EDPFY - EDP: Reservoirs Back To Normal Buying Out EDP Brasil

2023-05-28 05:26:33 ET

Summary

- EDP has been benefiting mostly from a huge recovery in hydrology conditions YoY, which were a disaster last year with droughts.

- Otherwise, EDP continues to grow its capacity and electricity production in wind and solar.

- Networks continue to demonstrate highly stable performance.

- At ~13x run-rate PE with what we believe are sustainable earnings, and a decent move to buy out minorities in EDP Brasil, EDP actually looks good right now.

- Especially as cost of debt concerns aren't major for them given fixed rate structure and favourable maturity profile.

Energias de Portugal ( OTCPK:EDPFY )( OTCPK:ELCPF ) is one of our preferred utility names in Europe. Currently they are benefiting from a major recovery in hydrology condition in Iberia that hassled the 2022 results, but also some decent organic growth in wind and solar. Moreover, their fixed rate debt structure insulates them from higher cost of debt. The big news is that they raised equity. They have quite high leverage, and equity raises aren't such a great sign, but in this case they did it to buy out minorities in EDP Brasil at a really good PE multiple, but also to finance some more renewable buildout. In the longer term, this should pay off, and we continue to believe in their asset rotation model and dividend over priorities like deleveraging, which isn't critical given their very favourable maturity profile.

Quick Q1 Look

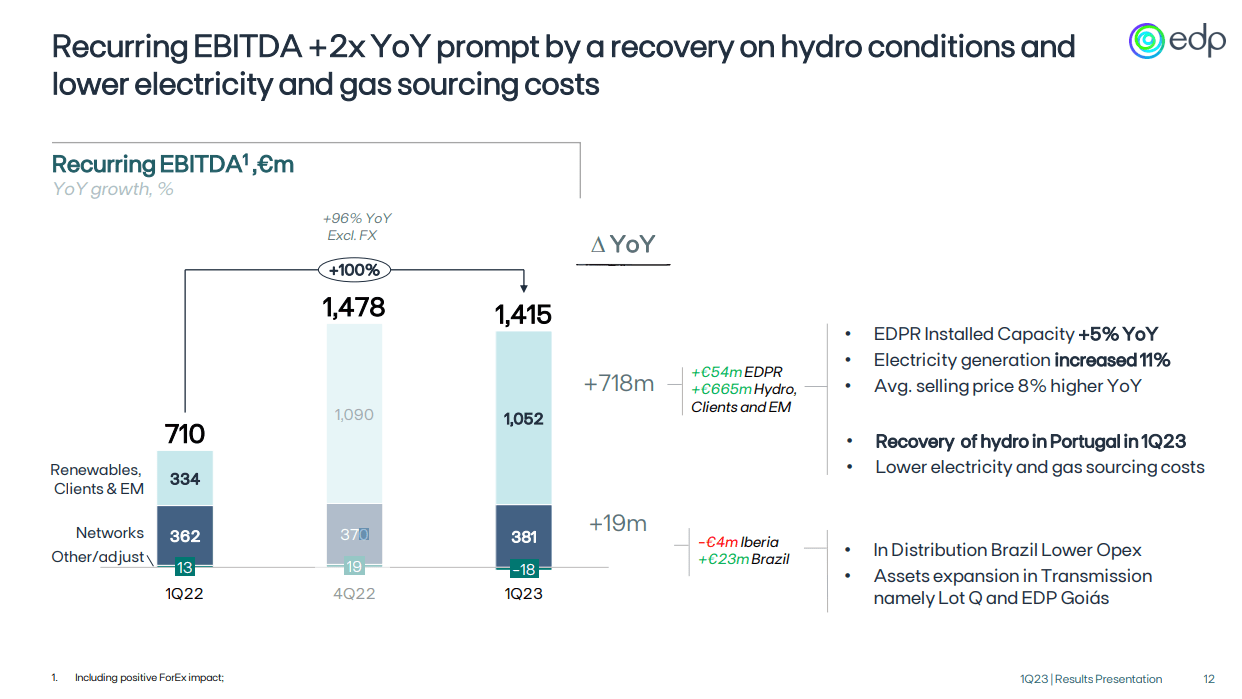

There was a major jump coming from the hydro results. Iberia and much of Southern Europe had major droughts that year that decimated hydropower income. Reservoirs are currently slightly above historical averages, although still within normal ranges, contributing to visibility in hydropower production, which is reassuring as we enter into the summer months. The EBITDA went from negative to normal, positive levels YoY driven entirely by generation volumes.

{kind=link}

Wind and solar saw continued increases in installed capacity as CAPEXing yield fruit, with installed capacity growing by 5%. Generation was up 11% with slight increases YoY in electricity prices consistent with general levels of inflation at around 8%. On price and volume effects the EBITDA was up 14% for wind and solar, showing strong organic results from the segment. The ratio between hydro EBITDA and wind & solar EBITDA is 2:1 currently.

In networks, stable performance continued after last year's jump due to revisions in the tariff arrangements with the Brazilian government, consistent with higher interest rate levels and inflation, to compensate their regulated utility concession in line with fair levels and the regulatory WACC.

