OXLCM - ECCC: Not A Compelling Value Proposition At Current Levels

2023-11-17 03:32:56 ET

Summary

- ECC is a closed-end investment company focused on CLO equity, seeking high current income and capital appreciation.

- ECCC represents a term preferred equity tranche with a maturity date of June 30, 2031, and an optional redemption from June 16, 2024.

- The CEF has an adequate asset coverage ratio for its liabilities, ratio which exceeds required provisions under the 1940 Act.

- Despite its robust coverage, ECCC is the longest tenor liability for the fund and does not provide an adequate yield when compared to similar securities with shorter tenors.

Thesis

Eagle Point Credit Company Inc. ( ECC ) is a closed-end management investment company focused on CLO equity. The CEF's primary investment objective is to generate high current income, with a secondary objective of generating capital appreciation.

The CEF invests primarily in CLO equity and mezz tranches, thus representing a very risk-on take on credit spreads and economic conditions. Furthermore the fund leverages up its exposure, with a current leverage ratio of 28%. For common equity holders ECC is a high risk / high reward proposal, which has done very well during the 2020/2021 zero rates environment:

Please note an interesting feature in the 5-year graph above. While the ECC total return for the past five years is 25%, the CEF's price is down -42%. This feature is due to the asset class held by the CEF, namely CLO equity.

CLO equity is an IRR based asset class, that has no set 'principal' amount. CLO equity does not return principal like a regular bond on a set date. If a CLO performs the equity is going to deliver a high amount to equity holders in the first few years of the life of the CLO. Therefore when CLO equity is quoted in the market it is done on an IRR basis (i.e. day 1 cash outlay versus the present value of estimated future cash flows).

Given the constant decay of the actual value of CLO equity via cash disbursements, CLO CEFs have a hard time to place traditional leverage via bank facilities or traditional preferred equity with no term.

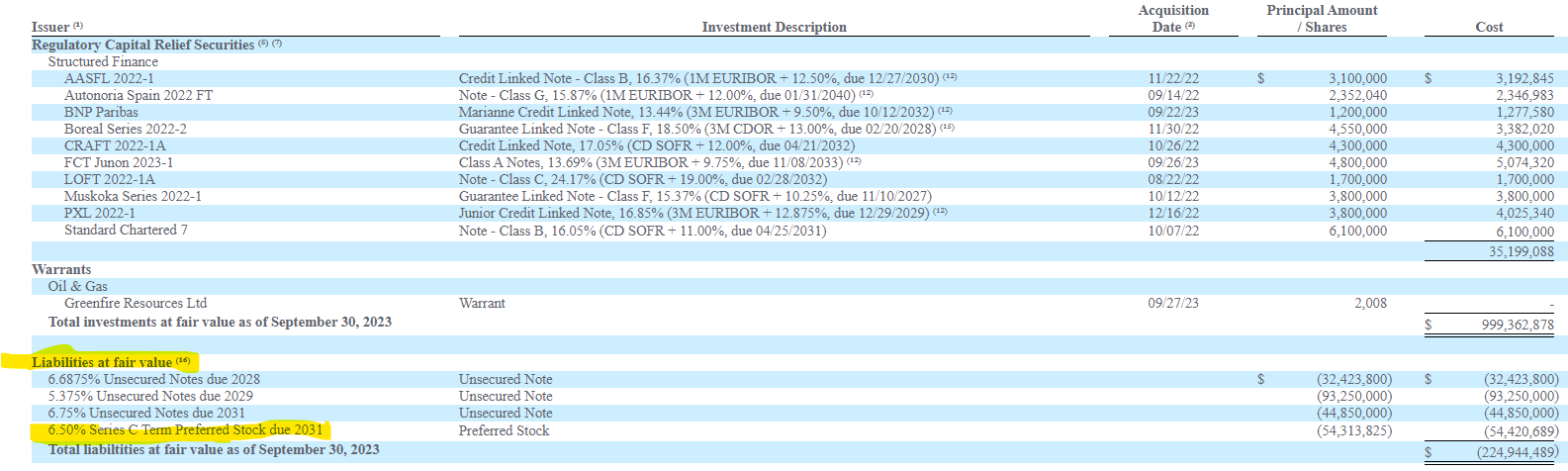

Just like in the case of Oxford Lane Capital Corporation (OXLC), we can see a term structure for all of ECC's liabilities:

{kind=link}

The fund contains a mix of unsecured notes and term preferred equity on the liability side.

In this article we are going to take a closer look at the ECC Series C Term Preferred Stock (ECCC), its features and analytics, and articulate why we do not believe ECCC is a compelling investment at this juncture.

Series C Term Preferred Equity

The CEF has placed a term preferred equity tranche is Series C:

The Company is required to redeem all outstanding shares of the Series C Term Preferred Stock on June 30, 2031, at a redemption price of $25 per share (the "Series C Liquidation Preference"), plus accrued but unpaid dividends, if any. At any time on or after June 16, 2024, the Company may, at its sole option, redeem the outstanding shares of the Series C Term Preferred Stock.

