ELAT - Elanco's Tangible Equity Units: Living With The Worst Case

Summary

- Elanco Animal Health, an Eli Lilly spin-off, is the second-largest pure-play in the industry.

- Acquisitions to achieve critical mass resulted in a protracted period of restructuring, reorganization and poor financial performance.

- Elanco's tangible equity units (NYSE: ELAT) offered interest payments and conversion to Elanco common on February 1, 2023.

- Most investors should pass on ELAT and ELAN.

- ELAN is suitable for value investors with a 3 to 5-year time horizon looking for a speculative transformation play for a small portion of their portfolios.

If you believe your analysis is correct, value investing can require a fair amount of time living with your worst case scenario. For this 3 to 5-year time horizon value investor, the latest example is an investment in the tangible equity units ( ELAT ) of Elanco Animal Health Inc. ( ELAN ).

How bad has it been?

The units are a hybrid security consisting of stock and debt components that are approaching a mandatory conversion date.

Let's review the components of this hybrid security.

The Stock Component

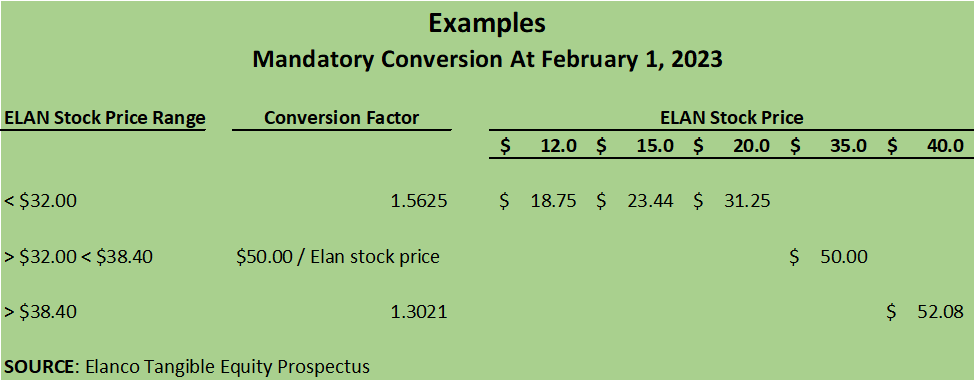

The stock component consists of a stock purchase contract that mandates conversion of the "stock portion" of each ELAT unit to ELAN common stock on February 1, 2023. Here are a few examples of possible outcomes given ELAN's stock price:

