ELMD - Electromed: FY'23 SmartVest Sales Outpace Pessimistic Views Reiterate Buy For The Long-Term

2023-08-24 13:46:18 ET

Summary

- Electromed, Inc. (ELMD) reported strong Q4 and FY'22 sales and is still growing its SmartVest segment.

- The stock has rebounded from lows and broke resistance levels, adding to the potential for a turn.

- These factors combine with exceptional profitability on capital employed into the business, setting up for growth in intrinsic value.

- Net-net, reiterate buy, eyeing $17–$22 price band.

Investment Briefing

Electromed, Inc. ( ELMD ) posted its FY'23 annual numbers on August 22 with a strong beat at the top line and multiple inflection points from its SmartVest segment. It has successfully launched the next-gen SmartVest device and continues growing its top-line and post-tax earnings at a respectable clip.

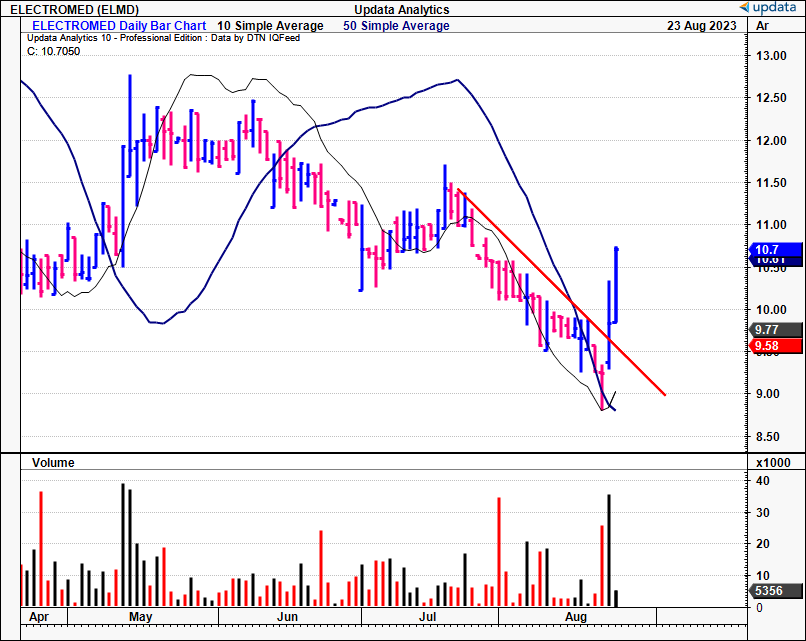

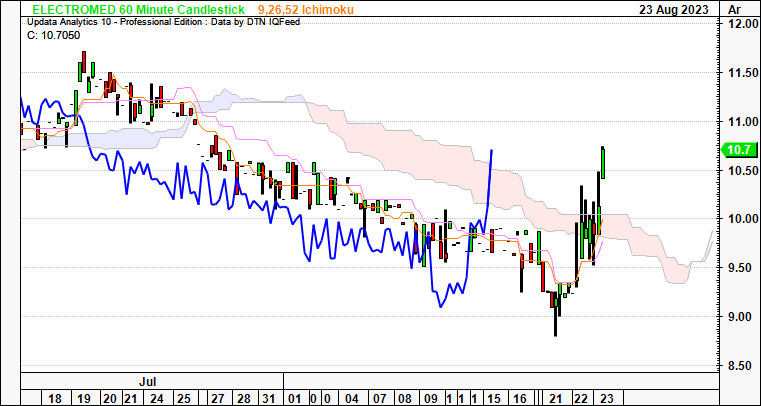

It's no secret the stock sold at major lows into August yet the full-year numbers have seen it catch a strong bid and break the longer term resistance line in the pre-market as I write [Figure 1]. New CEO Jim Cunniff is also at the helm and FY'24 will be the critical year to gauge his performance as the new skipper. Here I'll cover all of the moving parts in the ELMD investment debate and reiterate the buy thesis in doing so, keeping a long-term horizon in mind. Net-net, reiterate buy at $17–$22 share target band.