EDP to Buy Out EDP Brasil Minorities

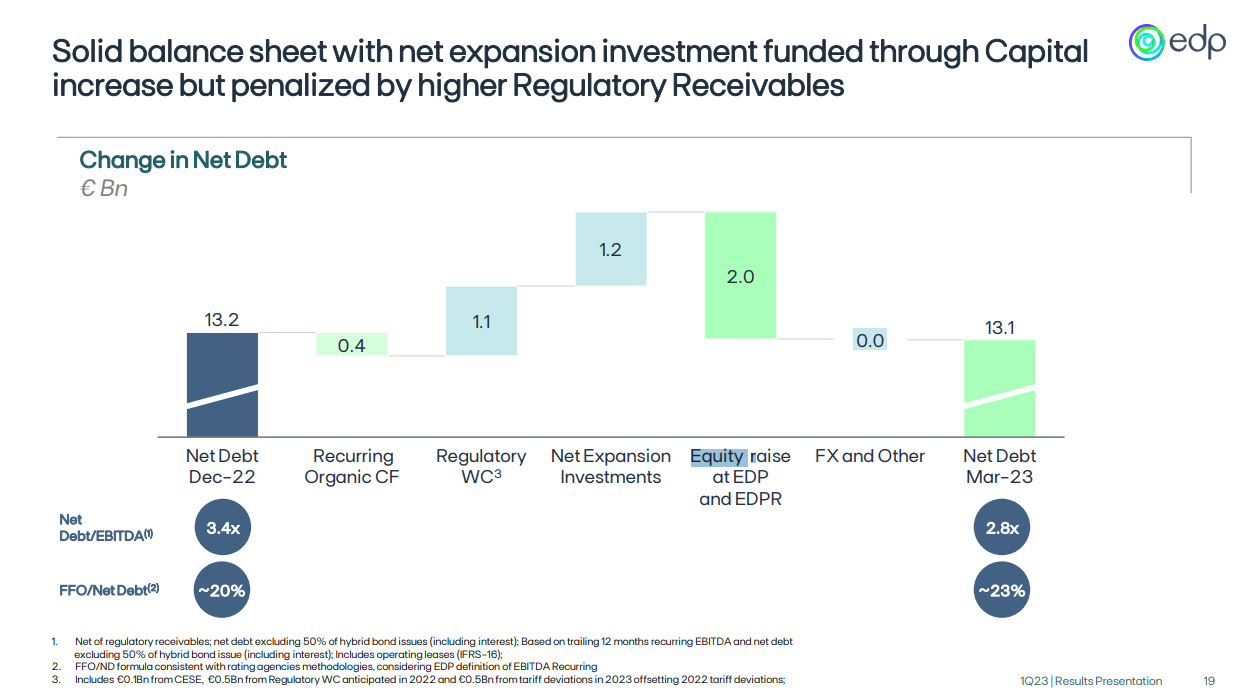

A quite surprising arrangement has been the decision by EDP to raise equity. From a finance optimisation perspective, it makes some sense due to the peculiarities around EDP's financial structure. They are 75% fixed rate debt, and maturities are mostly far out.

{kind=link}

Cost of debt has gone from 3.9% to 4.8%, which is quite the increase, and raising new debt would come in at that higher cost. Meanwhile, stock prices had held steady, so comparatively the cost of equity has gone down - especially considering EDP was priced according to pre-downturn levels, when equity earnings yield were probably pretty similar to the current rates of cost of debt.

The total amount raised equates to a 10% dilution, which is meaningful, and has resulted in EDP's recent declines. However, the use of the funds should give investors confidence for value accretion. They are buying out minority interests in EDP Brasil, and the multiple they are paying in PE is pretty low at around 3-4x. EDP Brasil contains the regulated utility businesses that EDP operates in Brazil, and the regime there is actually quite favourable, especially as Lula brings energy transition and electrification into focus.

{kind=link}

2 billion EUR were raised, 1 billion is going into the EDP Brasil purchase, where minorities used to own the other half, while the other billion is being put into various CAPEX projects to develop some more EDP assets that should come online in 2-3 years .

Bottom Line

EDP currently trades at around a 13x run-rate PE considering the reconsolidation of the EDP Brasil income that used to go to minorities. The dividend remains at around 4%. The dividend doesn't grow because EDP has focused on asset rotation, meaning developing then selling assets at pretty accretive multiples, almost always higher than the comprehensive EDP multiple. This has made meaningful gains on their project equity in the past, and we like the model. However, it doesn't lend itself to either deleveraging or a growing dividend because capital is being committed to that reinvestment cycle rather than other capital allocation priorities. Since the debt is fixed rate and matures mostly later, this is alright even in the current environment. Moreover, infrastructure remains one of the few areas where private market activity is still very strong. Considering everything, EDP actually looks like a rather decent deal right now as a resilient utility with easy scope for income growth as they mature more projects and rotate them at good multiples. They've always been a solid buy in our books.

For further details see:

EDP: Reservoirs Back To Normal, Buying Out EDP Brasil