

Our best estimates[40] of the NAV of $12.06 billion on 31 December 2023, using some reverse engineering, are as follows:

| Value () |

| Performance 2023 |

|

|

| Alphabet (x2) |

| 1,679 |

| +58.3% |

| Cash, receivables, other |

| 1,000 |

| CP Kansas City |

| 1,038 |

| +6.0% |

| Chipotle |

| 1,897 |

| +64.8% |

| Trade liabilities |

| (203) |

| Hilton Hotels |

| 1,632 |

| +44.1% |

| Deferred tax liability ((HHH)) |

| (85) |

| Howard Hughes Corp |

| 1,403 |

| +11.9% |

| Performance fee |

| (255) |

| Lowes |

| 1,368 |

| +11.7% |

| Bonds at par |

| (2,609) |

| Restaurant Brands |

| 1,587 |

| +20.8% |

| NET OTHER |

| (2,152) |

| UMG (inc SPV attribution) |

| 3,298 |

| +18.6% |

| Other |

| 302 |

| NET ASSETS |

| 12,062 |

| TOTAL PORTFOLIO |

| 14,213 |

| Per share |

| $65.04 |

After a lengthy period underwater - and giving shareholders a little of a free ride - PSH's NAV is back over its prior high water mark ((HWM)) on 31 December 2023 with NAV of $65.04 against a HWM of $56.23, thereby triggering the 16% performance fee in addition to the standard 1.5% ongoing fees.

But, as the above chart clearly shows, improved NAV performance does NOT translate into a narrowing discount to NAV of any consequence. Bluntly, this is the big issue for Ackman to solve - because there is over $775million[41] in it: just for him.

Where to from here? Why do we still Hold?

It is clear to most, and there have been several clues given by Ackman himself, that Ackman/PSCM are wedded to the "permanent capital" structure. PSH's assets under management of $14.7billion leave only $2.1billion with other investors in the "core" strategy, and the residue of the firm's managed assets (~$1.5billion) are in special purpose vehicles such as PS VII Master which holds ~76million UMG shares and of which PSH itself owns 28%[42]. So PSCM has nearly fully converted to this format.

The logical next step is to turn PSH into an operating company - which would fulfill Ackman's wishes of a "Berkshire" type structure[43] - but would require the "onshoring" of PSH. That would only be possible by PSH becoming an operating company[44] with (say) 40% of the assets being public investments. This is not going to happen overnight, but moves towards it may be seen in the further increase in shareholding of Howard Hughes Holdings to 37.6% of the property company[45]. Even a full acquisition of HHH would likely not satisfy the onshoring idea since, on a pro-forma basis, securities would still be ~54% of total assets of ~$21 billion.

The calculation above assumes a sale of Chipotle, which we view as being a possibility given the forward P/E of 41x; Ackman has shown a willingness to divest retail food franchises of strength in the past through the sale of Starbucks in January 2020. In the meantime, PSH gives us another discount exposure - in tandem with Bolloré and Vivendi - to UMG.

