EDIT - Editas Medicine: Progress Pitfalls And Future Expectations

2023-07-23 08:29:06 ET

Summary

- The progress of EDIT-301 in Phase 1/2 RUBY and EdiTHAL studies is encouraging.

- I am increasingly turning more bearish on EDIT due to increased competition and a less attractive financial outlook.

- The focus now is on year-end catalysts and increased clarity from management team for '301 and recent changes to EDIT's balance sheet.

Isn’t it thrilling to see gene-editing evolve? Every day we see developments and breakthroughs, and companies like Editas Medicine (EDIT) are at the headlines of this niche. I first covered EDIT on February 23 rd , and honestly, my sentiment hasn’t changed all that much since then, but my short-term outlook for the company has only gotten more bearish.

In my previous article , I pointed out EDIT-101, one of the biggest candidates for the firm. It has exhibited some pretty promising results in ongoing clinical trials for treating Lever congenital amaurosis 10. But when considering short-term investments or holding cash with EDIT, I feel EDIT might not be the best fit. The company faces a unique set of risks compared to other early-stage gene editing companies.

The absence of approved products in its commercial portfolio and a prolonged revenue drought is undoubtedly concerning. But what really caught my attention a while back was the cessation of their collaboration with AbbVie ( ABBV ) and the decision to halt enrollment in the BRILLIANCE study for EDIT-101 (my fav program vs EDIT-301). I brought this up in my last piece, so this is not something I will be covering today, and this has already been baked into the stock price.

Since my last article, EDIT has posted more color during April and June this year, which will be the meat and potatoes of the article today.

I am Close to Moving EDIT to Sell from Hold

As it stands, I’m giving EDIT shares a hold rating, a perspective shaped by many elements. EDIT is currently reassessing its R&D portfolio and mulling over its next steps, following sidelining of its primary program in LCA10 back in November 2022. The early clinical validation demonstrated in LCA10 and SCF is encouraging, no doubt, but it doesn’t paint the whole picture. Before I can fully back EDIT’s outlook, I need a clearer understanding of its long-term potential and commercial viability. Right now, all the focus seems to be on EDIT-301 and not anything else.

For their lead EDIT-301 program, which is in SCD and TDT, this is the main thing to keep an eye on now. This space is a rapid river with the current changing swiftly, as new players are expected to step in any day now; the potential competitors would pose a big challenge to EDIT, making the path to market leadership like navigating a labyrinth. So, that’s something to chew on.

As of writing, Editas Medicine ((EDIT)) shares are priced at $8.61. But after recent April and Q1 2023 management calls and updates, I have adjusted some things in my model, adjusting for uncertainty, and have set a Price Tag of $9.00 for FY23. See below for my digging on management updates:

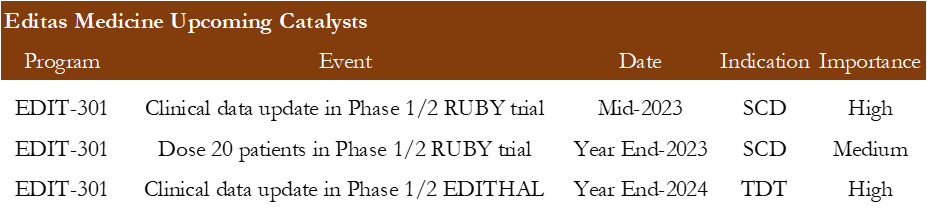

Just to keep you in the loop, here are some catalysts for Editas Medicine that you should keep on your radar:

Key Upcoming Catalysts (Company Reports)

{kind=link}

Q1 Review: Clear Differentiation and Regulatory Path Continue to Dominate

Looking at EDIT, priced at $9.67 as of June 9 th , ’23 (Q1 FY23), I found myself diving into another earnings call with Editas management following their recent update on the progression of EDIT-301 in the Phase ½ RUBY and EdiTHAL studies.

Following that call and presentation on June 9 th , I tried to get a hold of every detail about 301’s progress. I’ll be honest; the overall sense I got from the call was quite positive. The program seems to be advancing well, considering the pace of enrolment and the preliminary data that’s been coming in. The early data from the SCF and beta thal studies, in particular, suggested promising efficacy.

But I am not going to get ahead of myself here. The full scope of opportunities here is still a bit murky, largely due to the dynamics of competitors that are a few steps ahead in the development process. As the new kid on the block in the targeted ex vivo market, EDIT is going to need time (talking 3+ years) and some really compelling clinical evidence of differentiation to carve out a larger chunk of the market.