{kind=link}

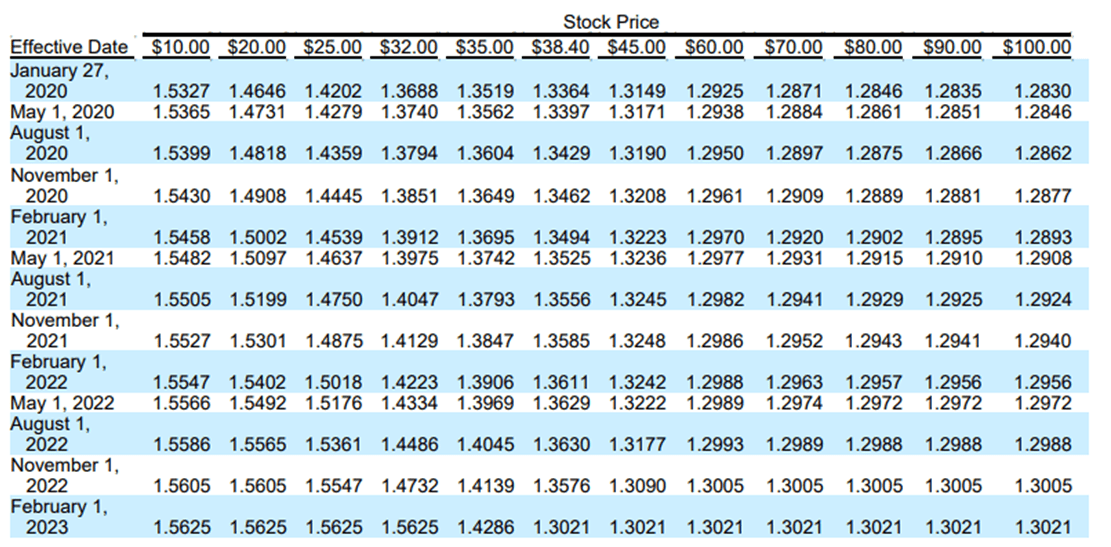

Note that a unit holder has the right 1) to convert early at a 1.3021 conversion ratio and 2) to convert upon a "fundamental change" to Elanco, e.g., a change in control, recapitalization, liquidation or delisting, etc., with a conversion rate (interpolated if necessary) as follows:

Elanco Tangible Equity Unit Prospectus

{kind=link}

With the November 2022 special situation conversion date past and ELAN stock hovering around $12.00 to $13.00 per share, it's likely that the 1.5625 fixed rate will be operative. An ELAT holder at those prices, for example, would receive $18.75 to $20.31 per share in ELAN common.

The debt component, however, is what made the units of interest to me (pardon the pun) when I invested.

The Debt Component

When issued, the debt component consisted of senior amortizing notes with a total principal amount of $79.0 million, about $7.20 per note with one note per unit. The notes pay 2.75% annual interest in quarterly cash installments of $0.625 ($2.50 per year) on each February 1, May 1, August 1, and November 1 until the maturity date of February 1, 2023. Each installment consists of a payment of interest and principal, for a combined "cash yield" of 5.00% per year on the $50.00 stated value of each unit. When I purchased units they were trading at a large discount to the $50 stated value, so my yield was much higher.

As of December 15, 2022, with one payment of $0.625 per note remaining, the principal amount had been amortized to roughly $0.621 per note, i.e., only about $0.04 of the remaining payment consists of interest. Below is the amortization schedule; note that as return of capital is not taxable:

Herding Value Analysis, Elanco Tangible Equity Unit Prospectus

The darker portion in the table above is what has already been paid.

ELAN can repurchase the notes, but only if a unit holder has requested a repurchase coincident with ELAN's exercise of its right of early mandatory conversion. In that event, the conversion table in "The Stock Component" above will be applied based on the current stock price with some adjustments for possible eventualities such as defeasance, default, etc. Although the possibility of any of these events seems remote, please see the prospectus for more detail. Here is a link to the original prospectus .

There are also two supplements, but other than registration fees, etc. nothing changed from the original.

Let's walk through the investment and see if it still makes sense.

What is Elanco Animal Health, Inc.?

Elanco Animal Health, Inc. is the 2019 spin-off of Eli Lilly's (NYSE: LLY ) animal health business. There was precedent in Pfizer's (NYSE: PFE ) highly successful 2013 spin-off of its animal health business as Zoetis (NYSE: ZTS ).

ELAN, however, unlike ZTS, did not immediately prosper. The Pfizer unit was bigger (2021 revenues of $7.8 billion compared to ELAN's $4.8) and better organized. ELAN needed scale and structure and management responded with the "Innovation, Portfolio and Productivity Strategy" designed to address organizational and operational issues plus three notable acquisitions; $234.0 million in 2019 for Aratana to bulk up the drug pipeline, $6.9 billion in 2020 for Bayer Animal Health, which made ELAN the second-largest pure-play public animal health business and $444.0 million in 2021 for Kindred Biosciences, a biotech company focused on therapies for dogs, cats and horses.