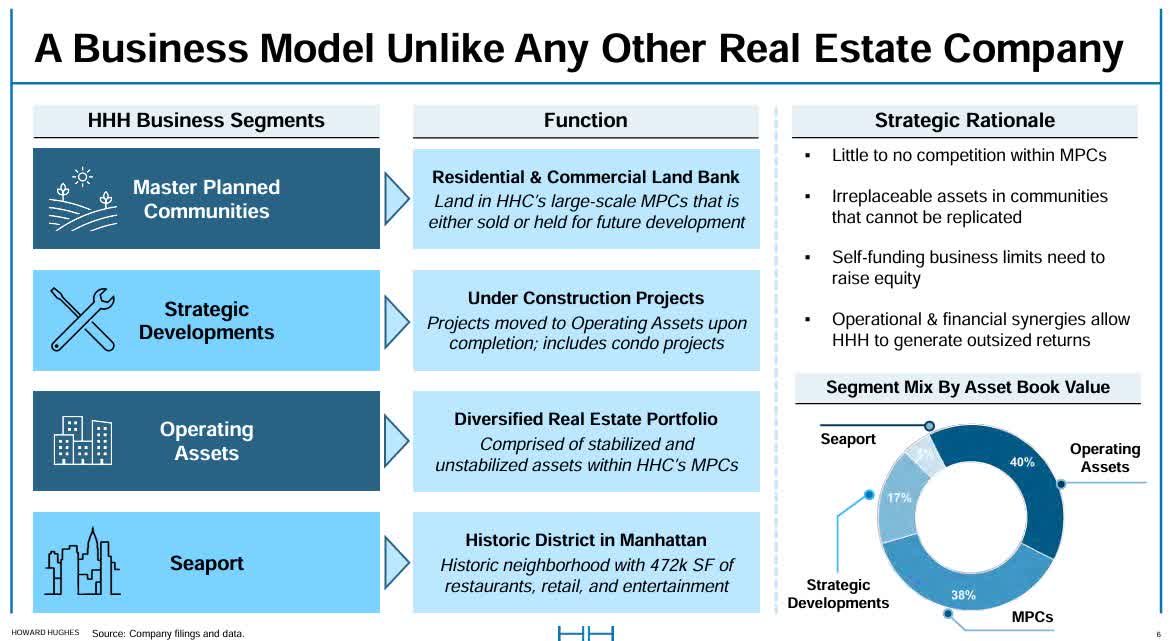

So, is an investment in Howard Hughes Holdings desirable with its equity market capitalisation of $4.3 billion and enterprise value estimated at $9 billion (subject to working capital) desirable?

{kind=link}

Arguably, the investor issue with HHH is the complexity of the company - which precludes a detailed analysis in this report - with its mix of completed developments, multiple projects under construction, and an enormous landbank in five desirable locations from a demographic and tax standpoint: Houston, Phoenix, Las Vegas, Maryland, and Hawaii. Only four sell-side analysts seem to cover the company. HHH has been heavily tarnished by the Seaport development in downtown Manhattan, which obviously suffered during COVID, but in the last quarter was the subject of a $700m impairment charge. That - of course - was aligning an appropriate valuation ahead of a hoped-for spin-off in 2024, to leave the main company in a clean position.

E72DT has a holding in another "condominium" rental/industrial/commercial development company centred in Washington DC and its environs: FRP Holdings ( FRPH ), which is a family-controlled entity but also has the benefit of a 90% margin aggregates royalty. The shares were moribund for some time but saw greater interest once the residential developments were stabilised - in FRPH's case with significant rentals. We suspect HHH is in a similar position when investors can identify hard asset value through cash on completed sales or place a firm yield on rentals.

HHH does fit PSH's desire for attractive long-term returning assets, of which UMG is arguably its best. PSH is a modest 1.7% position in the E72DT portfolio - sadly given its recent strong performance - but we continue to expect positive evolutions - over time. Our main concern is ensuring the largest shareholder and manager keeps his eye on the ball amidst other distractions. The past five years have proven his intellect and performance capability when disciplined.

For further information:

Andrew Brown

Executive Chair

0418 215 255

Copyright and Disclaimer

©Other than material being the property of its respective owners, this presentation is copyright 2023 East 72 Management Pty Ltd. All Rights Reserved. You may not reproduce parts of this work without permission, which can be sought by email, but you are free to distribute the work in its entirety with full attribution.

This communication has been prepared by Andrew Brown and East 72 Management Pty Limited ( E72M ) (ACN 663980541); E72M is Corporate Authorised Representative 001300340 of Weserry Operations Pty Limited (AFSL 302802) of which Andrew Brown is a Responsible Manager.

While E72M believes the information contained in this communication is based on reliable information, no warranty is given as to its accuracy, and persons relying on this information do so at their own risk. E72M and its related companies, their officers, employees, representatives, and agents expressly advise that they shall not be liable in any way whatsoever for loss or damage, whether direct, indirect, consequential, or otherwise arising out of or in connection with the contents of an/or any omissions from this report except where liability is made non-excludable by legislation.

Any projections contained in this communication are estimates only. Such projections are subject to market influences and contingent upon matters outside the control of E72M and therefore may not be realised in the future.

This update is for general information purposes; it does not purport to provide recommendations or advice or opinions in relation to specific investments or securities. It has been prepared without taking account of any person's objectives, financial situation or needs and because of that, any person should take relevant advice before acting on the commentary. The update is being supplied for information purposes only and not for any other purpose. The update and information contained in it do not constitute a prospectus and do not form part of any offer of, or invitation to apply for securities in any jurisdiction.

The information contained in this update is current as of 31 December 2023 or such other dates which are stipulated herein. All statements are based on E72's best information as of 31 December 2023. This presentation may include officers and reflect their current views with respect to future events. These views are subject to various risks, uncertainties and assumptions which may or may not eventuate. E72M makes no representation nor gives any assurance that these statements will prove to be accurate as future circumstances or events may differ from those which have been anticipated by the Company.

[1] We did gain an advantage from ownership of EXOR, STLA's largest shareholder which together with the 58% gain in Ferrari ( RACE ) shares, saw EXOR rise 32% during 2023 yet still retain its ~40% discount to NAV.

[2] TFF Group is a French-based vertically integrated cask manufacturing and cooperage business which is obviously required to allow for forestry growth; shares in TFF Group are owned in E72DT portfolio.