As a reminder, I've remained bullish on ELMD for the last 8 months or so, starting in December last year. The thesis is built on a simple set of economic levers:

- High-frequency chest wall oscillation, the major function in ELMD's SmartVest unit, is a differentiated offering that mimics the function of pulmonary Physiotherapists. The modality of treatment is well supported throughout the literature. The SmartVest unit, along with all similar offerings, provides patients with direct access to chest-wall Physiotherapy and has benefits to compliance and downstream to improved outcomes.

- ELMD employs a direct sales force to get in front of physicians and other referral sources, unlike competitors in the field who sell through distributors. This allows it to focus directly on productivity of its sales force, and do the heavy lifting itself in terms of driving sales.

- The company is also narrowing in on the bronchiectasis corner of the market, a currently under-served segment that has the potential to solve unmet medical needs. I performed a deep dive into this condition and the treatment market in the December publication.

- ELMD's performance to date, and forward expectations that are reiterated here today.

I'd encourage you to run over the previous publications to understand the broad thesis here and what's kept me on the long side of the account for this time. You can see them by clicking here , also here , and here .

Figure 1.

{kind=link}

Data: Updata

Key risks to investment

These risks must be realized by investors before proceeding any further:

- SmartVest sales are the major ingredient to ELMD's success. Should it fail to add more volumes to its sales register each year, this would impact the thesis.

- Broad macro-forces are also relevant here, and could hinder the firm's ability to get in front of hospitals or physicians if there is a broader economic downturn of large proportions.

- The healthcare sector has incurred a sharp selloff in H2 CY'23, and this could spillover into ELMD's equity stock.

- The presence of ELMD's competitors is also noted, and this could present a challenge in the dynamics for market share if ELMD slows its cadence and others increase their pace.

As mentioned, investors must realize these risks in full before considering any investment decisions regarding ELMD.

Critical facts underpinning buy thesis

A blend of fundamental and economic characteristics are central to the bullish thesis in my view. Investors will be wise to review our recent publication on Tactile Medical Systems ( TCMD ), a key competitor in high-frequency chest wall oscillation ("HFCWO") with its AffloVest segment. It competes directly with ELMD's SmartVest segment.

In that profile, I opined that TCMD faces several headwinds to growing its HFCWO offering. ELMD's offering looks to surpass these challenges in an idiosyncratic fashion in my informed opinion. The U.S. market for HFCWO was estimated at $250mm in 2022, and by all accounts can compound at 9% annually with label expansions and by offering treatment benefits to the core respiratory market.

Many of the "bears" on ELMD's equity stock have made wrong predictions on the cadence of SmartVest sales, along with rather questionable predictions on ELMD's overall sales trajectory without any raw data to back these up. It is now a matter of which firm can capture the most market share in the shortest amount of time and hold onto this.

1. Fundamental drivers

ELMD's Q4 sales were up ~21% YoY to $13.6mm. This brought full-year net revenues to $48.1mm, a 15.4% growth YoY [a reminder, ELMD posted its FY'23 full-year revenues, corresponding to Q3 CY'23] . Critically, this was above the 9% estimated growth rates, indicating ELMD captured additional market share this year.

The direct home care sales channel accounted for 91% of the top-line in FY '23, growing c.$6mm or 15.6% YoY to $43.9mm. Hospital revenues increased YoY 25.3% to $2.1mm, underscored by capital purchases and higher consumable volumes. Home care distributor revenue was also up ~10% to $1.6mm due to intensified demand from the primary home care distribution partner. It pulled the $48mm in sales to 76% gross, gaining ~50bps in margin on last year. Home care revenues were the major driver as well, propped by the Medicare allowable rate increase that was implemented in January 2023. Operating income was $4mm as reported, up 33% YoY and I've calculated ~30% of SG&A as investment vs. expenditure, and capitalized this onto the balance sheet as an intangible asset, to be amortized with a useful life of 7 years. Thus, adj. operating income was $13.48mm, and adj. EBITA of $14.5mm using this convention.