Financial Performance

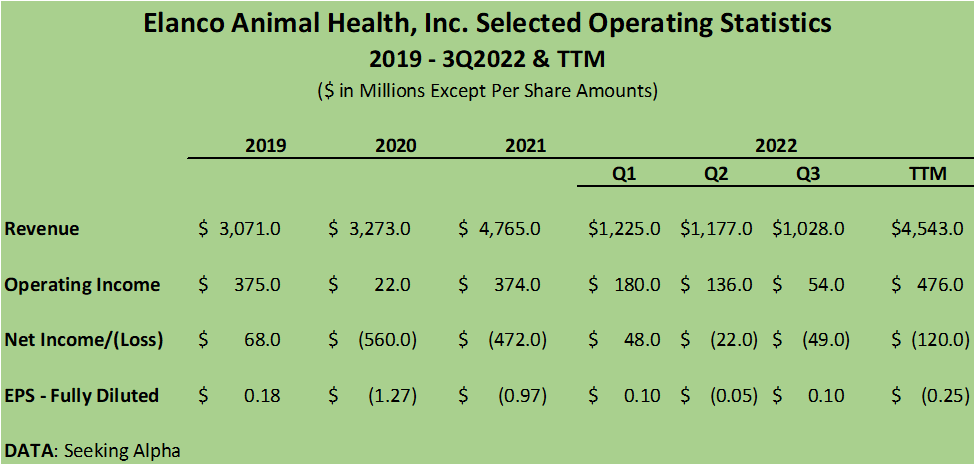

The result, although arguably necessary for long term profitability, has been a protracted period of restructuring, reorganization and poor financial performance.

{kind=link}

The data in the chart above is all on a GAAP basis.

Management supplements GAAP numbers with adjusted numbers to screen out all the acquisition static. For example, management reported adjusted 3Q2022 net income of $96.0 million compared to the GAAP $49.0 million net loss. The adjusted numbers have been scrubbed for acquisition-related amortization, impairment and restructuring expenses.

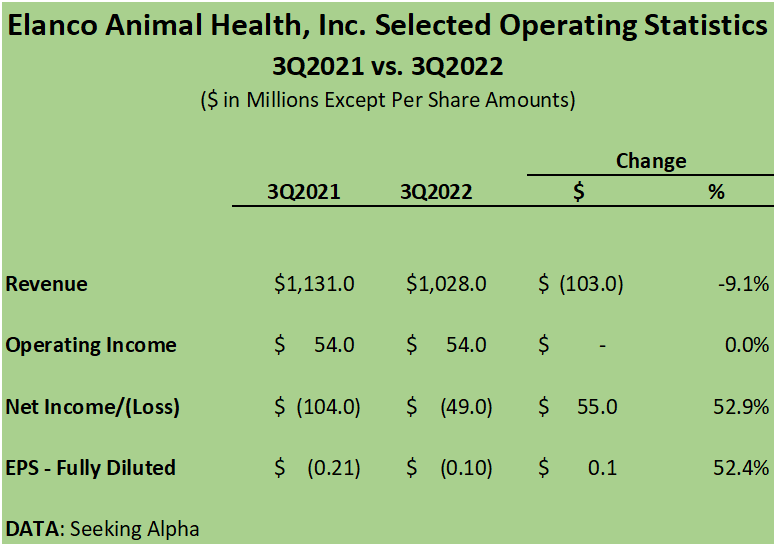

The most recent earnings report for 3Q2022 was mixed. Of the 9.1% decline in revenue, about 5.1% was currency exchange-rate related leaving 4.0% attributable to COVID, China lockdowns (ELAN does a sizable business in that country) and declines in the aging Advantage and Seresto companion animal product lines.

{kind=link}

Adjusted EPS of $0.20 per share (GAAP presented above) was a positive surprise for the Street as the consensus estimate was adjusted EPS of $0.16. Guidance was cut, however, with management predicting midpoint adjusted EPS of $1.04 compared to previous (August) guidance of adjusted EPS of $1.10. The stock subsequently sold off.

Elanco: Investment Thesis

Since its spin-off, ELAN has disappointed investors who counted on at least an approximation of the next ZTS. Acquisitions aimed at transforming the business through pipeline diversity and operational scale have hampered performance and obfuscated the numbers.