The management, for their part, has highlighted some potential differentiators for ‘301 (see the visual presentation here ), including parameters like hematology, quality of life, and organ damage. But, as I see it, I think we are still some ways away from having the kind of concrete evidence that would persuade physicians to pick ‘301 over other ex vivo options such as bluebird bio ( BLUE )’s Zeynteglo, Intellia Therapeutics ( NTLA )’s CRISPR/Cas9, and CRISPR Therapeutics ( CRSP )’s CTX001. For this reason, my sentiment on EDIT has turned more bearish. I don’t see compelling reasons to hold or buy the company right now in comparison to other opportunities, and I believe EDIT will continue to lag behind its peers and the broader market. So, as we await more updates on the clinical and regulatory fronts, I’d suggest investors consider selling some of their EDIT stakes or holding with a very long-term outlook.

But I will dive a bit deeper. The Phase ½ RUBY trial in SCD has enrolled 20 patients , most of them in the US. The plan is to have 20 patients dosed in this study by year-end. Meanwhile, the Phase ½ EdiTHAL trial in TDT has brought 5 patients to date, with 22 sites activated for RUBY and 7 for EdiTHAL.

As for EDIT’s FY23 Q1 earnings presentation, it was relatively unremarkable. The company’s planning to share updates from the Phase ½ RUBY trial for ‘301 in SCD at an oral presentation at the upcoming EHA in July. They plan to present 10-month follow-up data from the first patient (up from the previous 5 months), 6-month follow-up data from the second patient (vs. 1.5 months previously), and data on safety, engraftment, and VOE from the first 4 patients. They’re also on track to dose 20 SCD patients by year-end, and we can expect neutrophil and platelet data from EDITHAL (by year-end, of course).

So, to sum it up, EDIT is slowly inching its way toward its key data goals set for later this year. Yet, I’m still well on the sidelines, given the lack of clarity around the ‘301 strategy. I see the potential for their gene-editing system, but I believe the market needs a bigger step forward from ‘301 to reignite interest. Thus, I maintain my neutral stance on EDIT shares, with a price tag of $9.

What to Expect for FY23 Q2 and Q3 from EDIT

Editas Medicine ((EDIT)) releases Q2 earnings on August 2 nd this year. Here are some things I will be looking for:

- Results from the RUBY and EDITHAL trials involving EDIT-301

- More color on the recent $125M equity offering

- More color about the continuous decrease in net debt

- New Drug Applications or requesting Fast Track, Breakthrough Therapy, or Orphan Drug Status

- Any Changes in key staff – especially the appointment of a new CSO

- New drug candidates entering EDIT’s pipeline or new partnerships (unlikely)

- BLUE, CRSP, and NTLA also publish Q2 Results in early August. So definitely something to keep an eye o

EDIT – Changes to My Valuation

Cash Per Share

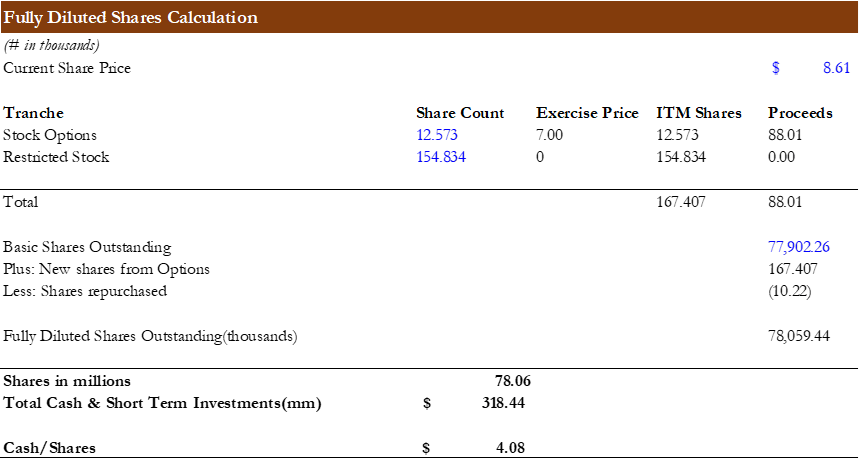

My last cash-per-share valuation of EDIT was when EDIT was trading at $10.15 per share, with roughly $68 million shares diluted and $419 million cash and short-term investments. This gave me a $6.12 cash/share ratio – at the time that showed that 60% of EDIT’s fully diluted equity value was backed by 60% in cash and short-term investments.

Since then, EDIT’s cash & equivalents have decreased by $100 million, shares outstanding have risen by nearly 10 million, and the share price has dropped to $8.61. There has been no change in stock options nor restricted stock as per the Q1 2023 10-Q .

After the recent changes, EDIT’s Cash/Share ratio has dropped to $4.08 (~2/3 the value from 5 months ago). This represents that ~47% of EDIT’s fully diluted equity value is backed by cash & short-term investments (vs 60% 5 months ago) despite the equity value dropping ~-15% in the past 5 months.