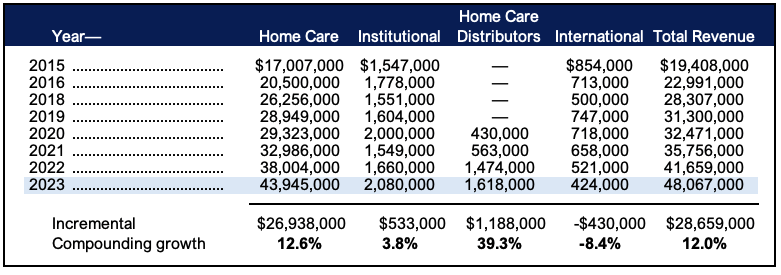

As to where this sits in the broad scheme of things, Figure 2 outlines the company's growth numbers spanning back to 2015. Only 2017 is missing from the data shown, but it incorporated into all calculations. It shows that:

- The firm has compounded sales growth at ~12.5% per year in home care and 12% overall since 2015.

- Critically, sales booked from home care distributors have grown at an annual ~39% rate since 2020. Combined, this lays the platform for a substantial wave of momentum heading into the new fiscal year.

- International sales have tracked down 8.4% geometrically over the years, but this isn't ELMD's main market. It is focused on U.S. sales, and thus stripping this out, you get to ~15% compounding growth rate in adjusted revenues from 2015–2023.

Figure 2.

{kind=link}

Data: BIG Insights, Company filings

Additional data from the facts pattern includes the following:

- As a reminder, TCMD sells its AffloVest units entirely through durable medical equipment ("DME") distributors. As such, it does not have a direct salesforce. This has proven to be a challenge of late, creating lumpiness in sales volumes, and strained relationships between purveyors. I believe this is a headwind in growing market share. Unlike TCMD, ELMD employs a direct sales force that concentrates on getting in front of physicians, clinicians, patients, and third-party payers while enhancing market awareness about the merits of HFCWO specifically for bronchiectasis treatment. This is another differentiator—ELMD's target on bronchiectasis. For a deep dive on bronchiectasis, its pathophysiology, the treatment market and so on, see my December 2022 publication on ELMD. This explains why the majority of its revenue is booked via home care sales through the physician referral model.

- Regarding the sales force, ELMD ended the year with 46 direct reps in the headcount. Average revenue per rep was thus $945,000/rep and at the higher end of forecasts. It is eyeing 54 sales reps by FY'24, and at a comparable basis, this would call for top-line sales of $51.3mm at the same productivity level, but I'd be looking towards ~$1.5mm/rep in the upside case, on the basis ELMD is also now targeting the top 1,000 prescribers of HFCWO as it launches its new SmartVest unit. This could give it a larger pool of physicians open up referral flow, and ultimately call for $81mm in sales on these assumptions.

- Further, ELMD is launching Clearway into hospitals as well. It has only begun this in Q1 FY'24, so no data from FY'23 to report on. But this feeds into the point above, expanding its market and opening up the patient pool further.

2. Economic characteristics, returns on capital deployed

No analysis on this channel is complete without rigorous analysis of the economic characteristics of ELMD's business. I've gone back to 2015 once again to extrapolate the long-term data and value creation.

