ECAT - ECAT: Attractive Discount And Activist Position Grows

2023-11-26 03:31:59 ET

Summary

- BlackRock ESG Capital Allocation Term Trust is a target of the activist group Saba Capital Management.

- Even if Saba is unsuccessful, the fund is still worth considering with the large discount in a highly diversified portfolio.

- In the long run, investors should receive NAV back anyway as ECAT is a term fund providing an attractive monthly distribution to investors.

Written by Nick Ackerman, co-produced by Stanford Chemist.

The last time we covered BlackRock ESG Capital Allocation Term Trust ( ECAT ) was over a year ago . However, we had shorter updates on a couple of occasions as I've been building up a position in this fund in my own portfolio.

The biggest draw, besides the attractive discount that this fund continues to trade at, is that it is a target of Saba Capital Management. This is an activist group, and they've continued to build up a position in this fund. More recently, they have crossed 19% ownership in the fund with the purchase of over 2 million shares through November . This isn't necessarily a small fund either, with assets of over $1.75 billion; it is quite large for a closed-end fund.

One of the ways that Boaz Weinstein is looking to push ECAT is to merge into one of the BlackRock ESG-focused mutual funds. Of course, that's because traditional mutual funds can be purchased and, more specifically, redeemed at NAV. Thus, the discount would be eliminated, and that would provide a huge bump to investors.

At the end of the day, I'm comfortable with whatever outcome. Currently, buying shares at a large discount is enticing for essentially a 70/30 portfolio. Roughly 70% is invested in equities currently, and another 30% in fixed-income. The fund doesn't use leverage in the form of borrowings, so we don't have to worry about that.

We recently covered BlackRock Capital Allocation Term Trust ( BCAT ), as Saba is starting to build up a position there as well. However, they started with ECAT and have been more aggressive with ECAT.

The Basics

- 1-Year Z-score: 1.11

- Discount: -11.38%

- Distribution Yield: 9.93%

- Expense Ratio: 1.29%

- Leverage: N/A

- Managed Assets: $1.748 billion

- Structure: Term (anticipated liquidation date September 27th, 2033)

ECAT has a fairly basic investment objective ; "to provide total return and income through a combination of current income, current gains and long-term capital appreciation." This is essentially copy-paste from most of their other funds.

To achieve this, the fund will "invest in a portfolio of equity and debt securities. Generally, The Trust's portfolio will include both equity and debt securities. At any given time, however, the Trust may emphasize either debt securities or equity securities. The Trust will invest at least 80% of its total assets in securities that, in the Advisor's assessment, meet the environmental, social and governance criteria as described in the Trust's Prospectus and shareholder reports."

Performance And Discount

Since our last update, ECAT put up a solid total return performance. A meaningful portion of this was from the fund's discount narrowing from the 18%+ level it had been to now below a 12% discount. Despite this move already, I would still be comfortable with giving the fund a 'Buy' rating today.

ECAT Performance Since Prior Update (Seeking Alpha)

ECAT and BCAT are positioned differently in terms of their split between equity and fixed income. BCAT also has utilized leverage in the past and has the ability to leverage up again through borrowings, though at this time, it isn't. ECAT and BCAT performed quite similarly on both a total share price and NAV return basis for a period of time. Unfortunately, it's only a short comparison period because ECAT isn't that old, being launched toward the end of 2021.

However, ECAT started to pull away around the time that the market started to bottom in late 2022. Additionally, I've included the Thornburg Income Builder Opportunities Trust ( TBLD ) for an outside comparison. TBLD also isn't leveraged but takes the approach of being a multi-asset fund that can invest anywhere and anyhow at any time.

Ycharts

The discount for all three of these funds is quite deep. However, making any of them a fairly interesting choice. That said, considering ECAT is getting the most attention from Saba, it could be argued that ECAT is the best choice here as it is the most likely to have a positive catalyst.

Ycharts

The 1-year z-score for ECAT is also positive. So that indicates it's trading at a narrower discount relative to where it had been the last year. That said, between the activist pressure and coming off a hard period for the fund, it isn't as negative for the fund as it would traditionally indicate, in my opinion.