For a value investor, however, there are positives to consider:

- Animal health is a growing and somewhat recession-resistant industry.

- ELAN is the second-largest pure play in the industry.

- Management has transformed the company; the traditional drug pipeline is deeper thanks to Aratana, Bayer and ELAN's own science and Kindred provided bio-tech expertise and a non-traditional drug pipeline.

- Management is committed to rationalization of operations.

Let's review perhaps the most important positive, the product pipeline, in more detail.

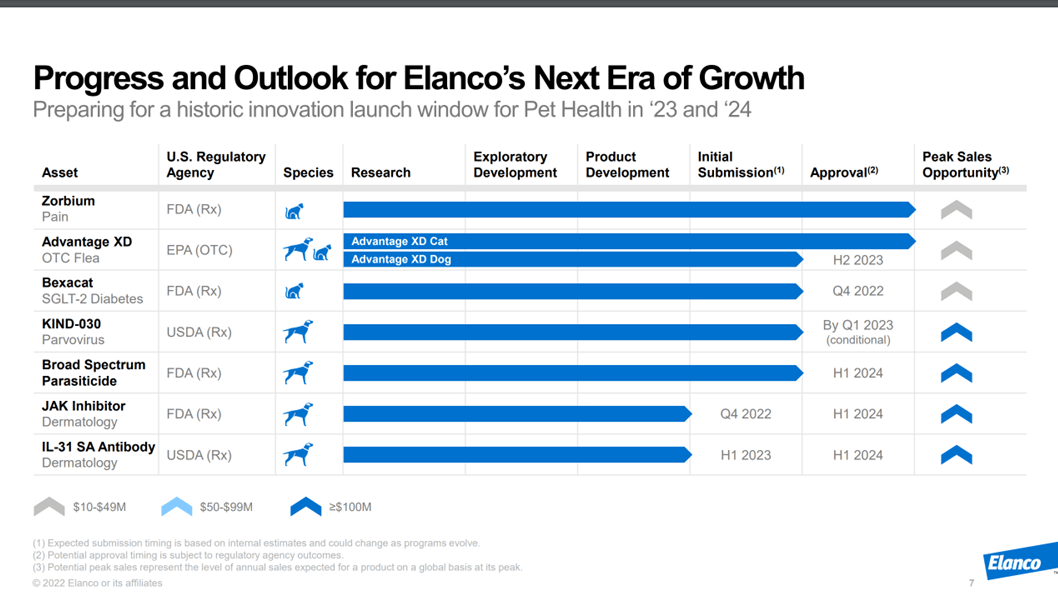

Product Pipeline

Here is management's latest take on the product pipeline:

Elanco 3Q2022 Investor Presentation

{kind=link}

Bexacat was approved by the FDA on December 9, 2022. It is the first orally administered prescription diabetes medication for cats. Although not a blockbuster, the drug represents estimated annual sales of up to $50.0 million.

Other drug approvals slated for 2023 include Advantage XD (fleas) for dogs with estimated annual sales of up to $50.0 million and KIND-030, a genetically engineered parvovirus treatment developed by Kindred with estimated annual sales in excess of $100.0 million.

The 2024 approval calendar looks even more promising with three drugs due for approval with all expected to exceed $100.0 million in sales.

There are also a few negatives:

- ELAN carries a lot of debt largely due to its acquisitions.

- ELAN has not reported GAAP net income since 2019, its first full year as an independent company.

- A March 2021 USA Today article, followed by lawsuits, claimed that there had been 1,700 pet deaths linked to the Seresto flea collar, a Bayer Animal Health product. ELAN, generally supported by the veterinary industry, disputes the article's findings as no scientifically valid investigative work was performed prior to publication. Subsequently, in June 2022, the Subcommittee on Economic and Consumer Policy of the House Committee on Oversight and Reform released a report recommending the recall of the collar after finding that about 2,500 pet deaths were anecdotally attributed to the collar - out of about 34 million collars sold, or about 0.01% of pets using the collars - without conducting a scientific evaluation and despite the collar being approved in 80 jurisdictions around the world.

