EDIT - Editas Medicine: RUBY Gems Sparkling Catalysts In Sickle Cell Arena

2023-10-03 02:59:03 ET

Summary

- Editas Medicine's reduced R&D costs and strong cash position provide operational comfort but necessitate future capital, especially amid looming competition from exa-cel.

- EDIT-301 shows early promise in sickle cell disease, pivotal for Editas' valuation as it approaches critical milestones, including RUBY trial results and FDA decision on competitor exa-cel.

- Investment Recommendation: Buy Editas for its stable finances and early-stage clinical promise in EDIT-301, albeit with cognizance of high-risk factors like competition and potential financing needs.

At a Glance

Building on my prior analysis , Editas Medicine ( EDIT ) is at a critical financial and operational crossroads, amplifying its profile as a high-risk, high-reward investment. The competitive landscape has escalated, particularly due to rivalry from exa-cel ((CRSP)). Upcoming RUBY trial data for sickle cell disease [SCD] now serves as an even more crucial catalyst, especially given the existing high short interest. While the firm holds a solid cash position, it's not fully shielded from future capital obligations, warranting close monitoring of cash burn and potential dilutive actions. Additionally, the changing dynamics of insider transactions and institutional ownership require investor attention, underlining the need for a calculated, data-driven investment strategy focused on near-term clinical and regulatory milestones.

Q2 Earnings

To begin my analysis, looking at Editas Medicine's most recent earnings report for the quarter ended June 30, 2023, one can discern a mixed financial landscape. R&D expenses have declined YoY from $43.7M to $29.8M, offering some relief, yet collaboration and R&D revenues dropped from $6.4M to $2.9M, aggravating the operating loss to $44.1M. Other income showed improvement, notably a $3.3M uptick in net interest income. There's a slight dilution concern as the weighted average common shares outstanding increased from 68.6M to 71.4M. Despite a lower net loss of $40.3M compared to $53.5M YoY, the liquidity runway should be scrutinized given the shrinking revenues.

Financial Health

Turning to Editas Medicine's balance sheet , as of June 30, 2023, the firm had $220.8M in 'Cash and cash equivalents' and $211.2M in 'Marketable securities,' summing to total liquid assets of $432M. The 'Current ratio,' calculated as total current assets ($440.9M) divided by total current liabilities ($54.5M), stands robust at approximately 8.1. Net cash used in operating activities over the past six months was $74.5M, translating to a monthly cash burn rate of about $12.4M. This provides the company with a cash runway of approximately 35 months. Note that these are estimates based on past performance and may not necessarily predict future outcomes.

Given its substantial cash position and a comfortable cash runway, the immediate need for additional financing appears limited. However, the monthly cash burn rate cannot be ignored. Assuming no drastic changes in operating expenses or new streams of revenue, the likelihood of the company needing to raise equity within the next twelve months appears moderate. In summary, while Editas is well-capitalized for the near term, future financing could become essential depending on operational shifts and capital deployment strategies.

Equity Analysis

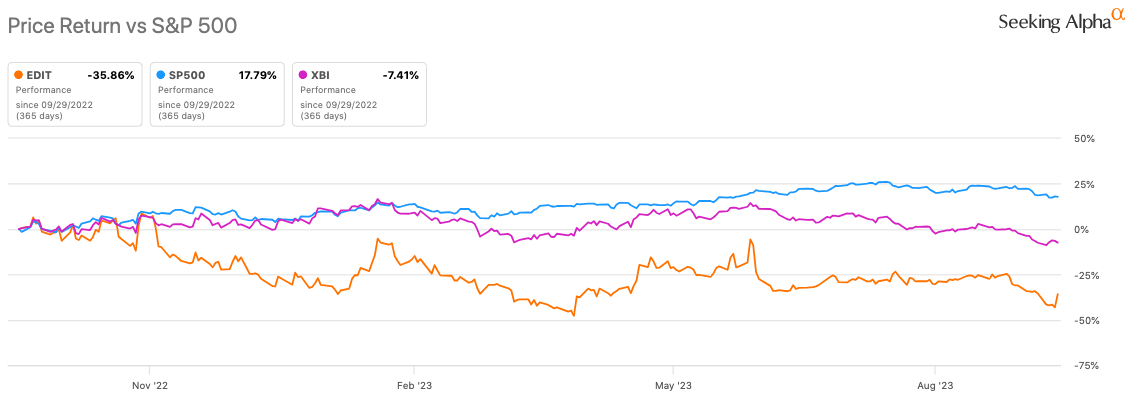

According to Seeking Alpha data, Editas Medicine has a market cap of $620.49M, signaling a moderate level of market confidence given its early-stage pipeline. Analysts project a 31.09% YoY revenue increase for 2025 to $24.4M, indicative of future growth, albeit from a low base. The stock underperformed the SP500 across all major timeframes, most notably trailing by over 50% in the past year. The 24-month beta of 1.91 suggests higher volatility compared to the market.

