EIC - EICB: Covered 7.8% Yield From This CEF Preferred Equity

2023-11-18 06:17:26 ET

Summary

- EICB is a preferred equity series issued by a closed-end fund focused on junior CLO tranches (CLO debt and equity), tranches primarily rated below investment grade.

- EIC utilizes a combination of a small bank facility and two series of term preferred equity for leverage, shifting toward more reliance on preferred equity.

- This preferred equity matures in July 2028, offering a current yield of 7.79%. Optional redemption begins in July 2025.

- The CEF maintains robust asset coverage (coverage ratio exceeding 4x) for the preferred equity, contributing to stability, and potential principal recovery even in severe crisis scenarios.

Thesis

Eagle Point Income Company Inc. (EIC) is a closed end fund. The fund aims to generate a high level of income via investments in junior CLO tranches. These represent the below investment grade portion of CLO debt, and are usually rated in the BB band. The CEF can also take positions in CEF equity, which represents 25% of the current collateral pool:

Collateral Composition (Company Presentation)

CLO debt is less risky than CLO equity because it contains a higher degree of subordination, but nonetheless the CEF contains leveraged high yielding collateral that can gap down substantially in a prolonged recession.

One has to keep in mind that securitized products that are tranched have embedded leverage, with the equity and junior tranches of a CLO structure being the first ones to absorb any collateral losses. As an example, if you have a pool of leveraged loans worth $100, the first $10 in defaults/write-downs here come exclusively from the CLO equity / junior tranches. Thus low overall default levels do not affect the BBB/AAA CLO slices, but can wipe out the entire junior capital structure.

The riskiness of a CEF's collateral pool has a 1:1 correlation with the leverage it can get from a bank and the cost of that leverage. As we have seen with Oxford Lane Capital Corporation ( OXLC ) and Eagle Point Credit Co LLC ( ECC ), the direct result of such collateral is the reshuffling of the liability structure for such CEFs when compared to traditional fixed income ones. While most fixed income CEFs have a mix of bank facilities and preferred equity, CLO equity CEFs contain unsecured notes and term preferred equity.

EIC is a hybrid of the two, containing both a small bank facility (currently undrawn) and two series of term preferred equity. In this article we are going to analyze the Series B Term Preferred Stock due 2028 ( EICB ), its analytics and metrics, and derive an opinion regarding the risk and rewards associated with owning this security.

CEF Liability structure

As discussed above the CEF has a small bank facility and two series of preferred equity, as shown in its Q3 figures:

Liability Structure (Presentation)

As per its Semi-Annual Report back in June, the bank facility had the following characteristics:

On September 24, 2021 the Company entered into a credit agreement, which was amended on September 6, 2022, with BNP Paribas, as lender, that established a revolving credit facility (the "BNP Credit Facility"). Pursuant to the terms of the BNP Credit Facility, the Company can borrow up to an aggregate principal balance of $25.0 million (the "Commitment Amount"). Such borrowings under the BNP Credit Facility bore interest at 1 month LIBOR plus a spread under the original credit agreement, and will bear interest at Term SOFR plus a spread under the amended credit agreement. The Company is required to pay a commitment fee on the unused amount.

The CEF is moving towards more reliance on term preferred equity, with the analyzed tranche, Series B, being issued in July 2023. The shares were offered at $25/share and resulted in the CEF securing $27.1 million in financing.

The series matures in July 2028, but have an optional redemption date commencing in July 2025. The optional redemption allows the issuer to redeem the shares early if market conditions permit the placing of new preferred shares with more advantageous features from a funding perspective. We do not expect the Series B to be called in the next three years given the elevated interest rate environment and how the forward fed funds curve shapes up.

To note that the first tranche of preferred equity from the CEF, namely the Series A Term Preferred Stock, has a term maturity of October 30, 2026. At any time on or after October 31, 2023, the CEF may redeem the outstanding shares of the Series A Term Preferred Stock. Given the low coupon of 5% on the Series A we do not expect it to be called until maturity date.