We've dealt with financial performance. Regarding Seresto, per the 3Q2022 10-Q, ELAN is "vigorously defending" its position that the collars are safe.

We need to deal with the debt question.

The Debt Question

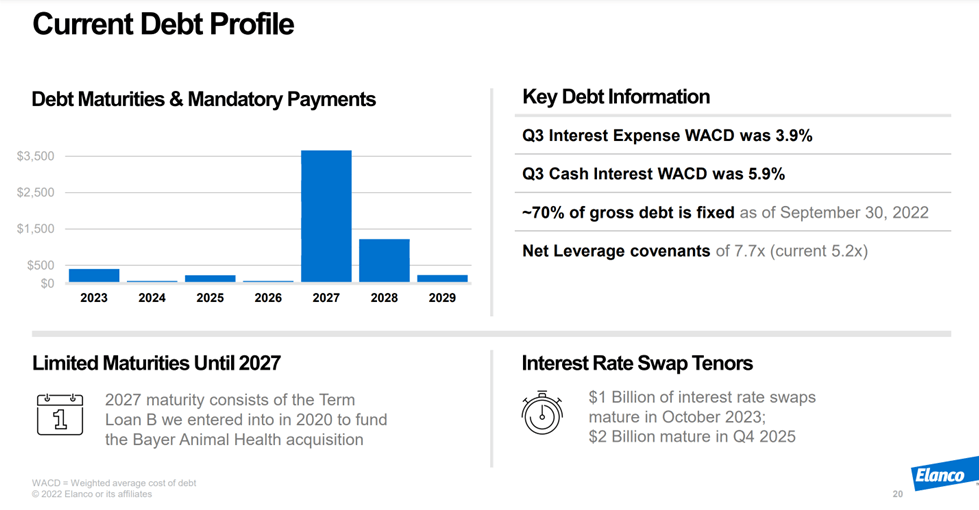

The price for achieving scale has been a heavy debt load. As of the end of 3Q2022, ELAN carried $5.5 billion in long term debt against a $6.01 billion market cap. In comparison, much larger competitor ZTS carried $5.2 billion in long term debt against a $71.5 billion market cap.

At the end of 3Q2022, ELAN's net leverage ratio was 5.2 x adjusted EBITDA, down slightly from 5.3 at the end of the previous quarter, but still much higher than the approximately 1.2 x EBITDA of ZTS. Although ELAN's net leverage ratio is high, as noted in the chart below, maturities are limited until 2027 and net leverage covenants are 7.7 x adjusted EBITDA.

Elanco 3Q2022 Investor Presentation

{kind=link}

Management's guidance is for the net leverage ratio to remain stable through year-end and analysts generally expect improvement in 2023. ELAN's corporate family ratings are non-investment grade; BB from S&P and Ba2 from Moody's. With an expected increase in EBITDA, an acquisition halt and some debt paydowns, ELAN's debt should be manageable, but will bear watching.