{kind=link}

Short interest is substantial at 20.3%, signifying bearish sentiment likely due to competitive headwinds. Institutional ownership dominates at 76.44%, providing a stable shareholder base but also setting the stage for potential activist involvement. Insider trading shows a recent trend towards selling , albeit at moderate volumes, which could raise minor concerns about management's confidence in the firm's short-term prospects.

Editas Advances Hemoglobinopathy Therapies

Editas Medicine has been making significant inroads in the field of ex vivo hemoglobinopathies. The company's EDIT-301 candidate, aimed at SCD, is on track to dose 20 patients in the RUBY trial by year's end. It has already gained traction with positive initial clinical safety and efficacy data. Notably, the company's data presentation at reputable venues, like the European Hematology Association, lends a layer of credibility to these early results. The company is also progressing with its EDIT-301 candidate for Transfusion-dependent Beta Thalassemia (TDT) under the EDITHAL trial. The use of parallel dosing here might serve as an accelerant for data collection and eventual market entry.

This operational rigor aligns well with recent market sentiment. Stifel's recent upgrade of Editas from "Hold" to "Buy," and the price target elevation to $17, suggests that the investment community is beginning to take notice. Analyst Dae Gon Ha specifically mentioned that the full potential of EDIT-301 in SCD may not yet be priced into the stock. Stifel's call for a "fresh look" at Editas comes at an opportune moment given the impending FDA decision, slated for December, on exa-cel, another gene-editing therapy for SCD.

If exa-cel receives FDA approval, it could serve as a double-edged sword for Editas: creating a favorable regulatory environment but also introducing strong competition. Thus, both from a clinical and investment standpoint, Editas seems to be at a crucial juncture that warrants keen attention and scrutiny.

My Analysis & Recommendation

In summary, Editas Medicine finds itself in a precarious yet promising position. The company's prudent R&D expenditure coupled with its robust balance sheet provides ample runway to navigate the inevitable challenges that accompany clinical-stage assets like EDIT-301. The looming RUBY trial milestones are not just potential inflection points for the company but also for the broader gene therapy market, which continues to grapple with regulatory complexities and high costs of goods.

As the gene therapy field contends with unresolved challenges like inconsistent efficacy, safety concerns, and the specter of regulatory clampdowns, it is crucial for investors to understand that the general market hurdles are not exclusive to Editas. These challenges could introduce unforeseen delays and require additional capital, irrespective of Editas' current liquidity.

The firm's underperformance compared to the SP500 and high short interest of 20.3% represent short-term volatility risks. Yet, these could also morph into opportunities for a short squeeze, particularly if the RUBY trial data turns out favorable. Also noteworthy is the significant institutional ownership, which, while lending stability, opens the door for potential activist involvement, something that could tip the scales in either direction.

Keep an eye on the FDA decision regarding exa-cel. An approval could be interpreted as a constructive regulatory outlook for Editas' SCD endeavors but also bring forth intensified competition. With a market cap of $620.49M and revenue projections signaling growth, the upside seems substantial if Editas successfully navigates these obstacles.

Against this backdrop, my stance on Editas Medicine remains a "Buy." However, this is not a blanket endorsement but a carefully weighed decision based on the firm’s strategic positioning, financial resilience, and future growth prospects. High-risk tolerance and a keen eye for nuance are essential for investors seeking to capitalize on the imminent clinical and regulatory milestones. Expect the stock to react significantly to news flows around RUBY trial results and any shifts in the competitive landscape.

Risks to Thesis

While the thesis strongly supports a "Buy" stance on Editas Medicine, there are counterarguments worth noting. First, CRISPR technology itself faces ethical and safety concerns that could influence regulatory outcomes. Any adverse events in gene-editing trials across the industry could lead to stricter regulations, impacting Editas' pace of development.

Second, the competition is more diversified in technology and application than just exa-cel. Broad patents from other gene-editing companies like CRISPR Therapeutics ( CRSP ) or Intellia ( NTLA ) could limit Editas' operational scope or impose litigation costs.

Third, the noted reduction in R&D spend could be a double-edged sword. While it extends the cash runway, it also could indicate a slower pace of innovation, something critical in a fast-moving field like gene editing.

Lastly, the high institutional ownership, though generally a bullish sign, can create liquidity risk. Institutions often have longer holding periods, and if they decide to offload shares, the stock could suffer from rapid devaluation.

For further details see:

Editas Medicine: RUBY Gems, Sparkling Catalysts In Sickle Cell Arena