Attractive Distribution

Based on the current share price, the fund's distribution yield works out to 9.93%. Given the discount, the fund's NAV rate is lower at a more modest 8.8%.

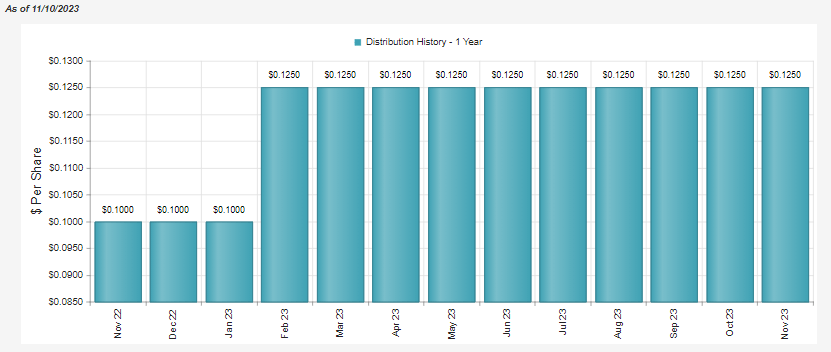

Similar to BCAT, ECAT received a distribution boost early this year, and I wouldn't be shocked if it was a discussion in the boardroom to try to get activists off their backs.

ECAT Distribution History (CEFConnect)

{kind=link}

The reason was that it wasn't necessarily really warranted to see a distribution boost for either fund. They both came out of 2022, which was a rough year for all investments, equities and fixed-income. It didn't really matter where you looked. Basically, that is representative of these funds because they invest in everything and anything.

This year, results have been better, with the last NAV at $17.05, and they started out at $16.70. Meaning that they would technically be considered covering their distribution to investors this year.

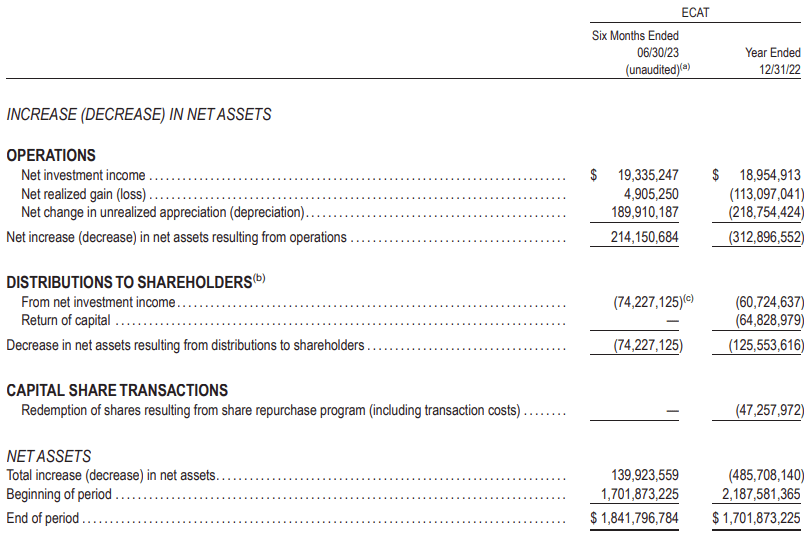

This came primarily from unrealized gains in the first half of the year . They had realized gains, but that wasn't from their underlying investments. Instead, realized gains came primarily from foreign currency transactions and foreign currency exchange contracts that offset the losses that they realized from their portfolio. Additionally, futures contracts and swaps also saw realized gains.

ECAT Realized/Unrealized Gains/Losses (BlackRock (highlights from author))

The fund also has put up some respectable net investment income. NII is on track to outpace last year's NII by a meaningful margin as well, so that can help cover the distribution from a more steady and reliable source.