Analytics and yields

The Series B currently yields 7.79% (current yield is very close to yield to maturity given proximity to par), or treasuries plus roughly 300 bps:

Yield (Preferred Stock Channel)

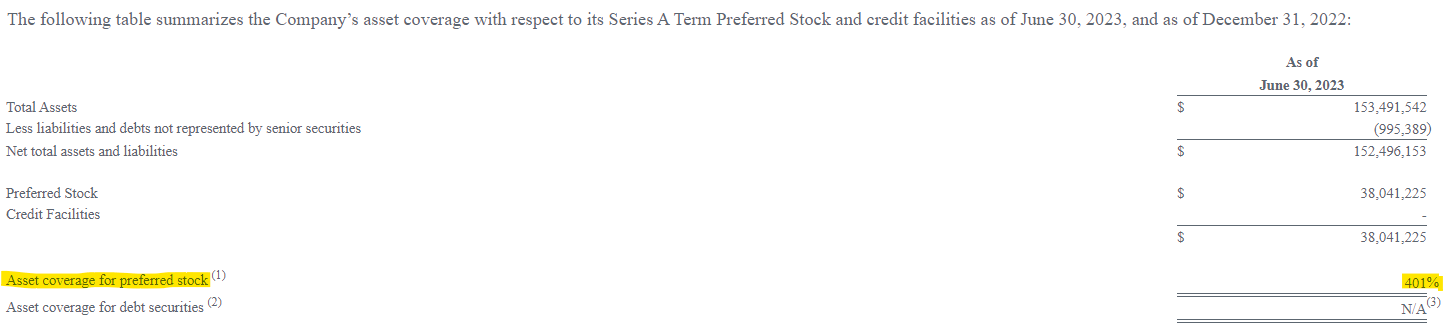

The spread is borderline high yield, although the preferred equity is supported by the CEF's collateral pool and has a term maturity date. Many tranches of preferred equity have poor ratings from the rating agencies due to their perpetual structure. Not in this case. Furthermore, the asset coverage for the tranche meets the 200% regulatory requirement by miles:

{kind=link}

What we like about the collateral pool here is the fact that it is not only CLO equity. CLO debt which is two thirds of the holdings here, has set maturity dates and return of principal features. To that end, we are going to see much more stability price wise in the collateral pool for this CEF versus an outright CLO equity CEF. That will translate into very stable and robust asset coverage ratios. We view the Series B preferred equity as the equivalent of a well-supported five year investment grade bond. To that end the yield and risk/reward features are very attractive here.

Risk factors

The main risk factor here is a widening of credit spreads which would put pressure on the series B pricing. Since EICB has a five year duration, any 100 bps move in credit spreads should equate to around a -5% loss in price for the security. With Fed rate hikes behind us, we consider credit spreads as the only viable risk factor here.

From a fundamental perspective, given the term maturity date for the preferred equity and robust asset coverage, we are not worried about a decrease in the probability of 100% principal recovery here. Even if a severe fundamental crisis develops and some of the CEF collateral defaults, the structure has enough collateral to account for a full principal repayment of the Series B.

Conclusion

EICB is a newly issued preferred equity from the Eagle Point Income CEF. The structure focuses on CLO debt and equity, with mainly below investment grade holdings. The fund obtains leverage via preferred shares and a small bank facility, and is switching to higher preferred equity utilization via the recent July 2023 EICB issuance.

The CEF has a very robust asset coverage for preferred equity, coverage ratio which exceeds 4x. EICB has a 2028 maturity date, and a 7.79% current yield, equating treasuries plus 300 bps. We like the asset coverage and the term maturity date here for EICB, with the security offering a very attractive risk/reward proposition at the current elevated risk free rates. We are a buy for the name here.

For further details see:

EICB: Covered 7.8% Yield From This CEF Preferred Equity