See below for the new calculation:

Cash & Short Term Investments per FDSO Calculation (Author's Data)

{kind=link}

This is a big change in the past 5 months to EDIT’s financials and only reassures my increasingly bearish view of the company in the short term.

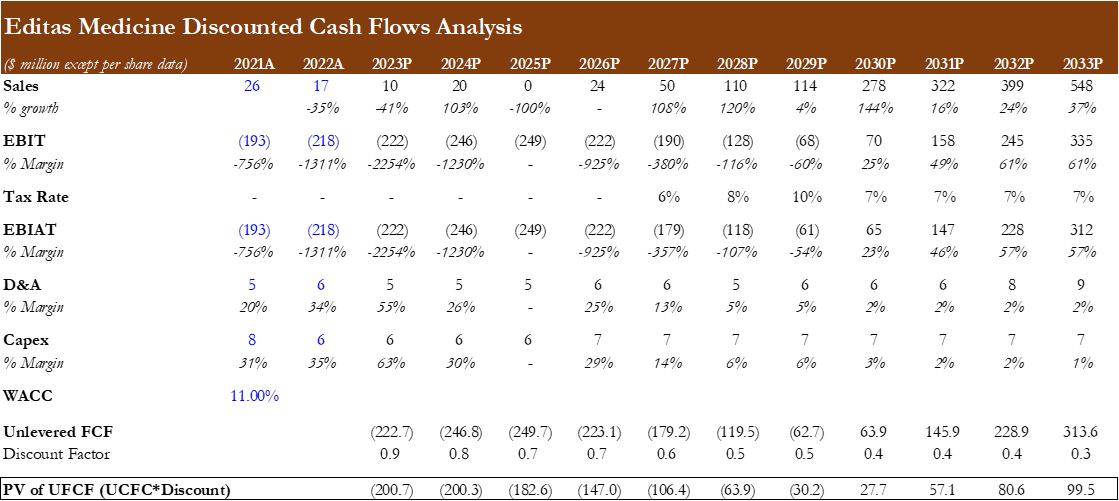

Discounted Cash Flows Analysis

When I covered EDIT last time, I had set a rather high price target of ~$18 per share (no specific date). Using the same 10-year DCF, I now arrive at half that implied price of $9.00 per share (set for year-end). My valuation has changed with adjustments to pipeline developments, corporate expenses, Net Operating Losses (NOLs), and existing cash holdings after their new offering and cash outflows from Q1.

To shape the SCD component of the valuation, I relied on similar assumptions (11% WACC and 0% Terminal Growth Rate). What I included was a Probability of Success (PoS) of 25% and a Gross-To-Net ((GTN)) value of 20% (PoS is an estimate of the likelihood that the drug will receive approval, and GTN is the difference between the list price of the drug and net price after adjusting for discounts/rebates). I then continue projecting cash flows all the way to 2033, without anticipating any growth beyond this time horizon. The PoS and GTN value has been adjusted to all estimates in the adjusted DCF below:

DCF (Author's Data) Calculation of Firm Value (Author's Data) Sensitivity Analysis (Author's Data)

{kind=link}

Despite my DCF estimates changing to reflect a more risk-adjusted forecast and to represent my increasingly bearish view on EDIT, more things have changed in EDIT’s capital structure. See below for changes since my last article (5-month timeline):

- Cash & Short Term Investments dropped to $318.4M (vs. $419.6M previously)

- Total Debt rose to $37.1M (vs. $21.3M previously)

- Long-term marketable securities increased to $83.3M (vs. $58.8M previously)

Overall, this is now $281.3M in net debt, a large decrease from the $398.3M 5 months ago. This is obviously a concern and something I am hoping to get more color on from the management team at the earnings presentation in early August.

The Last Word

While Editas Medicine ((EDIT)) is making steady progress with its EDIT-301 therapy, the broader picture reveals significant challenges. The competition is fierce, and it will take time and further evidence to carve out a more substantial market share. Meanwhile, financial metrics show a decline that echoes my increasingly bearish view on EDIT’s short-term. The hope is that future earnings presentations will bring clarity and perhaps positive changes. Still, as it stands, EDIT requires both scrutiny and cautious optimism. At this point, I believe (depending on your investment strategy) that reducing your stake in EDIT and moving money elsewhere is something to consider. It’s a wait-and-see game as we anticipate the unfolding of Q2 and Q3 developments, keeping a close eye on EDIT’s journey through the increasingly competitive landscape. As such, I maintain my neutral/hold rating on EDIT, with a new $9.0 price tag for FY23.

For further details see:

Editas Medicine: Progress, Pitfalls, And Future Expectations