ECAT Semi-Annual Report (BlackRock)

{kind=link}

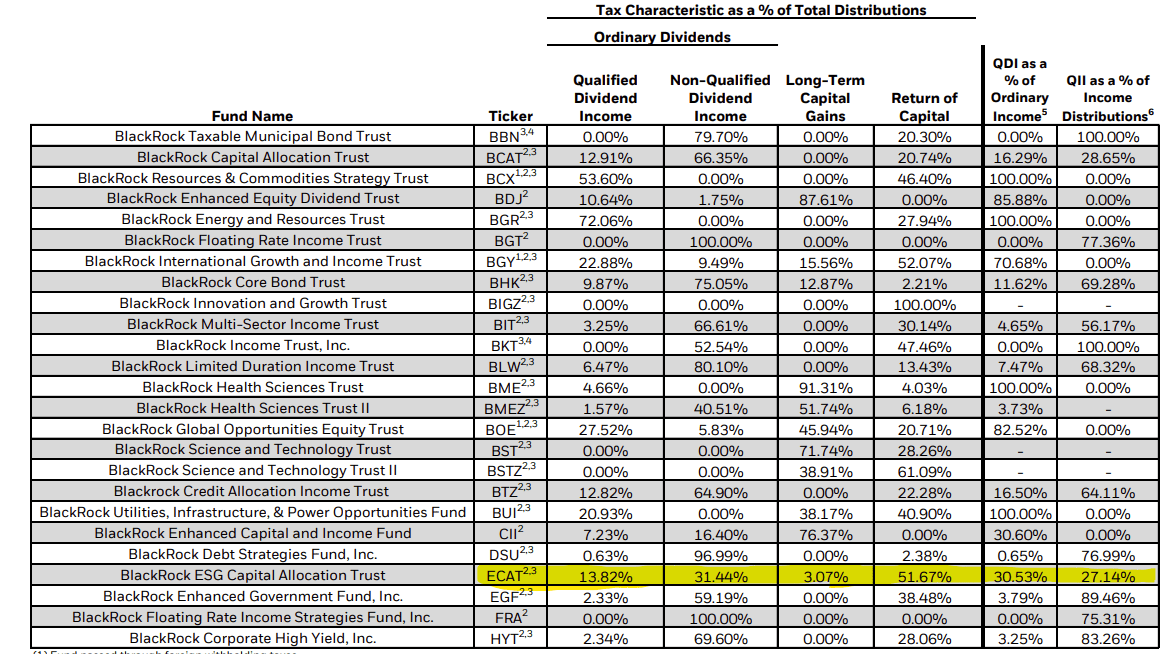

For tax purposes, in 2022, ECAT saw a little bit of everything. There was qualified dividend income, non-qualified dividend income, long-term capital gains and return of capital. The ROC, in this case, would be considered destructive for 2022 as the NAV slumped. Going forward, the distribution is likely going to continue to include ROC even if the fund performs well because of the capital loss carryforwards.

BlackRock Tax Character of Distributions (BlackRock (highlights from author))

{kind=link}

However, if the fund makes it to the long run before being merged, it would be expected to see long-term capital gains as the main tax classification for the distribution. At the very least, that would be the ideal scenario, but if equities and fixed-income struggle as they did in 2022, then expect more ROC.

ECAT's Portfolio

The portfolio is currently titled toward mostly equities but is an otherwise fairly standard portfolio split that someone may set up in their own portfolio. Of course, ECAT is just one fund, and they've actually taken roughly 700 positions. So, they are likely holding more positions than any individual would, but it could essentially be a one-stop shop portfolio for an investor if they wanted.

ECAT Asset Allocation (BlackRock)

{kind=link}

Since our last update over a year ago, the split hasn't changed too drastically. The fund held a higher equity allocation at that time, too, but it came only to around 56%, where fixed-income was at ~30%. The difference at that time was the fund still had a material cash allocation of ~14%.