[3] "The NBC Family Advantage" which also tracks the performance of (currently 43) large-cap family-controlled companies on the Toronto Stock Exchange

[4] All $ in this piece are C$

[5] There was an unlisted market in Empire Life shares predating its float

[6] We have EXCLUDED warrants issued which would magnify returns significantly

[7] Calculations by East 72 Management Pty Limited; E&OE

[8] Dynasty Trust also owns securities in Economic Investment Trust (EVT.TO)

[9] A well-known story is of Hal Jackman parking his very old Lincoln car at the Argus building of Conrad Black. The car was thought to be derelict and so was towed away leaving the mul-millionaire stranded and having to borrow a subway token to return home (various sources notably Ottawa Citizen 20 Nov 1991)

[10] In our view, one of the best ever Berkshire Hathaway Annual Report Chair's letters is from 1982 where there is a full section on "Issuance of Equity" "Our share issuances follow a simple basic rule: we will not issue shares unless we receive as much intrinsic business value as we give."

[11] National Post 10 November 2001 (page 106); Fell's son Anthony ended up as Chair of Dominion Securities (now RBC Dominion Securities)

[12] D&A stock was the highest priced in the Canadian market at over $ 500 per share in 1960, providing impetus for a 50-1 stock split; the common shares were delisted in 1971 and the preferred stock in October 1982.

[13] Hal was Lieutenant Governor of Ontario for 5 years to January 1997. He also separately built National Trustco which was sold to Bank of Nova Scotia in 1997 for $1.25billion

[14] Dominion and Anglo Investment Corp., Debenture and Securies Corp of Canada, and Canadian and Foreign Securities Limited.

[15] In Ontario; elsewhere was 30% limit

[16] On 31 December 1971, ELF had 2,733,834 common shares + 597,171 Series "A" convertible preference (1-1 to common) + 531,411 warrants exercisable by 22 December 1978 at $12 (most were) = diluted capital of 3,862,416 shares. ELF currently has ~3,461,722 shares on issue.

[17] Assuming all other variables stay the same - highly unlikely

[18] Prudential PLC "IFRS 17 Briefing" 20 July 2023

[19] Policyadvisor.com

[20] Manulife Financial Corporation Q3 2022 Report to Shareholders page 10

[21] Sun Life Financial Inc Q3 2023 Report to Shareholders page 19

[22] Empire Life Q3 2023 financial report note 6.9 page 41

[23] $112.56 share price on 27/12/23 versus $180.13 NAV (Source: UCL)

[24] UNC-issued capital is now ~11,256,465 shares

[25] 2022 Management Information Circular 22 February 2023 page 1

[26] Annual Information Circular issued 9 March 2023 page 44

[27] See the 1983 portfolio of Dominion and Anglo Investment Corp overleaf

[28] (Canada) Income Tax Act subsection 85.1(3)

[29] For example, an order garnered from the Ontario Securities Commission on 12 March 2004 that Dominion and Anglo is NOT a reporting corporation.

[30] 25 January 2013 (https: //www.youtube.com/watch?v=6QWZbxeJd6g )

[31] "Betting on Zero" released on 14 April 2016 (Zipper Brothers Films, Biltmore Films)

[32] Q3 2017

[33] Now Bausch Health Companies (NYSE: BHC)

[34] SEC Press Release 31 July 2020 "Pharmaceutical Company and former Executives Charged with misleading financial disclosures"

[35] Examples: 50 slides on Howard Hughes Corp (Ira Sohn Conference - 8 May 2017); 2'44" 128 slide presentation regarding UMG ( https://www.youtube.com/watch?v=BpeHWiRuu2k ) ; 43 slides on Starbucks ("Doppio" 9 October 2018)

[36] Episode 3, S1 of the "Dirty Money" series on Nelix (2018)

[37] PSH Monthly Performance Report October 2014

[38] PSH Monthly Performance Report December 2017

[39] PSH Monthly Performance Report December 2023

[40] We could be wildly wrong here.

[41] 21% of 185 million shares x (NAV - price)

[42] PSH owns ~105.3million UMG shares directly

[43] Interview with Fifth Avenue Synagogue May 2021 ( William A. Ackman, CEO and Portfolio Manager of Pershing Square Capital Management L.P. ) containing, for example, "If you follow him (Buffett) from the mid-1950s to the late 1960s he managed what is best described as an activist hedge fund and then he gave his investors the option in effect... he basically said look I'm going to return all the assets but if you'd like you can go along with me in a company called Berkshire Hathaway. Sort of merged his hedge fund into what became this… what was a textile company at the time and became a conglomerate that he's managed over time. The benefit… what was interesting is he gave up the right to receive a share of the profits in exchange for permanent capital which tells you how he valued it, or how highly he valued it. We started about 12 years in at Pershing Square. We launched a public entity, structured as a European closed-end fund with a business plan to get to the same place ultimately as Buffett."

[44] Hedge funds cannot be listed on US public exchanges

[45] 18,851,725 shares held of issued capital of 50,078,903

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

East 72 Dynasty Trust Q4 2023 Quarterly Report