Valuation

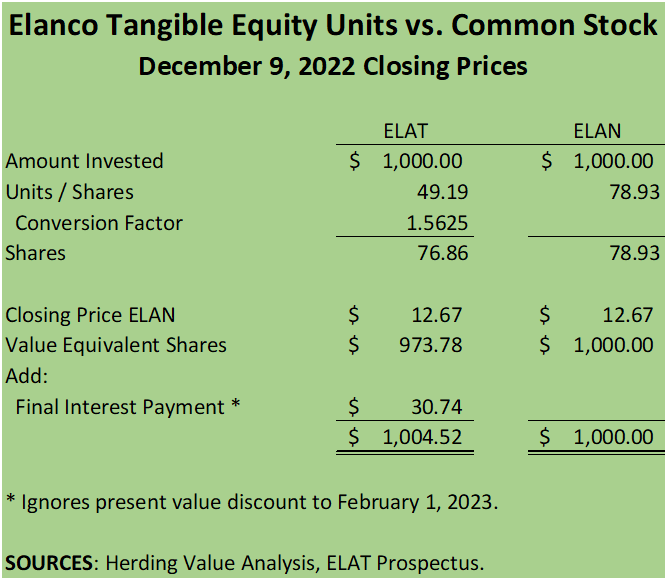

As the graph below indicates, Elanco's tangible equity units and common stock have been trading to provide nearly identical value with the price gap due to the conversion factor and the present value of the interest payments.

In other words, there's no free lunch, other than extremely short periods when the securities were possibly "out of synch" and could be exploited by a hedge fund's super computer. Most investors, however, can assume the two securities as almost perfect substitutes. For example, consider the calculations in the following chart:

Elanco Tangible Equity Unit Prospectus, Herding Value Analysis

{kind=link}

With the stream of income provided by the debt component almost completely gone, and the units and common stock trading in synch, any decision about ELAT is really a decision about the future of ELAN.

I put ELAN into a DCF model assuming a beginning $0.95 per share of free cash flow per Seeking Alpha, 3.00% annual growth, a long-term S&P 500 market multiple of 17 as the exit multiple, discounted at my personal 12.00% hurdle rate and came up with a per share value of $13.93. Performing a series of simple sensitivity analyses produced values of $12.00 to $15.00 per share.

In terms of multiples, ELAN appears to be trading off adjusted EPS. Management's 2022 guidance is for adjusted EPS of $1.04 and GAAP EPS of -$0.12 to - $0.17. At December 12, 2022's $12.64 per share, the implied adjusted PE is 12.15. Analysts are looking for 2023 to be another year of muddling through with (assumed) adjusted consensus EPS estimates of $1.05 to $1.07 depending on the source. With no multiple expansion, we get a share value of $12.88 at the adjusted 2023 EPS midpoint.

Most analysts see 2024 as the year when management's vision for the company begins to become reality with consensus estimates of $1.23 in adjusted EPS. Applying the same current multiple to be conservative provides an estimate of $14.94 per share - hardly compelling.

Recommendation

Investors should now pass on ELAT as the only reason to prefer the units to direct purchase of ELAN common stock, the debt component, disappears with the last remaining payment on February 1, 2023. Additionally, any arbitrage opportunity vis-à-vis ELAN common stock is so slight as to be useless for the non-institutional investor.

Investors with shorter time horizons and smaller portfolios should pass on ELAT and ELAN. A lot of puzzle pieces have to click for a meaningful increase in the share price over the next two years. Buy "best-in-breed" ZTS instead and forget about the complications of ELAN.

If, however, you're a value investor with a 3 to 5-year time horizon looking for a speculative transformation play for a small portion of your portfolio, consider ELAN common stock. Some notable investors have done so:

- Dodge & Cox filed a 13G on December 9, 2022 reporting its acquisition of 86.0 million shares or about 18.1% of ELAN's stock.

- Sachem Head Capital Management filed a 13D on September 7, 2022 reporting its ownership of 28.6 million shares or 6% of ELAN's common stock. At the same time, activist investor and head of Sachem Scott Ferguson resigned from ELAN's board with the following excerpt from his statement in an ELAN Press Release (my italics):

I have enjoyed working with my fellow directors since my appointment in December 2020, and I believe that the Company has established the right plan to create shareholder value through sustained cost discipline and developing its innovation pipeline. As the Company executes on its plan, I believe the market will come to appreciate the good work that is being done by management and the Board.

When I bought ELAT, I considered the worst case to be pocketing the interest payments during my holding period, converting at 1.5625 and waiting for a better selling opportunity. Here we are at the worst case.

For further details see:

Elanco's Tangible Equity Units: Living With The Worst Case