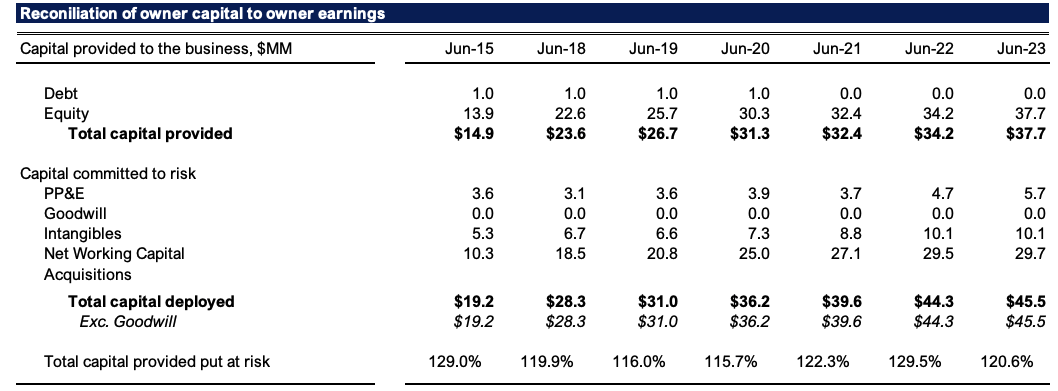

Figure 3 shows the capital investors have provided to ELMD relative to what's been put at risk into growing the business. The firm is all equity financed, with retained earnings flowing back into operational growth at the end of each year. A total of $37.7mm has been provided of which 120% of $45.5mm has been put at risk and deployed into operations. These are all core assets and ~$7.5mm in cash on hand. As mentioned earlier, I've capitalized ~30% of SG&A as investment vs. expenditure given the heavy investment into the headcount and marketing spend, with an amortization schedule of 7 years.

Figure 3.

{kind=link}

Data: BIG Insights, Company filings

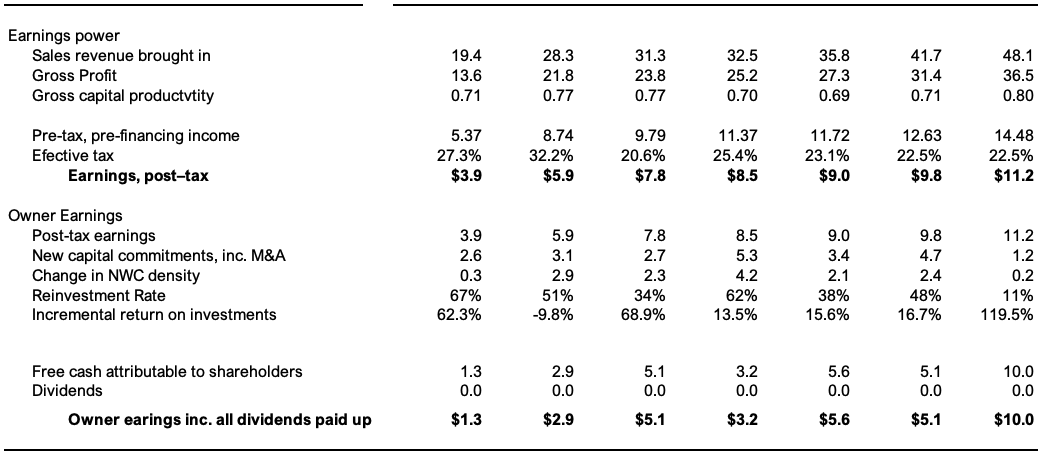

The $45.5mm in capital produces $11.2mm in adj. post-tax earnings, otherwise c.25% return on investment. More importantly, <$5mm in additional commitments were employed from 2021—2023 each year to grow the business, resulting in incremental returns of 15–120%. Net-net, considering the growth percentages outlined in section (1) of the report, ELMD still spun off $10mm in cash to its shareholders, all of which can be redeployed at the c.20–25% rates of return that's been in situ since 2015. With 1) higher sales momentum, and 2) continued earnings leverage, this could seriously ramp up profitability into the coming 2–5 years in my opinion.

Figure 4.

{kind=link}

Data: BIG Insights, Company filings

Critically, the company's productivity strengths are observed at the margin, with 23% of revenue booked as post-tax earnings. This, on capital turnover of ~1x, consistent with the firm's history. This tells me two things. One, it is employing cost differentiation in its pricing strategies, pricing its offerings slightly above market rates. Secondly, it implies ELMD enjoys consumer advantages, which fits the numbers and narrative surrounding its SmartVest momentum in FY'23. It also bodes well for the coming fiscal years. In addition, these rates are above long-term market return on capital of ~12%, and thus beat the hurdle in this instance. You can see the accretion in economic earnings ELMD has spun off each year below, pulling to $5.8mm in FY'23, ahead of its reported earnings of $3.2mm.

Figure 5.

{kind=link}

Data: BIG Insights, Company filings

Valuation

The company sells at 24x forward earnings and 12.5x forward EBITDA estimates, which are respective discounts to the sector at the time of writing (10% and 2%, respectively). It's also catching a bid at 1.8x trailing sales. These are attractive prices in my view, because they add to the asymmetrical upside that could be on offer if ELMD rates back to previous highs. Hence, in relative terms, I am attracted to ELMD at these valuations, although the calculus on intrinsic value discussed later is more central to my outlook on ELMD's valuation. Just want to make that clear.