Source: Semi-Annual Report

As per the above, the CEF has a required maturity date of June 30, 2031 for the Series C, with an optional redemption date starting June 2024. The optional redemption purely allows the company to call the Series C if the funding markets are open for a lower cost option. With the current rates environment versus the time the Series C was placed, we place a very small probability around the series to be called until the maturity date in 2031. In effect we are looking at an 8 year term for this security.

The term structure allowed the CEF to place the security at an attractive day 1 yield, with perpetual preferred shares in this underlying asset class (CLO equity) being quasi impossible to place. However, the Series C maturity date is the further one out in the capital structure, with all the unsecured notes placed by the CEF having earlier maturity dates.

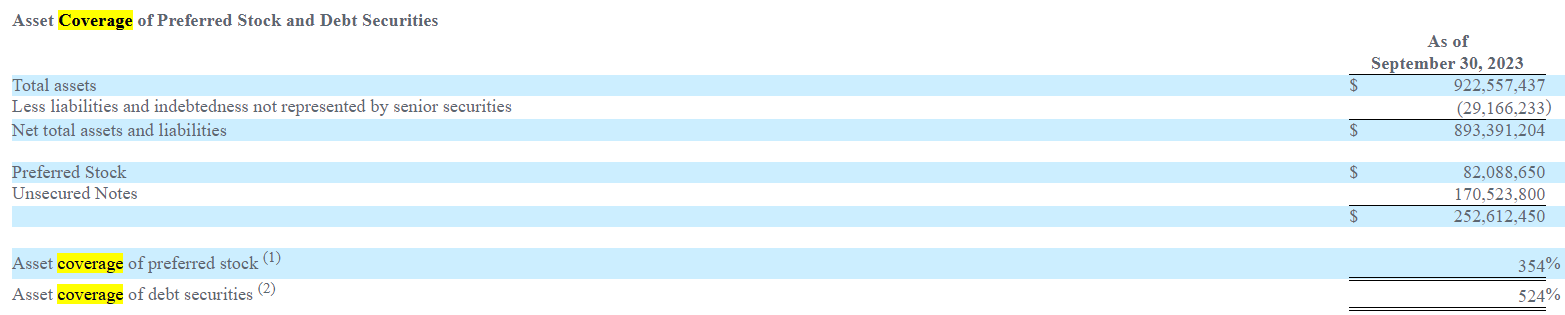

Asset Coverage

Given the underlying collateral, it is important for a potential investor to understand how the asset coverage shapes up for the liability structure, although generally speaking CEF preferred shareholders are usually well protected under the provisions of the 1940 Act:

With respect to senior securities that are stocks, such as the Preferred Stock, the Company is required to have asset coverage of at least 200%, as measured at the time of issuance of any such senior securities that are stocks and calculated as the ratio of the Company's total consolidated assets, less all liabilities and indebtedness not represented by senior securities, over the aggregate amount of the Company's outstanding senior securities representing indebtedness plus the aggregate liquidation preference of any outstanding shares of senior securities that are stocks.

Currently the CEF exhibits an asset coverage in excess of the 1940 Act requirements:

{kind=link}

An adequate asset coverage percentage simply translates into the fund having enough collateral to imply a robust return of principal coverage for the preferred shares. A retail investor can interpret this figure as an assurance for a 100% recovery in the principal invested.

Yield is Not compelling

While the coverage is adequate for ECCC, the preferred shares fail to offer a compelling yield given their tenor:

Yields (PreferredStockChannel)

The securities offer a mere 7.78% yield for an eight year tenor, or better put around 300 bps over treasuries. We would expect a higher term premium here, especially in light of the recently covered OXLCM, a preferred equity series from OXLC with a mid-2024 maturity date and a 6.8% yield. So for 1-year risk an investor gets a 6.8% yield with OXLC, but only 100 bps more for 8-year risk via ECCC. The spread differential is not compelling, especially in light of the potential gap-down in price for ECCC when another market risk-off event develops, given its long tenor.

With Fed Funds above 5%, there are a plethora of investment opportunities in the fixed income space, and placing term cash with credit spread risk for a long maturity date requires a larger spread in our opinion. An investor can just ladder in a series of OXLC preferred shares at this point, which offer a more compelling maturity adjusted yield.

Conclusion

ECCC is the Series C Term Preferred Equity tranche from the Eagle Point CEF. The preferred shares have a 2031 maturity date and a robust asset coverage ratio, despite being the longest tenor in the CEF's liability structure. The shares are attractive via their term structure, which is an unusual feature in the preferred equity space, but fail to offer investors an attractive yield when compared to market alternatives. The shares are not attractive in our opinion at this juncture, with a retail investor better served to obtain a 6.8% yield via OXLCM and only consider ECCC on a market-wide dislocation which would push credit spreads much wider.

For further details see:

ECCC: Not A Compelling Value Proposition At Current Levels