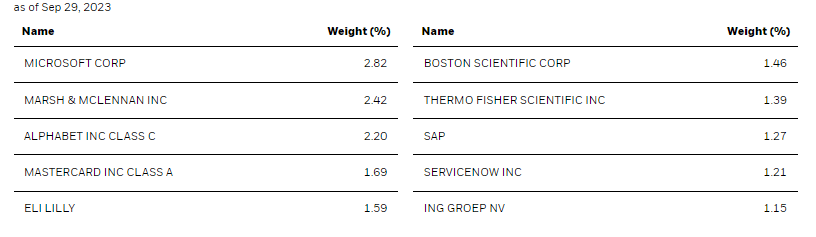

I know "ESG" is a hot topic where investors get quite passionate. Unfortunately, it's become more of a political topic than anything else. However, one can look at the top ten holdings and see that they aren't quite anything unique in terms of a tilt toward ESG. They hold just your standard traditional holdings, Microsoft ( MSFT ), Marsh & McLennan ( MMC ) Alphabet ( GOOG ) and Mastercard ( MA ), to name a few.

ECAT Top Ten Holdings (BlackRock)

{kind=link}

The fact is, this isn't a fund that is focused specifically on clean energy or anything ESG-specific. It is a multi-asset fund that invests in a very diversified portfolio. It's just more of what they don't invest in, and that is weapons, tobacco and coal. But they do have a position in Constellation Brands ( STZ ), so that vice gets a pass. Other pipeline companies, such as Enbridge ( ENB ), are also included as an oil and gas infrastructure position.

Tobacco and coal are dying industries anyway, so the absence of them isn't likely to be too detrimental to the health of one's portfolio. I even own Altria ( MO ), so I know how bad things are with cigarette shipments falling materially every quarter. They are shifting toward smoke-free products and other reduced-risk products, but so far, there isn't anything that seems like a sure bet. With coal, it is simply being replaced by natural gas or even by renewable/green energy sources. It isn't that these areas of the market can't be profitable, but as demand wanes, it just becomes more difficult to grow.

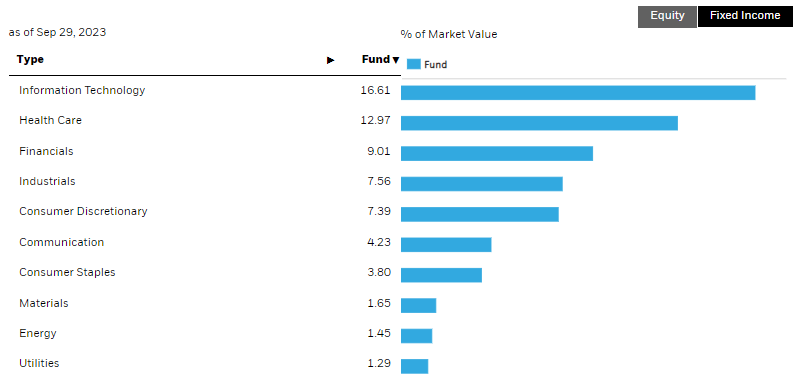

With that being said, their sector allocation in the equity sleeve has leaned toward the technology space.

ECAT Sector Allocation (BlackRock)

{kind=link}

The sector weighting hasn't seen a material shift as tech and healthcare were also the largest allocations last year.

In looking at the fixed-income sleeve, the top ten holdings here are quite diversified at allocations less than 1% primarily. After all, with over 700 positions, weightings are going to be fairly small. The exception to that is the UMBS 30 Year with a ~7% allocation. As an MBS, there are hundreds or thousands of loans in each of these securities, so if it was broken out, there would be even more positions for the fund, and the weightings of each would be quite small.

ECAT Top Ten Fixed-Income Holdings (BlackRock)

{kind=link}

Conclusion

ECAT is a target of Saba, but that isn't the only appealing feature of the fund. The fund is carrying a sizeable discount on a fairly standard portfolio, at least in their holdings. The derivatives they employ aren't generally going to be so widely utilized by most individual investors. So that being said, if nothing happens in terms of merging with a traditional mutual fund or ETF, a person likely isn't going to be too bad off with this pool of assets over the long run anyway. Additionally, since it is a term fund, it would be anticipated that NAV will be returned to investors in the future. Of course, at this point, that isn't too much of a consideration, with the term date not until 2033.

For further details see:

ECAT: Attractive Discount And Activist Position Grows