Further, looking at short-term pricing studies, namely the cloud chart in Figure 6, the price line and lagging line have broken the cloud top with authority and now trade bullishly in my view. This is a critical juncture that implies more positive sentiment in its equity stock, and is absolutely integral to seeing a reversal in the longer-term trend, absolving the price risk.

Figure 6.

{kind=link}

Data: Updata

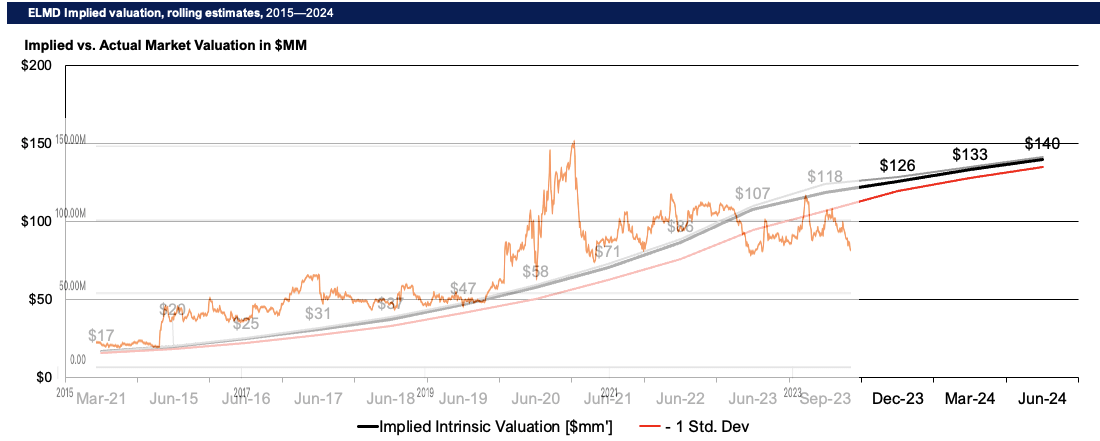

Furthermore, my market modelling and implied valuation estimates point to ELMD being undervalued at the point of this publication. The calculus is derived from the firm's returns on capital invested and the amount it has reinvested at these rates, to compound its intrinsic value. As a reminder—1) a positive spread in a firm's return on capital at risk and the hurdle rate is fundamental to value creation, and 2) a firm can compound its intrinsic value at the function of its ROIC and the reinvestment rate each year.

Applying this calculus to ELMD's equity line these past 9 years, you can see the market has been a fairly good judge of ELMD's intrinsic value over time, capturing the floor of implied market value each year. It has historically traded at a premium to intrinsic value estimates—something I'm happy to see. ELMD's market value has also reverted and bounced from this mark persistently over this time, bar the explosion of price in 2019, and the recent sluggish performance. This tells me of a high propensity to revert to the upside from here. I've got ELDM valued fairly at $14/share as I write, and $16.50 extending out to FY'24. In my upside case (not shown here) that sees $81mm in sales, 25% ROIC and ~70% reinvestment, I get to $22/share, in line with previous upside targets. I'm thus looking at 57–109% upside potential on the market price at the time of writing.

Figure 7.

{kind=link}

Source: BIG Insights, Seeking Alpha

In short

ELMD continues to display robust economic characteristics for patient and diligent investors who want long-term capital appreciation. It is recycling capital growth into additional profits over time. Around $45mm of capital produces $11mm in profits at present, otherwise 25% return on investments, in-line with historical range. Intelligent investors know that market returns typically mirror business returns over the long-run, thus, at these attractive rates ELMD is well-positioned to continue adding value for shareholders above the opportunity cost of capital. Added to this, actions taken by management and the new CEO in rolling out the next-gen SmartVest, beefing up the salesforce, and opening up the referral channels through physicians and hospitals are potential tailwinds in my opinion. Net-net, reiterate buy at target range of $17–$22/share.

For further details see:

Electromed: FY'23 SmartVest Sales Outpace Pessimistic Views, Reiterate Buy For The Long-Term